- Home

- »

- Plastics, Polymers & Resins

- »

-

Polypropylene Compounds Market Size Report, 2026-2033GVR Report cover

![Polypropylene Compounds Market (2026 - 2033)Report]()

Polypropylene Compounds Market (2026 - 2033)

Size, Share & Trends Analysis Report By Product (Mineral Filled, Compounded TPO, Compounded TPV), By Application (Fiber, Film & Sheet, Raffia), By End-use (Automotive, Textile), By Region, And Segment Forecasts

Market Size, 2025

$26.9BMarket Estimate, 2026

$28.9BMarket Forecast, 2033

$44.3BCAGR, 2026–2033

6.3%Polypropylene Compounds Market Summary

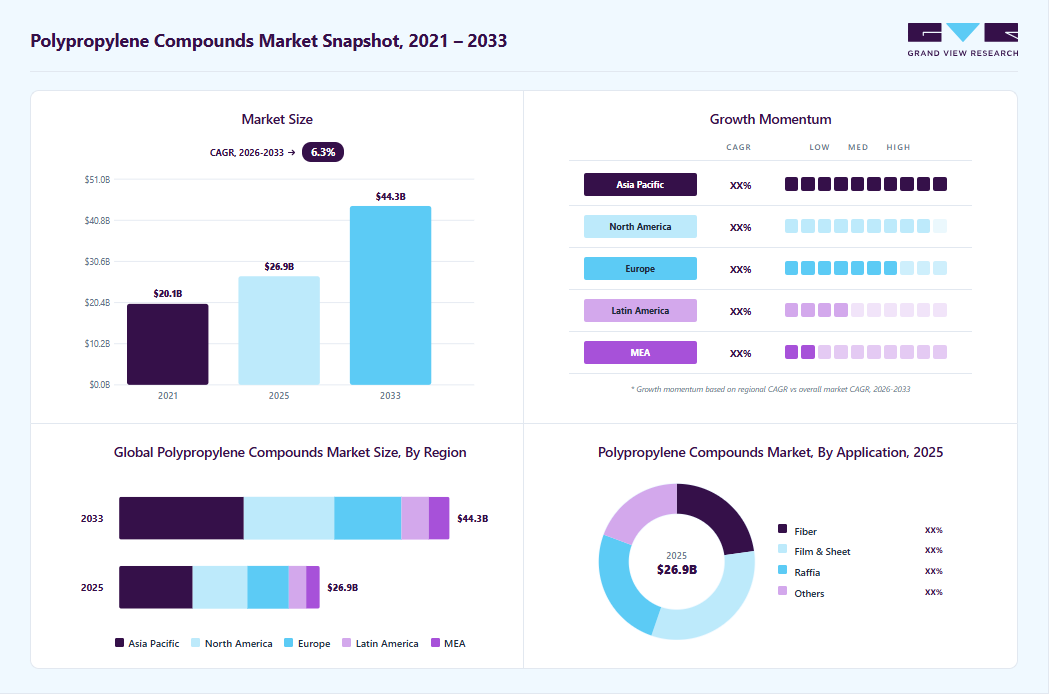

The global polypropylene (PP) compounds market size was valued at USD 26.9 billion in 2025 and is projected to grow from USD 28.9 billion in 2026 to USD 44.3 billion by 2033, growing at a CAGR of 6.3% from 2026 to 2033. Asia Pacific held the largest revenue share of 36.7% of the global market in 2025. Rising demand from the electrical and electronics industry is another key driver for the polypropylene (PP) compounds industry.

Key Market Trends & Insights

- By product: Mineral filled PP compounds segment held the largest market share of 29.5% in 2025.

- By application: Film & sheet segment held the largest market share of 32.5% in 2025.

- By end-use: Automotive segment held the largest market share of 54.6% in 2025.

Regional Highlights

- Largest regional market: Asia Pacific (36.7% market share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR of 6.6%, 2026-2033)

- By country: China held the largest market share in 2025.

Market Size & Forecast

- Market size in 2025: USD 26.9 Billion

- Estimated market size in 2026: USD 28.9 Billion

- Projected market size by 2033: USD 44.3 Billion

- CAGR (2026-2033): 6.3%

Polypropylene (PP) compounds are widely used in appliance housings, connectors, and cable insulation due to their cost efficiency, electrical insulation properties, and design flexibility. A key trend in the polypropylene compounds industry is the accelerated adoption of sustainable and high-performance formulations across major end use sectors.

