- Home

- »

- Plastics, Polymers & Resins

- »

-

Beverage Closures Market Size, Growth Report, 2026-2033GVR Report cover

![Beverage Closures Market (2026 - 2033)Report]()

Beverage Closures Market (2026 - 2033)

Size, Share & Trends Analysis Report By Material (Plastic, Metal), By Beverage Category (Water, Carbonated Soft Drink (CSD), Alcoholic, Juice), By Packaging Format (Plastic Bottles, Glass Bottles, Cans, Cartons), By Region, And Segment Forecasts

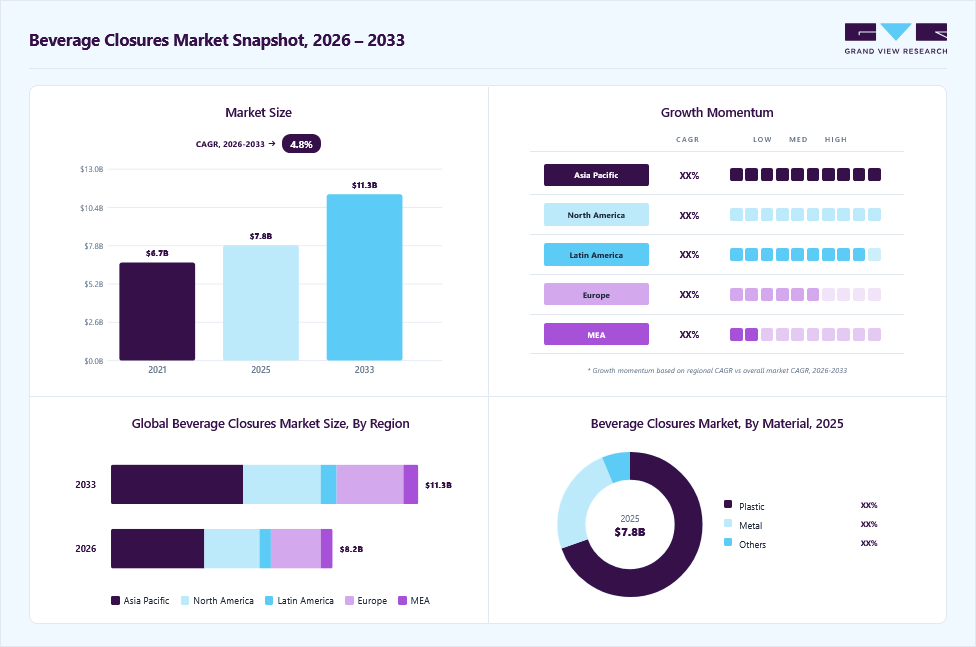

Market Size, 2025

$7.8BMarket Estimate, 2026

$8.2BMarket Forecast, 2033

$11.3BCAGR, 2026–2033

4.8%Beverage Closures Market Summary

The global beverage closures market size was valued at USD 7.8 billion in 2025 and is projected to grow from USD 8.2 billion in 2026 to USD 11.3 billion by 2033, at a CAGR of 4.8% from 2026 to 2033. Asia Pacific dominated the global market, accounting for the largest revenue share of 42.0% in 2025. Rising global consumption of bottled water, carbonated drinks, juices, dairy beverages, and ready-to-drink products is driving demand for reliable, tamper-evident, and convenience-oriented beverage closures across plastic, metal, and carton packaging formats.

Key Market Trends & Insights

- By material: Plastic segment is anticipated to expand at a CAGR of 5.0% from 2026 to 2033 in revenue terms.

- By beverage category: Water segment is forecast to grow at a CAGR of 5.2% from 2026 to 2033 in terms of revenue.

- By packaging format: Plastic bottles segment is expected to witness a CAGR of 5.1% from 2026 to 2033 in revenue terms.

Regional Highlights

- Largest regional market: Asia Pacific (42.0% revenue share, 2025)

- By country: The China beverage closures industry is a major contributor to the global market.

Market Size & Forecast

- Market size in 2025: USD 7.8 Billion

- Estimated market size in 2026: USD 8.2 Billion

- Projected market size by 2033: USD 11.3 Billion

- CAGR (2026-2033): 4.8%

Growth in premiumization, on-the-go lifestyles, and sustainability trends is further accelerating innovation in lightweight, resealable, recyclable, and high-performance closures that enhance user experience and brand differentiation.

