- Home

- »

- Plastics, Polymers & Resins

- »

-

Caps And Closures Market Size & Share Report, 2026-2033GVR Report cover

![Caps And Closures Market (2026 - 2033)Report]()

Caps And Closures Market (2026 - 2033)

Size, Share & Trends Analysis Report By Material (Plastic, Metal), By Product (Dispensing Caps, Screw Closures, Crown Closures, Aerosol Closures), By Application, By Region, And Segment Forecasts

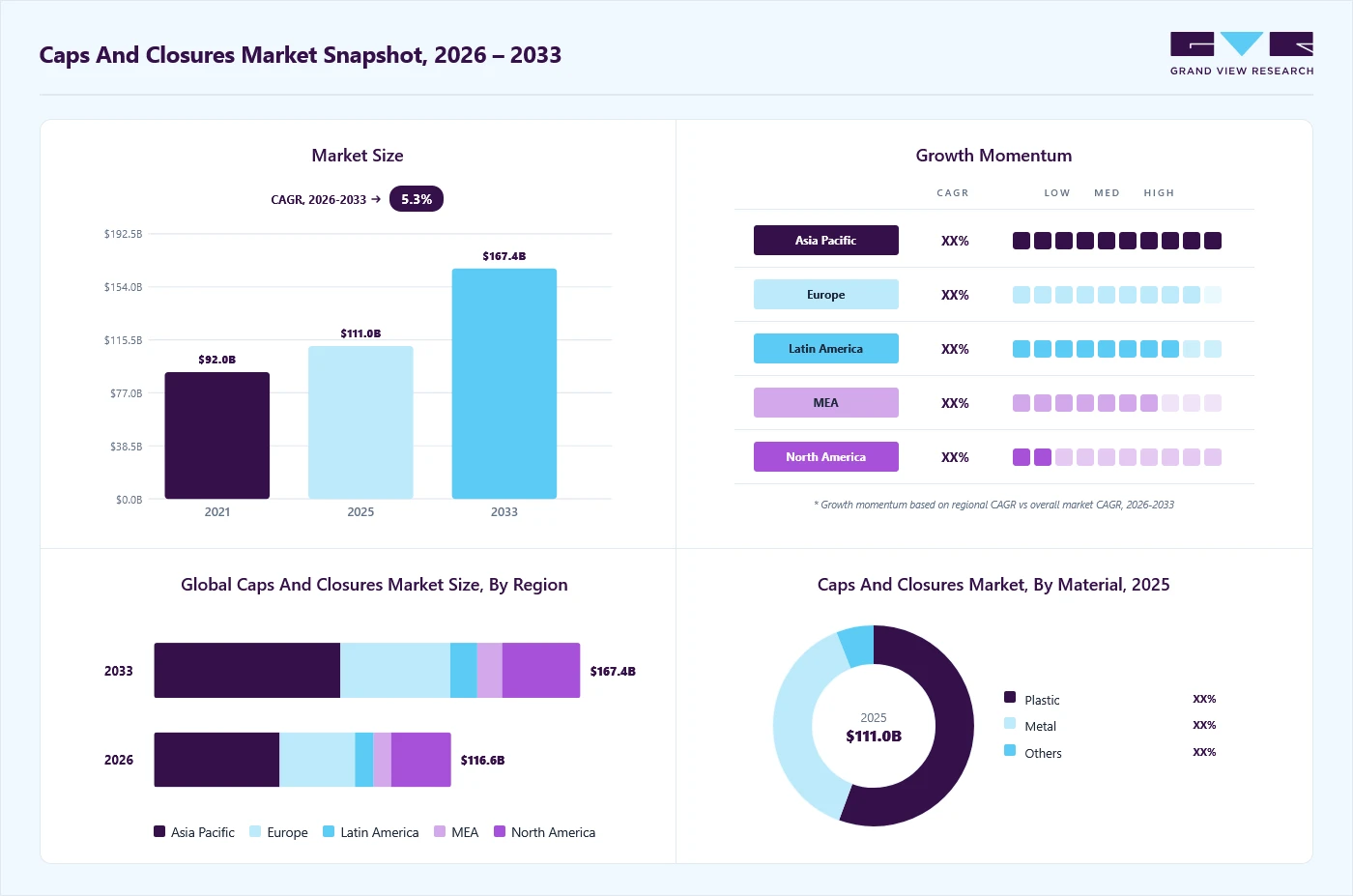

Market Size, 2023

$111.0BMarket Estimate, 2026

$116.6BMarket Forecast, 2033

$167.4BCAGR, 2024–2033

5.3%Caps And Closures Market Summary

The global caps and closures market size was valued at USD 111.0 billion in 2025 and is projected to grow from USD 116.6 billion in 2026 to USD 167.4 billion by 2033, at a CAGR of 5.3% from 2026 to 2033. The market in Asia Pacific dominated with a revenue share of 42.1% in 2025. The growing demand for various food products and alcoholic and non-alcoholic beverages is anticipated to drive market growth.

Key Market Trends & Insights

- By application: Food segment held the largest market share of 26.5% in 2025.

- By material: Plastics segment held the largest market share of 55.6% in 2025.

- By product: Dispensing caps segment held the largest market share of 35.3% in 2025.

Regional Highlights

- Largest regional market: Asia Pacific (42.1% revenue share, 2025)

- By country: China held the largest market share in 2025

Market Size & Forecast

- Market size in 2025: USD 111.0 Billion

- Estimated market size in 2026: USD 116.6 Billion

- Projected market size by 2033: USD 167.4 Billion

- CAGR (2026-2033): 5.3%

Caps and closures act as barriers, preventing packaged contents from exposure to ambient air and dust particles, while allowing easy dispensing. Caps and closures are used in several other end-use industries, including healthcare, personal care, home care, and automotive. Rising awareness about the benefits of healthy eating is likely to boost the demand for dietary supplements, which in turn is expected to further drive demand for packaging products.")

Council for Responsible Nutrition (CRN), a leading trade association representing dietary supplement and functional food manufacturers and ingredient suppliers in the U.S., conducted a consumer survey in 2023 on dietary supplements, wherein multivitamins were consumed by 70% of participants, followed by specialty supplements such as omega-3s, melatonin, probiotics, and fiber used by 52 % of participants. In addition, the sports nutrition supplements segment witnessed a 5% increase in consumption compared to previous years. All these factors are anticipated to drive the demand for market growth.

