- Home

- »

- Consumer F&B

- »

-

Fructose Market Size, Share & Trends Report 2026-2033GVR Report cover

![Fructose Market (2026 - 2033)Report]()

Fructose Market (2026 - 2033)

Size, Share & Trends Analysis Report By Product (High Fructose Corn Syrups, Fructose Syrups, Fructose Solids), By Application (Beverages, Processed Foods, Dairy Products), By Region, And Segment Forecasts

Market Size, 2025

$5.5BMarket Estimate, 2026

$5.7BMarket Forecast, 2033

$8.8BCAGR, 2026–2033

6.2%Fructose Market Summary

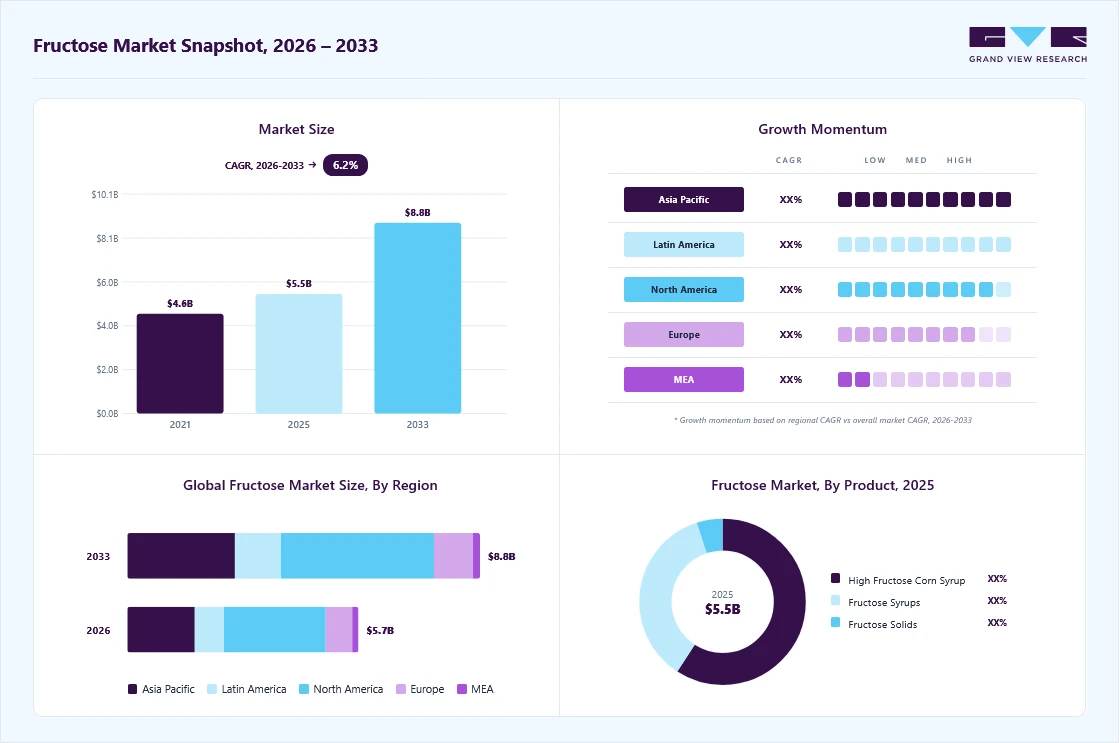

The global fructose market size was valued at USD 5.5 billion in 2025 and is projected to grow from USD 5.7 billion in 2026 to USD 8.8 billion by 2033, at a CAGR of 6.2% from 2026 to 2033. The market in North America dominated with a revenue share of 44.1% in 2025. The global market for fructose is expanding because it benefits from simultaneous growth in processed foods, beverage formulation, and industrial demand for cost-efficient sweeteners.

Key Market Trends & Insights

- By product: High fructose corn syrups segment held the largest market share of 59.1% in 2025.