Expanding demand for packaged water, carbonated soft drinks, juices, dairy beverages, sports drinks, and ready-to-drink teas and coffees has directly increased the need for reliable closure systems across plastic bottles, glass containers, cartons, and metal cans. Urbanization, changing lifestyles, and growing on-the-go consumption patterns are encouraging smaller, portable, and convenience-oriented packaging formats that depend heavily on easy-open, resealable, and tamper-evident closures. In emerging economies, improving retail penetration and increasing disposable incomes are further accelerating packaged beverage sales, creating sustained volume demand for closures.

")

Product innovation and premiumization trends are also significantly supporting industry expansion. Beverage producers are increasingly using closures not only for sealing but also for branding, differentiation, consumer convenience, and product integrity. Demand is rising for lightweight caps, sports caps, tethered closures, dispensing closures, child-resistant formats for functional drinks, and premium metal closures for alcoholic beverages. Moreover, growth in health-focused and functional beverage categories such as protein drinks, probiotic beverages, plant-based drinks, and nutraceutical beverages requires specialized closures that preserve freshness, carbonation, hygiene, and shelf life. As brands compete for shelf appeal and user experience, closure design has become an important packaging value driver.

Sustainability regulations and circular packaging initiatives are creating a new wave of demand transformation in the beverage closures industry. Governments and brand owners are increasingly promoting recyclable, lightweight, and attached-cap solutions to reduce litter and improve collection rates. This is pushing manufacturers to invest in recycled-content closures, mono-material designs, bio-based resins, and high-efficiency production technologies. Furthermore, beverage filling companies are modernising high-speed bottling lines, increasing demand for precision-engineered closures that support automation, leak prevention, and consistent application performance. The combination of environmental compliance, operational efficiency, and packaging innovation continues to strengthen long-term growth prospects for the beverage closures industry.

Market Concentration & Characteristics

The beverage closures industry is characterized by high-volume manufacturing, consistent repeat demand, and close linkage to beverage packaging output across water, soft drinks, dairy beverages, juices, alcoholic drinks, and ready-to-drink products. Demand is relatively stable because closures are essential consumable components required for every packaged beverage unit produced. The market therefore benefits from recurring orders, long-term supply contracts, and predictable replacement cycles tied to beverage consumption trends. Seasonal spikes may occur during summer months, festive periods, or promotional campaigns, but overall demand is driven by population growth, urbanization, and packaged beverage penetration.

The industry is highly technology- and quality-driven, as closures must meet strict performance standards related to sealing integrity, tamper evidence, carbonation retention, food safety, leak prevention, and compatibility with high-speed filling lines. Manufacturers rely on injection molding, compression molding, metal forming, and liner technologies supported by automation and precision tooling. Product customization is common, with beverage brands requesting specific colors, embossing, printing, opening torque, and dispensing features. Because closures directly affect user experience and product freshness, reliability and consistency are major competitive differentiators.

Material Insights

The plastic segment dominated the market in 2025 with a 69.6% revenue share due to its low cost, lightweight nature, and compatibility with high-speed beverage filling lines across water, carbonated drinks, juices, and dairy products. Plastic closures, especially polypropylene and polyethylene caps, offer strong sealing performance, resealability, tamper evidence, and design flexibility for multiple bottle formats. Their large-scale availability, efficient mass production, and growing use of recyclable lightweight designs further strengthened adoption among beverage manufacturers worldwide.

The metal segment held a significant share of the market due to its superior barrier protection, durability, and premium appearance, making it widely used for alcoholic beverages, glass bottled soft drinks, and specialty drinks. Metal closures, such as crown caps, screw caps, and aluminum roll-on closures provide strong sealing performance, carbonation retention, and longer shelf life. Demand is also supported by the recyclability of aluminum and steel, which aligns with sustainability goals and premium packaging trends.

Packaging Format Insights

The plastic bottles segment accounted for 56.4% of the market in 2025 due to the widespread global use of PET and HDPE bottles for packaged water, carbonated soft drinks, juices, dairy beverages, and edible liquid products. Plastic bottles are lightweight, shatter-resistant, cost-efficient, and easy to transport, making them highly preferred by beverage producers and retailers. Their compatibility with screw caps, sports caps, and tamper-evident plastic closures further accelerated large-scale adoption across mass-market beverage categories.