Increasing demand for caps and closures is closely associated with the rise of urbanization in the U.S. Consumers in urban areas prefer packaging solutions that are convenient and suitable for on-the-go consumption of food and beverages. Caps and closures play a vital role in providing this convenience by ensuring easy opening and closing of products and preventing spills. In addition, they create an airtight seal that keeps the products fresh for a longer period by preventing the entry of bacteria. These address the growing concerns about safety and hygiene associated with food and beverage products, as they help prevent spoilage. Hence, the expanding food and beverage industry with growing urbanization is expected to boost the demand for caps and closures over the forecast period.

Market Dynamics

The strongest growth driver for the caps and closures market is the accelerating global demand for sustainable and functional packaging. Consumer awareness around environmental impacts, combined with government restrictions on single-use plastics, has led brand owners to redesign packaging for circularity. This includes the adoption of lightweighted closures, tethered caps, and mono-material systems that enhance recyclability and meet Extended Producer Responsibility (EPR) mandates. The EU's Single-Use Plastics Directive (SUPD), for example, has made tethered closures mandatory for beverage containers by 2024, prompting widespread retooling and innovation in closure design. As brands seek to demonstrate measurable sustainability improvements, closures—being small yet high-volume, have become a visible and impactful area for reformulation.

Beyond sustainability, functional performance enhancements are driving adoption of advanced closure systems across industries. In beverages, consumers expect ergonomic, spill-proof, and resealable options that improve convenience; in pharmaceuticals, demand is rising for child-resistant, tamper-evident, and controlled-dispensing closures that meet stringent safety and hygiene standards. The food and personal care sectors are investing in smart and value-added closures integrating tamper sensors, freshness indicators, and embedded RFID/NFC tags for authenticity and traceability. These developments expand the closure's role from a simple seal to a multifunctional component central to product integrity and brand experience.

