- Home

- »

- Plastics, Polymers & Resins

- »

-

Styrenic Block Copolymer Market Size Report, 2026-2045GVR Report cover

![Styrenic Block Copolymer Market (2026 - 2045)Report]()

Styrenic Block Copolymer Market (2026 - 2045)

Size, Share & Trends Analysis Report By Product (Styrene-butadiene-styrene, Styrene-isoprene-styrene, HSBC), By Application (HSBC, SBS, SIS), By Region, And Segment Forecasts

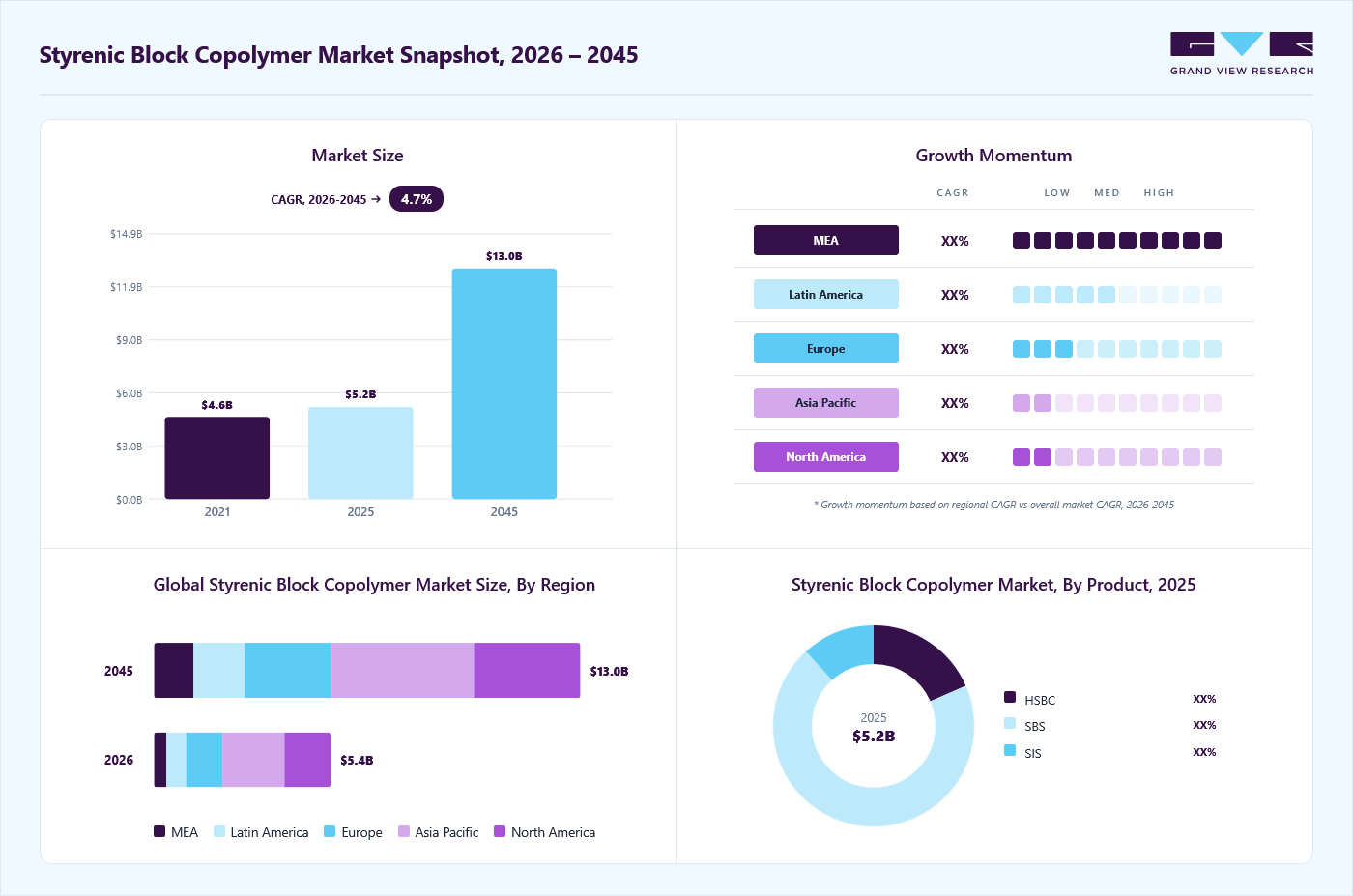

Market Size, 2025

$5.2BMarket Estimate, 2026

$5.3BMarket Forecast, 2045

$13.0BCAGR, 2026–2045

4.7%Styrenic Block Copolymer Market Summary

The global styrenic block copolymer market size was valued at USD 5.2 billion in 2025 and is projected to grow from USD 5.3 billion in 2026 to USD 13.0 billion by 2045, at a CAGR of 4.7% from 2026 to 2045. Asia Pacific dominated the market, accounting for 34.9% revenue share in 2025. The styrenic block copolymers (SBC) are produced by ionic copolymerization of styrene, isoprene, and butadiene and are considered one of the largest volume commercial thermoplastic elastomers.

Key Market Trends & Insights

- By product: The SBS segment dominated the market across product segmentation in terms of revenue, accounting for 69.7% market share in 2025.

- By application: The healthcare application segment is expected to grow at a CAGR of 5.9% from 2026 to 2045 in terms of revenue.

Regional Highlights

- Largest regional market: Asia Pacific (34.9% revenue share, 2025)

- Fastest-growing regional market: Middle East & Africa (highest CAGR, 2026-2045)

- The styrenic block copolymer industry in the China held the largest revenue share in 2025.

Market Size & Forecast

- Market size in 2025: USD 5.2 Billion

- Estimated market size in 2026: USD 5.3 Billion

- Projected market size by 2045: USD 13.0 Billion

- CAGR (2026-2045): 4.7%

The market is expected to be driven by the rising demand from various applications such as footwear, adhesives & sealants, paints & coatings, polymer modification, paving and roofing, toys, and medical devices.")

Demand for higher-performance styrenic block copolymers is shifting from commodity grades to engineered SEBS and SEPS grades that enable lightweighting and improved durability in transport and industrial applications. Buyers increasingly require low-carbon and mass-balance certified options to meet corporate scope 3 targets and regulatory disclosure. Design wins now hinge on validated lifecycle metrics and supply-chain traceability rather than base resin cost alone.

