- Home

- »

- Consumer F&B

- »

-

Zero Sugar Beverages Market Size, Growth Report, 2026-2033GVR Report cover

![Zero Sugar Beverages Market (2026 - 2033)Report]()

Zero Sugar Beverages Market (2026 - 2033)

Size, Share & Trends Analysis Report By Type (Carbonated Soft Drinks, Energy Drinks, Sports Drinks, Flavored Water), By Packaging (PET, Cans, Glass), By Distribution Channel (Online, Offline), By Region, And Segment Forecasts

Market Size, 2025

$70.8BMarket Estimate, 2026

$77.6BMarket Forecast, 2033

$148.8BCAGR, 2026–2033

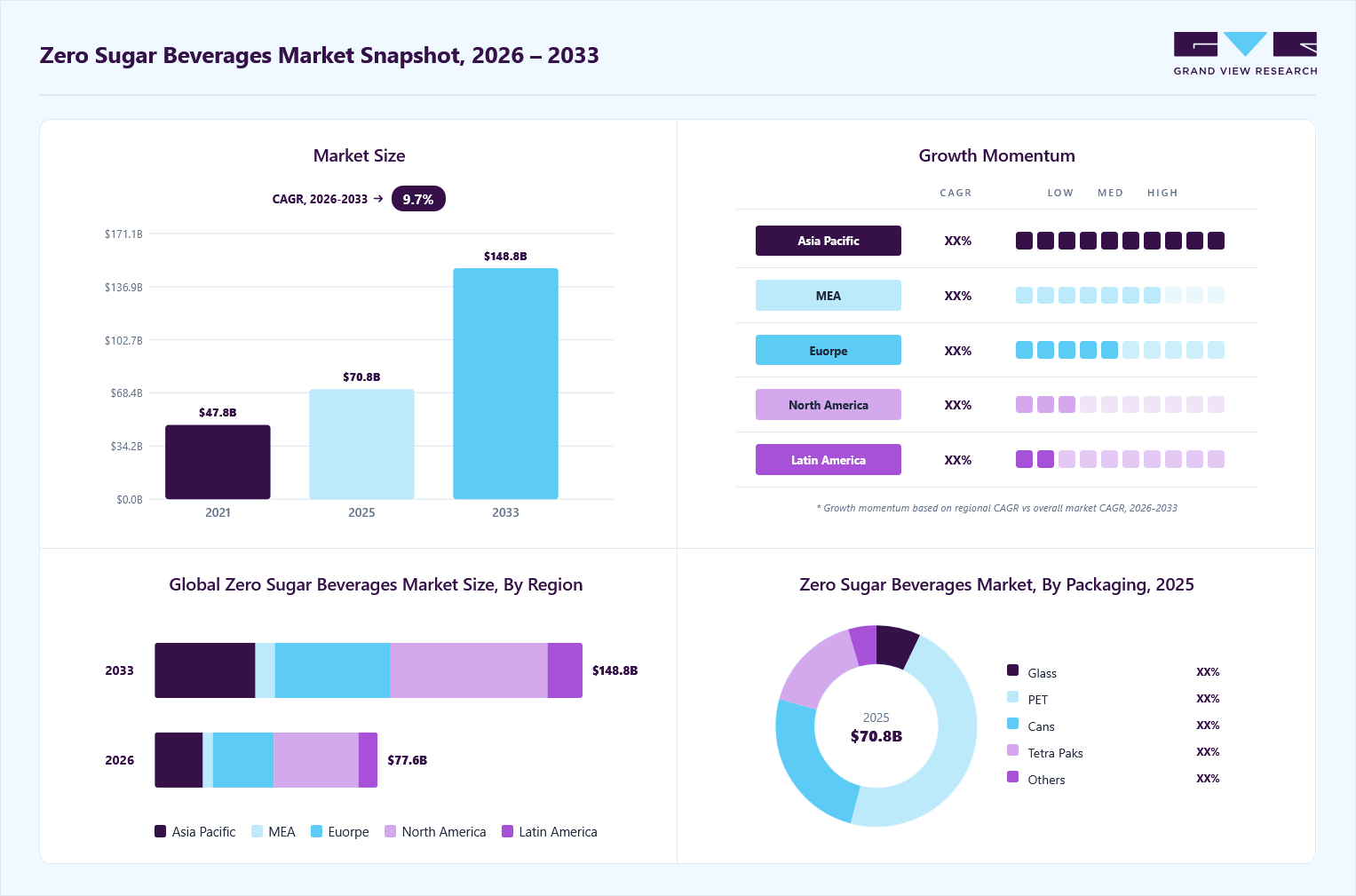

9.7%Zero Sugar Beverages Market Summary

The global zero sugar beverages market size was valued at USD 70.8 billion in 2025 and is projected to grow from USD 77.6 billion in 2026 to USD 148.8 billion by 2033, at a CAGR of 9.7% from 2026 to 2033. North America dominated the global market, accounting for the largest revenue share of 38.1% in 2025. The zero sugar beverages industry is experiencing rapid expansion as consumers increasingly prioritize health‑focused and environmentally responsible choices.

Key Market Trends & Insights

- By type: Carbonated soft drink segment led the market with the largest revenue share of 30.4% in 2025.

- By packaging: PET bottles segment led the market with the largest revenue share of 46.9% in 2025.

- By distribution channel: Offline segment led the market with the largest revenue share of 79.9% in 2025.

Regional Highlights

- Largest regional market: North America (38.1% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

- By country: The U.S held the largest market share in 2025

Market Size & Forecast

- Market size in 2025: USD 70.8 Billion

- Estimated market size in 2026: USD 77.6 Billion

- Projected market size by 2033: USD 148.8 Billion

- CAGR (2026-2033): 9.7%

The sugar-free beverages market is being driven by increasing consumer focus on calorie management, a rising prevalence of diabetes, and the growing influence of weight-loss pharmacy therapies. In addition, younger demographics are exhibiting a strong shift toward wellness-oriented consumption, driven by both health considerations and aesthetic aspirations.

Zero-sugar beverage sales are accelerating globally, driven by rising health awareness and growing concerns about diabetes and obesity. Strong demand for low-calorie alternatives, combined with product innovation, advanced packaging, and wider distribution, is fueling category expansion. The market now includes carbonated soft drinks, energy drinks, sports drinks, flavored waters, wellness beverages & others. Key growth markets such as the US, Germany, China, and India are leading adoption, while premium formulations and localized flavors continue to strengthen consumer appeal.