Moreover, technological innovations in materials—such as the development of biopolymers, recycled PET, and advanced TPE/TPU elastomers—allow manufacturers to achieve sustainability targets without sacrificing mechanical performance or sealing reliability. Global leaders like AptarGroup, Berry Global, and Silgan Holdings are leveraging digital design tools and additive manufacturing to accelerate product development cycles, enabling rapid customization for brands seeking differentiation. As sustainability becomes integral to packaging strategy, the market for eco-efficient, high-functionality closures will continue to expand, reinforcing this as the primary driver through the decade.

One of the key restraints in the caps and closures market is volatile polymer feedstock pricing, which directly impacts converter profitability and downstream pricing stability. Polypropylene (PP), polyethylene (PE), and polyethylene terephthalate (PET)—the primary materials used in closures—are tied to crude oil and natural gas markets, making their cost structures sensitive to geopolitical disruptions, energy price fluctuations, and refinery output cycles. During periods of supply-chain instability, such as post-pandemic recovery and the Russia–Ukraine conflict, resin prices have seen double-digit swings, eroding margins for converters locked into fixed-supply contracts. For smaller or regional manufacturers, this volatility creates procurement challenges, discourages capacity expansion, and limits competitiveness against vertically integrated players with resin access or hedging mechanisms.

Another layer of restraint is the regulatory complexity surrounding packaging materials, which varies significantly across regions. Food-contact compliance (FDA CFR 21, EU 10/2011), pharmaceutical packaging standards (ISO 8317, USP <661>), and environmental mandates (EPR, SUPD, Plastic Waste Management Rules) collectively impose high compliance costs.

Market Concentration & Characteristics

The global caps and closures market is characterized by high volume, low unit value, and a mission-critical role within the broader packaging ecosystem. Caps and closures are essential components that ensure product safety, integrity, freshness, and usability across end-use industries such as beverages, food, pharmaceuticals, personal care, and household chemicals. Despite representing a relatively small proportion of total packaging cost, they play a decisive role in leak prevention, shelf-life preservation, tamper evidence, and consumer convenience, making demand highly resilient and closely tied to underlying packaged goods consumption rather than discretionary spending cycles.

The caps and closures industry exhibits a moderate to high level of consolidation, particularly at the global and regional levels, with large multinational players benefiting from economies of scale, proprietary designs, and long-term supply agreements with major brand owners. These companies typically operate extensive manufacturing networks near bottling and filling facilities to reduce logistics costs and ensure just-in-time supply. At the same time, the market also includes a large number of small and mid-sized regional manufacturers that cater to local brands, niche applications, or specialized closure formats, creating a fragmented competitive landscape at the local level.

Material intensity and resin dependency are defining characteristics of the market. Plastics, especially polyethylene (HDPE, LDPE) and polypropylene (PP), dominate due to their durability, moldability, and cost efficiency. At the same time, metal closures continue to be used in select food, beverage, and premium packaging applications. As a result, the industry is highly sensitive to raw material price fluctuations, tooling costs, and energy prices, which directly influence margins and pricing strategies. Manufacturers often rely on long-term resin contracts, lightweighting, and design optimization to mitigate cost pressures.

The caps and closures market is also driven by technological differentiation and functional innovation rather than purely aesthetic packaging trends. Features such as tamper-evident bands, child-resistant closures, dispensing systems, flip-tops, sports caps, and anti-counterfeiting mechanisms are increasingly important, particularly in pharmaceutical and beverage applications. Customization and compatibility with high-speed filling lines are critical, making supplier qualification cycles long and switching costs relatively high once a closure is approved for commercial use.

Material Insights

The plastics segment accounted for the largest market share of 55.55% in 2025. This is attributed to its high versatility and functional performance across a wide range of packaging applications. Plastics such as polypropylene (PP) and polyethylene (HDPE and LDPE) offer an optimal balance of strength, flexibility, chemical resistance, and durability, making them suitable for use in beverages, food, pharmaceuticals, personal care, and household products. These materials can be precisely engineered to meet specific sealing, dispensing, and safety requirements, enabling manufacturers to design closures that ensure product integrity while enhancing consumer convenience.

Moreover, the dominance of plastics is their compatibility with high-speed, automated filling and capping lines. Plastic caps and closures can be molded to extremely tight tolerances, ensuring consistent performance at high production volumes without compromising seal integrity. This reliability is critical for large-scale bottling and packaging operations, where even minor inconsistencies can result in product leakage, contamination, or costly line stoppages. As a result, brand owners prefer plastic closures that integrate seamlessly with existing packaging infrastructure.