- By application: Fructose in beverages segment held the largest market share of 67.7% in 2025.

Regional Highlights

- Largest regional market: North America (44.1% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

- By country: U.S. held the largest market share in 2025

Market Size & Forecast

- Market size in 2025: USD 5.5 Billion

- Estimated market size in 2026: USD 5.7 Billion

- Projected market size by 2033: USD 8.8 Billion

- CAGR (2026-2033): 6.2%

The rise of packaged foods, where fructose, especially in syrup and crystalline formats, is widely used across soft drinks, confectionery, dairy, and bakery products, is leading to market expansion. Compared to sucrose, fructose delivers higher perceived sweetness at lower inclusion rates, making it attractive when manufacturers aim to maintain taste profiles while optimizing costs and label positioning for mass products.

")

Another major factor is the beverage industry’s shift toward stable mouthfeel and fast-dissolving caloric sweeteners. Fructose fits particularly well in cold beverages because of its high solubility, flavor-carrying ability, and compatibility with acidic or fruit-based formulations. As ready-to-drink teas, energy drinks, vitamin waters, and flavored milk beverages grow, formulators increasingly adopt fructose or fructose-heavy derivatives to achieve sweetness that does not crystallize or destabilize at low temperatures. This strengthens repeat purchase in high-consumption markets across North America and the Asia Pacific, where beverage innovation and heat-stable sweetener adoption move fastest.

Fructose is a key feedstock for fermentation-based production of ingredients such as bioplastics, bio-ethanol derivatives, and specialty chemicals. Expansion in sustainability-driven input materials by manufacturers like Cargill, Incorporated, and ADM reinforces raw material stability, global output, and contract-supply networks, enabling lower price-per-sweetness curves at scale.

Demand for fruit-branded, “clean sweetness,” and honey-like flavor notes encourages brands to adopt fructose-based blends that position better with natural or indulgence messaging. In addition, food inflation cycles have pushed formulators to switch from higher-cost imported sweeteners to syrup formats that achieve equivalent sweetness with lower gram input, increasing total fructose volume consumed per SKU released.

Product Insights

The high fructose corn syrups dominated the market, accounting for a share of 59.1% in 2025. The demand for high fructose corn syrups is rising globally because it remains one of the most cost-efficient industrial sweeteners for large-scale food and beverage production. Compared to refined sugar, it offers easier liquid handling, longer shelf stability, better freeze-thaw tolerance, and smoother blending for mass-manufactured categories such as soft drinks, flavored dairy, bakery fillings, confectionery coatings, and ready-to-eat sauces. In addition, brand owners launching value-focused, long-shelf beverages for high-footfall retail channels (hypermarkets, QSRs, and bottled beverage supply chains) prefer HFCS for stable flavor delivery without sharp input cost spikes, making it a practical choice in mass foodservice and retail production planning.

The fructose syrups segment is predicted to grow at a CAGR of 6.6% from 2026 to 2033. Fructose syrups deliver higher perceived sweetness at lower volumes, which allows both households and food businesses to achieve stronger flavor impact with reduced ingredient usage, making them attractive during inflationary periods. In addition, these syrups blend seamlessly in beverages and culinary applications such as cold coffees, boba-style drinks, fruit blends, and home dessert preparations, driving repeat purchase cycles. The rapid expansion of convenience-first foodservice formats, including cloud kitchens, cafés, and delivery-led beverage outlets, amplifies demand because fructose syrups dissolve faster, do not crystallize easily, and stabilize temperature-specific formulations better than sucrose-based sweeteners.

Application Insights

Beverages application accounted for a share of 67.7% of the global market in 2025. Compared with sucrose, fructose syrups dissolve more easily in cold and carbonated formats, allowing beverage brands to achieve uniform sweetness, smoother mouthfeel, and better flavor masking in fruit-based drinks, iced teas, flavored milk, and sodas. From an industry economics standpoint, the price of fructose syrup remains lower and less volatile due to efficient processing output from major producing clusters in China, India, and the U.S., which makes it attractive for mass beverage manufacturers managing margin pressure. The growth of café chains, cloud kitchens, and ready-to-drink supply to foodservice also expands syrup pull-through per prepared drink.