")

Demand for recycled polypropylene and bio-based compound variants is rising as manufacturers align with circular economy expectations and regulatory pressures. In automotive, ongoing lightweighting initiatives for electric vehicles are driving the uptake of engineered PP compounds with enhanced mechanical properties. Packaging and consumer goods segments are also shifting toward recyclable compound grades to meet sustainability targets.

Market Dynamics

The polypropylene compounds market is being driven by broad-based demand from automotive, packaging, appliances, electrical components, and consumer goods. Polypropylene compounds are widely used because they combine low weight, good impact performance, processability, and cost efficiency. These properties make them suitable for applications where manufacturers want to reduce material intensity without sacrificing functional performance. As end-use industries continue to favor engineered plastics that balance economics and durability, compound demand remains structurally supported.

A major growth factor is the ongoing shift toward lightweight design. Automotive OEMs and component suppliers are increasing the use of polypropylene compounds in interior trims, battery housings, under-the-hood parts, and structural applications where weight reduction is important. The same logic applies to appliances and electrical products, where molded parts must meet dimensional stability, heat resistance, and aesthetics requirements. This broadens the use case for filled, reinforced, and impact-modified grades across multiple downstream sectors.

One of the main restraints in the polypropylene compounds market is exposure to upstream feedstock volatility. Propylene prices, energy costs, and resin supply balances directly affect compound economics. Because many end users operate in competitive procurement environments, producers often struggle to pass through cost increases quickly. This creates margin pressure and makes pricing more cyclical than in higher-value specialty materials.

Market Concentration & Characteristics

The market growth stage is moderate, at an accelerating rate. The market exhibits fragmentation, with key players dominating the industry landscape. Major companies such as Mitsui Chemical, Inc., IRPC Public Company Limited, Exxon Mobil Corporation, and others play a significant role in shaping the market dynamics. These leading players often drive innovation in the market, introducing new products, technologies, and product types to meet the industry's evolving demands.

Innovation in the polypropylene compounds industry is marked by the rapid development of performance-enhanced and sustainable materials tailored to specific industry needs. Producers are advancing high-impact and nano-composite PP compounds that deliver superior mechanical strength, thermal stability, and flame resistance for demanding automotive and electronics applications. Sustainable grades incorporating recycled and bio-based feedstocks are gaining traction in packaging and consumer goods to address regulatory and ESG pressures. Digital design tools and AI-assisted formulation are further accelerating the development of new compounds.

Product substitutes for polypropylene compounds vary by application, with alternatives such as acrylonitrile butadiene styrene (ABS), polyamide, and polycarbonate competing in segments that require higher-temperature performance or aesthetic qualities. In packaging, non-plastic substitutes such as paperboard and biodegradable films are gaining attention due to environmental concerns, though they lack the mechanical performance and cost efficiency of PP compounds. Metal and glass remain considered for structural applications, though the lightweight and cost advantages of PP compounds continue to favor them.

Product Insights

Mineral filled PP compounds dominated the market across all product segments in terms of revenue, accounting for a 29.54% market share in 2025, and is forecasted to grow at a 6.8% CAGR from 2026 to 2033. These compounds are most widely used in home appliances and automotive interiors such as consoles, panels, and knee bolsters. Compounded TPVs have also witnessed substantial growth in under-the-hood automotive applications owing to their improved oil and temperature resistance. Minerals are incorporated into polypropylene compounds to improve heat distortion and rigidity. The most widely used minerals in polypropylene compounds include talc, glass beads, mica, silica, and calcium. The improved thermal stability and mechanical stiffness enable their extensive use in several end use applications such as automotive, electrical & electronics.

The glass fiber reinforced segment is anticipated to grow at a substantial CAGR of 6.5% through the forecast period. Glass fiber reinforced compounds exhibit superior properties, including rigidity & strength, excellent chemical resistance, good mechanical properties, improved dimensional stability, and resistance to warpage. Polypropylene with 30% chemically coupled glass reinforcement has a 180% improvement in tensile strength. Glass-reinforced polypropylene offers higher tensile strength, enhanced heat resistance, and significantly improved stiffness. They are commonly used in structural components that require the aforementioned properties and are predominantly used in furniture, appliances, and automotive applications.

Application Insights

Film & sheet dominated the market across all application segments in terms of revenue, accounting for a 32.45% market share in 2025, and is forecasted to grow at a 6.7% CAGR from 2026 to 2033. The film and sheet segment is benefiting from expanding flexible packaging demand and industrial use cases requiring robust yet lightweight barriers. Polypropylene compounds tailored for film applications deliver targeted mechanical and thermal properties that support high-speed production and consistent performance. Growth in protective sheeting for construction, agriculture, and protective packaging is reinforcing demand. Enhanced surface aesthetics and recyclability further strengthen adoption across consumer and industrial channels.