Cost efficiency and material economics also play a significant role in plastic’s leadership. Compared to metal or other materials, plastics offer lower raw material costs, reduced tooling wear, and lighter weight, resulting in savings across manufacturing, transportation, and handling. Lightweight plastic closures help reduce overall packaging weight, supporting logistics efficiency and lowering carbon emissions, which is particularly important for high-volume, mass-market consumer goods.

The ability of plastics to support functional innovation and customization further strengthens their market position. Plastic materials can be molded into complex shapes and integrated with advanced features such as tamper-evident bands, child-resistant mechanisms, dispensing nozzles, flip-tops, sports caps, and reclosable systems. This design flexibility allows brand owners to differentiate products, improve user experience, and meet evolving regulatory and safety requirements, especially in pharmaceutical and food packaging.

Product Insights

The dispensing caps segment dominated the caps and closures industry, accounting for the largest market share of 35.29% in 2025 and expected to grow at the fastest CAGR of 5.7% over the forecast period. This is due to their ability to enhance consumer convenience and control product use across a wide range of end-use industries. These caps enable precise, one-handed, spill-free dispensing of liquids, semi-liquids, and viscous products, making them highly preferred across categories such as personal care, household cleaning products, food condiments, and pharmaceuticals. As consumer lifestyles increasingly favor ease of use, portability, and hygiene, brand owners have widely adopted dispensing caps to improve functionality and differentiate products on retail shelves.

In addition, dispensing caps enhance product safety and optimize value, further driving their dominance. Features such as tamper evidence, child resistance, resealability, and controlled flow help reduce product waste, prevent contamination, and extend shelf life. From a manufacturing perspective, dispensing caps are compatible with high-speed filling lines and can be customized for different viscosities and container formats. This combination of functional versatility, consumer appeal, and operational efficiency has made dispensing caps the preferred closure type, securing their leading position in the global market.

Application Insights

The food segment led the caps and closures industry, accounting for the largest share of 26.45% in 2025. This is primarily due to the sheer volume and frequency of packaged food consumption worldwide. Packaged foods such as sauces, condiments, edible oils, dairy products, spreads, and ready-to-eat items require secure and reliable closure systems to maintain freshness, prevent leakage, and ensure food safety throughout storage and distribution. Given the high turnover and repeat-purchase nature of food products, demand for caps and closures in this segment remains consistently strong and less sensitive to economic cycles compared to discretionary consumer goods.

Furthermore, stringent food safety regulations and quality standards have reinforced the dominance of the food segment. Manufacturers must comply with hygiene, tamper-evidence, and shelf-life preservation requirements, driving the widespread adoption of advanced caps and closures with features such as airtight sealing, resealability, and tamper-evident mechanisms. The growing preference for convenience foods and portion-controlled packaging has further increased the use of specialized closures, including dispensing and easy-open caps, solidifying the food segment’s leading market position.

The cosmetics and toiletries segment is expected to register the fastest CAGR in the global caps and closures market, driven by rapid growth in personal care consumption, product premiumization, and evolving consumer preferences. Rising disposable incomes, urbanization, and increased awareness of personal grooming and hygiene-particularly in emerging economies-are driving higher demand for skincare, haircare, and beauty products. These products typically require specialized caps and closures that support controlled dispensing, portability, and aesthetic appeal, resulting in greater value-addition and faster growth than in more mature application segments.

Moreover, the cosmetics and toiletries segment is strongly influenced by innovation, branding, and e-commerce expansion, which accelerates closure demand. Brands increasingly rely on differentiated dispensing systems, airless pumps, flip-top caps, and customized designs to enhance user experience and reduce product waste. The shift toward smaller pack sizes, travel-friendly formats, and sustainable packaging solutions-such as lightweight and recyclable closures-has further boosted replacement cycles and new product launches. This combination of high innovation intensity, frequent product introductions, and strong online sales growth underpins the segment’s faster CAGR during the forecast period.

