- Home

- »

- Pharmaceuticals

- »

-

Bioanalytical Testing Services Market Size Report 2026-2033GVR Report cover

![Bioanalytical Testing Services Market (2026 - 2033)Report]()

Bioanalytical Testing Services Market (2026 - 2033)

Size, Share & Trends Analysis Report By Molecule (Small, Large), By Test (ADME, PD, PK, Bioavailability, Bioequivalence, Biomarker Testing, Cell-based Assay), By Workflow, By End Use, By Region, and Segment Forecasts

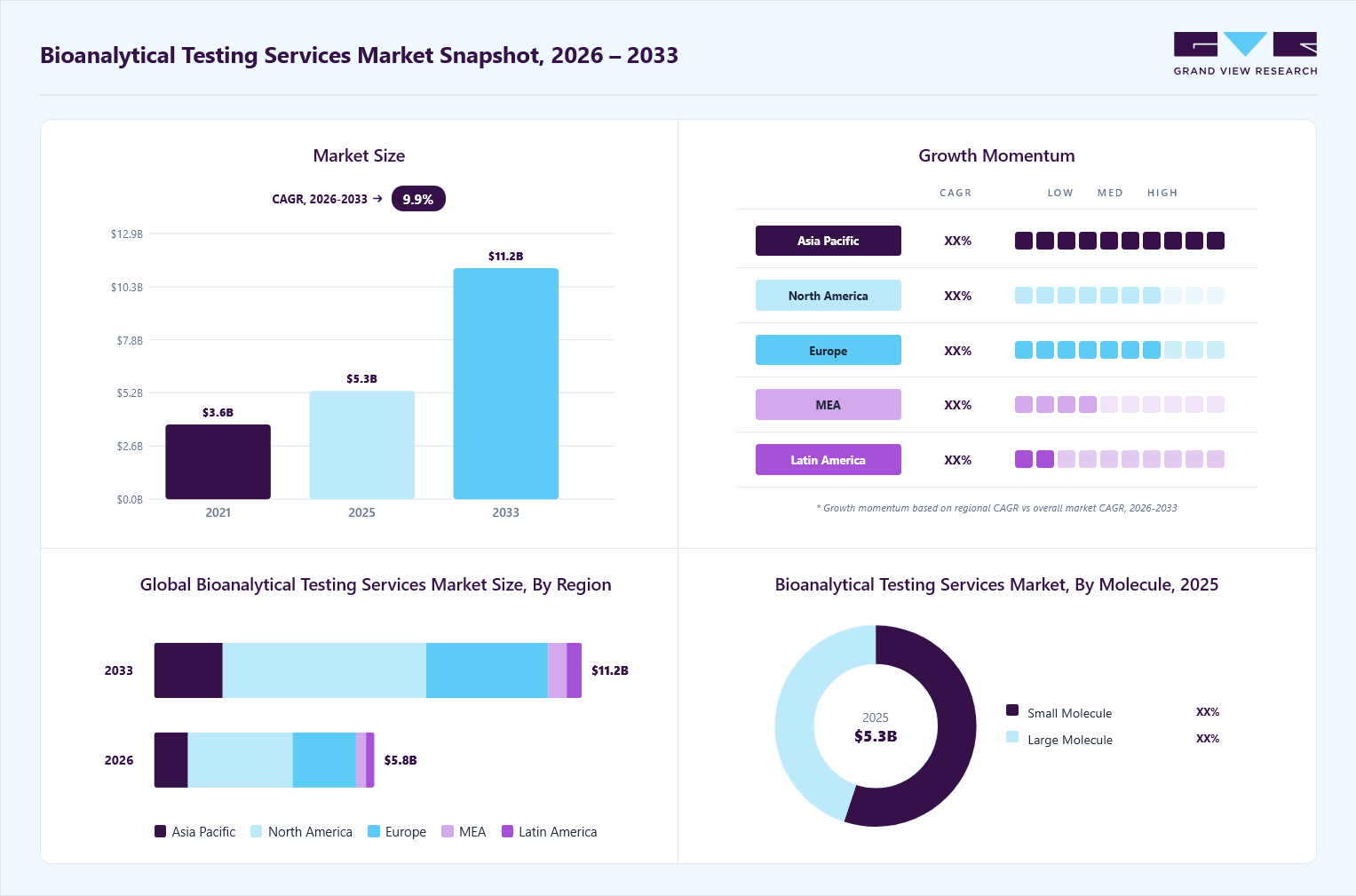

Market Size, 2025

$5.3BMarket Estimate, 2026

$5.8BMarket Forecast, 2033

$11.2BCAGR, 2026–2033

9.9%Bioanalytical Testing Services Market Summary

The global bioanalytical testing services market size was valued at USD 5.3 billion in 2025 and is projected to grow from USD 5.8 billion in 2026 to USD 11.2 billion by 2033, growing at a CAGR of 9.9% from 2026 to 2033. North America dominated the global market with the largest revenue share of 47.4% in 2025. The market growth is driven by increasing drug development activities for biologics, biosimilars, & personalized medicines, drug approval processes, the increasing complexity of therapeutics, and the rising need for precise analytical validation and regulatory compliance.

Key Market Trends & Insights

- By molecule: Small molecule segment led the market with the largest revenue share of 55.1% in 2025.

- By test: Bioavailability segment accounted for the largest market revenue share in 2025.

- By workflow: Sample analysis segment accounted for the largest market revenue share in 2025.

- By end use: Pharma & biopharma companies segment accounted for the largest market revenue share in 2025.

Regional Highlights

- Largest regional market: North America (47.4% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

- By country: The U.S. held the largest market share in 2025.

Market Size & Forecast

- Market size in 2025: USD 5.3 Billion

- Estimated market size in 2026: USD 5.8 Billion

- Projected market size by 2033: USD 11.2 Billion

- CAGR (2026-2033): 9.9%

Other factors contributing to the market include the rising number of clinical trials, pharmaceutical and biotechnology companies' growing outsourcing to specialized CROs, and technological advancements. In addition, stringent regulatory standards, expanding R&D investments, particularly in emerging markets, and the growing focus on biomarker analysis and pharmacokinetic studies are expected to drive the market growth.The bioanalytical testing services industry is driven by technological advancements & growing R&D investments, stricter regulatory controls, increasing awareness of bioanalytical testing, and the expansion of bioanalytical testing facilities.

")

Moreover, technological innovations are significantly driving market growth, as service providers increasingly implement advanced tools, digital platforms, and automation technologies to enhance operational efficiency, accuracy, and scalability. Companies are investing in advanced analytical techniques, automation, and digital solutions to meet the growing complexity of modern drug development, including biologics, biosimilars, and personalized therapies. For instance, in June 2025, IQVIA launched new custom-built AI agents powered by NVIDIA technology, designed to enhance workflows and accelerate insights in life sciences. These AI-driven tools aim to improve efficiency and data processing in bioanalysis, addressing the challenges of handling large and complex datasets and enabling faster, more precise decision-making. Such initiatives are boosting the adoption of these innovative technologies to optimize bioanalytical testing, reduce turnaround times, and support the increasing R&D demands of pharmaceutical and biotechnology companies.

Furthermore, increasing awareness among stakeholders regarding the critical role of bioanalytical testing in ensuring drug safety, efficacy, and quality has fueled demand for these services. Companies recognize that robust bioanalytical testing not only supports regulatory submissions but also mitigates risks, reduces development timelines, and enhances confidence in therapeutic outcomes. This combination of regulatory pressure and informed demand continues to drive the adoption of outsourced bioanalytical testing solutions globally. Besides, stringent regulatory requirements and heightened awareness of the critical role these services play in drug development are expected to drive the market growth.

