- Home

- »

- Power Generation & Storage

- »

-

Data Center Battery Market Size & Share Report, 2026-2033GVR Report cover

![Data Center Battery Market (2026 - 2033)Report]()

Data Center Battery Market (2026 - 2033)

Size, Share & Trends Analysis Report By Battery Type (Lead Acid, Lithium-ion, Nickel Zinc), By Data Center (Enterprise Data Centers, Colocation Data Centers), By Application, By Region, And Segment Forecasts

Market Size, 2025

$3.6BMarket Estimate, 2026

$3.8BMarket Forecast, 2033

$6.1BCAGR, 2026–2033

6.9%Data Center Battery Market Summary

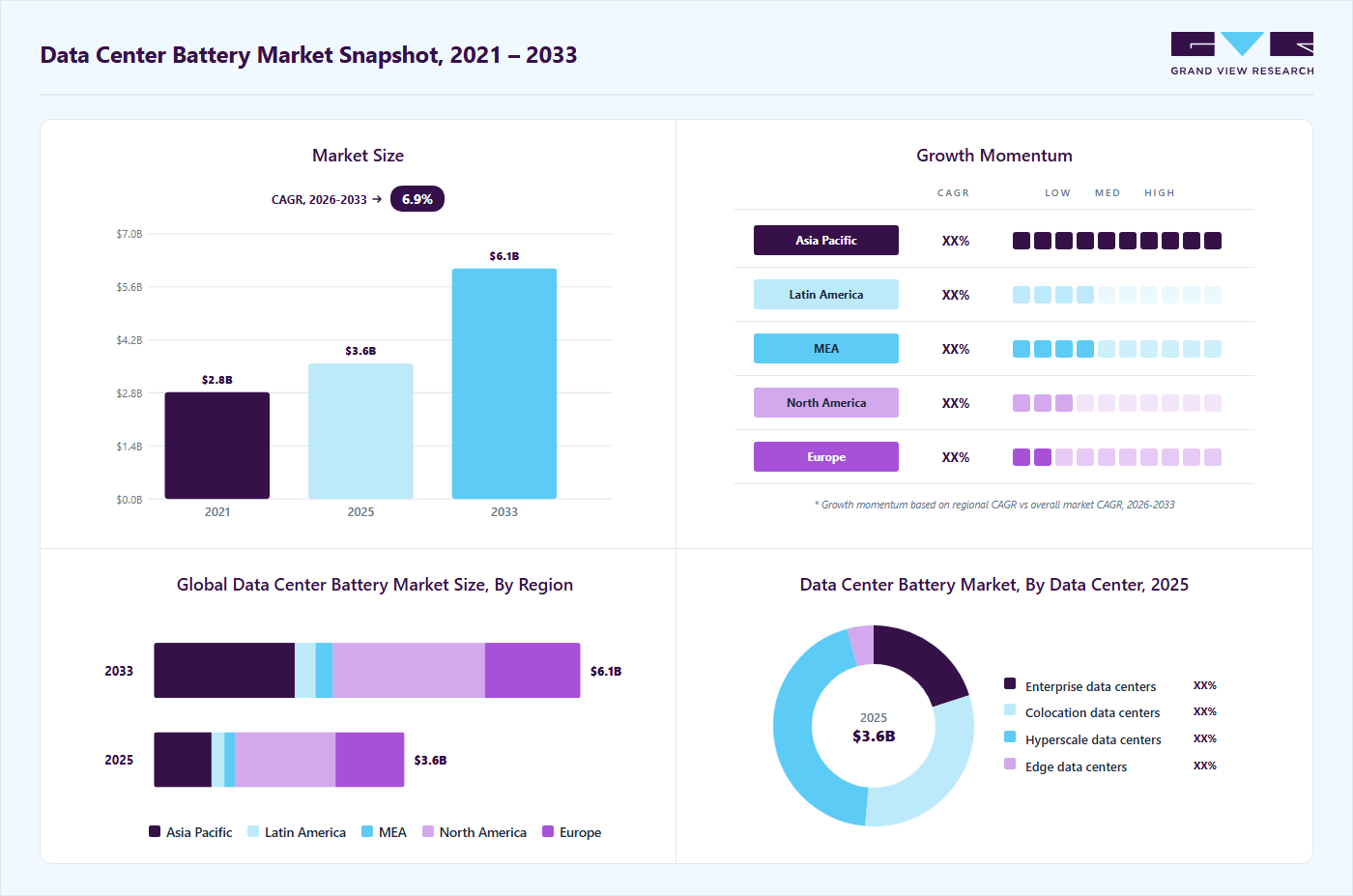

The global data center battery market size was valued at USD 3.6 billion in 2025 and is projected to grow from USD 3.8 billion in 2026 to USD 6.1 billion by 2033, at a CAGR of 6.9% from 2026 to 2033. North America held the largest revenue share of 40.2% of the global market in 2025. The growth is primarily driven by the rapid expansion of hyperscale facilities, increasing dependence on cloud-based services, and the rising need for uninterrupted power supply to support mission-critical operations.

Key Market Trends & Insights

- By battery type: Lead Acid segment dominated the market, with a revenue share of 56.3% in 2025.

- By data center: Hyperscale data centers segment held the largest market share of 44.3% in 2025.

- By application: Uninterruptible Power Supply (UPS) segment held the largest revenue share of 65.0% in 2025.

Regional Highlights

- Largest regional market: North America (40.2% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

- By country: The U.S. held the largest market share in 2025.

Market Size & Forecast

- Market size in 2025: USD 3.6 Billion

- Estimated market size in 2026: USD 3.8 Billion

- Projected market size by 2033: USD 6.1 Billion

- CAGR (2026-2033): 6.9%

As data centers handle growing volumes of digital traffic, operators are prioritizing advanced battery systems to ensure business continuity, minimize downtime, and maintain service reliability. Additionally, the shift toward edge computing and high-density workloads is further accelerating demand for efficient and scalable backup power solutions.

")

Technological advancements in battery chemistries, battery management systems (BMS), and thermal control technologies are improving energy efficiency, operational safety, and lifecycle performance, making modern battery solutions more cost-effective and dependable. Lithium-ion batteries are increasingly replacing traditional lead-acid alternatives due to their compact design, faster recharge capability, and longer service life. At the same time, data center operators are aligning