Regional Insights

Asia Pacific dominated the caps and closures market, accounting for the largest revenue share of 42.08% in 2025. This is due to the region’s large population and high consumption of packaged food, beverages, and personal care products. Rapid urbanization, changing lifestyles, and rising disposable incomes have significantly increased demand for packaged and convenience products across major economies, including China, India, Indonesia, and Vietnam. This high-volume consumption translates directly into strong demand for caps and closures, particularly in food, beverage, and household product applications, making APAC the largest regional market.

The China caps and closures market is growing due to the rapid expansion of its packaged food, beverage, and personal care industries, supported by rising urban populations and changing consumption patterns. The increasing adoption of modern retail formats and e-commerce has accelerated the shift from loose to packaged products, driving greater use of standardized, hygienic closures. In parallel, stricter food safety regulations and quality control norms are encouraging manufacturers to adopt advanced closure solutions, thereby boosting replacement demand and the adoption of value-added products.

North America Caps and Closures Market Trends

Across North America, the demand for caps and closures is increasing due to the expansion of beverage bottling, food processing, and household product manufacturing, supported by stable economic conditions and advanced packaging infrastructure. The region is witnessing strong uptake of sustainable and lightweight closure designs as brand owners align with environmental goals. High replacement cycles, along with the presence of major packaging manufacturers and continuous capacity upgrades, further drive steady market growth.

U.S. Caps and Closures Market Trends

The growth of the U.S. caps and closures industry is primarily driven by strong consumption of packaged foods, ready-to-drink beverages, and over-the-counter pharmaceuticals, as well as a well-established personal care market. Product innovation, including functional and dispensing closures, plays a critical role as brands focus on convenience, portion control, and user experience. Additionally, regulatory emphasis on tamper evidence and child-resistant packaging in food and pharmaceutical applications continues to sustain demand for high-performance caps and closures.

Europe Caps and Closures Market Trends

In Europe, rising demand is supported by increasing consumption of packaged foods and personal care products, alongside stringent packaging and sustainability regulations. Policies promoting recyclability, tethered caps, and reduced plastic waste are accelerating the transition to compliant, redesigned closure systems. Moreover, the region’s diverse consumer base and high penetration of premium and private-label brands continue to stimulate demand for differentiated and functional caps and closures across multiple end-use sectors.

The caps and closures market in Germany is expected to grow, primarily driven by Germany’s demand growth is fueled by its position as a major hub for food processing, beverages, and pharmaceutical manufacturing in Europe. The country’s strong focus on quality, precision engineering, and regulatory compliance drives the adoption of high-specification caps and closures. Additionally, growing emphasis on recyclable materials and circular economy practices is increasing demand for innovative, mono-material, and lightweight closure solutions across consumer and industrial packaging applications.

Key Caps and Closures Company Insights

The global caps and closures market is characterized by moderate to high competitive intensity, with the presence of several large multinational players alongside numerous regional and local manufacturers. Leading companies compete on the basis of scale, product portfolio breadth, material innovation, and long-term relationships with major food, beverage, pharmaceutical, and personal care brands. High switching costs, driven by tooling investments and compatibility requirements with filling lines, favor established suppliers and create barriers for new entrants, particularly in regulated applications.

At the same time, competition is increasingly shaped by innovation, sustainability, and customization capabilities. Companies are investing in lightweight designs, tethered caps, mono-material closures, and recycled-content solutions to meet evolving regulatory and brand-owner requirements. Strategic initiatives such as capacity expansions, geographic footprint optimization, and collaborations with brand owners for co-development of closure systems are common, as manufacturers seek to differentiate themselves beyond price and strengthen their competitive positioning in both mature and high-growth markets.

-

In April 2025, Ekam Global, a packaging sourcing and supply company, entered into a strategic partnership with sustainability-focused start-up Blue Ocean Closures to introduce an innovative fiber-based screw cap aimed at reducing plastic usage in packaging applications. This development marks the first commercial deployment of Blue Ocean Closures’ cellulose fiber screw cap, positioning it as a viable alternative to conventional plastic closures and highlighting growing industry momentum toward fiber-based and circular packaging solutions.

-

In September 2024, Berry Plastics Corporation launched a new tamper-evident pouring closure specifically designed for sauces, dressings, and edible oils. The closure emphasizes consumer convenience and functional performance while incorporating design features that enhance recyclability and overall sustainability, reinforcing Berry’s focus on innovation aligned with evolving regulatory and environmental requirements.