Regulatory bodies such as the U.S. FDA and the EMA have implemented rigorous standards to ensure the safety, efficacy, and quality of pharmaceuticals and biologics. These regulations necessitate precise and reliable bioanalytical testing, prompting pharmaceutical companies to increasingly outsource these services to specialized providers. For instance, in 2025, SGS expanded its bioanalytical testing services in North America, including method development, validation, pharmacokinetic and immunogenicity testing, to support compliance with FDA and EMA guidelines for clinical trials. This expansion was explicitly aimed at helping pharmaceutical companies meet regulatory standards while ensuring reliable, high-quality data for submissions. Such factors are driving the market growth over the forecast period.

Market Dynamics

The bioanalytical testing services market is currently experiencing steady growth, driven by an expanding pipeline of biologics, biosimilars, and advanced therapeutics, along with increased clinical trial activity globally. This growth is accelerated by rising regulatory demands for drug safety, efficacy, and quality, which in turn boosts the need for specialized bioanalytical testing solutions. Currently, most pharmaceutical and biopharmaceutical companies are seeking outsourcing partnerships to improve operational efficiency, manage development costs effectively, and speed up their time-to-market. Some of the major factors contributing to the market growth are adoption of advanced analytical platforms, automation technologies, high-throughput testing capabilities, and AI-driven data analytics, all aimed at enhancing accuracy and productivity. Furthermore, ongoing investments in precision medicine, cell and gene therapies, and the characterization of complex large molecules are creating substantial growth opportunities within the market.

The expansion of bioanalytical testing facilities is emerging as a significant growth driver for the global bioanalytical testing services market. As pharmaceutical and biopharmaceutical companies continue to advance complex drug pipelines, including biologics, biosimilars, cell therapies, gene therapies, and antibody-drug conjugates, the demand for specialized analytical testing capabilities has increased substantially. To address rising sample volumes and evolving regulatory requirements, contract research organizations (CROs) and testing service providers are investing in new laboratory infrastructure, advanced analytical platforms, and expanded operational capacity.

Most facility expansions enable service providers to enhance throughput, reduce turnaround times, and support a broader range of testing services, including pharmacokinetics, immunogenicity, biomarker analysis, and bioavailability studies. In addition, the establishment of regional testing centers in emerging pharmaceutical markets improves accessibility to high-quality analytical services while supporting global clinical development programs. Investments in automation, digital laboratory management systems, and high-sensitivity analytical technologies further strengthen operational efficiency and data quality.

As outsourcing continues to gain traction across the pharmaceutical industry, expanded bioanalytical infrastructure is becoming essential to meet growing demand. Consequently, ongoing facility expansion initiatives are expected to enhance service capabilities, improve market competitiveness, and contribute significantly to long-term market growth.

Compliance challenges is one of the key restraint in the bioanalytical testing services market. Pharmaceutical and biopharmaceutical companies must ensure that outsourced testing activities meet strict regulatory standards related to laboratory practices, data quality, and study documentation. Managing compliance across multiple service providers and geographic regions can be complex, particularly when regulatory requirements differ between countries. Any issues in data recording, sample management, validation processes, or reporting can result in regulatory delays, additional costs, and extended drug development timelines. Furthermore, sponsors are required to conduct regular audits and maintain close oversight of outsourced operations to ensure quality standards are consistently met. These additional monitoring requirements increase operational complexity and resource commitments. As a result, concerns regarding regulatory compliance and quality control may limit the willingness of some companies to outsource critical bioanalytical testing activities, thereby restraining overall market growth.

The rapid expansion of cell and gene therapy development presents a major growth opportunity for the bioanalytical testing services market. Pharmaceutical and biotechnology companies are increasingly investing in advanced therapies targeting oncology, rare diseases, genetic disorders, and autoimmune conditions. These therapies require highly specialized bioanalytical testing for pharmacokinetics, immunogenicity assessment, biomarker analysis, vector characterization, and long-term safety monitoring, creating strong demand for specialized testing expertise. As the clinical pipeline for cell and gene therapies continues to expand globally, many sponsors are outsourcing complex analytical activities to specialized service providers with advanced technological capabilities and regulatory expertise.

In addition, regulatory agencies are placing greater emphasis on comprehensive analytical characterization and safety evaluation of these novel therapies, further increasing testing requirements throughout the development lifecycle. Service providers that offer advanced platforms, high-sensitivity assays, and integrated bioanalytical solutions are well positioned to capitalize on this trend. With increasing clinical trial activity, rising investment in precision medicine, and a growing number of gene and cell therapy candidates progressing through development stages, demand for specialized bioanalytical testing services is expected to accelerate significantly over the coming years.

Market Concentration & Characteristics

The market growth stage is medium, and growth is accelerating. The market is characterized by the degree of innovation, level of M&A activities, regulatory impact, service expansion, and regional expansion. The bioanalytical testing services industry is advancing due to developments in sensitive bioanalytical techniques, such as digital PCR, next-generation sequencing, and advanced cell-based assay systems, which facilitate accurate measurement, biomarker analysis, and characterization of complex biological molecules across different phases of development. Automation and high-throughput systems have significantly contributed to this process by reducing turnaround times and enhancing reproducibility in large-scale clinical trials, enabling effective decision-making and data generation.

Strict regulatory policies implemented by organizations like the FDA and the EMA are contributing to the current state of the market by mandating full bioanalysis validation that includes PK, immunoassay, and biomarker studies. The level of validation required in these tests is creating greater demand for laboratories with good laboratory practice and good manufacturing practice accreditation.

There is an increasing trend of mergers and acquisitions taking place in the market due to the need for service providers to develop bioanalytical competencies, expand services, and adopt new technologies through the acquisition of specialized laboratories dedicated to performing large molecule testing, immunogenicity analysis, and biomarker testing services.

In addition to offering testing services, service providers are also providing comprehensive packages that include assay development, method validation, PK/PD study services, and regulatory affairs services. Such services fulfill the entire range of drug development needs. Specialized services such as immunogenicity testing, biomarker discovery, and cell-based functional assays have gained popularity as the complexity of biologics increases.

Geographic expansion continues to play an important role as organizations invest in new regions like India and China, where advantages such as cost savings, the availability of skilled labor, and a favorable regulatory environment have made outsourcing more attractive. Such expansions are making global services more accessible and helping accelerate clinical trials by leveraging the diversity of patients and laboratories.

Opportunity Analysis

The bioanalytical testing services industry is experiencing new growth opportunities, driven by the increased complexity of biologics, biosimilars, and advanced therapeutic products. These advancements require highly sensitive, well-validated analytical methods. As a result, there is a strong demand for specialized bioanalytical service providers with advanced capabilities. This includes techniques such as ligand-binding assays, mass spectrometry, and cell-based assays, which are essential for comprehensive large-molecule analysis and characterization.

In addition, the high number of drug development programs in clinical phases, ranging from Phase I to Phase III, provides opportunities for outsourced bioanalytical services. The clinical trials are becoming more personalized; ultimately, the number of small, biomarker-driven trials will increase, leading to greater outsourcing. The regulatory agencies' requirements for bioanalytical method validation are becoming increasingly stringent, making bioanalytical outsourcing necessary for pharmaceutical firms.

