- Home

- »

- Plastics, Polymers & Resins

- »

-

Rigid Plastic Packaging Market Size Report, 2026-2033GVR Report cover

![Rigid Plastic Packaging Market (2026 - 2033)Report]()

Rigid Plastic Packaging Market (2026 - 2033)

Size, Share & Trends Analysis Report By Material (PET, PE, PP, PVC, PS, Bioplastics), By Product (Extrusion, Injection Molding), By Application (Food, Beverages), By Region, And Segment Forecasts

Market Size, 2025

$252.6BMarket Estimate, 2026

$261.7BMarket Forecast, 2033

$321.2BCAGR, 2026–2033

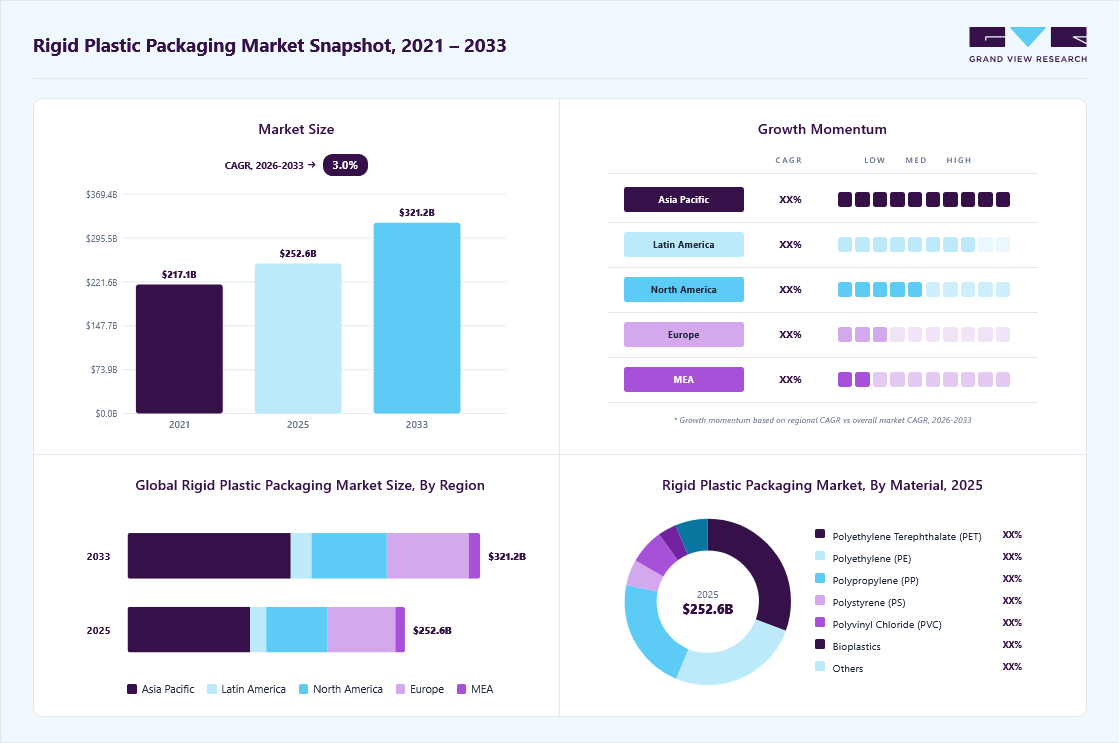

3.0%Rigid Plastic Packaging Market Summary

The global rigid plastic packaging market size was valued at USD 252.6 billion in 2025 and is projected to grow from USD 261.7 billion in 2026 to USD 321.2 billion by 2033, at a CAGR of 3.0% from 2026 to 2033. Asia Pacific dominated the global market with the largest revenue share of 44.2% in 2025. Rising demand for packaged food on account of growing preference toward ready-to-eat food products and increased adoption of plastic as a material in rigid packaging products are expected to support market growth.

Key Market Trends & Insights

- By material: polyethylene terephthalate (PET) segment led the market with the largest revenue share of 30.6% in 2025.

- By product: Bottles & Jars segment led the market with the largest revenue share of 51.5% in 2025.

- By application: Food segment led the market with the largest revenue share of 26.9% in 2025.

Regional Highlights

- Largest regional market: Asia Pacific (44.2% revenue share, 2025)

- By country: The rigid plastic packaging market in the China held the largest share in the Asia Pacific region in 2025.