sustainability goals by integrating battery storage with renewable energy sources and adopting energy-efficient infrastructure to reduce carbon footprints. Supportive government policies focused on energy efficiency, grid resilience, and emissions reduction, along with strategic collaborations between battery manufacturers, data center developers, and power solution providers, are strengthening the market ecosystem and positioning data center batteries as a critical component of resilient and sustainable digital infrastructure.

Drivers, Opportunities & Restraints

The industry is primarily driven by the rapid growth of hyperscale and colocation facilities, increasing dependence on cloud services, and the rising need for reliable backup power to ensure operational continuity. As digital workloads expand due to artificial intelligence, big data, and edge computing, data center operators are prioritizing advanced battery systems to minimize downtime and maintain service reliability.

Additionally, the growing emphasis on sustainability is encouraging the adoption of energy-efficient battery technologies that support renewable energy integration and help reduce carbon emissions. Supportive government policies promoting efficient power infrastructure, along with stricter uptime standards, are further contributing to market expansion.

However, high initial investment costs for advanced battery technologies, particularly lithium-ion systems, can limit adoption among smaller operators. Safety concerns, including thermal management and fire risks, combined with complex regulatory compliance requirements, add to deployment challenges. Supply chain uncertainties for key raw materials and the technical difficulty of upgrading legacy facilities also act as potential restraints for market growth.

Battery Type Insights

The Lead Acid segment accounted for the largest market share of around 56.3% in 2025, primarily driven by its cost-effectiveness, proven reliability, and long-standing presence in backup power applications for data centers. These batteries are widely deployed in uninterruptible power supply (UPS) systems due to their robust performance, predictable discharge characteristics, and ability to provide immediate power during outages. Lead-acid batteries are particularly preferred in small-to mid-sized data centers and legacy facilities where infrastructure is already optimized for their deployment. Their relatively lower upfront cost established a recycling ecosystem, and ease of replacement continues to support strong global adoption, especially in regions where budget constraints influence technology selection.