The emerging economies of India and China offer cost arbitrage opportunities, supported by the availability of skilled manpower and laboratory infrastructure, which facilitate outsourcing for multinationals. Moreover, progress in automation and high-throughput screening platforms enables the service provider to handle large volumes of samples, thereby enabling scalability and increased profits. The utilization of artificial intelligence in data interpretation expands niche areas in predictive analytics for pharmacokinetics and immunogenicity analysis.

Furthermore, the growing biosimilars development initiatives create a need for comparative bioanalytical services, particularly for regulatory authorities that require evidence for approval. Similarly, many small- and medium-scale biotechnology companies outsource end-to-end bioanalytical services because they do not provide them in-house, thereby expanding the service provider's customer base. In addition, growing interest in treating rare diseases and orphan drugs is driving demand for highly specific assay services for small samples.

The growing trend of collaboration between CROs and biopharmaceutical firms enables joint assay development, helping build stronger service relationships and increase revenues. All these factors together create a favorable environment for bioanalytical testing service providers.

Impact of U.S. Tariffs on the Bioanalytical Testing Services Market

The U.S. tariffs on laboratory tools and equipment, including reagents and analytical equipment, are affecting the cost structure of the global market by increasing input costs from purchasing technologies abroad. This is especially significant for mass spectrometry devices, chromatography columns, and specialized test kits that require high sensitivity, as these products are often imported and crucial to their functionality. The rising costs are encouraging contract research organizations to adjust pricing policies, potentially leading smaller and mid-sized pharmaceutical firms to shift away from outsourcing due to limited resources. Adjusting supply chains is becoming increasingly prevalent as firms seek to mitigate the effects of tariffs by changing supply routes or sources, gradually reorienting procurement channels. In addition, tariffs are also driving partial localization of production processes in the U.S.

This trend has provided a boost to the local equipment and service vendors; however, it has the potential to impact the low-cost advantage offered by international outsourcing. Moreover, cross-border collaborations in clinical trials and bioanalysis are facing operational challenges owing to rising costs and prolonged delivery times for the materials involved. Furthermore, low-cost service markets are increasingly drawing the attention of outsourcing organizations, thereby influencing global demand for bioanalytical testing services.

Technological Advancements

Technological innovations in the bioanalytical testing services industry are aimed at enhancing sensitivity, throughput, and handling of complex data, influenced by the increasing trend towards biological drugs and personalized medicine. High-resolution mass spectrometry and liquid chromatography-mass spectrometry methods are enabling the detection of rare substances, thereby facilitating pharmacokinetics and pharmacodynamics studies in complex drug research projects.

Next-generation sequencing is improving genomic mapping, thereby aiding biomarker identification and targeted treatment design in oncology and rare disease studies. The use of artificial intelligence and machine learning in the bioanalytical testing services industry is revolutionizing data analysis by enabling pattern recognition, predictive modeling, and the elimination of manual intervention in large datasets. Automations and robotics simplify sample preparation and handling, thereby minimizing errors and enhancing consistency in high-throughput testing.

In addition, multiplex immunoassays enable the analysis of multiple biomarkers with limited sample volumes, which is essential for complex biological research and cell and gene therapy trials. These technologies improve efficiency and scalability, enabling CROs to handle higher trial volumes with greater precision. In addition, the possibility of collecting multidimensional datasets has contributed to the trend toward personalized medicine. Moreover, the increased use of such technologies will help consolidate the trend towards outsourcing, as sponsors seek access to dedicated facilities and expertise.

Pricing Model Analysis

Pricing strategies in the bioanalytical testing services industry are becoming sophisticated, reflecting the complexity and duration of the project, as well as its value to the sponsor. The milestone approach is common in structured projects, where payments are made based on distinct milestones such as method development and sample analysis, thereby providing clear financial visibility for both companies. The value pricing strategy has become popular in projects related to advanced biologics and personalized medicine, where costs are tied to outcomes such as improved patient stratification and reduced regulatory delays. Fixed pricing remains important in standard studies, where the scope of work is clearly defined, ensuring accurate budgeting and cost management.

The models that involve subscriptions or retainers are gaining momentum in long-term business arrangements, where sponsors need ongoing bioanalytical support across multiple projects. This model ensures that the service provider has an income stream, whereas the client has guaranteed access to resources. In addition, increasingly flexible pricing models are enhancing the relationship between the value and pricing of these services. Furthermore, outsourcing is driving the use of hybrid models based on the specific requirements of the project.

Molecule Insights

Based on molecule, the small molecule segment led the market with the largest revenue share of 55.1% in 2025 and is expected to grow at the fastest CAGR over the forecast period. Small molecules have been the key factor in pharmaceutical development due to their extensive pharmacokinetics and established manufacturing processes. According to the FDA, bioanalytical method validation for small molecules involves thorough testing to ensure accuracy, precision, and reliability in quantifying drug concentrations in biological matrices. This includes assessing parameters such as selectivity and stability, which are critical for supporting regulatory submissions and ensuring patient safety.

Moreover, the increasing demand for generic drugs and the need for bioequivalence studies are driving the need for bioanalytical testing services tailored to small molecules. Advanced analytical techniques, such as liquid chromatography-mass spectrometry (LC-MS/MS) and high-performance liquid chromatography (HPLC), are widely used to ensure the efficacy, safety, and regulatory compliance of these therapies. Thus, these factors are likely to impact the segment's growth over the analysis period.

The large-molecule segment is expected to grow at the fastest CAGR during the forecast period. The large molecule market is witnessing rapid growth driven by increasing demand for complex biologics, including monoclonal antibodies, therapeutic proteins, and gene therapies. These molecules are more complex than small molecules, which require highly specialized testing techniques to ensure safety, efficacy, and regulatory compliance. Moreover, the rising prevalence of chronic diseases such as cancer, autoimmune disorders, and rare genetic conditions is further fueling the need for biologics, as they offer targeted treatment options.

In addition, advances in technologies such as high-resolution mass spectrometry, ligand-binding assays, and multiplexed immunoassays have significantly improved the ability to characterize and quantify large molecules, enabling the development and approval of these therapies faster and more reliably. The outsourcing of bioanalytical testing to CROs has become increasingly common, allowing pharmaceutical companies to access specialized expertise, reduce timelines, and focus resources on core drug development activities.

Test Insights

Based on test, the bioavailability segment led the market with the largest revenue share in 2025. The growth is attributed to the use of bioavailability tests to determine the rate at which the drug is absorbed and available in the bloodstream. In addition, increasing production of biologics and specialty drugs is expected to drive investment in advanced techniques such as LC-MS/MS and HPLC, which measure drug concentrations in biological samples, ensuring accurate pharmacokinetic profiling, regulatory compliance, and optimized drug formulation and delivery efficiency.

Furthermore, the growing number of generic drug launches has fueled demand for bioavailability studies to establish therapeutic equivalence. Regulatory agencies such as the FDA and EMA have also mandated comprehensive bioavailability testing for both new and reformulated drugs, underscoring the need for specialized analytical services.

The ADME segment is projected to grow at the fastest CAGR during the forecast period. This growth is driven by the increasing use of ADME to understand a drug’s behavior in the body and its absorption, distribution, metabolism, and excretion. Besides, these provide critical data for determining pharmacokinetics, optimizing dosing, predicting drug interactions, and ensuring safety and efficacy throughout drug development and regulatory approval.