Market Size & Forecast

- Market Size in 2025: USD 252.6 Billion

- Estimated Market Size in 2026: USD 261.7 Billion

- Projected Market Size by 2033: USD 321.2 Billion

- CAGR (2026-2033): 3.0%

The global market for rigid plastic packaging is anticipated to experience consistent growth, fueled by a rising need from the food and beverage industry for packaging that is durable, tamper-proof, and lightweight. The expansion of e-commerce and retail is expected to further enhance the demand for protective and ready-to-shelf rigid containers, particularly for personal care, pharmaceutical, and electronic goods.Furthermore, the growth of e-commerce and retail distribution channels is anticipated to drive the need for protective and stackable rigid packaging formats, especially in industries such as personal care, pharmaceuticals, and electronics. These sectors depend significantly on packaging that can endure the stresses of transportation while preserving brand aesthetics.

")

In addition, regulatory requirements set by organizations such as the FDA and EPA are encouraging businesses to implement compliant, high-performance rigid plastics for the safe storage and distribution of consumables and delicate products. These regulations are likely to promote the development and adoption of food-grade and medical-grade rigid packaging solutions.

Market Dynamics

The rigid plastic packaging market is experiencing steady growth driven by increasing demand from the food & beverage, healthcare, personal care, and household products industries, where durable, lightweight, and cost-effective packaging solutions are essential for product protection and shelf-life extension. Rising consumption of packaged and convenience foods, expanding pharmaceutical production, and the growth of e-commerce are supporting market expansion. At the same time, manufacturers are investing in recyclable, reusable, and post-consumer recycled (PCR) plastic packaging to address evolving sustainability goals and regulatory requirements. However, concerns regarding plastic waste, stringent environmental regulations, and growing competition from alternative packaging materials continue to challenge market growth. Technological advancements in lightweighting, barrier performance, and circular packaging solutions are creating new opportunities for innovation and long-term market development.

The increasing demand for packaged, processed, and convenience foods is a major driver of the market. Rigid plastic containers, bottles, jars, trays, and tubs are widely used across food and beverage applications due to their durability, lightweight nature, cost efficiency, and ability to protect products from contamination and physical damage. Changing consumer lifestyles, urbanization, and the growing preference for ready-to-eat and on-the-go food products have significantly increased the need for reliable packaging solutions that can maintain product quality and extend shelf life.

The expansion of modern retail channels, e-commerce grocery platforms, and beverage consumption is further strengthening demand for rigid plastic packaging. Manufacturers are increasingly adopting advanced packaging formats with improved barrier properties, tamper-evident features, and enhanced convenience to meet evolving consumer expectations. The material’s versatility, compatibility with high-speed production processes, and ability to support attractive product presentation continue to make rigid plastic packaging a preferred choice for food and beverage companies worldwide.

A significant restraint for the market is the increasing regulatory pressure and growing public concern regarding plastic waste and environmental sustainability. Governments across multiple regions are implementing stricter regulations on single-use plastics, extended producer responsibility (EPR) programs, recycled content requirements, and waste management practices, which are increasing compliance costs for packaging manufacturers. At the same time, rising consumer preference for environmentally friendly packaging alternatives such as paper-based, biodegradable, and reusable materials is creating competitive pressure on traditional rigid plastic packaging solutions. These factors are compelling manufacturers to invest heavily in sustainable materials, recycling infrastructure, and product redesign initiatives, which can impact profit margins and slow market growth in certain applications.

The growing emphasis on sustainability presents a significant opportunity for the market. Brand owners, retailers, and regulatory bodies are increasingly promoting the use of recyclable packaging, post-consumer recycled (PCR) plastics, and circular economy practices to reduce environmental impact. This shift is encouraging packaging manufacturers to develop innovative rigid plastic solutions that incorporate higher recycled content while maintaining product performance, safety, and aesthetics. Advances in recycling technologies, material processing, and lightweight packaging design are enabling companies to meet sustainability targets and evolving consumer expectations. As industries such as food & beverage, healthcare, and personal care continue to seek environmentally responsible packaging options, demand for sustainable rigid plastic packaging is expected to create substantial growth opportunities for market participants.