Meanwhile, the Nickel Zinc segment is projected to register the fastest growth at a CAGR of 13.4% during the forecast period, supported by increasing demand for safer, high-performance, and environmentally friendly battery alternatives. Nickel zinc batteries offer advantages such as higher power density, improved thermal stability, and reduced fire risk compared to traditional chemistries, making them well-suited for modern high-density data center environments. Additionally, their ability to operate efficiently across a wide temperature range, combined with a lower environmental impact due to the absence of toxic heavy metals, is encouraging adoption among operators focused on sustainability and regulatory compliance. Growing investments in next-generation data center infrastructure and the shift toward compact, energy-efficient backup solutions are expected to accelerate the deployment of nickel-zinc battery technologies further.

Data Center Insights

The Hyperscale data centers segment accounted for the largest market share of approximately 44.3% in 2025, driven by the rapid expansion of cloud computing, artificial intelligence workloads, and large-scale digital platforms. These facilities require highly reliable and scalable backup power infrastructure to maintain continuous operations and prevent costly service disruptions. As hyperscale operators manage massive volumes of data and support latency-sensitive applications, the deployment of advanced battery systems has become critical for ensuring power stability and operational resilience. Strong investments by major technology companies, along with the growing need for energy-efficient and sustainable infrastructure, continue to support segment dominance. Additionally, hyperscale facilities increasingly integrate renewable energy sources, further strengthening the role of high-capacity battery storage in managing power fluctuations and supporting grid reliability.

Meanwhile, the Edge data centers segment is projected to register the fastest growth at a CAGR of 12.6% during the forecast period, supported by the rising demand for low-latency data processing and real-time analytics. The proliferation of Internet of Things (IoT) devices, 5G networks, autonomous technologies, and smart city initiatives is accelerating the deployment of edge facilities closer to end users. These smaller, distributed data centers require compact, high-performance battery solutions capable of operating in space-constrained and remote environments. Increasing enterprise adoption of edge computing to enhance user experience and reduce network congestion, combined with advancements in modular power architecture, is expected to drive segment growth further. As organizations prioritize faster data delivery and localized processing, edge data centers are set to become a key contributor to future battery demand.

Application Insights

The Uninterruptible Power Supply (UPS) segment accounted for the largest market share of approximately 65% in 2025, primarily driven by the critical need for continuous power in data center operations. UPS systems serve as the first line of defense against power interruptions, protecting sensitive IT equipment from outages, voltage fluctuations, and grid instability. As data centers increasingly support mission-critical workloads such as cloud computing, financial transactions, and real-time analytics, the demand for highly reliable battery-backed UPS infrastructure continues to grow. Additionally, stringent uptime requirements, including Tier standards, and the rising cost of downtime are encouraging operators to invest in robust backup solutions. The widespread deployment of lithium-ion and advanced battery technologies within UPS architectures is further enhancing system reliability, reducing maintenance, and improving overall operational efficiency.

Meanwhile, the Energy Storage Systems (ESS) segment is projected to register the fastest growth at a CAGR of 26.3% during the forecast period, supported by the growing shift toward intelligent energy management and sustainable data center operations. ESS enables facilities to store excess energy, integrate renewable power sources, and participate in grid services such as peak shaving and demand response, helping operators optimize energy costs and improve resilience. Increasing focus on carbon reduction, coupled with advancements in battery performance and energy management software, is accelerating ESS adoption across both hyperscale and colocation facilities. Furthermore, the transition toward grid-interactive and net-zero data centers is expected to position energy storage as a strategic asset, driving substantial growth in this segment over the coming years.

Regional Insights

North America data center battery market accounted for the largest revenue share of approximately 40.2% in the global Data Center Battery market, driven by the strong presence of hyperscale data centers, rapid cloud adoption, and significant investments in digital infrastructure. The region benefits from advanced power management technologies, early adoption of lithium-ion and next-generation battery systems, and stringent uptime requirements across mission-critical facilities. Major technology companies continue to expand their data center footprint across the U.S. and Canada, further strengthening demand for reliable backup power solutions. Additionally, increasing emphasis on sustainability and renewable energy integration is encouraging operators to deploy energy-efficient battery systems that support grid stability and carbon reduction goals.