In addition, advanced analytical platforms, such as high-resolution mass spectrometry, LC-MS/MS, and cell-based models, are now routinely used to evaluate metabolic pathways, drug-drug interactions, and potential accumulation risks. Moreover, regulatory agencies like the FDA and EMA emphasize the integration of ADME data early in the development cycle to support investigational new drug (IND) applications and ensure translational reliability between preclinical and clinical studies. As a result, ADME bioanalytical testing services have become an important tool in drug development, driving efficiency, regulatory compliance, and informed decision-making in pharmaceutical research.

Workflow Insights

Based on workflow, the sample analysis segment led the market with the largest revenue share in 2025. The segment’s growth is driven by increasing demand for accurate pharmacokinetic and pharmacodynamic data, rising clinical trial activity, and the development of complex biologics and personalized medicines. In addition, the growing adoption of advanced technologies is expected to drive outsourcing to specialized CROs, further contributing to segment growth.

The sample collection and preparation segment is expected to grow at the fastest CAGR during the forecast period, as the workflow plays a major role in ensuring the accuracy and reliability of analytical results. The sample collection and preparation phase involves standardized collection of biological specimens, such as blood, plasma, serum, and urine, followed by stabilization and preparation for downstream analytical assays. The growing complexity of biologics and cell- and gene-based therapies has increased the demand for precise collection and preparation protocols that minimize degradation and maintain analyte integrity. Moreover, as regulatory guidelines are becoming increasingly stringent, the FDA and EMA are requiring pre-analytical processes, CROs, and CDMOs to invest heavily in advanced biorepository infrastructure and automation technologies. Besides, biological samples require proper handling, labeling, and storage to maintain sample integrity and prevent contamination or degradation, thereby further driving growth in the market segment.

End Use Insights

Based on end use, the pharma & biopharma companies segment led the market with the largest revenue share in 2025 and is projected to grow at the fastest CAGR during the forecast period. Several pharmaceutical and biopharmaceutical companies are at the forefront of drug discovery, development, and commercialization. This has led pharmaceutical companies to focus on small-molecule drugs, while biopharma specializes in biologics, including proteins, antibodies, and gene therapies. Moreover, these companies invest heavily in R&D, collaborate with CROs for bioanalytical testing, and navigate stringent regulatory requirements to ensure the safety, efficacy, and quality of innovative therapeutics for global healthcare markets.

The CRO segment is expected to grow at the second-fastest CAGR during the forecast period, as these providers offer services to pharmaceutical and biopharmaceutical companies, supporting drug discovery, development, and regulatory compliance. They offer expertise in clinical trials, bioanalytical testing, pharmacokinetics, and laboratory services, enabling sponsors to reduce costs, accelerate timelines, and access specialized technology. Thus, driving the segment growth over the forecast period.

Regional Insights

North America dominated the bioanalytical testing services market with the largest revenue share of 47.4% in 2025. The growth in the region is mainly driven by rising demand for biopharmaceuticals, ongoing technological advancements, and increased investment in R&D for new drugs. Furthermore, growing innovations in mass spectrometry, chromatography, and other analytical methods have enhanced the sensitivity, specificity, and throughput of testing processes. These technologies have enabled laboratories to conduct more precise and efficient analyses, facilitating faster drug development timelines and reducing costs.

Moreover, the biopharmaceutical & biotechnology industries in the region are rapidly expanding, with a growing focus on the accuracy, safety, and efficacy of drug candidates. This has increased the need for bioanalytical testing services to accelerate R&D, reduce clinical risk, and ensure regulatory compliance. These services, offered through advanced analytical platforms, enhance product quality, shorten development timelines, and drive innovation in biopharmaceutical and biotechnology pipelines. In addition, the region's strong R&D ecosystem and focus on personalized medicine are accelerating the adoption of innovative analytical solutions to support faster, safer, and more effective drug development.

U.S. Bioanalytical Testing Services Market Trends

The bioanalytical testing services market in the U.S. held the largest share in the North America region in 2025. The market is experiencing growth due to the expansion of CROs, increased investment in biopharmaceutical R&D, rising number of clinical trials, and growing demand for personalized medicine, coupled with strong regulatory supervision by the FDA, which further promotes high-quality analytical standards. In addition, the growing demand for biopharmaceuticals and rising drug safety requirements has increased reliance on bioanalytical testing services, which allow companies to access cost-effective expertise, further boosting demand for these services in the market. Furthermore, the expanding biologics & biosimilars sector is anticipated to drive demand for advanced techniques, including immunogenicity, pharmacokinetics, and stability testing, thereby increasing the adoption of sophisticated analytical methods, in turn, contributing to the growth of the market in the country.

The Canada bioanalytical testing services market is expected to grow at a significant CAGR during the forecast period, driven by the growth of the pharmaceutical and biotechnology sectors, the development of biologics and biosimilars, and stringent regulatory compliance requirements. In Canada, the supportive regulatory framework is expected to drive the investment in clinical trials, enabling faster approvals of innovative therapies & creating opportunities for bioanalytical service providers. This has led most pharmaceutical and biotechnology companies to rely on CROs to outsource their bioanalytical testing for cost-effective operation and access to specialized expertise. Moreover, due to a supportive regulatory framework, several companies collaborate with market players, academic institutions, and CROs to strengthen their market innovations and expand their service capabilities. Thus, the aforementioned factors are anticipated to present new growth opportunities to leverage advanced technologies, strategic partnerships & regulatory support to meet client needs for high-quality, reliable bioanalytical services.

Europe Bioanalytical Testing Services Market Trends

The bioanalytical testing services market in Europe is experiencing steady expansion, driven by technological advancements, an increasing number of clinical trials, and the emergence of key players offering advanced analytical testing solutions. Besides, the region has become a hub for clinical research due to its diverse patient populations and well-established regulatory frameworks. This has led to a need for robust bioanalytical testing in the region, driven by the growing demand to monitor the pharmacokinetics, pharmacodynamics, and safety profiles of new drugs. Therefore, the growing number of clinical studies in the field is expected to drive demand for bioanalytical testing services, further necessitating that service providers expand their capabilities and offerings.

Moreover, growing outsourcing trends among pharmaceutical companies to specialized CROs to enhance operational efficiency and compliance with EMA and FDA guidelines are expected to drive the market growth. Countries like Germany, the UK, and France are leading hubs due to their advanced laboratory infrastructure and skilled scientific workforce. Thus, integrating technology such as automation, digital data management, and biomarker-based testing is further transforming the region's analytical workflows. Also, the region remains a pivotal market supporting global clinical research and regulatory approval processes through robust bioanalytical testing capabilities.

The Germany bioanalytical testing services market is expected to witness significant growth, owing to its strong pharmaceutical and biotechnology sectors, advanced R&D infrastructure, highly skilled workforce, and stringent regulatory standards. In addition, the increasing prevalence of chronic diseases has driven the demand for biologics, biosimilars, and specialty drugs, further creating a growing need for reliable, compliant bioanalytical testing services for the development of these drugs. Some other factors contributing to market growth include the increasing number of CROs offering comprehensive services such as LC-MS/MS, immunoassays, pharmacokinetics, and biomarker analysis, which further support market growth.

The bioanalytical testing services market in the UK is expected to grow at a substantial CAGR over the forecast period. The rising pharmaceutical manufacturing capabilities, stringent regulatory standards, extensive R&D initiatives, robust clinical research activities, and a growing demand for biologics, biosimilars & personalized medicine drive the UK market. Besides, growing advancements in bioanalytical techniques further drive collaboration among CROs and academic institutions, along with government support for life sciences innovation, speeding up the need for secure, compliant, and reliable bioanalytical testing services to meet quality standards and compliance requirements. In addition, the country's requirements for biologics, biosimilars, and personalized medicine help boost targeted, effective therapies through strong research. Moreover, government focus and investments by pharmaceutical and biotech companies are expected to drive the collaboration for bioanalytical testing services.

