- Home

- »

- Next Generation Technologies

- »

-

Automotive Software Market Size & Share Report, 2026-2033GVR Report cover

![Automotive Software Market (2026 - 2033)Report]()

Automotive Software Market (2026 - 2033)

Size, Share & Trends Analysis Report By Application (ADAS & Safety, Infotainment, Navigation), By Vehicle Type (Passenger, Commercial Vehicles), By Product (OS, Middleware), By Propulsion Type, By Region, And Segment Forecasts

Market Size, 2025

$33.0BMarket Estimate, 2026

$37.4BMarket Forecast, 2033

$108.6BCAGR, 2026–2033

16.4%Automotive Software Market Summary

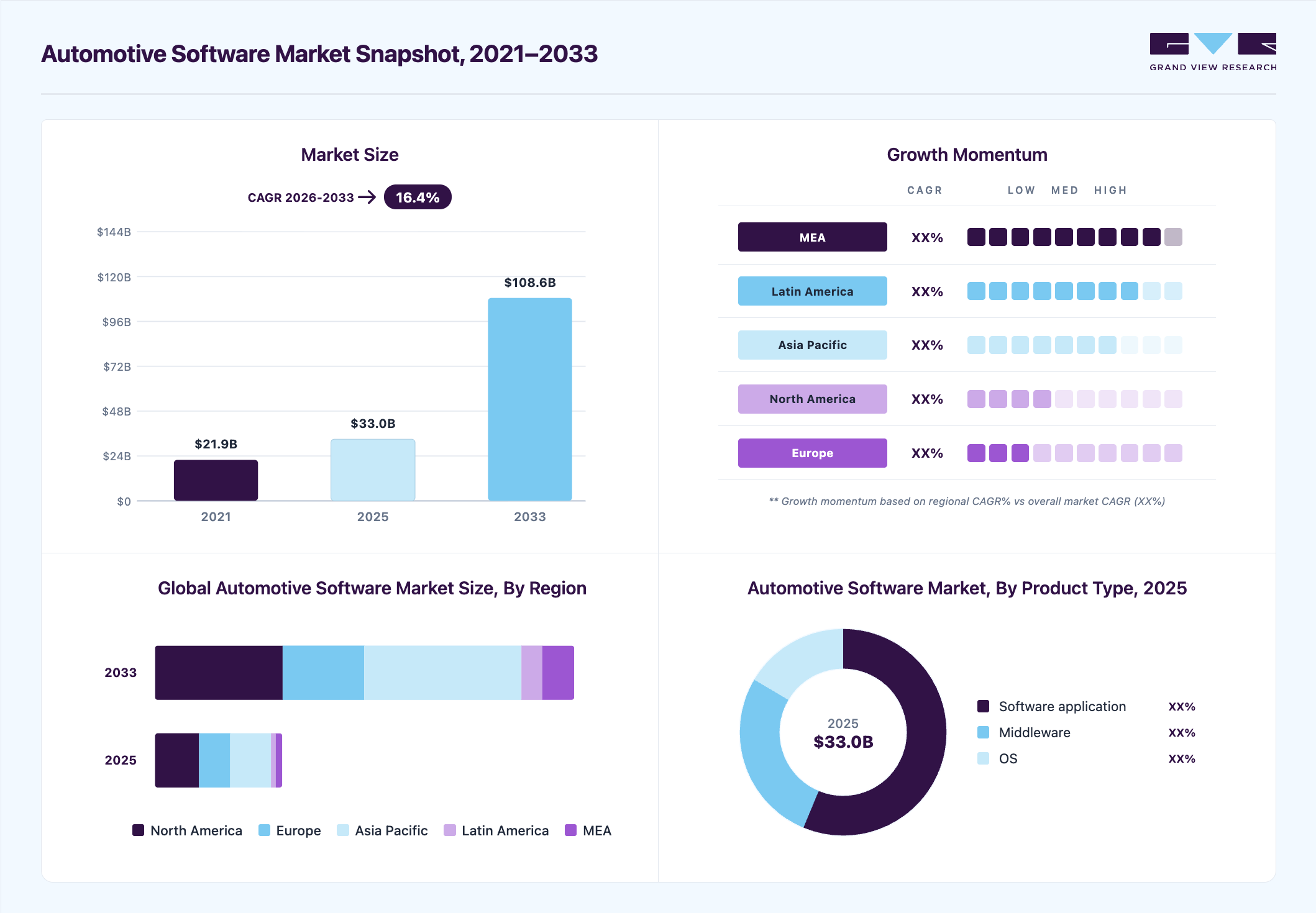

The global automotive software market size was valued at USD 33.0 billion in 2025 and is projected to grow from USD 37.4 billion in 2026 to USD 108.6 billion by 2033, at a CAGR of 16.4% from 2026 to 2033. North America dominated the market with the largest revenue share of 34.6% in the global market in 2025. Automotive software refers to a set of programmable instructions designed for computer-based in-vehicle applications.