U.S. Data Center Battery Market Trends

The data center battery market in the United States is supported by the concentration of hyperscale operators and continuous investments in advanced computing infrastructure. Growing reliance on AI-driven workloads, big data, and streaming services is increasing the need for highly resilient backup power systems. Data center operators are increasingly transitioning toward lithium-ion and other advanced chemistries to enhance efficiency, reduce maintenance, and optimize space utilization. Furthermore, regulatory focus on energy efficiency and the rising adoption of renewable power sources are encouraging the integration of battery storage systems to improve operational sustainability.

Asia Pacific Data Center Battery Market Trends

The data center battery market in Asia Pacific is expected to register the fastest CAGR of 11.8% over the forecast period, supported by rapid digitalization, expanding internet penetration, and growing investments in large-scale data center projects. Countries such as China, India, Japan, Singapore, and Australia are witnessing rising demand for colocation and hyperscale facilities as enterprises accelerate cloud migration. Government initiatives promoting digital economies, smart infrastructure, and energy-efficient technologies are further driving battery adoption. Additionally, the growing construction of edge data centers to support 5G networks and real-time data processing is creating significant opportunities for compact, high-performance battery solutions across the region.

Europe Data Center Battery Market Trends

The data center battery market in Europe is supported by strict energy efficiency regulations, strong sustainability commitments, and ambitious carbon neutrality targets. The region is witnessing increased deployment of green data centers designed to minimize environmental impact while maintaining high operational reliability. Countries such as Germany, the U.K., France, Ireland, and the Netherlands are key contributors due to robust digital infrastructure and favorable regulatory frameworks. Additionally, the growing use of renewable energy in data center operations is accelerating the need for advanced battery storage solutions capable of managing intermittent power supply.

Latin America Data Center Battery Market Trends

The data center battery market in Latin America is driven by expanding digital connectivity, rising cloud adoption, and increasing investments from global technology providers. Brazil, Mexico, and Chile are emerging as important data center hubs due to improving network infrastructure and supportive government policies. As enterprises modernize their IT capabilities, the demand for reliable power backup systems is increasing. Operators are also exploring energy-efficient battery technologies to address power reliability challenges and support long-term operational stability.

Middle East & Africa Data Center Battery Market Trends

The data center battery market in the Middle East & Africa (MEA) is in a developing phase, supported by growing digital transformation initiatives and rising investments in smart city projects. Countries such as the United Arab Emirates, Saudi Arabia, and South Africa are expanding their data center capacity to support economic diversification and technological advancement. While infrastructure limitations and high deployment costs remain challenges, increasing awareness of energy resilience and the need for uninterrupted services are expected to drive gradual adoption of advanced battery systems. Sustainability initiatives and renewable energy projects are also likely to create future growth opportunities across the region.

Key Data Center Battery Company Insights

Some of the key players operating in the global data center battery market include EnerSys, Exide Technologies, East Penn Manufacturing, GS Yuasa Corporation, Saft Groupe S.A., Samsung SDI, LG Energy Solution, Panasonic Holdings Corporation, Leclanché SA, and ZincFive, among others. These companies are actively engaged in the design, manufacturing, and deployment of advanced battery solutions to support uninterrupted power supply across hyperscale, colocation, enterprise, and edge data centers. Their product offerings span multiple chemistries, including lead-acid, lithium-ion, and nickel-zinc, enabling operators to select solutions based on performance, safety, lifecycle, and cost requirements.

Market participants are increasingly focusing on enhancing battery efficiency, improving safety features, extending service life, and integrating intelligent battery management systems to optimize power reliability. Strategic initiatives such as partnerships with data center developers, UPS providers, and power infrastructure companies are strengthening deployment capabilities and expanding global reach. Additionally, rising investments in sustainable data center infrastructure are encouraging manufacturers to develop energy-efficient and recyclable battery technologies that align with carbon reduction goals. As digital infrastructure continues to expand worldwide, these companies are well-positioned to capitalize on growing demand for resilient and scalable energy storage solutions, further accelerating innovation and competition within the Data Center Battery market.

Key Data Center Battery Companies:

The following key companies have been profiled for this study on the data center battery market.

- EnerSys

- Exide Technologies

- East Penn Manufacturing

- GS Yuasa Corporation

- Saft Groupe S.A.

