- Home

- »

- Biotechnology

- »

-

Transduction Technologies Market, Industry Report, 2033GVR Report cover

![Transduction Technologies Market Size, Share & Trends Report]()

Transduction Technologies Market (2025 - 2033) Size, Share & Trends Analysis Report By Product (Transduction Kits, Transduction Enhancers), By Target Cell Type, By Application (Gene Therapy, Cell Therapy, Vaccines), By End-use, By Region, And Segment Forecasts

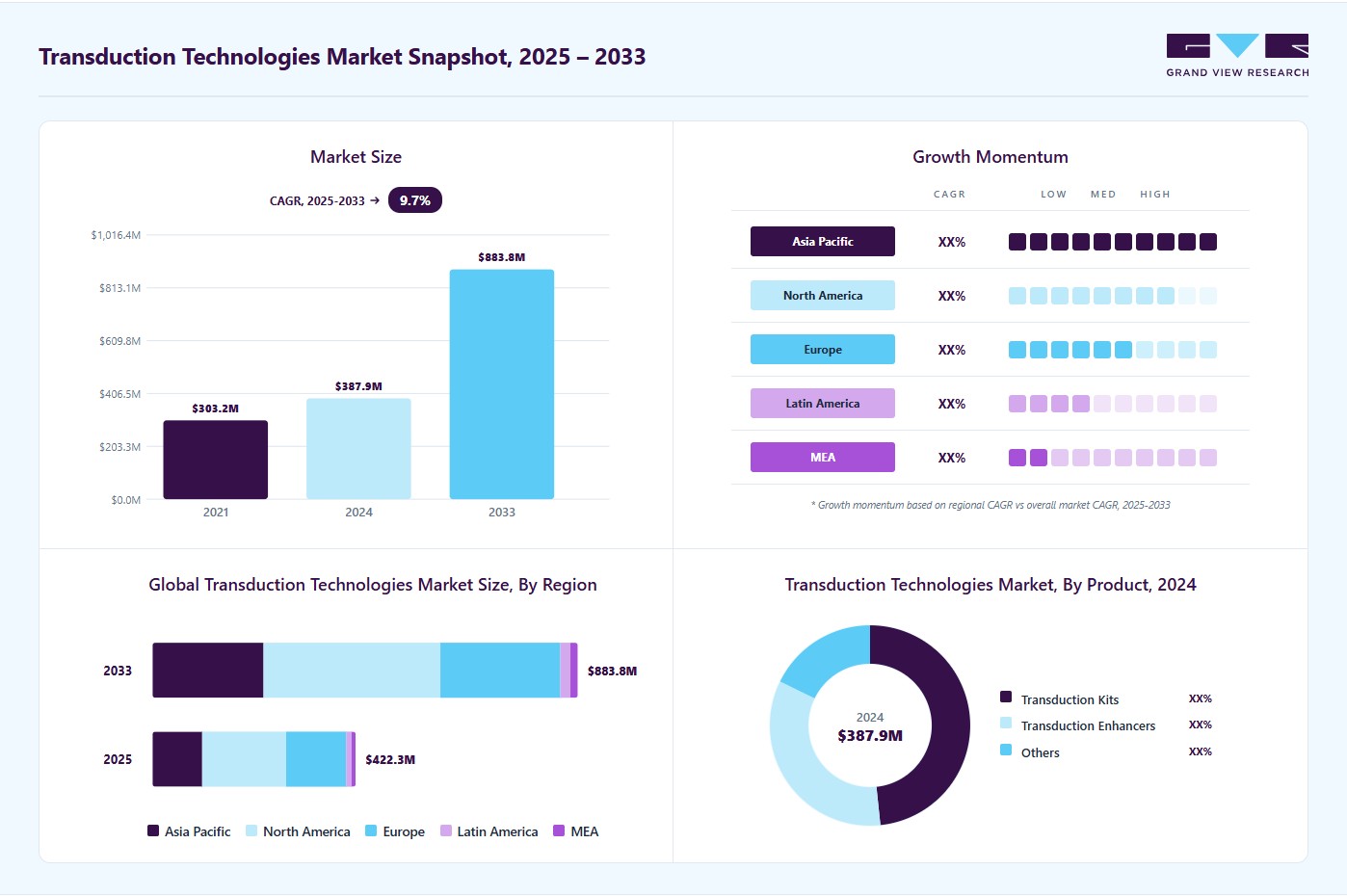

Market Size, 2024

$387.8MMarket Estimate, 2026

$460.4MMarket Forecast, 2033

$883.9MCAGR, 2025–2033

9.7%Transduction Technologies Market Summary

The global transduction technologies market size was estimated at USD 387.8 million in 2024 and is projected to reach USD 883.9 million by 2033, growing at a CAGR of 9.67% from 2025 to 2033. The market is expanding due to the growing use of sophisticated gene and cell therapy methods, the need for effective delivery methods, and ongoing advancements in transduction platform technology.

Key Market Trends & Insights

- North America dominated the transduction technologies market with the largest revenue share of 41.29% in 2024.

- The transduction technologies industry in the U.S. accounted for the largest market revenue share in 2024.

- By product, the transduction kits segment led the market with the largest revenue share of 48.34% in 2024.

- Based on target cell type, the immune cells segment accounted for the largest market revenue share in 2024.

- By application, the gene therapy segment accounted for the largest market revenue share in 2024.

Market Size & Forecast

- 2024 Market Size: USD 387.8 Million

- 2033 Projected Market Size: USD 883.9 Million

- CAGR (2025-2033): 9.67%

- North America: Largest market in 2024

- Asia Pacific: Fastest growing market

")

The market is also anticipated to grow over the forecast period due to rising research investments and expanding applications in biotechnology, pharmaceuticals, and regenerative medicine.

Rise of Gene Editing and Synthetic Biology

One of the main factors propelling the market for transduction technologies in the life sciences is the rapid development of gene editing and synthetic biology. Because they allow for precise DNA-level modifications, advanced genetic engineering tools like CRISPR-Cas9, TALENs, and base editors have completely changed research and therapeutic development. They enable scientists to monitor genetic material changes in real time, verify editing results, and optimize protocols for various uses, including metabolic engineering and functional genomics.