")

The zero sugar beverages industry is experiencing strong global growth, driven by rising consumer awareness around health, wellness, and sugar reduction. As consumers become more conscious of daily calorie intake and lifestyle-related conditions such as obesity and diabetes, they are increasingly shifting away from traditional sugar-sweetened beverages toward zero-calorie and low-sugar alternatives. Zero-sugar beverages are positioned as healthier options that deliver taste, refreshment, and convenience without added sugar, making them highly attractive to health-conscious consumers. Advancements in sweetening technologies, including stevia, monk fruit, sucralose, and blended sweetener systems, have significantly improved taste profiles and mouthfeel, helping brands overcome historical taste barriers and broaden consumer adoption.

Leading beverage manufacturers are actively expanding their zero-sugar portfolios through new launches, flavor innovation, and category diversification. Global players in the sugar-free drinks market, such as The Coca-Cola Company and PepsiCo, continue to scale offerings, including Coca-Cola Zero Sugar, Sprite Zero Sugar, Pepsi Zero Sugar, and functional no-sugar beverages across multiple markets. Companies are also investing in ready-to-drink teas, flavored sparkling waters, energy drinks, hydration beverages, and wellness-focused products to capture evolving demand. Premium packaging, convenient on-the-go formats, and bold flavor variants are further enhancing shelf appeal and encouraging repeat purchases.

Changing consumer preferences, particularly among Millennials and Gen Z, are playing a major role in market expansion. Younger consumers increasingly favor products that align with fitness goals, active lifestyles, transparency, and clean-label expectations. Many seek beverages with natural ingredients, no added sugar, lower calories, and functional benefits such as hydration, vitamins, electrolytes, probiotics, caffeine, or immunity support. This shift has accelerated demand for zero-sugar teas, sports drinks, energy beverages, kombuchas, and fortified sparkling drinks. Social media influence, wellness culture, and increasing experimentation with healthier alternatives are also strengthening category momentum.