Market Concentration & Characteristics

Prominent players operating in rigid plastic packaging industry include Berry Global Inc., Amcor plc, Sonoco Products Company, ALPLA, WINPAK LTD, Nuplas Industries, DS Smith, Genpak, SILGAN PLASTICS, Anchor Packaging LLC, and PLASTIPAK HOLDINGS, INC.

Global rigid plastic packaging industry is highly fragmented with presence of significant number of packaging manufacturers. Companies operational in this market space are focusing developing new products catering to changing regulatory landscape, indicating a high impact level of regulations. For instance, in December 2023, Novolex, a U.S. based packaging manufacturer launched food packaging containers having 10% post-consumer recycled plastic content. According to Association of Plastic Recyclers as of 2023, four states of the U.S. have passed laws mandating inclusion of recycled content in plastic packaging. Also, active proposals related to recycled plastic-based packaging are progressing in European Union and Canada, which pushes companies to develop rigid packaging complying to these laws.

Significant presence of companies also influences level of mergers and acquisitions. Well-established mature players which are seen to acquire emerging or small local level companies to grow their market presence. For instance, in October 2023, Greif Inc announced its intent and its ongoing discussions to acquire small plastic containers and jerrycan manufacturer PACKCHEM Group SAS for a transaction valued at USD 538.0 million.

Analyst Perspective

The rigid plastic packaging market is expected to maintain steady growth, driven by increasing demand from the food & beverage, pharmaceutical, personal care, and industrial sectors for durable, lightweight, and cost-effective packaging solutions. The market continues to benefit from rising consumption of packaged products, expanding e-commerce activities, and the need for enhanced product protection, shelf-life extension, and supply chain efficiency. Simultaneously, sustainability has emerged as a key industry focus, prompting manufacturers to invest in recyclable materials, post-consumer recycled (PCR) content, lightweight packaging designs, and circular economy initiatives. While regulatory pressures related to plastic waste present challenges, ongoing advancements in material technology, recycling infrastructure, and sustainable packaging innovation are creating new growth opportunities. Companies that successfully combine performance, regulatory compliance, and environmental responsibility will be well positioned to strengthen their competitive standing and capture long-term market growth.

Material Insights

Based on material, the market is segmented into polyethylene terephthalate (PET), polypropylene (PP), polyethylene (PE), polyvinyl chloride (PVC), polystyrene (PS), bioplastics, and others. Polyethylene terephthalate (PET) segment led the market with the largest revenue share of 30.6% in 2025. Properties such as lightweight, recyclability, durability, along with its excellent transparency makes it a popular choice for end users, which require product visible packaging, thereby contributing to its high market share.

Bioplastics are expected to progress at a CAGR of 5.1% from 2026 to 2033. High growth rate can be attributed to growing concerns related to plastic packaging waste pollution and its environmental impacts. Governments worldwide are imposing stringent regulations such as ban on single use plastics, which can push rigid packaging manufacturers to shift from fossil fuel-based plastics to plant derived bioplastics.

Product Insights

Based on product, the market is segmented into trays & clamshells; bottles & jars; tubs, cups, and pots; pallets; drums & barrels; crates; and pallets among others. The bottles & Jars segment led the market with the largest revenue share of 51.5% in 2025. The bottles & jars segment demand is driven by their versatility. In terms of versatility, bottles & jars are available in variety of sizes and shapes, catering to a vast range of end-use industries such as beverage, cosmetics, pharmaceutical, and industrial. In addition, its high market share is also correlational to the consumption of beverages. High population results in increased beverage consumption, directly influencing demand for bottles & jars.

Plastic pallets and other products are expected to progress with a significant CAGR of 2.4% over forecast period. High growth rate can be attributed to increasing shift of end-use industries from traditional wooden pallets to plastic pallets on account of rising logistics costs and high price of wooden pallets.

Application Insights

Based on application, the market is segmented into food, beverages, pharmaceutical & healthcare, personal care & cosmetics, automotive, building & construction, and other applications. Food segment led the market with the largest revenue share of 26.9% in 2025. This positive outlook is due to growing demand for packaged food products and requirement for sturdy packaging products to protect food during transit. Furthermore, rise in online food delivery industry is also expected to contribute to high dominance of food in rigid plastic packaging industry.

The pharmaceutical & healthcare application segment is expected to progress with a CAGR of 3.5% over the forecast period. High growth rate can be attributed to growing use of plastic based rigid packaging products such as bottles, jars, trays in packaging of sensitive pharmaceutical dosages and medical devices. Excellent barrier properties along with lightweight of plastics contribute to their high adoption in pharmaceutical & healthcare rigid packaging.