These technologies guarantee that engineered cells display the intended characteristics free from unwanted mutations by enabling the ongoing evaluation of genetic alterations in living cells. Furthermore, transducers facilitate automation and high-throughput testing, both of which are becoming increasingly crucial for extensive synthetic biology initiatives.

Demand from Personalized Medicine and Cell Therapies

The growing focus on personalized medicine and advanced cell therapies significantly influences the market. Stem cells, CAR-T cells, and induced pluripotent stem cells (iPSCs) are engineered cells increasingly used in therapeutic applications to treat cancer, genetic disorders, and degenerative diseases. These cells must be precisely characterized genetically and functionally to guarantee that they carry out the intended therapeutic function without producing negative side effects before they can be safely given to patients.

In addition, growing cell and gene therapy pipelines in biopharmaceutical companies and research institutions are driving the adoption of transduction technologies. These technologies guarantee consistent performance and safety by enabling real-time, non-invasive monitoring of engineered cells during production, quality control, and post-modification evaluation. Rapid, accurate, and quantitative data generation on genetic and metabolic alterations facilitate regulatory compliance and speeds up the transition from lab to clinical settings.

Market Concentration & Characteristics

The transduction technologies industry is highly innovative due to ongoing developments in molecular detection platforms, nanotechnology, microfabrication, and biosensing materials. Traditional signal detection has been transformed into automated, high-throughput, multiplexed platforms by integrating AI, lab-on-a-chip systems, and microfluidic devices. Furthermore, using new biocompatible materials and nanostructured surfaces improves signal-to-noise ratios and makes single-molecule detection possible.

The transduction technologies industry has a moderate to high level of mergers and acquisitions (M&A) activity, which reflects increasing consolidation among major players looking to broaden their product and technological offerings. Major life science and biotechnology companies are aggressively acquiring businesses that specialize in biosensors, nanomaterials, and microfluidic-based detection systems to improve their position in the quickly changing fields of genetic engineering and molecular diagnostics. For example, in January 2021, Thermo Fisher Scientific expanded its European cell and gene therapy production capacity for commercial and clinical customers by completing the acquisition of Novasep's viral vector manufacturing business.