The raffia segment is anticipated to grow at a substantial CAGR of 6.4% through the forecast period. Raffia applications are gaining traction as the agricultural and industrial fabrics market prioritizes durable, cost-efficient materials that withstand environmental stress. Woven PP raffia offers high tensile strength and moisture resistance, making it ideal for sacks, geotextiles, and erosion control products. Rising infrastructure activity and agricultural mechanization in emerging economies are increasing demand for engineered raffia materials that deliver long service life with low maintenance.

End-use Insights

Automotive dominated the market across the end use segmentation in terms of revenue, accounting for a 54.55% market share in 2025, and is forecast to grow at a 6.6% CAGR from 2026 to 2033. This segment is expected to witness rapid growth, driven by the increasing use of plastics in automotive components and a simultaneous rise in passenger car & heavy-duty vehicle production, particularly in Asia and Central & South America. Polypropylene compounds have become a popular alternative for engineering plastics and metals in automotive applications. They are used in interior, exterior, and under-the-hood applications in the automotive segment, including instrument panels, trims, and bumper fascias. The use of PP compounds can provide significant weight reduction and cost savings for manufacturers, owing to their low cost, exceptional mechanical properties, and good flexibility.

The electrical & electronics segment is expected to expand at a robust 6.3% CAGR over the forecast period in the automotive polypropylene compounds glazing market. The electrical and electronics sector is driving demand for specialized PP compounds that deliver superior insulation, heat resistance, and flame-retardant performance. These materials are preferred for housings, connectors, and insulating components as devices become more compact and operate at higher power densities. Growth in consumer electronics, smart appliances, and telecommunications infrastructure is expanding the use of engineered polypropylene grades that meet stringent safety and performance standards.

Regional Insights

The Asia Pacific polypropylene compounds industry held the largest share, accounting for 36.66% of the revenue in 2025, and is expected to grow at the fastest CAGR of 6.6% over the forecast period. Asian countries such as Vietnam, Indonesia, Thailand, India, China, and Japan are expected to emerge as the primary growth markets for PP compounds in the Asia Pacific. The growing manufacturing sector is expected to propel the demand for PP compounds in the automotive industry. Japan, South Korea, China, Taiwan, and other Southeastern Asian countries are the manufacturing hubs for household appliances with intense competition due to the presence of global manufacturers such as LG Electronics, Samsung, and Panasonic Corporation.

China Polypropylene Compounds Market Trends

The polypropylene compounds industry in China is expected to grow at a substantial CAGR of 7.0% from 2026 to 2033. China’s polypropylene compounds industry is propelled by its dominant manufacturing base and the rapid expansion of the automotive and infrastructure sectors. As the world’s largest polypropylene consumer, demand for compounds in vehicle interiors, construction materials, and consumer electronics remains robust. Growth in electric vehicle production and investments in research and development boost demand for high-performance PP grades. Government initiatives supporting industrial development and export competitiveness further reinforce market expansion.

North America Polypropylene Compounds Market Trends

The polypropylene compounds industry in North America is witnessing demand for polypropylene compounds, which is bolstered by the region’s mature automotive and packaging industries, which are focused on lightweight, sustainable solutions. Manufacturers are investing in advanced PP compound formulations to meet stringent fuel efficiency and emissions standards. The region’s strong emphasis on R&D and recycling technologies also encourages the adoption of engineered and recycled compound grades. High domestic demand across consumer goods and construction sectors reinforces steady market expansion.

The U.S. polypropylene compounds industry is driven by innovation and demand for high-performance polypropylene compounds across automotive, healthcare, and infrastructure sectors. Automotive OEMs are increasingly using engineered PP grades to reduce vehicle weight and improve fuel economy. Post-pandemic healthcare needs have sustained demand for medical products utilizing PP compounds. Investments in next-generation materials and sustainable production practices further support market growth, fostering competitiveness in global supply chains.

Europe Polypropylene Compounds Market Trends

In Europe polypropylene compounds industry, stringent environmental regulations and circular-economy initiatives are key drivers for polypropylene compound demand. Regulatory frameworks under the European Green Deal and related plastics policies are pushing manufacturers toward the use of recyclable, eco-friendly materials. Automotive and packaging sectors are adopting advanced PP compounds to meet emission targets and sustainability commitments. Strong engineering capabilities and focus on high-quality materials further enhance regional demand growth.