- Samsung SDI

- LG Energy Solution

- Panasonic Holdings Corporation

- Leclanché SA

- ZincFive

Recent Developments

-

In November 2025, Exide Technologies unveiled its latest energy storage solutions at Data Centre World Paris, introducing the Solition Data Center system. This advanced lithium-ion energy storage solution is specifically designed for data center and commercial UPS applications, featuring intelligent fire protection at the module level, support for combining new and used batteries, and a compact design that reduces the required space by up to 60%. These enhancements aim to improve safety, reliability, and total cost of ownership for data center operators.

Data Center Battery Market Report Scope

Report Attribute

Details

Market Definition

The Data Center Battery market size represents the global revenue generated from the development, manufacturing, and deployment of battery systems that provide backup power and energy storage to ensure uninterrupted operations across hyperscale, colocation, enterprise, and edge data centers worldwide.

Market size value in 2025

USD 3.6 billion

Estimated Market size in 2026

USD 3.8 billion

Projected Market size by 2033

USD 6.1 billion

Growth rate

CAGR of 6.9% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, competitive landscape, growth factors, and trends

Segments covered

Battery type, data center, application, region

Regional scope

North America; Europe; Asia Pacific; Latin America; Middle East & Africa

Country scope

U.S.; Canada; Mexico; Germany; UK; France; Italy; Spain; China; India; Japan; Brazil; Argentina; Saudi Arabia; UAE; South Africa

Key companies profiled

EnerSys; Exide Technologies; East Penn Manufacturing; GS Yuasa Corporation; Saft Groupe S.A.; Samsung SDI; LG Energy Solution; Panasonic Holdings Corporation; Leclanché SA; ZincFive

Customization scope

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Data Center Battery Market Report Segmentation

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global data center battery market report on the basis of battery type, data center, application and region:

-

Battery Type Outlook (Revenue, USD Million, 2021 - 2033)

-

Lead Acid

-

Lithium-ion

-

Nickel Zinc

-

Others

-

-

Data Center Outlook (Revenue, USD Million, 2021 - 2033)

-

Enterprise data centers

-

Colocation data centers

-

Hyperscale data centers

-

Edge data centers

-

-

Application Outlook (Revenue, USD Million, 2021 - 2033)

-

Uninterruptible power supply (UPS)

-

Backup power systems

-

Energy storage systems (ESS)

-

Peak shaving and load balancing

-

-

Regional Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

France

-

Italy

-

Spain

-

-

Asia Pacific

-

China

-

India

-

Japan

-

-

Latin America

-

Brazil

-

Argentina

-

-

Middle East & Africa

-

Saudi Arabia

-

UAE

-

South Africa

-

-

Frequently Asked Questions About This Report

North America dominated with a 40.2% revenue share in 2025.

Asia Pacific is the fastest-growing region over the forecast period, with an expected CAGR of 11.8%.

The lead acid segment led with a 56.3% revenue share in 2025 due to its reliability and cost-effectiveness, while nickel zinc is the fastest-growing segment at a 13.4% CAGR.

The uninterruptible power supply (UPS) segment held the largest share (65.0%) in 2025, while energy storage systems (ESS) is the fastest-growing application model.

The global data center battery market size was estimated at USD 3.6 billion in 2025 and is expected to reach USD 3.8 billion in 2026.

The global data center battery market is expected to grow at a compound annual growth rate of 6.9% from 2026 to 2033 to reach USD 6.1 billion by 2033.

Based on the data center segment, Hyperscale data centers held the largest revenue share of over 44% in the data center battery market in 2025.

Some of the key vendors operating in the global data center battery market include EnerSys, Exide Technologies, East Penn Manufacturing, GS Yuasa Corporation, Saft Groupe S.A., Samsung SDI, LG Energy Solution, Panasonic Holdings Corporation, Leclanché SA, and ZincFive, among others.

The key factors driving the data center battery market include the rapid expansion of hyperscale and edge data centers, increasing reliance on cloud computing and digital services, and the growing need for an uninterrupted power supply to prevent downtime and data loss.

About the Author(s)

Power Generation & Storage Research Team

Energy & Power · Power Generation & StorageThis report was authored by the power generation & storage research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the power generation & storage segment of the energy & power industry. All findings are based on proprietary energy & power databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.