Regulatory authorities such as the U.S. FDA, EMA, and other regional bodies mandate strict standards for device accuracy, safety, biocompatibility, and validation before commercialization, influencing product development timelines and market entry strategies. Good Laboratory Practices (GLP) and Good Manufacturing Practices (GMP) must be followed in genetic engineering applications to guarantee the accuracy and repeatability of results, especially when transduction technologies are incorporated into cell and gene therapy workflows. These regulations can slow approval procedures and raise development costs, but they also boost market credibility and encourage the use of technologies that live up to high standards.

The transduction technologies industry is driven primarily by product expansion, as businesses consistently create cutting-edge, adaptable, and application-specific solutions to satisfy the changing demands of genetic engineering and life sciences. Businesses spend money on multiplexed detection platforms, lab-on-a-chip technology, and next-generation biosensors because they provide increased sensitivity, quicker reaction times, and automation. Market participants improve their competitive positions and meet the increasing need for precise, effective, and scalable molecular detection technologies by consistently enhancing and broadening their product offerings.

Regional expansion is a significant growth driver for the transduction technologies industry, as companies aim to capture emerging opportunities in high-demand geographies and strengthen their global footprint. North America and Europe are key markets because of their sophisticated research facilities, well-established biotech hubs, and widespread use of genetic engineering and molecular diagnostics. To increase accessibility and shorten product time-to-market, businesses utilize regional manufacturing facilities, distribution networks, and local partnerships.

Product Insights

The transduction kits segment led the market with the largest revenue share of 48.34% in 2024, because transduction kits are widely used in gene delivery, cell engineering, and therapy development applications. These kits have also become more popular among academic institutions, biotechnology companies, and pharmaceutical companies due to the increased focus on cell and gene therapy and ongoing developments in viral and non-viral vector technologies.

The transduction enhancers segment is anticipated to expand at the fastest CAGR during the forecast period, owing to the rising demand for more effective gene transfer and efficient genetic material delivery into target cells. In gene and cell therapy applications, these enhancers are essential for increasing the rates of viral and non-viral transduction, decreasing cytotoxicity, and increasing the total yield of functional cells, which further supports the segment growth.

Target Cell Type Insights

The immune cells segment led the market with the largest revenue share of 40.55% in 2024, as immune cells - particularly T cells, NK cells, and dendritic cells - are increasing for use in gene therapy, immunotherapy, and the R&D of vaccines. The popularity of immune cells has been further stimulated by their potent and durable ability to be genetically engineered for specific therapeutic applications, most notably in CAR-T and TCR-T cell therapy. Their transduction technologies sector has also been assisted by increases in viral vector mediated transduction methods, with the advantages of immune cells, especially those from human sources.

The stem cells segment is projected to experience at the fastest CAGR during the forecast period, which can be attributed to the increasing demand for regenerative medicine, cell-based therapies, and disease modeling applications. The unique property of stem cells to differentiate into diverse cell types makes them ideal for gene editing, tissue engineering, and personalized medicine applications. Moreover, growing investments in stem cell research, use of viral and non-viral methods in transduction, and increasing emphasis on developing effective therapies for chronic and genetic disorders are also driving the adoption of stem cells into the transduction technologies industry.

Application Insights

The gene therapy segment led the market with the largest revenue share of 46.39% in 2024, driven by the growth of gene-based therapeutics for genetic disorders, cancers, and rare diseases. The growing clinical pipeline of innovative gene therapy treatments and the need for effective and reliable transduction technologies have supported the growth of the gene therapy segment as a dominant component of the transduction technologies industry.

The cell therapy market is projected to witness at the fastest CAGR during the forecast period. Light of the growing utilization of cell-based therapies in cancer treatment, autoimmune diseases, and regenerative medicine. The market growth is driven by increasing cell therapy funding, transduction efficiency, and new delivery systems (viral and non-viral). In addition, increased clinical trials, relevant regulatory bodies, and demand for personalized therapeutic solutions further support cell therapy adoption in the global healthcare setting.