Asia Pacific Bioanalytical Testing Services Market Trends

The bioanalytical testing services market in the Asia Pacific is anticipated to grow at the fastest CAGR during the forecast period, driven by the rapid expansion of pharmaceutical and biotechnology companies, rising healthcare expenditures, increased international trade for biologics and biosimilars, and the ongoing development of the healthcare industry in emerging countries. Other factors contributing to market growth are low service costs, adherence to evolving GDP standards, improved access to medicines, and increasing focus on regulatory compliance & technological advancements, further supporting market growth.

Furthermore, demand for outsourcing services, such as bioanalytical testing, has surged to facilitate market innovation in biologics and biosimilars. This has led to a growing need for cost-effective bioanalytical testing services, with technological advancements expected to support the market. Such factors are expected to drive the market over the estimated period.

The China bioanalytical testing services market is driven by its attractive destination for outsourcing clinical trials, the increasing prevalence of chronic diseases, and the rising demand for advanced therapies and high-quality healthcare products. Besides, the expansion of domestic and international pharmaceutical & biopharmaceutical manufacturing capabilities, along with strong government initiatives to improve healthcare accessibility and efficiency, has led to a significant increase in the outsourcing of bioanalytical testing operations. Moreover, increased R&D investments, stringent quality standards, and a regulatory framework for innovative drug development have created a growing need for specialized bioanalytical testing services that ensure testing accuracy, efficiency, and compliance with global regulatory requirements.

The bioanalytical testing services market in Japan is driven by the growing demand for advanced medical treatments, a strong focus on precision medicine and regenerative therapies, and the expansion of its pharmaceutical/biopharmaceutical sectors. In addition, the growing prevalence of chronic and lifestyle-related diseases has increased the need for high-quality analytical services that comply with an established regulatory framework aligned with PMDA and ICH guidelines. In addition, government policies aimed at improving healthcare access and the country's emphasis on quality and precision operations have fueled the market growth. Moreover, collaborations among CROs, academic institutions, and global pharmaceutical companies strengthen the country's position as a regional hub for bioanalytical research supporting innovation in drug discovery, development, and quality assurance across therapeutic areas.

The India bioanalytical testing services market is growing rapidly due to the expansion of the biopharmaceutical and biotechnology sectors, rising clinical trial activity, and increasing demand for high-quality bioequivalence and bio-similarity studies. In addition, the government's "Make in India" initiatives and favorable regulatory reforms for the pharmaceutical sector are encouraging investment in advanced analytical infrastructure, thereby contributing to market growth. In addition, the growth of personalized medicine further drives the need for precise biomarker and pharmacokinetic analysis.

Latin America Bioanalytical Testing Services Market Trends

The bioanalytical testing services market in Latin America is driven by rising demand for pharmaceuticals and biopharmaceuticals, expanding regional drug manufacturing, and growing government initiatives to improve access to essential medicines. In addition, the presence of major countries such as Brazil and Argentina is expected to drive global demand for drug discovery, leading to an increasing need for advanced analytical techniques to improve the accuracy and efficacy of testing. In addition, growing penetration of digital technologies and the use of advanced analytical instruments further contribute to market growth.

Moreover, government initiatives across Latin America significantly support the adoption of bioanalytical testing services. The presence of regional and national regulatory bodies is strengthening regulatory frameworks across the region to align with international standards, enhancing data reliability and the global acceptance of local trials. Besides, growing public investments, the establishment of advanced bioanalytical laboratories, and rising collaboration with CROs support the market growth in the region.

The Brazil bioanalytical testing services market is driven by factors such as the development of the pharmaceutical/biopharmaceutical & biotechnology industries, increasing investments in clinical research and drug development, and favorable regulatory requirements that attract international CROs, further strengthening the market's capabilities. Some other factors contributing to the market include increasing advancements in laboratory automation and bio-sample analysis, which support improvements in accuracy & efficiency among biopharmaceutical and biotechnology companies.

Middle East and Africa Bioanalytical Testing Services Market Trends

The bioanalytical testing services market in the Middle East & Africa is expected to grow steadily, driven by rising pharmaceutical product requirements, healthcare investments, increasing privatization, and growing government initiatives to improve healthcare infrastructure. The growing number of clinical trials fuels the need for precise pharmacokinetic, pharmacodynamic, and immunogenicity testing services. Some other factors contributing to market growth are the outsourcing of R&D activities by global pharmaceutical companies, advances in analytical technologies, and enhancements in laboratory capabilities that improve testing efficiency & accuracy. Thus, these factors establish MEA as a growing hub for bioanalytical services.

The South Africa bioanalytical testing services market is growing due to the rising emphasis on the biopharmaceutical & clinical research and the expansion of both public and private healthcare sectors. In addition, increasing clinical trial activity, the rising prevalence of chronic and infectious diseases, and government support for advanced drug development and testing are expected to drive the market. In addition, technological advancements in mass spectrometry and chromatography, the growing presence of global CROs, and investment in biosimilar and vaccine development will likely drive demand for testing services in the country.

The bioanalytical testing services market in UAE is growing due to key factors such as rising investment in healthcare infrastructure, expanding biopharmaceutical R&D, and increasing demand for high-quality biologics and biosimilars. Besides, growing strategic collaborations among international CROs and UAE-based companies are expected to enhance the technological capabilities and services, further contributing to market growth. In addition, modernized regulations and efforts to improve access to specialized therapies have increased the need for efficient, compliant testing services in the country.

Key Bioanalytical Testing Services Company Insights

The key players operating across the bioanalytical testing services industry are adopting strategic initiatives such as service launches, mergers & acquisitions, partnerships & agreements, and expansions to gain a competitive edge in the market.

For instance, in June 2025, Svar Life Science and Lablytica Life Science entered into a strategic partnership to strengthen bioanalytical services using LC-MS/MS technology to conduct pharmacokinetic, pharmacodynamic, and biomarker studies.

Key Bioanalytical Testing Services Companies

The following key companies have been profiled for this study on the bioanalytical testing services market.

-

Thermo Fisher Scientific, Inc.

-

ICON plc

-

Charles River Laboratories

-

Laboratory Corporation of America Holdings.

-

IQVIA Inc.

-

Syneos Health

-

SGS SA

-

Intertek Group Plc

-

Pace Analytical Services, LLC

-

Medpace Holdings, Inc.

-

WuXi AppTec

Competitive Benchmarking

Category

Operating Strategies

Competitive Edge

Weakness

Established Players ( Thermo Fisher Scientific, Inc., ICON plc, Charles River Laboratories, Laboratory Corporation of America Holdings)

- End-to-end integration across preclinical and clinical bioanalytical services; global footprint expansion via acquisitions and capacity build-out; strong investment in automation, digitalization, and data analytics; deep strategic partnerships with large pharma and biopharma sponsors for scalable outsourcing models.

- Strong global scale and regulatory credibility; diversified service portfolios across drug development value chain; advanced technological and analytical capabilities; robust sponsor relationships; ability to manage complex, multi-regional clinical programs with high compliance standards.

- High cost structure and lower operational agility; limited flexibility for small/customized studies; integration challenges from frequent acquisitions; exposure to pharma outsourcing cyclicality; slower decision-making impacting responsiveness.

Emerging Players (Pace Analytical Services, LLC, Medpace Holdings, Inc.)