Processed food applications are expected to grow at a CAGR of 7.6% from 2026 to 2033. Ingredients such as fructose syrups are cheaper to source than traditional sugar in many importing regions, offering a stable, bulky sweetening base that supports margins for packaged food producers. From a formulation standpoint, these syrups improve moisture retention, browning reactions in baked goods, texture stability in frozen or shelf-stable snacks, and faster dissolvability in concentrates, making them attractive to manufacturers focused on performance. In addition, rising demand for sweetness-forward categories such as confectionery fillings, flavored spreads, cereals, RTD coffee/tea bases, and fruit-profile snack coatings lifts usage of fructose syrups because they enhance taste intensity without overpowering aroma, while scaling efficiently across high-throughput industrial food processing lines.

Regional Insights

The North American fructose industry accounted for a share of 44.1% in 2025. Sweeteners such as high-fructose syrup remain significantly cheaper than household sugar on an industrial scale, making them the preferred choice for beverage manufacturers and contract food processors looking to manage input costs amid food inflation. Key drinks format carbonated beverages, flavored iced teas, sports drinks, and packaged fruit drinks still rely heavily on fructose syrup for flavor intensity, solubility, and long shelf stability.

The boom in ready-to-drink consumption after the pandemic, paired with growth in vending, convenience retail, and drive-thru beverage volumes at scale, directly lifts demand. In parallel, B2B buyers are seeing improved output predictability from domestic processing clusters and cross-border supply from partners like Mexico, reducing logistics friction and ensuring consistent availability throughout retail and foodservice channels.

U.S. Fructose Market Trends

The fructose industry in the U.S. is rising because they offer a cost-efficient sweetening solution that scales well across mass beverage and packaged food manufacturing. Compared to cane sugar, fructose syrups deliver stronger sweetness intensity at lower input volumes, reducing formulation cost for large-scale producers in categories like carbonated drinks, flavored dairy, bakery fillings, and tabletop sweetener blends. Their liquid form enables easier mixing, stable shelf performance, and extended moisture retention, which is valuable for high-throughput industrial production and private-label beverage manufacturing lines across the U.S.

Europe Fructose Market Trends

Europe fructose industry is expected to grow at a CAGR of 5.6% from 2026 to 2033. Demand for fructose syrups is rising in Europe primarily due to regulatory cost-efficiency loops and industrial supply strength at a country level. In France and the UK, high sucrose levies incentivize beverage makers to adopt fructose-syrup and isoglucose blends that match sweetness at a lower taxed cost per liter, protecting margins in RTD teas and chilled syrup bases. Germany and Spain benefit from strong corn wet-milling and isoglucose plants that ensure a stable, cost-competitive local supply and scalable contract manufacturing, accelerating industrial adoption. In Italy, demand is reinforced in bakeries and iced-drink formulations, where fructose syrups support low crystallization and superior cold solubility, reducing precipitation in chilled formats. The growth is therefore cost-structure and infrastructure-led, not declining, across beverage and food applications.

Asia Pacific Fructose Market Trends

The Asia Pacific fructose industry is expected to grow at a CAGR of 6.9% from 2026 to 2033. The demand for fructose syrups is rising in the Asia Pacific as a result of rapid packaged-food adoption, beverage manufacturing scale-up, and cost-efficient sweetener substitution loops. Expanding urban populations and the growth of ready-to-drink soft beverages, flavored dairy drinks, and convenience snacks increase the structural need for stable, liquid sweeteners that dissolve well, blend easily, and extend shelf life. Fructose-rich syrups are also price-efficient compared to crystalline sugars in high-throughput manufacturing, encouraging bulk usage among food and beverage producers in markets such as China, India, and Indonesia.