The glass bottles segment held a notable share of the market due to strong demand from alcoholic beverages, premium soft drinks, juices, and specialty beverages, where product image and quality perception are important. Glass offers excellent barrier properties, preserves taste, and supports longer shelf life, making it suitable for sensitive or carbonated beverages. Its compatibility with crown caps, metal screw caps, corks, and premium closures also supports continued use in value-added packaging segments.

Beverage Category Insights

The water segment dominated the market in 2025, accounting for 35.7% of total market share, due to the massive global consumption of bottled drinking water across residential, commercial, and on-the-go channels. Rising health awareness, concerns over water quality, urbanization, and growing travel convenience needs have significantly increased demand for packaged water. High production volumes of PET water bottles using standard screw caps and tamper-evident closures further strengthened this segment’s leadership.

The carbonated soft drink (CSD) segment held a significant share of the market due to high global consumption of cola, flavored sodas, and sparkling beverages across retail and foodservice channels. These products require specialized closures with strong sealing strength and carbonation retention to maintain pressure, freshness, and shelf life. Large production volumes in PET bottles, cans, and glass bottles continue to generate steady demand for closure systems worldwide.

Regional Insights

Asia Pacificbeverage closures industry dominated the global market in 2025 due to its large population base, rapid urbanization, and rising consumption of packaged water, soft drinks, dairy beverages, and ready-to-drink products. Strong beverage manufacturing capacity in countries such as China, India, Japan, and Indonesia, along with expanding retail distribution networks, supported high closure demand. Cost-competitive packaging production, growing disposable incomes, and increasing demand for convenience beverages further strengthened the region’s market leadership.

North America Beverage Closures Market Trends

North America beverage closures industry held a significant share of the global market in 2025 due to high per capita consumption of bottled water, carbonated drinks, alcoholic beverages, and functional beverages. The region benefits from a mature beverage packaging industry, advanced bottling infrastructure, and strong demand for premium, resealable, and convenience-oriented closure formats. Sustainability initiatives, recycled material adoption, and continuous packaging innovation further supported market growth.

U.S. Beverage Closures Market Trends

TheU.S. beverage closures industry accounted for a major share of the North American market in 2025 due to its large packaged beverage industry and high consumption of bottled water, soft drinks, energy drinks, beer, and ready-to-drink beverages led by brands such as The Coca-Cola Company, PepsiCo, Keurig Dr Pepper, and Anheuser-Busch. Strong packaging demand is supported by closure suppliers including AptarGroup, Silgan Holdings, Amcor plc, and O.Berk Company. Sustainability regulations, lightweight cap innovation, and growth in recycled-content packaging further strengthened the U.S. market position.

Europe Beverage Closures Market Trends

Europe beverage closures industry held a notable share of the market in 2025 due to strong demand for bottled water, carbonated drinks, beer, wine, dairy beverages, and premium packaged products across countries such as Germany, France, Italy, and United Kingdom. The region has an advanced beverage packaging industry supported by companies such as Guala Closures, Corvaglia Group, and Closure Systems International, driving innovation in tethered caps, lightweight closures, and premium metal closures. Strict sustainability regulations, recycling targets, and preference for high-quality packaging further supported regional market growth.

Key Beverage Closures Company Insights

The beverage closures industry is fragmented, with numerous global, regional, and local manufacturers competing across plastic caps, metal closures, sports caps, and specialty sealing formats. Large companies such as AptarGroup, Amcor plc, Silgan Closures, Guala Closures, and Corvaglia Group hold notable positions, a substantial share of demand is served by regional molders and domestic packaging suppliers. Competition is driven by price efficiency, customization, short lead times, and the ability to meet beverage brand specifications for sealing performance and design. Innovation in lightweight, tethered, and recyclable closures is becoming an important differentiator, while local players remain competitive through flexible production and proximity to bottling facilities.

-

In November 2025, Corvaglia Group partnered with Wisecap Group to expand beverage closure production across Europe. Wisecap integrated Corvaglia’s manufacturing network in Italy, Spain, the Czech Republic, Poland, and Egypt, while Corvaglia retained a minority stake and supplied injection-molding technology. The partnership improves supply security, production flexibility, and innovation for European beverage customers.