Drivers, Opportunities & Restraints

Styrenic block copolymers deliver unmatched tack, elasticity, and processability for pressure-sensitive adhesives, hot-melt systems, and bitumen modification. End-use expansion in packaging labels, construction membranes, and specialty tapes is lifting demand for grades with tailored molecular architecture and hydrogenation. Technical developments in SBC-based formulations continue to widen addressable applications and improve formulation economics for converters.

Manufacturers that convert existing capacity to accept certified renewable monomers can capture premium value from sustainability-focused converters. Localized ISCC Plus manufacturing footprints reduce carbon intensity claims and shorten lead times for regional customers. Investment in renewable-feedstock production and validated product carbon footprints creates a differentiated go-to offering for multinational brand owners seeking drop-in, lower-emission elastomer solutions.

The SBC value chain is exposed to feedstock cyclicality for styrene and diene monomers. Volatile ethylbenzene and butadiene markets can compress margins and force grade substitutions or reformulation costs for converters. Regulatory reviews on monomers and tighter emissions or recycling mandates increase compliance costs and raise barriers for smaller producers to remain competitive. These factors restrain near-term capacity additions and weigh on pricing stability.

Market Concentration & Characteristics

The market growth stage is medium, and growth is accelerating. The market exhibits fragmentation, with key players dominating the industry landscape. Major companies such as LCY Group, KRATON CORPORATION, ZEON CORPORATION, Asahi Kasei Corporation, China Petroleum & Chemical Corporation (Sinopec), INEOS, Styrolution Group GmbH, JSR Corporation, Korea Kumho Petrochemical Co., Ltd., TSRC, En Chuan Chemical Industries Co., Ltd., and others play a significant role in shaping the market dynamics. These leading players often drive innovation in the market by introducing new products, technologies, and materials to meet the industry's evolving demands.