The region’s growing cold-chain beverages, cloud kitchens, and industrial bakery/confectionery output increase syrup adoption, driven by manufacturers seeking high-volume, cost-efficient, and easy-to-use liquid sweeteners for mass-market tastes and factory production needs.

Key Fructose Company Insights

The presence of a few established players and new entrants characterizes the market. Many big players are increasing their focus on the growing trend of the fructose industry. Players in the market are diversifying their service offerings in order to maintain market share.

Key Fructose Companies:

The following key companies have been profiled for this study on the fructose market.

- ADM

- Cargill, Incorporated

- DuPont

- Galam

- Ingredion, Inc.

- Shijiazhuang Huaxu Pharmaceutical Co., Ltd

- Tate & Lyle

- Roquette Frères

- COFCO Corporation

- Südzucker AG

Fructose Market Report Scope

Report Attribute

Details

Market size in 2025

USD 5.5 billion

Market size value in 2026

USD 5.7 billion

Revenue forecast in 2033

USD 8.8 billion

Growth rate

CAGR of 6.2% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion, Volume in Kilotons, and CAGR from 2026 to 2033

Report coverage

Revenue & volume forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Product, application, region

Regional scope

North America, Europe, Asia Pacific, Central & South America, Middle East & Africa

Country scope

U.S.; Canada; Mexico; UK; Germany; France; Italy; Spain; China; India; Japan; South Korea; Australia & New Zealand; Brazil; South Africa

Key companies profiled

ADM; Cargill, Inc.; DuPont; Galam; Ingredion, Inc.; Shijiazhuang Huaxu Pharmaceutical Co., Ltd.; Tate & Lyle; Roquette Frères; COFCO Corporation; Südzucker AG

Customization scope

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Fructose Market Report Segmentation

This report forecasts revenue growth at global, regional & country levels and provides an analysis on the latest trends and opportunities in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global fructose market report based on product, application, and region:

-

Product Outlook (Volume, Kilotons; Revenue, USD Million, 2021 - 2033)

-

High Fructose Corn Syrups

-

Fructose Syrups

-

Fructose Solids

-

-

Application Outlook (Volume, Kilotons; Revenue, USD Million, 2021 - 2033)

-

Beverages

-

Processed Foods

-

Dairy Products

-

Confectionary

-

Bakery & Cereals

-

Others

-

-

Regional Outlook (Volume, Kilotons; Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

UK

-

Germany

-

France

-

Italy

-

Spain

-

-

Asia Pacific

-

China

-

India

-

Japan

-

Australia & New Zealand

-

South Korea

-

-

Central & South America

-

Brazil

-

-

Middle East & Africa (MEA)

-

South Africa

-

-

Frequently Asked Questions About This Report

The key factors that are driving the fructose market include a growing trend for sugar, fat, and calorie reduction, coupled with increased demand from the food & beverage industry.

The global fructose market size was valued at USD 5.5 billion in 2025 and is estimated at USD 5.7 billion in 2026.

The global fructose market is expected to grow at a CAGR of 6.2% from 2026 to 2033, reaching USD 8.8 billion by 2033.

The beverages segment held the largest revenue share of 67.7% in 2025.

North America dominated the fructose market with a 44.1% revenue share in 2025.

Asia Pacific is the fastest-growing region over the forecast period.

The High Fructose Corn Syrup (HFCS) segment led with a 59.1% revenue share in 2025, while crystalline fructose is the faster-growing segment.

Key players include ADM, Cargill, Incorporated, DuPont, Galam, Ingredion, Shijiazhuang Huaxu Pharmaceutical Co., Ltd, Tate & Lyle.

About the Author(s)

Consumer F&B Research Team

Consumer Goods · Consumer F&BThis report was authored by the consumer f&b research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the consumer f&b segment of the consumer goods industry. All findings are based on proprietary consumer goods databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.