Regional Insights

Asia Pacific dominated the rigid plastic packaging market with the largest revenue share of 44.2% in 2025. The region is likely to dominate the industry over the forecast period. Asia Pacific boasts major plastic resin manufacturers such as LG Chem, TORAY INDUSTRIES, INC, Reliance Industries Limited, Mitsui Chemicals, Inc, Indorama Ventures Public Company Limited, BASF SE, and China Petrochemical Corporation among others creating strong raw material supply network, thereby contributing to the market. Furthermore, the region boasts a rapidly growing population, particularly in countries like China and India, creating a huge consumer base for various products, from food and beverages to personal care items, creating a strong demand for rigid plastic packaging.

The rigid plastic packaging market in the China held the largest share in the Asia Pacific region in 2025. The China rigid plastic packaging industry is anticipated to experience consistent growth, fueled by heightened demand from the food and beverage sector, growing urbanization, and changing consumer habits. As e-commerce and food delivery services expand, the requirement for sturdy, lightweight, and protective packaging options is expected to rise, making rigid plastics a favored choice.

The rigid plastic packaging industry in Southeast Asia is expected to progress at a significant CAGR over forecast period. This is attributed to various factors such as rising urban population and increasing cosmetic trend. Thailand is a major original equipment manufacturer (OEM) for international cosmetic brands. There are over 762 cosmetics manufacturing plants is Thailand as per Thai Cosmetic Cluster, indicating a strong personal care & cosmetics sector growth. This can simultaneously influence rigid plastic packaging industry growth related to it.

North America Rigid Plastic Packaging Market Trends

North American rigid plastic packaging industry is expected to progress at a moderate CAGR. While growth is expected, sustainability concerns and changing consumer preferences are driving innovation and adaptation within the industry. For instance, growing environmental awareness and stringent regulations are pushing manufacturers towards sustainable alternatives like recycled plastics and bioplastics.

The U.S. rigid plastic packaging industry dominated the North American regional space, accounting for a share of over 80.90% in 2025. High share is driven by growing demand of functional beverages in country and increased demand for packaged food products.

The rigid plastic packaging industry in Canada is driven by growing exports of fruits. Canada has free trade agreements with several major markets, which facilitates export growth. The USMCA agreement eliminates tariffs for agricultural exports which can promote agricultural produce export and contribute to rigid plastic packaging industry.

Europe Rigid Plastic Packaging Market Trends

The rigid plastic packaging industry in the Europeis anticipated to grow over the forecast period.According to European Commission, the pharmaceutical sector is a leading contributor to region’s economy. Pharmaceutical strategy for Europe adopted in November 2020 aims to boost research and technologies to boost local pharmaceutical sector which presents positive outlook for the market.

The rigid plastic packaging industry in Germany is anticipated to grow on account of rising organic packaged food market. Germany dominated the market in Europe. Growing awareness related to organic farming and its associated health benefits are expected to create a strong market forecast for organic products such as organic spread, ready meals, baby food, dairy products, organic baked goods, and confectionary.

Central & South America Rigid Plastic Packaging Market Trends

The rigid plastic packaging industry in Latin America is estimated to grow over the forecast period owing to steady economic growth, leading to rising disposable incomes and increased consumer spending. This fuels demand for packaged goods. According to National Library of Medicine, consumption of carbonated soft drinks has increased significantly, thus contributing to demand of rigid plastic packaging products.

The rigid plastic packaging industry in Brazil dominated the Central & South American regional space in 2025. Brazil has emerged as an attractive market for personal care and cosmetics production. According to Associação Brasileira da Indústria de Higiene (Abhipec) international trade of Brazil’s personal care & cosmetic products registered a growth of 30.9% in first quarter of 2023 compared to the same period in 2022. Skin creams and tanning products recorded highest sales percentage, thus presenting positive market forecast for rigid plastic packaging products used for packaging personal care & cosmetic products.

Middle East & Africa Rigid Plastic Packaging Market Trends

The rigid plastic packaging industry in Middle East & Africa is growing due to rising bottled mineral water consumption in region. Lack of confidence in quality of water supplied through pipeline and tankers as well as growing tourism sector in Middle East & Africa is expected to contribute to bottled water market and relative rigid plastic packaging industry growth.