North America remains one of the most mature and high-value markets for zero-sugar beverages, led by the U.S., where strong consumer awareness, advanced retail infrastructure, and aggressive brand innovation continue to support category growth. Consumers in the U.S. are increasingly replacing traditional sodas with zero sugar carbonates, flavored waters, and fitness-oriented drinks. Europe is also witnessing solid growth in reduced-sugar products, particularly in markets such as Germany, the UK, France, and Spain, where sugar taxes, stricter labeling regulations, and wellness trends are driving reduced-sugar consumption. Manufacturers across Europe are responding by reformulating and launching premium zero-sugar products.

Asia Pacific is emerging as the fastest-growing regional market, supported by rising disposable incomes, urbanization, and growing middle-class health awareness. China has seen strong demand for sugar-free tea and functional beverages, reflecting a structural shift toward healthier drink categories. India is also becoming a key growth hub, with urban consumers increasingly opting for no-sugar colas, low-calorie hydration drinks, and zero-sugar juices amid rising diabetes concerns and shifting dietary preferences. Japan and South Korea continue to drive innovation in ready-to-drink teas, functional beverages, and the convenience-led zero sugar beverages industry.

Consumer Insights

Zero sugar beverages are increasingly perceived as healthier and higher-quality alternatives to regular drinks, driving strong demand across markets such as the U.S., Germany, China, and India. Rising consumer focus on sugar reduction, weight management, and diabetes prevention is accelerating adoption, with shoppers paying closer attention to calorie and sugar labels. Manufacturers are expanding portfolios through launches featuring natural sweeteners, clean-label formulations, and functional ingredients. Wider availability across supermarkets, convenience stores, gyms, cafés, vending machines, e-commerce, and direct-to-consumer channels is strengthening market penetration. Quick-commerce platforms are helping brands engage younger consumers through targeted promotions and subscription models. Overall, the category is evolving into a mainstream global beverage segment, supported by health trends, premiumization, innovation, and broader distribution.

Type Insights

The carbonated soft drinks segment led the market with the largest revenue share of 30.4% in 2025. The segment’s leadership is driven by strong consumer demand for healthier alternatives to conventional sugary sodas, supported by the continued expansion of zero-sugar cola, lemon-lime, and sparkling beverage portfolios by major manufacturers. Product innovation in flavors, packaging, and sweetener formulations, along with widespread retail availability, continues to drive growth in the global segment.

The RTD coffee/tea segment is expected to witness at a significant CAGR from 2026 to 2033, supported by rising consumer preference for convenient, low-calorie, and functional beverage options. Zero-sugar teas and ready-to-drink coffee products are gaining momentum among consumers seeking refreshment, energy, and benefits without added sugar. Increasing product launches featuring natural sweeteners, clean-label ingredients, and premium positioning are expected to further accelerate demand across key markets.

Packaging Insights

The PET bottles segment led the market with the largest revenue share of 46.9% in 2025. PET bottles remain the preferred format due to their lightweight structure, cost efficiency, durability, and convenience. They are widely used across the carbonated soft drink, flavored water, sports drink, and ready-to-drink tea categories, supported by strong retail compatibility and efficient transportation. Advancements in recyclable PET, increased use of recycled content, and lightweight bottle designs are also helping manufacturers meet sustainability targets while reducing logistics costs. Premium glass packaging remains relevant for functional and premium beverage categories, where brand image and product positioning are important.

The canned segment is projected to witness at the fastest CAGR of 10.5% from 2026 to 2033, driven by rising demand for portable, sustainable, and on-the-go packaging solutions. Aluminum cans are gaining preference for zero sugar carbonated drinks, energy drinks, and sparkling beverages due to high recyclability, faster chilling capability, and lower transportation weight versus glass formats. Tightening environmental regulations across North America, Europe, and the Asia Pacific are accelerating the shift toward recyclable and low-carbon materials, while China, India, Japan, Germany, and the U.S. are seeing strong adoption of lightweight single-serve formats. Smart packaging, biodegradable materials, and the integration of recycled content are expected to drive the next phase of packaging innovation.

Distribution Channel Insights

The offline segment led the market with the largest revenue share of 79.9% in 2025, highlighting the continued importance of physical retail in beverage purchasing decisions. Supermarkets & hypermarkets remained the leading offline channel, supported by broad product assortments, promotional pricing, and high consumer footfall. Convenience stores benefited from impulse and immediate consumption demand, while grocery and health-focused retailers supported routine household purchases and wellness-oriented consumption trends. Offline retail remains particularly important for carbonated soft drinks, flavored waters, sports drinks, and energy beverages, where shelf visibility, chilled availability, and brand recognition strongly influence purchasing behavior. Major retailers across North America, Europe, and the Asia Pacific are also expanding shelf space for reduced sugar and zero sugar beverage portfolios.