Key Caps and Closures Companies:

The following key companies have been profiled for this study on the caps and closures market.

- Crown

- Amcor plc

- Closure Systems International

- Ball Corporation

- Silgan Holdings Inc.

- Guala Closures S.p.A

- AptarGroup, Inc.

- BERICAP

- Nippon Closures Co., Ltd.

- Sonoco Products Company

- Webpac Ltd

- JELINEK CORK GROUP

- UAB Elmoris

- CL Smith

- PELLICONI & C. SPA

- O. BERK

- UNITED CAPS

Caps and Closures Market Report Scope

Report Attribute

Details

Market size in 2025

USD 111.0 billion

Estimated market size in 2026

USD 116.6 billion

Projected market size by 2033

USD 167.4 billion

Growth rate

CAGR of 5.3% from 2026 to 2033

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, competitive landscape, growth factors, and trends

Segments covered

Product, material, application, and region

States scope

North America; Europe; Asia Pacific; Latin America; Middle East & Africa

Country Scope

U.S.; Canada; Mexico; UK; Germany; France; Italy; China; Japan; India; Australia; Brazil; Saudi Arabia

Key companies profiled

Crown; Amcor plc; Closure Systems International; Ball Corporation; Silgan Holdings Inc.; Guala Closures S.p.A; AptarGroup, Inc.; BERICAP; Nippon Closures Co., Ltd.; Sonoco Products Company; Webpac Ltd; JELINEK CORK GROUP; UAB Elmoris; CL Smith; PELLICONI & C. SPA; O.BERK; UNITED CAPS

Customization scope

Free report customization (equivalent up to 8 analyst’s working days) with purchase. Addition or alteration to country, regional, and segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Caps And Closures Market Report Segmentation

This report forecasts revenue growth at a global level and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global caps and closures market report based on product, material, application, and region:

-

Material Outlook (Revenue, USD Million, 2021 - 2033)

-

Plastic

-

Metal

-

Others

-

-

Product Outlook (Revenue, USD Million, 2021 - 2033)

-

Dispensing Caps

-

Screw Closures

-

Crown Closures

-

Aerosol Closures

-

Others

-

-

Application Outlook (Revenue, USD Million, 2021 - 2033)

-

Food

-

Beverage

-

Healthcare

-

Cosmetics & Toiletries

-

Automotive

-

Pharmaceutical

-

Others

-

-

Regional Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

France

-

UK

-

Italy

-

-

Asia Pacific

-

China

-

India

-

Japan

-

Australia

-

-

Latin America

-

Brazil

-

-

Middle East & Africa

-

Saudi Arabia

-

-

Frequently Asked Questions About This Report

The global caps and closures are expected to grow at a CAGR of 5.3% from 2025 to 2033 to reach around USD 167.4 billion by 2033.

The key market player in the caps and closures market includes Crown, Amcor plc, Closure Systems International, Ball Corporation, Silgan Holdings Inc., Berry Global Inc., Guala Closures S.p.A, AptarGroup, Inc., BERICAP, Nippon Closures Co., Ltd., Sonoco Products Company, Webpac Ltd, JELINEK CORK GROUP, UAB Elmoris, CL Smith, PELLICONI & C. SPA, O.BERK, UNITED CAPS.

Rising consumption of bottled water coupled with alcoholic beverages from the growing population across the globe is expected to drive the caps and closures market during the forecast period.

Food emerged as a dominating application with a value share of around 26.5% in the year 2025.

Plastics held the largest revenue share 55.6% in 2025.

Dispensing caps held the largest share (over 35.3%) in 2025.

Asia Pacific dominated with a 42.1% revenue share in 2025.

The global caps and closures market was estimated at around USD 111.0 billion in the year 2025 and is expected to reach around USD 116.6 billion in 2026.

About the Author(s)

Plastics, Polymers & Resins Research Team

Bulk Chemicals · Plastics, Polymers & ResinsThis report was authored by the plastics, polymers & resins research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the plastics, polymers & resins segment of the bulk chemicals industry. All findings are based on proprietary bulk chemicals databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.