- Focus on niche therapeutic areas and mid-sized biotech clients; expansion through asset-light and cost-efficient models; emphasis on agility, speed, and customization; selective geographic expansion; partnerships to scale capabilities without heavy capital investment.

- High operational agility and faster turnaround times; competitive pricing models; strong customization capabilities; focused domain expertise in select therapeutic areas; lean organizational structure enabling client-centric service delivery.

- Limited global scale and infrastructure; constrained financial and technological resources; narrower service portfolio; high client concentration risk; limited ability to compete for large-scale global outsourcing contracts.

Recent Developments

-

In October 2025, Intertek launched expert E&L testing services in Switzerland to help pharmaceutical companies meet new mandatory Korean Pharmacopeia safety requirements for drugs, packaging, and delivery systems.

-

In February 2025, Charles River collaborated with Singapore General Hospital to provide CGMP-compliant master cell banking and NGS testing for cord blood-derived allogeneic CAR-T cell cancer therapies.

Bioanalytical Testing Services Market Report Scope

Report Attribute

Details

Market size in 2025

USD 5.3 billion

Estimated market size in 2026

USD 5.8 billion

Projected market size by 2033

USD 11.2 billion

Growth rate

CAGR of 9.9% from 2026 to 2033

Historical data

2021 - 2025

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Molecule, test, workflow, end use, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S., Canada, Mexico, UK, Germany, France, Italy, Spain, Denmark, Sweden, Norway, Japan, China, India, Thailand, South Korea, Australia, Brazil, Argentina, South Africa, Saudi Arabia, UAE, Kuwait, Oman, Qatar.

Key companies profiled

Thermo Fisher Scientific, Inc., ICON plc, Charles River Laboratories, Laboratory Corporation of America Holdings, IQVIA Inc., Syneos Health, SGS SA, Intertek Group Plc, Pace Analytical Services, LLC, Medpace Holdings, Inc., WuXi AppTec, among others.

Customization scope

Free report customization (equivalent up to 8 analysts' working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Bioanalytical Testing Services Market Report Segmentation

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global bioanalytical testing services market based on molecule, test, workflow, application, end use, and region.

-

Molecule Outlook (Revenue, USD Million, 2021 - 2033)

-

Small Molecule

-

Large Molecule

-

LC-MS Studies

-

Immunoassays

-

Pharmacokinetics (PK)

-

ADA Assay

-

Other

-

-

Other Large Molecule Tests

-

-

-

Test Outlook (Revenue, USD Million, 2021 - 2033)

-

ADME

-

In-vivo

-

In-vitro

-

-

Pharmacokinetics (PK)

-

Pharmacodynamics (PD)

-

Bioavailability

-

Bioequivalence

-

Biomarker Testing

-

Cell-based Assay

-

Virology Testing

-

Other Tests

-

-

Workflow Outlook (Revenue, USD Million, 2021 - 2033)

-

Sample Collection and Preparation

-

Sample Collection, Handling, and Storage

-

Protein Precipitation

-

Liquid-Liquid Extraction

-

Solid Phase Extraction

-

Others

-

-

Method Development and Validation

-

Sample Analysis

-

Hyphenated technique

-

Chromatographic technique

-

Electrophoresis

-

Ligand Binding Assay

-

Mass Spectrometry

-

Spectroscopic Techniques

-

Nuclear Magnetic Resonance (NMR)

-

Others

-

-

Genomic and Molecular Techniques

-

Polymerase Chain Reaction (PCR)

-

Next-Generation Sequencing (NGS)

-

Others

-

-

-

Other processes

-

-

End Use Outlook (Revenue, USD Million, 2021 - 2033)

-

Pharma & BioPharma Companies

-

CDMO

-

CRO

-

Others

-

-

Regional Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

UK

-

Germany

-

France

-

Italy

-

Spain

-

Denmark

-

Sweden

-

Norway

-

-

Asia Pacific

-

Japan

-

China

-

India

-

Australia

-

Thailand

-

South Korea

-

-

Latin America

-

Brazil

-

Argentina

-

-

Middle East & Africa

-

South Africa

-

UAE

-

Saudi Arabia

-

Kuwait

-

Qatar

-

Oman

-

-

Research Methodology

Segment Definition

Segment - Molecule

Definition

Small Molecule

The segment captures revenue generated by providing small molecule bioanalytical testing services to sponsors. It includes quantitative and qualitative analysis of chemically synthesized drug compounds, metabolites, and related substances in biological matrices to support pharmacokinetic, bioavailability, bioequivalence, toxicology, and clinical studies.

Large Molecule

The segment captures revenue generated by providing large molecule bioanalytical testing services to sponsors. It includes testing of biologics such as monoclonal antibodies, proteins, peptides, vaccines, gene therapies, and biosimilars to support drug development, regulatory submissions, and clinical research programs.

LC-MS Studies

The segment captures revenue generated by providing LC-MS (Liquid Chromatography-Mass Spectrometry) bioanalytical testing services for large molecules to end users. The segment includes quantitative and qualitative analysis of peptides, oligonucleotides, antibody-drug conjugates (ADCs), protein fragments, biomarkers, and complex biologics using hybrid LC-MS platforms for pharmacokinetic, biomarker, and metabolite characterization studies.

Immunoassays

The segment captures revenue generated by providing immunoassay-based bioanalytical testing services for large molecules to end users. The segment includes ligand-binding assays (LBAs), ELISA, ECL, MSD, RIA, and other antibody-based analytical methods used for quantification, characterization, and monitoring of biologics, biosimilars, monoclonal antibodies, recombinant proteins, and related biomarkers.

Pharmacokinetics (PK)

The segment captures revenue generated by providing pharmacokinetic (PK) bioanalytical testing services for large molecules to end users. The segment includes drug concentration measurement, absorption, distribution, metabolism, and excretion (ADME) profiling, exposure assessment, dose proportionality studies, bioavailability evaluation, and PK data generation for biologics, biosimilars, peptides, and other therapeutic proteins.

ADA Assay

The segment captures revenue generated by providing anti-drug antibody (ADA) bioanalytical testing services for large molecules to end users. The segment includes immunogenicity assessment through screening, confirmatory, titration, and neutralizing antibody assays designed to detect and characterize immune responses against therapeutic proteins, monoclonal antibodies, gene therapies, and other biologic products.

Other

The segment captures revenue generated by providing other specialized bioanalytical testing services for large molecules to end users that are not classified under LC-MS studies, immunoassays, or ADA assays. The segment includes customized analytical methods, exploratory biomarker testing, potency assessments, and emerging large-molecule analytical services supporting preclinical and clinical development programs.

Other Large Molecule Tests

The segment captures revenue generated by providing other large-molecule bioanalytical testing services to end users. The segment includes biomarker assays, cell-based assays, neutralizing antibody testing, receptor occupancy studies, potency testing, pharmacodynamic assessments, target engagement analysis, and other specialized analytical evaluations performed for biologics, vaccines, cell and gene therapies, and advanced therapeutic products.

Segment - Test

Revenue capture definition

ADME

The segment captures revenue generated by providing ADME (Absorption, Distribution, Metabolism, and Excretion) bioanalytical testing services to sponsors. It includes analysis of drug absorption, tissue distribution, metabolic pathways, and elimination profiles using biological samples to support preclinical and clinical drug development.

In-vivo

The segment captures revenue generated by providing in-vivo ADME bioanalytical testing services to sponsors. It includes analysis of absorption, distribution, metabolism, and excretion characteristics of drug candidates in animal models and human subjects through the measurement of drug and metabolite concentrations in biological matrices to support preclinical and clinical development.