End-use Insights

The pharmaceutical & biotechnology companies segment led the market with the largest revenue share of 45.68% in 2024, as pharmaceuticals and biotechnology companies use transduction technologies broadly in drug discovery, gene therapy development, cell-based research, etc. The segment dominance in the transduction technologies industry is further supported by strategic partnerships, expanding research pipelines, and the increasing emphasis on personalized medicine.

The CROs & CDMOs segment is projected to grow at the fastest CAGR during the forecast period, as pharmaceutical and biotechnology companies are increasing outsourcing of research and development and manufacturing, and are relying on contract service providers for scalable, economical values in terms of transduction capacity, whether it be viral vector production, non-viral vector production, cell engineering, or gene therapies. The increased need for specialized scientists, advanced methodologies, and speed to market new therapeutics will continue to accelerate the use of CRO and CDMO services in the transduction technologies industry.

Regional Insights

North America dominated the transduction technologies market with the largest revenue share of 41.29% in 2024, due to its significant biotechnology hubs, sophisticated research infrastructure, and widespread use of genetic engineering and molecular diagnostic tools. Innovation in biosensors, lab-on-a-chip devices, and automated detection systems is made possible in the region by significant R&D investments, supportive regulations, and cooperation between academic institutions and biopharma companies. Rising demand for cell/gene therapy applications and personalized medicine has also strengthened the market.

U.S. Transduction Technologies Market Trends

The transduction technologies market in the U.S. accounted for the largest market revenue share in 2024, with the help of top biotech firms, cutting-edge academic research facilities, and vast clinical trial networks. Significant investments in gene therapies, personalized medicine, and synthetic biology research have accelerated the use of transduction technologies for high-throughput screening and real-time molecular detection.

Europe Transduction Technologies Market Trends

The transduction technologies market in Europe holds a significant share because of its robust life sciences research networks, state-of-the-art laboratory facilities, and government programs promoting biotechnology and genomics research. Countries like Germany and the UK are at the forefront of adopting next-generation biosensors and microfluidic platforms for genetic engineering and molecular diagnostics. Strict regulatory requirements that promote the creation of dependable and superior detection technologies further support the market.

The UK transduction technologies market is driven by extensive genomic research programs, robust biotech funding, and collaboration between universities and biopharma companies. Adoption of biosensors and lab-on-a-chip systems for gene editing validation and molecular diagnostics is growing steadily.

The transduction technologies market in Germany is a key region of the European market due to its strong biotechnology sector, precision engineering capabilities, and research-driven healthcare system. German research institutes and biopharma companies increasingly rely on automated transduction-based platforms for genetic engineering, cell therapy monitoring, and diagnostic applications.

Asia Pacific Transduction Technologies Market Trends

The transduction technologies market in the Asia Pacific is expected to witness at the fastest CAGR of 10.62% during the forecast period, fueled by rising investments in biotechnology, expanding research infrastructure, and increasing adoption of cell and gene therapy platforms. The need for sensitive and effective transduction technologies is growing due to the region's increased emphasis on personalized medicine and high-throughput screening.

The transduction technologies market in China is growing quickly in China owing to significant government investments in biotechnology, the expansion of R&D facilities, and an increased emphasis on cell and gene therapy research. In both academic and commercial research settings, sophisticated biosensors, microfluidic devices, and automated detection systems are growing.

The Japan transduction technologies market is a leading market in Asia-Pacific due to its highly advanced life sciences research infrastructure, government support for biopharma innovation, and early adoption of automated molecular detection technologies. Transduction platforms are widely used in genetic engineering, personalized medicine, and high-throughput screening applications.

Middle East & Africa Transduction Technologies Market Trends

The transduction technologies market in the Middle East & Africa are emerging markets for transduction technologies. Countries such as Kuwait are investing in life sciences infrastructure and genomic research programs, which are gradually driving demand for transduction-based detection platforms in research and clinical applications.

The Kuwait transduction technologies market represents an emerging market in the Middle East, with rising demand fueled by investments in healthcare infrastructure, genomic research initiatives, and partnerships with global biotech companies. The nation is progressively adopting transduction technologies for use in clinical and research settings, especially in molecular diagnostics and genetic research.