Innovation in the styrenic block copolymer sector is pragmatic and application-led. Producers are moving beyond formulation tweaks to platform changes that lower lifecycle emissions and improve recyclability. Commercial-scale renewable-feedstock production and mass-balance certification enable drop-in, lower-carbon grades for customers with scope 3 targets. Research on recyclability and compatibilization is creating routes to reclaim SBCs from mixed waste streams and to produce tougher recyclate for high-value applications.

Substitution dynamics vary by end use and specification. For medical and wearable applications, thermoplastic polyurethane offers higher abrasion resistance and well-established medical-grade supply chains, prompting OEMs to prefer TPU where biocompatibility is critical. For automotive interiors and artificial leather, polyolefin elastomers provide a lower cost and fully polyolefin solution that eases recycling and reduces odor. Silicone and engineered olefin elastomers remain competitive where extreme temperature or chemical resistance is required.

Product Insights

The SBS segment dominated the market across product segmentation in terms of revenue, accounting for 69.7% market share in 2025, and is forecast to grow at a 4.4% CAGR from 2026 to 2045. Demand for styrene-butadiene-styrene grades is increasingly anchored to public works and resurfacing programs that mandate long service life and recycled content. Specifiers are asking for SBS-modified binders that enable higher reclaimed asphalt content while protecting rutting resistance and low temperature flexibility. Producers are responding with tailored high-styrene and oil-extended SBS grades to hit dosage economics and performance windows. Capacity investments announced by manufacturers reflect this pull from paving and roofing value chains.

The HSBC segment is expected to expand at a 5.5% CAGR over the forecast period. Hydrogenated styrenic block copolymers now attract demand where heat ageing, UV stability, and low odor are non-negotiable. End users in hot-filled packaging, high-temperature overmolding, and specialty adhesives prefer HSBC because hydrogenation removes unsaturation and improves oxidative stability. Compounders are formulating HSBC blends to meet higher service temperatures and extended lifetime claims. Regional capacity additions for hydrogenated grades aim to shorten supply chains and support just-in-time production for formulators.

Application Insights

The footwear segment led the market by application, accounting for 20.7% of revenue in 2025, and is projected to grow at a 4.3% CAGR from 2026 to 2045. Footwear brands are shifting specifications away from multi-component rubber constructs toward single-material TPE designs that simplify recycling and improve cost in use. SEBS and hydrogenated variants enable low-density foamed midsoles, resilient outsoles, and soft touch over molds while preserving injection and compression molding cycle efficiencies. Compounders provide tailor-made grades that deliver rebound, abrasion resistance, and coloration stability for high-volume production. This technical alignment with brand sustainability targets is accelerating material conversions across athletic and casual segments.

The healthcare segment is expected to grow at the fastest CAGR of 5.9% over the forecast period in the automotive styrenic block copolymer glazing market. Medical device makers favour SEBS and hydrogenated SBC-based TPEs when steam sterilisation, low extractables, and biocompatibility are required. Several TPE families meet ISO 10993 test protocols and support FDA 510(k) pathways for non-implant devices. Performance benefits include solvent resistance, improved seal integrity, and compatibility with overmolding and co-extrusion. These attributes shorten assembly steps and reduce leachable risks versus traditional PVC formulations, creating clear substitution opportunities across tubing, bags, seals, and instrument components.

Regional Insights

The Asia Pacific styrenic block copolymer market held the largest revenue share of 34.9% in 2025. The region is expected to grow at a CAGR of 4.5% over the forecast period. Growth across consumer electronics, footwear, and automotive electrification is supporting higher SBC demand in the Asia Pacific region. Regional brand owners are prioritizing lightweighting and soft-touch solutions that improve product differentiation and recyclability. Local compounders and polymer producers are expanding capacities and tailoring HSBC and SEBS grades to regional processing practices. Strategic site investments are focused on lowering lead times and offering certified renewable content to multinational converters operating in Asia.

China Styrenic Block Copolymer Market Trends

The styrenic block copolymer market in China dominated the Asia Pacific due to its large downstream synthetic rubber and tire industry, which underpins strong domestic demand for diene feedstocks and SBC intermediates. New domestic projects producing styrene-butadiene copolymers and integrated supply chains increase local availability and price competitiveness versus imports. State and provincial manufacturing growth supports capacity scale-ups, while local producers pursue vertical integration to secure monomer streams and meet fast-evolving OEM specifications. These shifts are rebalancing regional trade flows for SBC feedstocks.