In-vitro

The segment captures revenue generated by providing in-vitro ADME bioanalytical testing services to sponsors. It includes laboratory-based studies using biological systems such as liver microsomes, hepatocytes, recombinant enzymes, plasma, and cell cultures to evaluate metabolic stability, enzyme interactions, permeability, protein binding, and other ADME properties during early-stage drug development.

Pharmacokinetics (PK)

The segment captures revenue generated by providing pharmacokinetic (PK) bioanalytical testing services to sponsors. It includes measurement and analysis of drug and metabolite concentrations in biological matrices over time to evaluate absorption, distribution, metabolism, and excretion characteristics.

Pharmacodynamics (PD)

The segment captures revenue generated by providing pharmacodynamic (PD) bioanalytical testing services to sponsors. It includes assessment of the biological and physiological effects of a drug, including target engagement, mechanism of action, and dose-response relationships using biomarkers and other analytical endpoints.

Bioavailability

The segment captures revenue generated by providing bioavailability bioanalytical testing services to sponsors. It includes measurement and comparison of the rate and extent of drug absorption into systemic circulation to support formulation development and regulatory submissions.

Bioequivalence

The segment captures revenue generated by providing bioequivalence bioanalytical testing services to sponsors. It includes comparative analysis of pharmacokinetic parameters between reference and test drug products to demonstrate therapeutic equivalence and support generic drug approvals.

Biomarker Testing

The segment captures revenue generated by providing biomarker testing bioanalytical services to sponsors. It includes identification, quantification, and validation of molecular, cellular, genetic, or protein biomarkers used to evaluate disease progression, therapeutic response, patient stratification, and clinical outcomes.

Cell-based Assay

The segment captures revenue generated by providing cell-based assay bioanalytical testing services to sponsors. It includes in vitro testing using living cells to assess drug potency, efficacy, toxicity, mechanism of action, and biological activity during drug development and regulatory evaluation.

Virology Testing

The segment captures revenue generated by providing virology bioanalytical testing services to sponsors. It includes viral detection, viral load quantification, infectivity assessment, viral clearance studies, and related testing required for vaccine, gene therapy, biologics, and antiviral drug development programs.

Other Tests

The segment captures revenue generated by providing other bioanalytical testing services to sponsors. It includes specialized analytical services such as immunogenicity assessments, neutralizing antibody testing, receptor occupancy studies, method development and validation, and other bioanalytical evaluations not classified under the specified categories.

Segment - Workflow

Revenue capture definition

Sample Collection and Preparation

The segment captures revenue generated by providing sample collection and preparation bioanalytical testing services to sponsors. It includes biological sample collection, handling, processing, storage, extraction, purification, and preparation of samples such as blood, plasma, serum, urine, and tissue for subsequent bioanalytical testing and analysis.

Sample Collection, Handling, and Storage

The segment captures revenue generated by providing sample collection, handling, and storage bioanalytical testing services to sponsors. It includes the collection, labeling, transportation, processing, handling, tracking, and controlled storage of biological samples such as blood, plasma, serum, urine, and tissue to maintain sample integrity prior to bioanalytical testing.

Protein Precipitation

The segment captures revenue generated by providing protein precipitation bioanalytical testing services to sponsors. It includes sample preparation procedures that remove proteins from biological matrices using precipitation agents to improve analyte recovery and facilitate accurate quantitative bioanalytical analysis.

Liquid-Liquid Extraction

The segment captures revenue generated by providing liquid-liquid extraction bioanalytical testing services to sponsors. It includes sample preparation techniques that separate and concentrate target analytes from biological matrices using immiscible solvent systems to enhance analytical sensitivity and selectivity.

Solid Phase Extraction

The segment captures revenue generated by providing solid phase extraction bioanalytical testing services to sponsors. It includes sample purification and analyte isolation procedures using solid sorbent materials to remove matrix interferences and improve the accuracy, precision, and sensitivity of bioanalytical assays.

Others

The segment captures revenue generated by providing other sample preparation bioanalytical testing services to sponsors. It includes techniques such as supported liquid extraction, filtration, centrifugation, dilution, derivatization, microextraction, and other specialized sample processing methods not classified under protein precipitation, liquid-liquid extraction, or solid phase extraction.

Method Development and Validation

The segment captures revenue generated by providing method development and validation bioanalytical testing services to sponsors. It includes the design, optimization, qualification, and validation of analytical methods to ensure accuracy, precision, sensitivity, specificity, reproducibility, and regulatory compliance for the measurement of drugs, metabolites, biomarkers, and biologics in biological matrices.

Sample Analysis

The segment captures revenue generated by providing sample analysis bioanalytical testing services to sponsors. It includes the qualitative and quantitative measurement of drugs, metabolites, biomarkers, and biologics in biological matrices using validated analytical methods to support preclinical and clinical studies.

Hyphenated technique

The segment captures revenue generated by providing hyphenated technique bioanalytical testing services to sponsors. It includes analytical methods that combine two or more technologies, such as LC-MS/MS and GC-MS, to improve analyte separation, identification, characterization, and quantification in biological samples.

Chromatographic technique

The segment captures revenue generated by providing chromatographic technique bioanalytical testing services to sponsors. It includes analytical methods such as liquid chromatography (LC), high-performance liquid chromatography (HPLC), ultra-performance liquid chromatography (UPLC), and gas chromatography (GC) used to separate and quantify analytes in biological matrices.

Electrophoresis

The segment captures revenue generated by providing electrophoresis-based bioanalytical testing services to sponsors. It includes analytical techniques that separate proteins, peptides, nucleic acids, and other biomolecules based on their charge and size characteristics to support characterization and quality assessment studies.

Ligand Binding Assay

The segment captures revenue generated by providing ligand binding assay (LBA) bioanalytical testing services to sponsors. It includes antibody-antigen or receptor-ligand based analytical methods used to detect and quantify biologics, biomarkers, therapeutic proteins, and immunogenicity responses in biological samples.

Mass Spectrometry

The segment captures revenue generated by providing mass spectrometry bioanalytical testing services to sponsors. It includes highly sensitive analytical techniques used for the identification, characterization, and quantification of drugs, metabolites, peptides, proteins, and biomarkers in biological matrices.

Spectroscopic Techniques

The segment captures revenue generated by providing spectroscopic technique bioanalytical testing services to sponsors. It includes analytical methods such as UV-Visible spectroscopy, fluorescence spectroscopy, infrared spectroscopy, and related techniques used for analyte identification, characterization, and concentration measurement in biological samples.

Nuclear Magnetic Resonance (NMR)

The segment captures revenue generated by providing Nuclear Magnetic Resonance (NMR) bioanalytical testing services to sponsors. It includes the use of NMR spectroscopy for the identification, structural characterization, quantification, and metabolic profiling of drugs, metabolites, biomarkers, proteins, and other biological molecules to support drug discovery, development, and clinical research.

Others

The segment captures revenue generated by providing other spectroscopic technique-based bioanalytical testing services to sponsors. It includes analytical methods such as ultraviolet-visible (UV-Vis) spectroscopy, fluorescence spectroscopy, infrared (IR) spectroscopy, Raman spectroscopy, circular dichroism (CD), and other spectroscopic approaches used for analyte identification, characterization, and quantification in biological samples.