The online segment is projected to register at the fastest CAGR of 11.6% from 2026 to 2033. Growth is driven by rising digital adoption, quick-commerce platforms, subscription-based purchasing models, and a growing preference for doorstep delivery. E-commerce enables brands to deploy targeted promotions, bundle offers, personalized recommendations, and premium or niche zero sugar product ranges with limited traditional retail presence. In parallel, on-premises consumption through cafés, restaurants, hotels, gyms, vending machines, and entertainment venues is gaining momentum as consumers seek healthier beverage choices outside the home. Overall, the market is evolving toward an integrated omnichannel model combining strong offline scale with rapidly expanding digital and out-of-home demand.

Regional Insights

North America dominated the global zero sugar beverages market with the largest revenue share of 38.1% in 2025, driven by rising health awareness and increasing efforts to reduce sugar consumption. Consumers across the U.S., Canada, and Mexico are shifting from traditional sugary drinks toward zero sugar carbonated beverages, flavored waters, sports drinks, energy drinks, and functional hydration products. Strong demand is particularly evident among Millennials and Gen Z consumers, who prioritize wellness, convenience, and low-calorie beverage choices. The region also benefits from an advanced retail ecosystem, with supermarkets, warehouse clubs, convenience stores, and e-commerce platforms significantly improving product accessibility.

U.S. Zero Sugar Beverages Market Trends

The zero sugar beverages market in the U.S. accounted for the largest market revenue share in North America in 2025. Its leadership is supported by the largest population base in the region, high consumer spending power, and a mature premium beverage market with strong demand for functional, clean-label, and zero sugar product innovations. Mexico is expanding steadily through growth in modern retail and digital commerce, while Canada benefits from rising wellness trends and sugar-reduction initiatives. Leading beverage companies continue to invest in natural sweeteners, premium packaging, and flavor innovation, reinforcing North America’s strategic importance in the global zero sugar beverages industry.

The Canada zero sugar beverages market holds a notable share of the North American market and is projected to grow at a significant CAGR of 10.5% from 2026 to 2033, outpacing several regional peers. Growth is supported by rising health awareness, increasing concerns over obesity and diabetes, and strong consumer preference for low-calorie, sugar-free beverage alternatives. Governments' focus on healthier nutrition choices and transparent food labeling is further encouraging demand for reduced sugar products. The country represents an attractive premium beverage market, where consumers are increasingly interested in clean-label formulations, natural sweeteners, functional ingredients, and sustainable packaging. Demand is particularly strong for zero sugar carbonated drinks, flavored waters, energy drinks, and RTD teas. Strong supermarket penetration, convenience retail expansion, and e-commerce growth continue to improve accessibility, positioning Canada as a key growth market for zero sugar beverages in North America.

Europe Zero Sugar Beverages Market Trends

The zero sugar beverages market in Europe held a significant share of 27.4% in 2025, reinforcing its position as a key regional market. Growth is supported by rising health awareness, sugar-reduction initiatives, and increasing consumer demand for low-calorie and sugar-free beverage alternatives. Strong regulatory measures such as sugar taxes, front-of-pack labeling standards, and wellness-focused public health campaigns are accelerating the shift away from traditional sugary drinks toward zero sugar options. The expanding availability of zero sugar beverages through supermarkets, convenience stores, foodservice outlets, and e-commerce platforms is further strengthening market penetration across Europe. In addition, manufacturers are accelerating innovation through natural sweeteners, functional ingredients, sustainable packaging, and localized flavors. Overall, Europe is expected to remain a strategically important market for zero sugar beverages, supported by regulatory momentum, premiumization trends, and continued product innovation.

The UK zero sugar beverages market is projected to record at the fastest CAGR of 10.9% from 2026 to 2033. Growth is primarily supported by strong regulatory measures such as the Soft Drinks Industry Levy (SDIL), introduced in 2018, which accelerated product reformulation and increased zero sugar beverage availability across the market. UK consumers are increasingly shifting toward zero sugar beverages due to rising health awareness, obesity reduction initiatives, and growing concerns around sugar consumption. High penetration of supermarkets, convenience stores, and e-commerce platforms, combined with continuous innovation in zero sugar carbonates, flavored waters, sports drinks, and functional beverages, is further supporting demand. Strong brand investment, clear front-of-pack labeling, and wellness-focused purchasing behavior position the UK as the fastest-growing market in Europe.