North America Styrenic Block Copolymer Market Trends

The styrenic block copolymer market in North America is being driven by infrastructure and construction programs that require durable, high-performance modifiers for asphalt membranes, roofing, and pressure-sensitive adhesives. Producers report rising specification requests for higher styrene-content SBS grades to improve rutting resistance while enabling recycled content targets. Regional converters favor local, reliable supply and certified lower-carbon options to meet corporate procurement rules. Capacity add-backs and plant upgrades are shortening lead times for formulators.

The U.S. styrenic block copolymer market is supported by regulatory scrutiny of 1,3-butadiene, and tighter occupational controls are reshaping feedstock risk and commercial planning. The draft TSCA risk evaluation and subsequent peer review have raised compliance and monitoring expectations for producers and downstream compounders. Manufacturers are evaluating process controls and alternative sourcing to mitigate potential supply disruptions and to preserve access to critical monomers for SBS and hydrogenated grades. This dynamic is slowing rapid capacity expansion decisions.

Europe Styrenic Block Copolymer Market Trends

The styrenic block copolymer market in Europe is being shaped by circularity mandates and energy-intensive production economics. Regulators and industry bodies are tightening recycled content and emissions expectations, driving formulators to seek hydrogenated and compatibilized SBC solutions that improve recyclate performance. At the same time, announced closures and selective site rationalizations compress local upstream capacity. Producers are investing selectively in lower-carbon production and in compatibilization technology to retain formulators facing stricter EU rules.

Key Styrenic Block Copolymer Company Insights

The styrenic block copolymer industry is highly competitive, with several key players dominating the landscape. Major companies include LCY Group, KRATON CORPORATION, ZEON CORPORATION, Asahi Kasei Corporation, China Petroleum & Chemical Corporation (Sinopec), INEOS, Styrolution Group GmbH, JSR Corporation, Korea Kumho Petrochemical Co., Ltd., TSRC, and En Chuan Chemical Industries Co., Ltd. The styrenic block copolymer industry is characterized by a competitive landscape with several key players driving innovation and market growth. Major companies in this sector are investing heavily in research and development to enhance the performance, cost-effectiveness, and sustainability of their products.

Key Styrenic Block Copolymer Companies:

The following key companies have been profiled for this study on the styrenic block copolymer market.

- LCY Group

- KRATON CORPORATION

- ZEON CORPORATION

- Asahi Kasei Corporation

- China Petroleum & Chemical Corporation (Sinopec)

- INEOS Styrolution Group GmbH

- JSR Corporation

- Korea Kumho Petrochemical Co., Ltd.

- TSRC

- En Chuan Chemical Industries Co., Ltd.

- Denka Company Limited

- Kuraray Co., Ltd.

- Dynasol Group

- LG Chem

- CHIMEI

- Versalis S.p.A.

- SIBUR

- Zhejiang Zhongli Synthetic Material Technology Co., Ltd.

- Fujian Gulei Petrochemical Co., Ltd.

Recent Developments

-

In June 2025, Teknor Apex completed the acquisition of Danimer Scientific, broadening its sustainable-materials portfolio and adding bioplastic capabilities that support SBC compounders seeking lower-carbon formulations and compostable blends for niche applications.

-

In February 2024, Kraton Corporation, a manufacturer of high-value biobased products and specialty polymers, announced an investment worth USD 35 million to upgrade its existing crude tall oil biorefinery towers in its production facility in Panama City, Florida, U.S.