Key Market Trends & Insights

- By application: ADAS & safety segment held the largest market share of 21.0% in 2025.

- By product: Software application segment held the largest market share of 56.0% in 2025.

- By vehicle type: Passenger cars segment held the largest market share of 77.0% in 2025.

- By propulsion type: Internal combustion engine segment held the largest market share in 2025.

Regional Highlights

- Largest regional market: North America (34.6% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

- By country: The U.S. held the largest market share in 2025.

Market Size & Forecast

- Market size in 2025: USD 33.0 Billion

- Estimated market size in 2026: USD 37.4 Billion

- Projected market size by 2033: USD 108.6 Billion

- CAGR (2026-2033): 16.4%

These automotive software are essential to the embedded systems of vehicles and encompass functions like body control, infotainment, telematics, comfort, safety features, Advanced Driver Assistance Systems (ADAS), and communication applications. The rising demand for car-to-car communication is expected to drive the global industry over the forecast period.Passenger cars dominate the market primarily due to the increasing integration of advanced software technologies aimed at improving safety, connectivity, and overall driving experience. Automakers are actively incorporating features such as advanced driver assistance systems (ADAS), infotainment platforms, and connected vehicle capabilities in passenger vehicles to enhance user convenience and vehicle performance. The growing consumer demand for comfort, safety, and smart mobility solutions has further accelerated the adoption of automotive software in passenger cars.

")

Modern passenger vehicles are increasingly equipped with connectivity features such as 4G/5G, Wi-Fi, and over-the-air (OTA) update capabilities to support real-time navigation, remote diagnostics, and in-vehicle entertainment systems. Additionally, the rapid development of autonomous and semi-autonomous driving technologies in passenger cars requires sophisticated software for sensor integration, object detection, and vehicle control systems, further driving the growth of automotive software in this segment

Application Insights

The ADAS & safety segment dominated the global automotive software industry and accounted for a revenue share of over 21.04% in 2025. There is a growing focus on safety in the automotive industry, with customers and regulators moving towards safer vehicles. ADAS technologies play a vital role in improving vehicle safety with features like lane-keeping assistance, adaptive cruise control, and collision avoidance. Additionally, customers are increasingly seeking autonomous vehicles with advanced safety features such as ADAS technologies, which are instrumental in reducing the number of accidents and improving road safety.

The connectivity segment is expected to experience the fastest CAGR from 2026 to 2033. Connectivity has become an extensive feature across various electronic devices, including automobiles. These services enable automotive dealers, fleet operators, and drivers to enhance resource utilization, strengthen safety, automate specific driver functions, and simultaneously gather valuable data related to vehicle performance and road conditions. Connectivity enables vehicles to optimize resource usage, such as fuel, by providing real-time data on traffic conditions and suggesting more efficient routes. It also facilitates predictive maintenance, helping vehicles to remain in optimal working condition.

Vehicle Type Insights

Passenger cars held the largest revenue share of this market in 2025. Passenger cars have seen higher adoption of software services compared to commercial vehicles, as passenger cars often come equipped with advanced infotainment systems, driver assistance technologies such as ADAS, and connected services, making them a significant market for automotive software. Countries where the automotive industry is more mature have a robust demand for highly advanced applications. Customers in these regions increasingly strive for vehicles with features such as ADAS, which enhance safety and convenience.

The commercial vehicle segment is projected to grow at the fastest CAGR during the forecast period. The commercial vehicle industry is subject to many regulations, such as those related to safety, emissions, and driver hours. Software solutions help commercial vehicle operators track and ensure compliance with these regulations, which has become increasingly important in many regions. Furthermore, automotive software assists commercial vehicle operators in reducing fuel consumption, maintenance costs, and downtime. These cost-saving benefits have driven the adoption of software solutions in the commercial vehicle industry.

Product Insights

The software application segment dominated the market in 2025. Software applications play a critical role in enabling vehicle connectivity and telematics services, including remote vehicle diagnostics, real-time traffic information, and software updates. Also, modern vehicles have become highly complex, integrating various Electronic Control Units (ECUs) and sensors. Software applications are essential for managing and coordinating these components, enabling features like infotainment, navigation, engine control, and ADAS.