The rigid plastic packaging industry in Saudi Arabia is expected to grow at a lucrative CAGR due to high production of dairy products within the country. Saudi Arabia dominated the rigid plastic packaging industry in 2025 in the Middle East & Africa region. Saudi Arabia is among the leading dairy products exporting countries in Middle East and across the globe.

The rigid plastic packaging industry in South Africa is expected to progress with a significant CAGR over forecast period. Growing carbonated soft drink consumption is encouraging entry of soft drink manufacturer such as Varun Beverages into South Africa, presenting positive rigid plastic packaging forecast.

Key Rigid Plastic Packaging Company Insights

The rigid plastic packaging industry is highly fragmented with a significant presence of global as well as local companies offering various types of rigid plastic packaging products. Major players operating in rigid plastic packaging industry undertake various strategies such as mergers, acquisitions, geographical expansion, new product launches, and joint ventures to strengthen their market presence.

-

In March 2025, LyondellBasell introduced Pro-fax EP649U, a novel polypropylene impact copolymer tailored for the rigid packaging sector. This cutting-edge product is specifically engineered for thin-walled injection molding, making it perfect for food packaging uses. Pro-fax EP649U boasts excellent flow characteristics and rapid crystallization, allowing for the efficient manufacture of thin-walled containers while improving both productivity and the quality of the final product. The additive formulation in Pro-fax EP649U promotes smooth mold release, minimizes static, and enhances downstream handling on high-speed filling lines.

-

In February 2025, Berry Global Group Inc. finalized its purchase of CMG Plastics, a company specializing in rigid packaging manufacturing. Berry continues to expand through acquisitions, as it approaches a key milestone in its acquisition by Amcor plc. Today, shareholders from both firms are set to vote on the all-stock agreement valued at USD 8.4 billion. The boards of directors for both companies have unanimously endorsed the deal. The acquisition of Berry by Amcor, which is anticipated to finalize by mid-2025, is projected to generate USD 650 million in annual cost savings and additional synergies within three years.

Key Rigid Plastic Packaging Companies

The following key companies have been profiled for this study on the rigid plastic packaging market.

-

Berry Global Inc.

-

Amcor plc

-

Pactiv Evergreen Inc.

-

Sonoco Products Company

-

ALPLA

-

WINPAK LTD

-

Nuplas Industries

-

DS Smith

-

Genpak

-

SILGAN PLASTICS

-

Anchor Packaging LLC

-

PLASTIPAK HOLDINGS, INC.

-

Greif

-

Gerresheimer AG

-

Manjushree Technopack Ltd

-

Mold-Tek Packaging Ltd

-

Greiner Packaging

-

Takween Advanced Industries

-

Ladain Alyamamah Plastic Factory

-

Arabian Plastic Industrial Company Co

-

Crown Packaging Int’l

-

S.E.A. Global Pte. Ltd

-

Dynapackasia

Competitive Benchmarking

Category

Operating Strategies

Competitive Edge

Weakness

Established Players (Berry Global Inc., Amcor plc, Pactiv Evergreen Inc., Sonoco Products Company, ALPLA, Winpak Ltd., DS Smith, Genpak, Silgan Plastics, Anchor Packaging LLC, Plastipak Holdings, Inc., Greif, Gerresheimer AG, Greiner Packaging, Takween Advanced Industries, Manjushree Technopack Ltd, and Mold-Tek Packaging Ltd)

- Invest in large-scale production facilities, automation, and sustainable packaging technologies to improve efficiency and meet evolving customer requirements.

- Pursue acquisitions, strategic partnerships, and long-term supply agreements to strengthen global market presence and customer retention.

- Extensive manufacturing networks and diversified product portfolios enable efficient servicing of multiple end-use industries across regions.

- Strong financial resources and advanced R&D capabilities support innovation, regulatory compliance, and sustainable packaging development.

- High fixed operating costs and complex organizational structures can reduce operational agility and increase overhead expenses.

- Greater exposure to sustainability regulations and fluctuations in resin prices can impact profitability and compliance costs.

Emerging Players (Nuplas Industries, Ladain Alyamamah Plastic Factory, Arabian Plastic Industrial Company Co, Crown Packaging Int’l, S.E.A. Global Pte. Ltd, and Dynapack Asia)

- Focus on regional expansion and customer-specific packaging solutions to build market share in targeted segments.