Styrenic Block Copolymer Market Report Scope

Report Attribute

Details

Market size in 2025

USD 5.2 billion

Estimated market size in 2026

USD 5.3 billion

Projected market size by 2045

USD 13.0 billion

Growth rate

CAGR of 4.7% from 2026 to 2045

Historical data

2021 - 2025

Forecast period

2026 - 2045

Quantitative units

Revenue in USD million/billion, volume in kilotons, and CAGR from 2026 to 2045

Report coverage

Revenue & volume forecast, competitive landscape, growth factors, and trends

Segments covered

Product, application, region

Regional scope

North America; Europe; Asia Pacific; CSA; MEA

Country Scope

U.S.; Canada; Mexico; Germany; UK; France; Italy; Spain; Netherlands; Norway; China; India; Japan; Australia; Thailand; South Korea; Malaysia; Indonesia; Brazil; Argentina; Saudi Arabia; UAE; South Africa

Key companies profiled

LCY Group; KRATON CORPORATION; ZEON CORPORATION; Asahi Kasei Corporation; China Petroleum & Chemical Corporation (Sinopec); INEOS Styrolution Group GmbH; JSR Corporation; Korea Kumho Petrochemical Co., Ltd.; TSRC, En Chuan Chemical Industries Co., Ltd.; Denka Company Limited, Kuraray Co., Ltd.; Dynasol Group; LG Chem; CHIMEI; Versalis S.p.A.; SIBUR; Zhejiang Zhongli Synthetic Material Technology Co., Ltd.; Fujian Gulei Petrochemical Co., Ltd.

Customization scope

Free report customization (equivalent to up to 8 analyst working days) with purchase. Addition or alteration to country, regional & segment scope

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Styrenic Block Copolymer Market Report Segmentation

This report forecasts revenue growth at the global, regional, and country levels and provides an analysis of the latest industry trends across sub-segments from 2021 to 2045. For this study, Grand View Research has segmented the global styrenic block copolymer market report based on product, application, and region:

-

Product Outlook (Volume, Kilotons; Revenue, USD Million, 2021 - 2045)

-

HSBC

-

SBS

-

SIS

-

-

Application Outlook (Volume, Kilotons; Revenue, USD Million, 2021 - 2045)

-

HSBC

-

Adhesives & Sealants

-

Polymer Modification

-

Medical Devices

-

Others

-

-

SBS

-

Footwear

-

Asphalt Modification

-

Polymer Modification

-

Adhesives

-

Others

-

-

SIS

-

Coating

-

Pressure Sensitive Adhesives

-

Healthcare

-

Others

-

-

-

Regional Outlook (Volume, Kilotons; Revenue, USD Million, 2021 - 2045)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

France

-

Italy

-

Spain

-

Netherlands

-

Norway

-

-

Asia Pacific

-

Japan

-

China

-

India

-

Australia

-

Thailand

-

South Korea

-

Malaysia

-

Indonesia

-

-

Central & South America

-

Brazil

-

Argentina

-

-

Middle East & Africa

-

Saudi Arabia

-

UAE

-

South Africa

-

-

Frequently Asked Questions About This Report

Some key players operating in the styrenic block copolymer market include LCY Group, KRATON CORPORATION, ZEON CORPORATION, Asahi Kasei Corporation, China Petroleum & Chemical Corporation (Sinopec), INEOS, Styrolution Group GmbH, JSR Corporation, Korea Kumho Petrochemical Co., Ltd., TSRC, En Chuan Chemical Industries Co., Ltd., and others.

Footwear segment held the largest revenue share 20.7% in 2025, while healthcare is the fastest-growing area.

Asia Pacific dominated with a 34.9% revenue share in 2025.

The global styrenic block copolymer market size was estimated at USD 5.2 billion in 2025 and is expected to reach USD 5.4 billion in 2026.

The global styrenic block copolymer market is expected to grow at a compound annual growth rate of 4.7% from 2026 to 2045 to reach USD 13.0 billion by 2045.

The SBS segment dominated the market across product segmentation in terms of revenue, accounting for 69.7% market share in 2025, and is forecast to grow at a 7.1% CAGR from 2026 to 2045.

The styrenic block copolymers (SBC) are produced by ionic copolymerization of styrene, isoprene, and butadiene and are considered one of the largest volume commercial thermoplastic elastomers. The market is expected to be driven by the rising demand from various applications such as footwear, adhesives & sealants, paints & coatings, polymer modification, paving and roofing, toys, and medical devices.

About the Author(s)

Plastics, Polymers & Resins Research Team

Bulk Chemicals · Plastics, Polymers & ResinsThis report was authored by the plastics, polymers & resins research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the plastics, polymers & resins segment of the bulk chemicals industry. All findings are based on proprietary bulk chemicals databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.