-

In April 2025, Amcor plc completed its all-stock acquisition of Berry Global Inc, creating a global packaging leader with around 400 facilities, 75,000 employees, and operations in 140 countries. The merger, valued at approximately USD 13.0 billion, enhances Amcor's portfolio with expanded material science and innovation capabilities, positioning it to deliver more consistent growth and improved margins.

-

In April 2024, Phoenix Closures, Inc. inaugurated the Firebird Design and Innovation Center at its national headquarters in Aurora, Illinois. The state-of-the-art facility supports the complete closure development process from concept and prototyping to validation and production, reinforcing the company’s customer-centric approach to delivering high-quality packaging solutions.

Key Beverage Closures Companies:

The following key companies have been profiled for this study on the beverage closures market.

- Amcor plc

- AptarGroup, Inc.

- Moulded Packaging Solutions Limited

- Closure Systems International

- Guala Closures

- Corvaglia Group

- Siligan Closures

- ALPLA

- UNITED CAPS

- MRP Solutions

- Blackhawk Molding Co. Inc.

- Phoenix Closures, Inc.

- Reliable Caps, LLC

Beverage Closures Market Report Scope

Report Attribute

Details

Market size in 2025

USD 7.8 billion

Estimated Market size in 2026

USD 8.2 billion

Projected Market size by 2033

USD 11.3 billion

Growth rate

CAGR of 4.8% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Material, packaging format, beverage category, region

Regional Scope

North America; Europe; Asia Pacific; Latin America; Middle East & Africa

Key companies profiled

Amcor plc; AptarGroup, Inc.; Moulded Packaging Solutions Limited; Closure Systems International; Guala Closures; Corvaglia Group; Siligan Closures; ALPLA; UNITED CAPS; MRP Solutions; Blackhawk Molding Co. Inc.; Phoenix Closures, Inc.; Reliable Caps, LLC

Customization scope

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail of customized purchase options to meet your exact research needs. Explore purchase options

Global Beverage Closures Market Report Segmentation

This report forecasts revenue growth at the regional and country levels and provides an analysis on the latest industry trends and opportunities in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the beverage closures market report based on material, packaging format, beverage category, and region:

-

Material Outlook (Revenue, USD Million, 2021 - 2033)

-

Plastic

-

Metal

-

Others

-

-

Packaging Format Outlook (Revenue, USD Million, 2021 - 2033)

-

Plastic Bottles

-

Glass Bottles

-

Cans

-

Cartons

-

Others

-

-

Beverage Category Outlook (Revenue, USD Million, 2021 - 2033)

-

Water

-

Carbonated Soft Drink (CSD)

-

Alcoholic

-

Juice

-

Others

-

-

Regional Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

France

-

UK

-

Italy

-

Spain

-

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

Australia

-

-

Latin America

-

Brazil

-

Argentina

-

-

Middle East & Africa

-

Saudi Arabia

-

UAE

-

South Africa

-

-

Frequently Asked Questions About This Report

The global beverage closures market size was valued at USD 7.8 billion in 2025 and is estimated at USD 8.2 billion for 2026.

The global beverage closures market is expected to grow at a CAGR of 4.8% from 2026 to 2033, reaching USD 11.3 billion by 2033.

The water segment emerged as the largest contributor to the beverage closures market in 2025, capturing 35.7% of overall market share, and is anticipated to expand at a CAGR of 5.2% during 2026 to 2033 in revenue terms.

Key players include Amcor plc; AptarGroup, Inc.; Moulded Packaging Solutions Limited; Closure Systems International; Guala Closures; Corvaglia Group; Siligan Closures; ALPLA; UNITED CAPS; MRP Solutions; Blackhawk Molding Co. Inc.; Phoenix Closures, Inc.; Reliable Caps, LLC.

Rising global consumption of bottled water, carbonated drinks, juices, dairy beverages, and ready-to-drink products is driving demand for reliable, tamper-evident, and convenience-oriented beverage closures across plastic, metal, and carton packaging formats.

Asia Pacific dominated with a 42.0% revenue share in 2025.

The plastic segment led with a 69.6% revenue share in 2025.

Plastic bottles segment dominated the market and accounted for the largest revenue share of 56.4% in 2025.

About the Author(s)

Plastics, Polymers & Resins Research Team

Bulk Chemicals · Plastics, Polymers & ResinsThis report was authored by the plastics, polymers & resins research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the plastics, polymers & resins segment of the bulk chemicals industry. All findings are based on proprietary bulk chemicals databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.