- Emphasize operational flexibility and cost-effective manufacturing to address niche and mid-sized customer requirements.

- Faster decision-making and greater responsiveness allow quick adaptation to changing customer needs and market trends.

- Competitive pricing and customized product offerings help secure business in specialized applications and regional markets.

- Limited capital resources and production capacity can constrain expansion and technology investments.

- Smaller customer bases and lower brand recognition may reduce bargaining power and competitiveness against established industry leaders.

Rigid Plastic Packaging Market Report Scope

Report Attribute

Details

Market size in 2025

USD 252.6 billion

Estimated market size in 2026

USD 261.7 billion

Projected market size by 2033

USD 321.2 billion

Growth rate

CAGR of 3.0% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Material, product, application, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; Germany; UK; France; Italy; Spain; China; Japan; India; South Korea; Australia; Brazil; Argentina; Saudi Arabia; South Africa; UAE

Key companies profiled

Berry Global Inc.; Amcor plc; Pactiv Evergreen Inc.; Sonoco Products Company; ALPLA; WINPAK LTD; Nuplas Industries; DS Smith; Genpak; SILGAN PLASTICS; Anchor Packaging LLC; PLASTIPAK HOLDINGS, INC.; Greif; Gerresheimer AG; Manjushree Technopack Ltd; Mold-Tek Packaging Ltd; Greiner Packaging; Takween Advanced Industries; Ladain Alyamamah Plastic Factory; Arabian Plastic Industrial Company Co; Crown Packaging Int’l; S.E.A. Global Pte. Ltd; Dynapackasia

Customization scope

Free report customization (equivalent up to 8 analysts' working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Rigid Plastic Packaging Market Report Segmentation

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of latest industry trends in each sub-segment from 2021 to 2033. For this study, Grand View Research has segmented the global rigid plastic packaging market report based on material, product, application, and region:

-

Material Outlook (Volume, Kilotons; Revenue, USD Million, 2021 - 2033)

-

Polyethylene Terephthalate (PET)

-

Polyethylene (PE)

-

Polypropylene (PP)

-

Polystyrene (PS)

-

Polyvinyl Chloride (PVC)

-

Bioplastics

-

Others

-

-

Product Outlook (Volume, Kilotons; Revenue, USD Million, 2021 - 2033)

-

Bottles & Jars

-

Trays & Clamshells

-

Tubs, Cups, and Pots

-

Pallets

-

Drums & Barrels

-

Crates

-

Others

-

-

Application Outlook (Volume, Kilotons; Revenue, USD Million, 2021 - 2033)

-

Food

-

Beverages

-

Pharmaceutical & Healthcare

-

Personal Care & Cosmetics

-

Automotive

-

Building & Construction

-

Others

-

-

Regional Outlook (Volume, Kilotons; Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

France

-

Italy

-

Spain

-

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

Australia

-

Southeast Asia

-

-

Central & South America

-

Brazil

-

Argentina

-

-

Middle East & Africa

-

Saudi Arabia

-

UAE

-

South Africa

-

-

Research Methodology

Segment Definition

Segment - Material

Revenue capture definition

Polyethylene Terephthalate (PET)

Revenue generated from the sale of rigid plastic packaging manufactured using polyethylene terephthalate (PET), valued for its clarity, strength, lightweight properties, and recyclability. This segment includes PET bottles, jars, containers, and other packaging formats used in food, beverage, personal care, and pharmaceutical applications.

Polyethylene (PE)

Revenue generated from the sale of rigid plastic packaging produced from polyethylene materials, including high-density polyethylene (HDPE) and low-density polyethylene (LDPE). This segment includes containers, bottles, drums, and industrial packaging solutions used across food, healthcare, chemical, and household product applications.

Polypropylene (PP)

Revenue generated from the sale of rigid plastic packaging made from polypropylene, known for its durability, heat resistance, and chemical stability. This segment includes tubs, cups, pots, caps, closures, and food packaging products used in consumer, industrial, and healthcare sectors.

Polystyrene (PS)

Revenue generated from the sale of rigid plastic packaging manufactured from polystyrene materials. This segment includes trays, containers, cups, and protective packaging products used in food service, retail packaging, and consumer goods applications.