Asia Pacific Zero Sugar Beverages Market Trends

The zero sugar beverages market in the Asia Pacific is anticipated to grow at the fastest CAGR of 11.1% from 2026 to 2033. Growth is driven by rising disposable incomes, rapid urbanization, expanding middle-class populations, and increasing health awareness across the region. Rising obesity and diabetes concerns are accelerating the shift from sugary drinks toward zero sugar carbonated beverages, flavored waters, RTD teas, sports drinks, and functional beverages. China remains the largest growth market, supported by strong demand for sugar-free tea and wellness drinks, while Japan leads in product innovation and in the adoption of functional beverages. India is emerging as a high-potential market due to its young population and expanding urban consumer base. Australia and Southeast Asia are also witnessing steady growth, supported by premiumization, active lifestyles, and the expansion of modern retail channels.

The India zero sugar beverages market is gaining momentum and is projected to grow at a rapid CAGR of 12.2% from 2026 to 2033, making it one of the fastest-growing markets in the Asia Pacific. Growth is driven by rising health awareness, rapid urbanization, and increasing demand for clean-label, low-calorie beverage options. Urban consumers are becoming more conscious of sugar intake, fitness, and lifestyle-related conditions such as obesity and diabetes, accelerating the adoption of zero sugar carbonated drinks, flavored waters, energy drinks, and RTD teas. Younger demographics, particularly Gen Z and millennials, are showing a stronger preference for wellness-oriented and premium beverage choices. The market is also benefiting from premiumization trends, rising disposable incomes, and evolving consumption habits in metro cities such as Mumbai, Delhi, Bengaluru, and Hyderabad. The expansion of modern retail, quick commerce, and e-commerce channels is improving product accessibility and brand visibility. Global and domestic players are investing in localized flavors, natural sweeteners, and innovative packaging, positioning India as a high-growth zero sugar beverages industry in the Asia Pacific.

Key Zero Sugar Beverages Company Insights

The zero sugar beverages industry is characterized by the presence of several global beverage companies with strong brand equity, diversified product portfolios, and extensive distribution networks. Leading players have established significant penetration across supermarkets, convenience stores, foodservice outlets, and e-commerce channels. These companies continue to strengthen market positioning through new flavor launches, functional variants, premium packaging formats, and strategic investments in manufacturing capacity, supply chains, and marketing initiatives.

Alongside major participants, the market also includes emerging regional and niche brands that are driving category innovation through natural sweeteners, clean-label formulations, and localized taste profiles. Start-ups and wellness-focused brands are contributing to diversification across carbonated drinks, flavored waters, sports drinks, and RTD tea segments. Overall, the zero sugar beverages industry remains highly competitive, with companies focusing on product innovation, wider retail presence, digital engagement, and consumer-centric branding strategies to capture evolving demand and sustain long-term growth

Key Zero Sugar Beverages Companies:

The following key companies have been profiled for this study on the zero sugar beverages market.

- Coca-Cola

- PepsiCo

- Suntory Oceania

- Keurig Dr Pepper

- Nestle

- Red Bull GmbH

- Arizona Beverage Company

- Fresh Bev LLC

- Pokka

- Spade

Recent Developments

-

In April 2026, The Coca-Cola Company and Jack Daniel's launched the first Jack & Coca-Cola Zero Sugar Flavors Pack nationwide in the US, introducing Cherry Zero Sugar and Vanilla Zero Sugar variants. The launch demonstrates continued flavor innovation and premiumization within the zero-sugar ready-to-drink category.

-

In February 2026, Zero- and low-sugar beverages reached a five-year high in India, with zero-sugar drinks accounting for 30% of Coca-Cola’s total beverage volume in 2025. The portfolio includes Coke Zero, Diet Coke, Sprite Zero, and other no-sugar variants, highlighting the category’s transition into a mainstream growth driver.

-

In February 2026, Varun Beverages, a key bottling partner of PepsiCo, reported that no-sugar and mid-sugar beverages represented 59% of total Q4 2025 volumes, up from 53% a year earlier. The performance signals rising consumer demand for healthier beverage alternatives across emerging markets.