The operating system (OS) segment is projected to grow at the fastest CAGR during the forecast period. Automotive OS serves as the foundational software platform for the vehicle's electronic control units and various sub-systems. These operating systems provide the essential framework for coordinating and managing different functions, from powertrain control to infotainment. Modern vehicles require operating systems that can handle safety-critical functions, such as autonomous driving features. These functions demand a high level of reliability and real-time responsiveness, which a specialized automotive OS provides.

Propulsion Type Insights

The internal combustion engine (ICE) segment dominated the market in 2025. As the automotive industry is rapidly moving toward electrification and autonomous driving, a significant part of the global vehicle fleet still includes ICE vehicles. These vehicles require software for engine management, emission control, transmission control, and other crucial functions. Furthermore, many developing economies continue to rely heavily on ICE vehicles. This diversity in regional markets contributes to the dominance of the ICE segment.

The electric vehicle (EV) segment is expected to witness the fastest CAGR during the forecast period. Increased awareness regarding environmental issues, notably climate change and air pollution, has led to a shift toward cleaner transportation alternatives. Moreover, ongoing advancements in battery technology have resulted in an increased EV range, faster charging times, and reduced costs. These advancements have made EVs more practical and appealing to a wider range of consumers.

Regional Insights

North America automotive software market dominated the industry with a revenue share of 34.62% in 2025 and is projected to grow at a significant CAGR over the forecast period. The region has a well-established and robust automotive industry, with a large number of automakers, suppliers, and technology companies. This industry strength drives innovation and the development of software solutions for vehicles. Furthermore, North America is a significant market for EVs and autonomous vehicles. Both segments heavily rely on software for powertrain control, battery management, autonomous driving features, and connectivity, which propels the growth of the market in the region.

U.S. Automotive Software Market Trends

The automotive software market in the U.S. dominated the regional industry in 2025. The U.S. consumers and regulators are increasingly prioritizing vehicle safety, leading to high adoption of ADAS features such as lane departure warnings, automatic emergency braking, and adaptive cruise control. Moreover, regulatory bodies such as the National Highway Traffic Safety Administration (NHTSA) continue to encourage the integration of ADAS, pushing automotive software development in this country.

Europe Automotive Software Market Trends

The automotive software market in Europe is expected to experience a CAGR of over 13% during the forecast period. The European Union's Road Safety and Environmental Goals have mandated more safety features and lower emissions, leading to increased investment in software solutions for vehicle systems such as Advanced Driver Assistance Systems (ADAS) and eco-driving technologies. Moreover, EU Green Deal initiatives and regulations are pushing automakers to shift toward electric mobility, thus increasing the need for EV-specific software solutions.

Asia Pacific Automotive Software Market Trends

The automotive software market in Asia Pacific is expected to experience a CAGR of 18.7% during the forecast period. The substantial technological progress witnessed in this region plays a key role in driving the surging demand for automotive software in the region. Furthermore, the growing embrace of technological innovations has further propelled the demand for automotive software solutions. The region has a substantial and growing population, which provides a large customer base for automotive manufacturers and is expected to fuel the growth of the automotive software industry.

Key Automotive Software Company Insights

Some key companies in the automotive software market include Robert Bosch GmbH and Continental AG, and others. These two companies play a crucial role in the automotive software industry by developing advanced driver assistance systems (ADAS), autonomous driving solutions, and connected vehicle software.

-

Robert Bosch GmbH offers one of the most comprehensive automotive software portfolios, covering everything from powertrain solutions to telematics, safety, and cybersecurity. Its offerings address a wide range of automotive needs, positioning it as a one-stop shop for OEMs.

-

Continental AG focuses on embedded and connected software solutions essential for modern automotive functions like infotainment, OTA (over-the-air) updates, and cybersecurity. The company develops scalable, high-performance software that has made them integral to next-generation, software-defined vehicles.

Key Automotive Software Companies:

The following key companies have been profiled for this study on the automotive software market.

- Amazon Web Services, Inc.

- Aptiv

- BlackBerry Limited

- Continental AG

- Cox Automotive

- Dassault Systemes

- NVIDIA Corporation

- Robert Bosch GmbH

- Siemens

- Sonatus, Inc.