Polyvinyl Chloride (PVC)

Revenue generated from the sale of rigid plastic packaging produced using polyvinyl chloride (PVC), offering transparency, durability, and barrier performance. This segment includes blister packs, containers, and specialized packaging solutions used in pharmaceutical, healthcare, and consumer product applications.

Bioplastics

Revenue generated from the sale of rigid plastic packaging manufactured from bio-based or biodegradable plastic materials. This segment includes sustainable bottles, containers, trays, and other packaging formats designed to reduce environmental impact across food, beverage, and consumer goods applications.

Others

Revenue generated from the sale of rigid plastic packaging manufactured from alternative materials not classified under PET, PE, PP, PS, PVC, or bioplastics. This segment includes specialized engineering plastics and customized packaging solutions for niche industrial and commercial applications.

Segment - Product

Revenue capture definition

Bottles & Jars

Revenue generated from the sale of rigid plastic bottles and jars used for packaging beverages, food products, pharmaceuticals, personal care products, and household chemicals.

Trays & Clamshells

Revenue generated from the sale of rigid plastic trays and clamshell packaging designed to provide product visibility, protection, and convenience. This segment includes packaging used for fresh produce, bakery products, ready meals, electronics, and retail goods.

Tubs, Cups, and Pots

Revenue generated from the sale of rigid plastic tubs, cups, and pots used for dairy products, desserts, ready-to-eat foods, personal care products, and specialty consumer goods.

Pallets

Revenue generated from the sale of rigid plastic pallets used for the storage, handling, and transportation of goods across manufacturing, logistics, food processing, and retail industries.

Drums & Barrels

Revenue generated from the sale of rigid plastic drums and barrels designed for the storage and transportation of liquids, chemicals, food ingredients, and industrial materials.

Crates

Revenue generated from the sale of rigid plastic crates used for material handling, warehousing, distribution, and transportation of agricultural, food, beverage, and industrial products.

Others

Revenue generated from the sale of other rigid plastic packaging products not included in the above categories. This segment includes pails, bins, intermediate bulk containers (IBCs), caps, closures, and customized packaging solutions.

Segment - Application

Revenue capture definition

Food

Revenue generated from the sale of rigid plastic packaging used for food products, including fresh produce, dairy products, bakery items, confectionery, frozen foods, and ready-to-eat meals requiring protection, preservation, and shelf-life enhancement.

Beverages

Revenue generated from the sale of rigid plastic packaging used for bottled water, carbonated soft drinks, juices, dairy beverages, alcoholic beverages, and functional drinks. This segment includes bottles, caps, closures, and related packaging formats.

Pharmaceutical & Healthcare

Revenue generated from the sale of rigid plastic packaging used for pharmaceutical products, medical devices, diagnostic products, and healthcare supplies. This segment includes bottles, containers, blister packaging components, and specialized healthcare packaging solutions.

Personal Care & Cosmetics

Revenue generated from the sale of rigid plastic packaging used for skincare, haircare, cosmetics, fragrances, and personal hygiene products. This segment includes bottles, jars, tubs, dispensers, and cosmetic containers.

Automotive

Revenue generated from the sale of rigid plastic packaging used for the storage, protection, and transportation of automotive components, spare parts, lubricants, and maintenance products throughout the automotive supply chain.

Building & Construction

Revenue generated from the sale of rigid plastic packaging used for construction chemicals, adhesives, sealants, coatings, hardware products, and other building materials requiring durable storage and transportation solutions.

Others

Revenue generated from the sale of rigid plastic packaging used across additional industries not covered under the above categories, including consumer goods, electronics, agriculture, industrial manufacturing, and logistics applications.

Estimation Model

Layer Name

Key Question

Description

End-Use Consumption Layer

What forms the demand base?

Identify global consumption volumes of products packaged in rigid plastic formats across key end-use industries, including food, beverages, pharmaceuticals & healthcare, personal care & cosmetics, automotive, building & construction, and other industrial sectors. This layer establishes the total addressable demand for rigid plastic packaging driven by product production, distribution, storage, and retail requirements.

Packaging Penetration Layer

Where is rigid plastic packaging utilized?

Estimate the penetration of rigid plastic packaging relative to alternative materials such as flexible plastics, paperboard, glass, and metal across various applications and regions. Assess adoption rates of PET, PE, PP, PS, PVC, bioplastics, and other materials based on product protection needs, shelf-life requirements, regulatory standards, sustainability initiatives, and cost considerations.