Key Transduction Technologies Company Insights

The market for transduction technologies is marked by several established competitors who have matured their market positions via comprehensive product offerings, collaborations, and sustained investment in R&D. Leading companies such as Thermo Fisher Scientific, Merck KGaA, Takara Bio, and Mirus Bio have significant contributions to their market position due to their advanced viral and non-viral technologies, broad consistency in applications, and global distribution chains.

Organizations, including Revvity, OZ Biosciences, Miltenyi Biotec, System Biosciences, Applied Biological Materials, and Akron Biotech, are expanding their reach by introducing innovative transduction solutions, optimized viral vectors, and custom services that have all been specifically created to enhance the demand of pharma organizations, biotechnology companies, contract research organizations, and the academic sector.

As demand grows for personalized medicine, gene therapies, and regenerative medicine, the market will, to an increasing degree, be influenced by obligations to scalability, safety, and regulatory compliance. These obligations will be the defining factors of the future development of the transduction technologies industry to align with the continued innovation in healthcare related to new therapeutics.

Key Transduction Technologies Companies:

The following are the leading companies in the transduction technologies market. These companies collectively hold the largest market share and dictate industry trends.

- Thermo Fisher Scientific, Inc.

- Merck KGaA

- Takara Bio

- Revvity, Inc.

- OZ Biosciences

- Mirus Bio

- System Biosciences

- Miltenyi Biotec

- Applied Biological Materials

- Akron Biotech

Recent Developments

-

In May 2024, Takara Bio USA launched the Lenti‑X Transduction Sponge in the U.S., a dissolvable microfluidic enhancer improving lentiviral gene delivery efficiency across multiple human cell types.

-

In July 2021, Polyplus-transfection launched FectoVIR-AAV, a transfection reagent in Europe and internationally, designed to enhance large-scale AAV production, boosting viral titers up to tenfold for gene therapy applications.

Transduction Technologies Market Report Scope

Report Attribute

Details

Market size value in 2025

USD 422.2 million

Revenue forecast in 2033

USD 883.9 million

Growth rate

CAGR of 9.67% from 2025 to 2033

Base year for estimation

2024

Historical data

2021 - 2023

Forecast period

2025 - 2033

Quantitative units

Revenue in USD million/billion, and CAGR from 2025 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Product, target cell type, application, end-use, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; UK; Germany; France; Italy; Spain; Denmark; Sweden; Norway; India; China; Japan; Australia; South Korea; Thailand; Brazil; Argentina; Saudi Arabia; UAE; South Africa; Kuwait

Key companies profiled

Thermo Fisher Scientific, Inc.; Merck KGaA; Takara Bio; Revvity, Inc.; OZ Biosciences; Mirus Bio; System Biosciences; Miltenyi Biotec; Applied Biological Materials; Akron Biotech

Customization scope

Free report customization (equivalent up to 8 analyst’s working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Transduction Technologies Market Report Segmentation

This report forecasts revenue growth and provides an analysis on the latest trends in each of the sub-segments from 2021 to 2033. For this report, Grand View Research has segmented the global transduction technologies market report based on product, target cell type, application, end-use, and region.

-

Product Outlook (Revenue, USD Million, 2021 - 2033)

-

Transduction Kits

-

Transduction Enhancers

-

Others

-

-

Target Cell Type Outlook (Revenue, USD Million, 2021 - 2033)

-

Stem Cells

-

Cancer Cells

-

Immune Cells

-

Others

-

-

Application Outlook (Revenue, USD Million, 2021 - 2033)

-

Gene Therapy

-

Cell Therapy

-

Vaccines

-

Others

-

-

End-use Outlook (Revenue, USD Million, 2021 - 2033)

-

Pharmaceutical & Biotechnology Companies

-

Academic & Research Institutes

-

CROs & CDMOs

-

-

Regional Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

France

-

Italy

-

Spain

-

Denmark

-

Sweden

-

Norway

-

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

Australia

-

Thailand

-

-

Latin America

-

Brazil

-

Argentina

-

-

Middle East and Africa (MEA)

-

South Africa

-

Saudi Arabia

-

UAE

-

Kuwait

-

-

About the Author(s)

Biotechnology Research Team

Healthcare · BiotechnologyThis report was authored by the biotechnology research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the biotechnology segment of the healthcare industry. All findings are based on proprietary healthcare databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.