Genomic and Molecular Techniques

The segment captures revenue generated by providing genomic and molecular technique-based method development and validation bioanalytical testing services to sponsors. It includes the development, optimization, qualification, and validation of analytical methods based on molecular biology and genomics technologies, such as PCR, qPCR, digital PCR, next-generation sequencing (NGS), genotyping, and nucleic acid-based assays, to ensure accuracy, sensitivity, specificity, reproducibility, and regulatory compliance for the analysis of genetic materials, biomarkers, and advanced therapeutics.

Polymerase Chain Reaction (PCR)

The segment captures revenue generated by providing Polymerase Chain Reaction (PCR)-based bioanalytical testing services to sponsors. It includes conventional PCR, quantitative PCR (qPCR), reverse transcription PCR (RT-PCR), and digital PCR methods used for the detection, amplification, quantification, and characterization of nucleic acid targets to support drug development, biomarker studies, gene therapy programs, and clinical research.

Next-Generation Sequencing (NGS)

The segment captures revenue generated by providing Next-Generation Sequencing (NGS)-based bioanalytical testing services to sponsors. It includes high-throughput DNA and RNA sequencing, genomic profiling, transcriptomic analysis, mutation detection, gene expression studies, and biomarker identification to support precision medicine, oncology, cell and gene therapy, and clinical development programs.

Others

The segment captures revenue generated by providing other genomic and molecular technique-based bioanalytical testing services to sponsors. It includes methods such as microarray analysis, Sanger sequencing, fluorescence in situ hybridization (FISH), genotyping, nucleic acid hybridization assays, epigenetic analysis, and other molecular biology techniques used for genetic characterization, biomarker assessment, and therapeutic development.

Other processes

The segment captures revenue generated by providing other workflow-related bioanalytical testing services to sponsors. It includes sample management, data analysis, pharmacokinetic data processing, assay transfer, laboratory information management, regulatory documentation support, stability testing, and other bioanalytical workflow activities not classified under sample collection and preparation or method development and validation.

Segment - End Use

Revenue capture definition

Pharma & BioPharma Companies

The segment captures revenue generated by providing bioanalytical testing services to pharmaceutical and biopharmaceutical companies. It includes testing services performed to support drug discovery, preclinical research, clinical trials, regulatory submissions, lifecycle management, and commercialization of small-molecule drugs, biologics, biosimilars, vaccines, and advanced therapies.

CDMO

The segment captures revenue generated by providing bioanalytical testing services to Contract Development and Manufacturing Organizations (CDMOs). It includes analytical support for drug development, process development, formulation studies, manufacturing validation, comparability assessments, stability studies, and quality-related testing conducted on behalf of CDMO clients and their sponsor programs.

CRO

The segment captures revenue generated by providing bioanalytical testing services to Contract Research Organizations (CROs). It includes laboratory testing services subcontracted by CROs to support preclinical and clinical studies, including pharmacokinetic, bioavailability, bioequivalence, biomarker, immunogenicity, and other bioanalytical evaluations required for sponsor-sponsored research programs.

Others

The segment captures revenue generated by providing bioanalytical testing services to other end users. It includes services delivered to academic and research institutes, government organizations, biotechnology startups, nonprofit research organizations, diagnostic developers, and other entities requiring bioanalytical testing support for research, development, regulatory, or clinical applications.

Estimation Model

Bottom-Up Service Revenue Model

Top-Down Market Validation Model

Drug Development Pipeline Demand Model

Provider Revenue Benchmarking & Market Share Model

Market size is estimated by aggregating revenues generated by bioanalytical testing service providers. This is based on factors such as sample volumes processed, average pricing per study, testing complexity, and lab capacity utilization focused on pharmacokinetics, immunogenicity, biomarker, and cell & gene therapy testing services.

Market size is validated through an analysis of pharmaceutical and biopharmaceutical R&D expenditures, outsourcing penetration rates, clinical development spending, and the share of bioanalytical testing in the overall expenditures for CRO and laboratory services across key regions

Estimation is supported by examining clinical trial activity, the pipelines for biologics and biosimilars, ongoing cell and gene therapy programs, and regulatory requirements for bioanalysis, which aids in forecasting the demand for outsourced bioanalytical testing services throughout all stages of development.

Market size is cross-verified through a financial analysis of leading bioanalytical testing service providers. This analysis includes evaluating service-line revenues, laboratory expansion activities, and estimating market share contributions to derive the total industry revenue within global bioanalytical outsourcing networks.

This estimation framework enhances market visibility by integrating service-provider revenues, indicators of clinical development demand, and industry benchmarking, resulting in a comprehensive understanding of the bioanalytical testing services market. The triangulated methodology drives the forecast reliability, effectively captures the evolving dynamics of outsourcing and the requirements for advanced therapy testing. This approach allows for the precise identification of growth opportunities, competitive positioning, and investment priorities, all while reducing dependency on any single-source estimation method.

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

Cross-Segmentation Analysis

Performed cross-sectional analysis across molecule types (small and large molecules), test types, workflows, end users, and regions to identify high-growth combinations, outsourcing intensity, and emerging demand patterns.

Enabled identification of lucrative market niches, optimized investment prioritization, and uncovered untapped growth opportunities across the bioanalytical testing ecosystem.

Industry Outlook, Value Chain & Business Model Assessment

Evaluated industry evolution, sponsor-CRO/CDMO relationships, service delivery models, value chain dynamics, pricing structures, and outsourcing trends across drug development stages.

Provided strategic insights into revenue drivers, margin optimization, partnership opportunities, and evolving customer procurement behavior.

Regional Expansion & Market Entry Strategy

Assessed country-level opportunities, regulatory complexity, clinical trial activity, laboratory infrastructure, and competitive intensity across established and emerging markets.

Supported regional expansion planning, market entry decisions, partnership identification, and resource allocation strategies.

Competitive Dynamics, Capacity & Volume Benchmarking

Benchmarked leading providers based on laboratory capacity, technology adoption (LC-MS, NGS, PCR, automation), turnaround times, service specialization, and M&A activity.

Enabled competitive positioning, capacity planning, identification of acquisition targets, and evaluation of future growth opportunities driven by biologics and advanced therapeutics.

Frequently Asked Questions About This Report

The global bioanalytical testing services market size was valued at USD 5.3 billion in 2025 and is estimated at USD 5.8 billion for 2026.

Key factors include increasing drug development activities for biologics, biosimilars, & personalized medicines; drug approval processes; the increasing complexity of therapeutics; and the rising need for precise analytical validation and regulatory compliance.

The global bioanalytical testing services market is expected to grow at a CAGR of 9.9% from 2026 to 2033, reaching USD 11.2 billion.

The small molecule segment led with a 55.1% revenue share in 2025, while the large molecule is the fastest-growing segment.

Bioavailability held the largest revenue share of 18.7% in 2025, while bioequivalence is the fastest-growing area.

Pharma & biopharma companies held the largest share of 75.0% in 2025 and is the fastest-growing segment.

North America dominated with a 47.4% revenue share in 2025.

Asia Pacific is the fastest-growing region over the forecast period.

Key players include Thermo Fisher Scientific, Inc., ICON plc, Charles River Laboratories, Laboratory Corporation of America Holdings, IQVIA Inc., Syneos Health, SGS SA, Intertek Group Plc, Pace Analytical Services, LLC, Medpace Holdings, Inc., WuXi AppTec, among others.

About the Author(s)

Pharmaceuticals Research Team

Healthcare · PharmaceuticalsThis report was authored by the pharmaceuticals research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the pharmaceuticals segment of the healthcare industry. All findings are based on proprietary healthcare databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.