-

In December 2025, PepsiCo announced the expansion of its Pepsi Challenge into 2026 after reporting that Pepsi Zero Sugar recorded 30.8% YTD sales growth in 2025 and gained over one million additional households. The campaign will also feature Pepsi Wild Cherry Zero Sugar, reflecting strong consumer traction in the zero-sugar cola segment

Zero Sugar Beverages Market Report Scope

Report Attribute

Details

Market size in 2025

USD 70.8 billion

Estimated Market size in 2026

USD 77.6 billion

Projected Market size by 2033

USD 148.8 billion

Growth rate

CAGR of 9.7% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion, and volume in million liters, CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Type, packaging, distribution channel, region

Regional scope

North America; Europe; Asia Pacific; Central & South America; Middle East & Africa

Country scope

U.S.; Canada; Mexico; Germany; UK; France; Italy; Spain; China; Japan; India; Australia & New Zealand; Brazil; UAE; Saudi Arabia; South Africa

Key companies profiled

Coca-Cola; PepsiCo; Suntory Oceania; Keurig Dr Pepper; Nestle; Red Bull GmbH; Arizona Beverages Company; Fresh Bev LLC; Pokka; Spade

Customization scope

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Zero Sugar Beverages Market Report Segmentation

This report forecasts revenue growth at the global, regional and country level and provides an analysis of the latest industry trends and opportunities in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global zero sugar beverages market report based on the type, packaging, distribution channel, and region.

-

Type Outlook (Volume, Million Liters; Revenue, USD Million, 2021 - 2033)

-

Carbonated Soft Drinks

-

Energy Drinks

-

Sports Drinks

-

Flavored Water

-

RTD Coffee/ Tea

-

Smoothie

-

Others

-

-

Packaging Outlook (Volume, Million Liters; Revenue, USD Million, 2021 - 2033)

-

PET

-

Cans

-

Glass

-

Tetra Pack

-

Others

-

-

Distribution Channel Outlook (Volume, Million Liters; Revenue, USD Million, 2021 - 2033)

-

Online

-

Offline

-

Supermarkets & Hypermarkets

-

Convenience store

-

Grocery Stores

-

Health & Food Stores

-

Others

-

-

-

Regional Outlook (Volume, Million Liters; Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

France

-

Italy

-

Spain

-

-

Asia Pacific

-

China

-

Japan

-

India

-

Australia & New Zealand

-

-

Central & South America

-

Brazil

-

-

Middle East & Africa

-

UAE

-

Saudi Arabia

-

South Africa

-

-

Frequently Asked Questions About This Report

North America dominated with a 38.1% revenue share in 2025.

The PET bottles segment led with a 46.9% revenue share in 2025, while the canned segment is the fastest-growing.

The offline segment led with a 79.9% revenue share in 2025, while the online segment is the fastest-growing.

Asia Pacific is the fastest-growing region over the forecast period.

The carbonated soft drinks accounted for a dominant share of 30.4% of the global revenue in 2025. The market demand is driven by strong consumer demand for healthier alternatives to conventional sugary sodas, supported by the continued expansion of zero-sugar cola, lemon-lime, and sparkling beverage portfolios by major manufacturers.

Some of the key players operating in the zero sugar beverages market are Coca-Cola, PepsiCo, Suntory Oceania, Keurig Dr. Pepper, Nestle, Red Bull GmbH, Arizona Beverages Company, Fresh Bev LLC, Pokka, and Spade

The zero sugar beverages market is experiencing rapid expansion as consumers increasingly prioritize health‑focused and environmentally responsible choices. The market is being driven by increasing consumer focus on calorie management, a rising prevalence of diabetes, and the growing influence of weight-loss pharmacy therapies.

The global zero sugar beverages market size was estimated at USD 70.8 billion in 2025 and is expected to reach USD 77.6 billion in 2026.

The global zero sugar beverages market is expected to grow at a compound annual growth rate of 9.7% from 2026 to 2033 to reach USD 148.8 billion by 2033.

About the Author(s)

Consumer F&B Research Team

Consumer Goods · Consumer F&BThis report was authored by the consumer f&b research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the consumer f&b segment of the consumer goods industry. All findings are based on proprietary consumer goods databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.