Packaging Volume Layer

How much rigid plastic packaging is consumed?

Analyze packaging consumption volumes by material type, product format, and application. Evaluate the usage of bottles & jars, trays & clamshells, tubs, cups & pots, pallets, drums & barrels, crates, and other rigid plastic packaging formats. Volume demand is influenced by manufacturing output, consumer consumption patterns, logistics requirements, e-commerce growth, and packaging intensity across industries.

Revenue Layer

How is market revenue generated?

Market revenue is quantified through the sale of rigid plastic packaging products across diverse end-use industries. Revenue generation includes standard and customized packaging solutions manufactured from PET, PE, PP, PS, PVC, bioplastics, and other materials. Growth is supported by increasing demand for lightweight, durable, recyclable, and high-performance packaging solutions, along with value-added features such as barrier protection, lightweighting, sustainability enhancements, and advanced packaging designs.

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

Regional Segmentation Analysis

Delivered detailed market sizing, growth forecasts, consumption trends, regulatory developments, and application-level demand analysis across North America, Europe, Asia Pacific, Central & South America, and Middle East & Africa, including key country-level assessments within major regional markets.

Enabled identification of high-growth regions, demand concentration areas, investment opportunities, and region-specific market dynamics to support expansion and resource allocation strategies.

Cross-Segmentation Analysis

Provided comprehensive analysis across Material (Polyethylene Terephthalate (PET), Polyethylene (PE), Polypropylene (PP), Polystyrene (PS), Polyvinyl Chloride (PVC), Bioplastics, Others), Product (Bottles & Jars, Trays & Clamshells, Tubs, Cups & Pots, Pallets, Drums & Barrels, Crates, Others), Application (Food, Beverages, Pharmaceutical & Healthcare, Personal Care & Cosmetics, Automotive, Building & Construction, Others), and Region.

Delivered granular insights into the most attractive material-product-application combinations, helping clients identify high-growth niches, emerging demand clusters, and portfolio expansion opportunities.

Opportunity Assessment

Identified emerging opportunities across recyclable and sustainable rigid plastic packaging solutions, bioplastics adoption, lightweight packaging formats, food and beverage packaging demand, pharmaceutical packaging expansion, and industrial logistics applications.

Enabled prioritization of high-potential growth areas, investment opportunities, product innovation initiatives, and long-term market development strategies.

Frequently Asked Questions About This Report

The Polyethylene Terephthalate segment led the market with a 30.6% revenue share in 2025 in the global rigid plastic packaging market.

Bottles & Jars segment held the largest revenue share of 51.5% in 2025 in the global rigid plastic packaging market

Food segment held the largest revenue share of 26.9% in 2025 in the global rigid plastic packaging market

Key players in the rigid plastic packaging market include Berry Global Inc., Amcor plc, Pactiv Evergreen Inc., Sonoco Products Company, ALPLA, WINPAK LTD, Nuplas Industries, DS Smith, Genpak, SILGAN PLASTICS, Anchor Packaging LLC, PLASTIPAK HOLDINGS, INC., Greif, Gerresheimer AG, Manjushree Technopack Ltd, Mold-Tek Packaging Ltd, Greiner Packaging, Takween Advanced Industries, Ladain Alyamamah Plastic Factory, Arabian Plastic Industrial Company Co, Crown Packaging Int’l, S.E.A. Global Pte. Ltd, and Dynapackasia.

The global rigid plastic packaging market size was valued at USD 252.6 billion in 2025 and is estimated at USD 261.7 billion for 2026.

The global rigid plastic packaging market is expected to grow at a CAGR of 3.0% from 2026 to 2033, reaching USD 321.2 billion by 2033.

Key factors driving the rigid plastic packaging market include rising demand for packaged food and beverages, growing pharmaceutical and healthcare production, expanding e-commerce activities, and increasing use of durable, lightweight, and cost-effective packaging solutions.

Asia Pacific dominated the rigid plastic packaging market with a 44.2% revenue share in 2025.

About the Author(s)

Plastics, Polymers & Resins Research Team

Bulk Chemicals · Plastics, Polymers & ResinsThis report was authored by the plastics, polymers & resins research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the plastics, polymers & resins segment of the bulk chemicals industry. All findings are based on proprietary bulk chemicals databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.