Key Polypropylene Compounds Company Insights

The polypropylene compounds industry is highly competitive, with several key players dominating the landscape. Major companies include Mitsui Chemical, Inc., IRPC Public Company Limited, Exxon Mobil Corporation, Avient Corporation, and GS Caltex Corporation. The polypropylene compounds industry is characterized by a competitive landscape with several key players driving innovation and market growth. Major companies in this sector are investing heavily in research and development to enhance the performance, cost-effectiveness, and sustainability of their products.

Key Polypropylene Compounds Companies:

The following key companies have been profiled for this study on the polypropylene compounds market.

- Mitsui Chemical, Inc.

- IRPC Public Company Limited

- Exxon Mobil Corporation

- Avient Corporation

- Japan Polypropylene Corporation

- SABIC

- Trinseo S.A.

- Sumitomo Chemical Co., Ltd.

- Washington Penn

- Borealis AG

- LyondellBasell Industries Holdings B.V.

- DAEHACOM Co., Ltd.

- GS Caltex Corporation

Competitive Benchmarking

Operating Strategies

Competitive Edge

Weakness

Mature Players: Mitsui Chemical, Inc., Exxon Mobil Corporation, Avient Corporation

- Broad portfolio coverage across filled, reinforced, impact-modified, and specialty polypropylene compounds.

- Strong integration across resin production, additives, and downstream compounding systems.

- Investment in recyclable, lightweight, and application-specific formulations for automotive, packaging, and industrial users.

- Strong brand recognition and deep technical credibility.

- Large-scale manufacturing improves supply security and cost efficiency.

- Broad customer reach across multiple end-use sectors reduces dependency risk.

- Large operating structures can slow adaptation to niche demand.

- Exposure to resin and energy price fluctuations affects profitability.

- Commodity-grade competition limits pricing power in some segments.

Emerging Players: IRPC Public Company Limited, DAEHACOM Co., Ltd.

- Focus on targeted regional demand and application-specific compound grades.

- Flexible production structures that allow adaptation to customer requirements.

- Emphasis on cost-sensitive industrial and molded part applications.

- Greater responsiveness to regional customer needs.

- Leaner structures can support more competitive pricing in selected markets.

- Ability to serve niche or localized demand pockets efficiently.

- Smaller scale reduces leverage in global procurement programs.

- Narrower geographic footprint limits diversification.

- Lower brand visibility versus multinational suppliers.

Recent Developments

-

In June 2025, Mitsui Chemicals’ Advanced Composites opened an MXN 250 million (about USD 14.3 million) production and logistics plant in Aguascalientes, Mexico, raising annual output by 9,000 tons of TPO and polypropylene compounds to serve local vehicle manufacturers and regional OEM supply chains.

-

In March 2025, Rialti (under Borealis ownership) launched new mechanically recycled PCR/PIR hybrid polypropylene compounds for injection molding. The grades target automotive and consumer applications and expand Borealis’ sustainable Borcycle M portfolio with industrial-scale recycled PP capacity.

Polypropylene Compounds Market Report Scope

Report Attribute

Details

Market size value in 2025

USD 26.9 billion

Market size value in 2026

USD 28.9 billion

Revenue forecast in 2033

USD 44.3 billion

Growth rate

CAGR of 6.3% from 2026 to 2033

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion, volume in kilotons, and CAGR from 2026 to 2033

Report coverage

Revenue forecast, competitive landscape, growth factors, and trends

Segments covered

Product, application, end-use, region

Regional scope

North America; Europe; Asia Pacific; Latin America; Middle East & Africa

Country Scope

U.S.; Canada; Mexico; Germany; UK; France; Italy; Spain; Norway; Netherlands; China; India; Japan; Australia; South Korea; Thailand; Malaysia; Indonesia; Brazil; Argentina; Saudi Arabia; UAE, South Africa

Key companies profiled

Mitsui Chemical, Inc.; IRPC Public Company Limited; Exxon Mobil Corporation; Avient Corporation; Japan Polypropylene Corporation; SABIC; Trinseo S.A.; Sumitomo Chemical Co., Ltd.; Washington Penn; Borealis AG; LyondellBasell Industries Holdings B.V.; DAEHACOM Co., Ltd.; GS Caltex Corporation

Customization scope

Free report customization (equivalent to up to 8 analyst working days) with purchase. Addition or alteration to country, regional & segment scope

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Polypropylene Compounds Market Report Segmentation

This report forecasts revenue growth at the global, regional, and country levels and provides an analysis of the latest industry trends across sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global polypropylene compounds market report based on product, application, end-use, and region:

-

Product Outlook (Volume, Kilotons; Revenue, USD Million, 2021 - 2033)

-

Mineral filled PP compounds

-

Compounded TPO

-

Compounded TPV

-

Glass fiber reinforced

-

Talc filled

-

Others

-

-

Application Outlook (Volume, Kilotons; Revenue, USD Million, 2021 - 2033)

-

Fiber

-

Film & sheet

-

Raffia

-

Others

-

-

End-use Outlook (Volume, Kilotons; Revenue, USD Million, 2021 - 2033)

-

Automotive

-

Building & Construction

-

Electrical & Electronics

-

Textile

-

Others

-

-

Regional Outlook (Volume, Kilotons; Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

UK

-

Germany

-

France

-

Italy

-

Spain

-

Norway

-

Netherlands

-

-

Asia Pacific

-

China

-

Japan

-

India

-

Australia

-

Thailand

-

South Korea

-

Indonesia

-

Malaysia

-

-

Latin America

-

Brazil

-

Argentina

-

-

Middle East and Africa

-

Saudi Arabia

-

South Africa

-

UAE

-

-

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

Opportunity Assessment

Conducted a detailed opportunity review across automotive lightweighting, packaging, electrical components, appliances, industrial parts, and sustainable compound applications. The analysis evaluated demand growth, regional adoption trends, value-added grade potential, recycled content opportunities, and shifting customer requirements across end-use sectors.

Supported expansion planning and market prioritization. Identified high-growth application areas and underpenetrated demand pockets. Improved visibility into sustainability-led opportunities and premium compound segments. Enabled more focused product development and commercial targeting.

Trade Assessment

Assessed global and regional trade flows for polypropylene compounds by reviewing export-import patterns, sourcing routes, logistics dependencies, tariff influences, and supply chain concentration. The study also examined cross-border movement of compounding feedstocks, regional manufacturing clusters, and trade sensitivity linked to polymer availability and geopolitical factors.

Supported sourcing strategy and supply chain planning. Identified key exporting and importing regions. Improved understanding of trade dependence and procurement risk. Enabled better planning around logistics, supplier diversification, and market access.

Pricing Analysis

Delivered a pricing analysis for major polypropylene compound categories, including filled, reinforced, impact-modified, and specialty grades. The review covered feedstock cost trends, regional price spreads, production economics, import-export pricing differences, and the impact of energy and regulatory costs on margins. It also considered the pricing effect of recycled content and performance enhancement requirements.

Supported procurement optimization and commercial negotiation. Improved visibility into raw material exposure and pricing behavior across regions. Assisted in margin planning and supplier comparison. Enabled better response to cost volatility and product-specific pricing pressure.

Frequently Asked Questions About This Report

Asia Pacific dominated with a 36.7% market share in 2025.

Asia Pacific is the fastest-growing region over the forecast period.

The film & sheet segment held the largest market share of 32.5% in 2025, while raffia segment is anticipated to grow at a substantial CAGR of 6.4% through the forecast period.

The automotive segment dominated the market across the end-use segmentation in 2025, while electrical & electronics segment is expected to grow at a 6.3% CAGR over the forecast period.

Some key players operating in the polypropylene compounds market include Mitsui Chemical, Inc., IRPC Public Company Limited, Exxon Mobil Corporation, Avient Corporation, Japan Polypropylene Corporation, SABIC, Trinseo S.A., Sumitomo Chemical Co., Ltd., Washington Penn, Borealis AG, LyondellBasell Industries Holdings B.V., DAEHACOM Co., Ltd., and GS Caltex Corporation.

The global polypropylene compounds market size was estimated at USD 26.9 billion in 2025 and is expected to reach USD 28.9 billion in 2026.

The global polypropylene compounds market is expected to grow at a compound annual growth rate of 6.3% from 2026 to 2033 to reach USD 44.3 billion by 2033.

Mineral filled PP compounds dominated the market across all product segments in terms of revenue, accounting for a 29.5% market share in 2025, and is forecasted to grow at a 6.8% CAGR from 2026 to 2033.

Rising demand from the electrical and electronics industry is another key driver for the polypropylene (PP) compounds market. PP compounds are widely used in appliance housings, connectors, and cable insulation due to their cost efficiency, electrical insulation properties, and design flexibility.

About the Author(s)

Plastics, Polymers & Resins Research Team

Bulk Chemicals · Plastics, Polymers & ResinsThis report was authored by the plastics, polymers & resins research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the plastics, polymers & resins segment of the bulk chemicals industry. All findings are based on proprietary bulk chemicals databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.