Recent Developments

-

In January 2025, Amazon Web Services (AWS) collaborated with Valeo to accelerate the development of software-defined vehicles (SDVs) using cloud-based development and validation tools. The partnership enables automakers to build, test, and deploy distributed vehicle software stacks, including Advanced Driver Assistance Systems (ADAS), infotainment, and autonomous mobility features, more efficiently through AWS cloud infrastructure and AI capabilities

-

In September 2024, SDVerse, an automotive software provider for B2B businesses, launched the B2B Automotive Software Marketplace, a software-defined vehicle. The marketplace provides robust matchmaking features and product discovery, allowing vendors to display their software capabilities while enabling buyers to search, communicate securely, compare products side by side, and choose the most suitable software products to fulfill their requirements.

-

In March 2024, Arm Limited, an automotive technology company, launched Armv9-based technologies, integrated into the automotive sector, allowing the industry to harness the advanced AI, security, and virtualization features of this latest generation of Arm architecture. The company introduced new Arm Automotive Enhanced (AE) processors, which combine advanced Armv9 technology with server-class performance, offering significant benefits for AI-driven applications in automotive use cases.

-

In March 2024, General Motors collaborated with Wipro Limited, a technology services company, and Magna International Inc., an automotive supplier, to develop SDVerse, a B2B sales platform for automotive software. This platform is designed to transform the sourcing and procurement process for automotive software by offering a matchmaking hub for buyers and sellers of embedded automotive software.

Automotive Software Market Report Scope

Report Attribute

Details

Market size in 2025

USD 33.0 billion

Estimated Market size in 2026

USD 37.4 billion

Projected Market size by 2033

USD 108.6 billion

Growth rate

CAGR of 16.4% from 2026 to 2033

Base year estimation

2025

Actual data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Application, vehicle type, product, propulsion type, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; Germany; UK; France; China; India; Japan; Australia; South Korea; Brazil; UAE; South Africa; KSA

Key companies profiled

Amazon Web Services, Inc.; Aptiv; BlackBerry Limited; Continental AG; Cox Automotive; Dassault Systemes; NVIDIA Corporation; Robert Bosch GmbH; Siemens; Sonatus, Inc.

Customization scope

Free report customization (equivalent to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Automotive Software Market Report Segmentation

This report forecasts revenue growth at the global, regional and country levels and provides an analysis of the latest trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global automotive software market report based on application, vehicle type, product, propulsion type, and region:

-

Application Outlook (Revenue, USD Million, 2021 - 2033)

-

ADAS & Safety

-

Infotainment

-

Navigation

-

Autonomous Driving

-

Engine & Transmission

-

Smart Diagnostics & Predictive Maintenance

-

In-car Voice Assistance

-

Connectivity

-

Others

-

-

Vehicle Type Outlook (Revenue, USD Million, 2021 - 2033)

-

Passenger Vehicles

-

Commercial Vehicles

-

-

Product Outlook (Revenue, USD Million, 2021 - 2033)

-

OS

-

Middleware

-

Software Application

-

-

Propulsion Type Outlook (Revenue, USD Million, 2021 - 2033)

-

ICE

-

EV

-

-

Regional Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

UK

-

Germany

-

France

-

-

Asia Pacific

-

China

-

India

-

Japan

-

Australia

-

South Korea

-

-

Latin America

-

Brazil

-

-

Middle East and Africa

-

UAE

-

KSA

-

South Africa

-

-

Frequently Asked Questions About This Report

Asia Pacific is the fastest-growing region over the forecast period.

Some key players operating in the automotive software market include Amazon Web Services, Inc.; Aptiv; BlackBerry Limited; Continental AG; Cox Automotive; Dassault Systemes; NVIDIA Corporation; Robert Bosch GmbH; Siemens; and Sonatus, Inc.

Key factors that are driving the automotive software market growth include the rising demand for car-to-car communication, and advancements in autonomous vehicles.

North America dominated with a revenue share of 34.6% in 2025.

The global automotive software market size was valued at USD 33.0 billion in 2025 and is projected to reach USD 37.4 billion in 2026.

The global automotive software market is expected to grow at a CAGR of 16.4% from 2026 to 2033, reaching USD 108.6 billion.

The ADAS & safety segment led with a 21.0% revenue share in 2025, while connectivity is the fastest-growing segment.

The software application segment held the market with the largest revenue share of 56.0% in 2025, while operating systems is the fastest-growing segment.

The passenger cars segment held the market with the largest revenue share of 77.0% in 2025, while commercial vehicles is the fastest-growing segment.

About the Author(s)

Next Generation Technologies Research Team

Technology · Next Generation TechnologiesThis report was authored by the next generation technologies research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the next generation technologies segment of the technology industry. All findings are based on proprietary technology databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.