- Home

- »

- Plastics, Polymers & Resins

- »

-

Biodegradable Packaging Market Size, Industry Report 2033GVR Report cover

![Biodegradable Packaging Market Size, Share & Trends Report]()

Biodegradable Packaging Market (2025 - 2033) Size, Share & Trends Analysis Report By Material (Paper & Paperboard, Bio-plastic, Bagasse), By Product Format (Bottles & Jars, Boxes & Cartons, Cans), By End-use, By Region, And Segment Forecasts

Market Size, 2024

$501.3BMarket Estimate, 2026

$531.1BMarket Forecast, 2033

$876.1BCAGR, 2025–2033

6.5%Biodegradable Packaging Market Summary

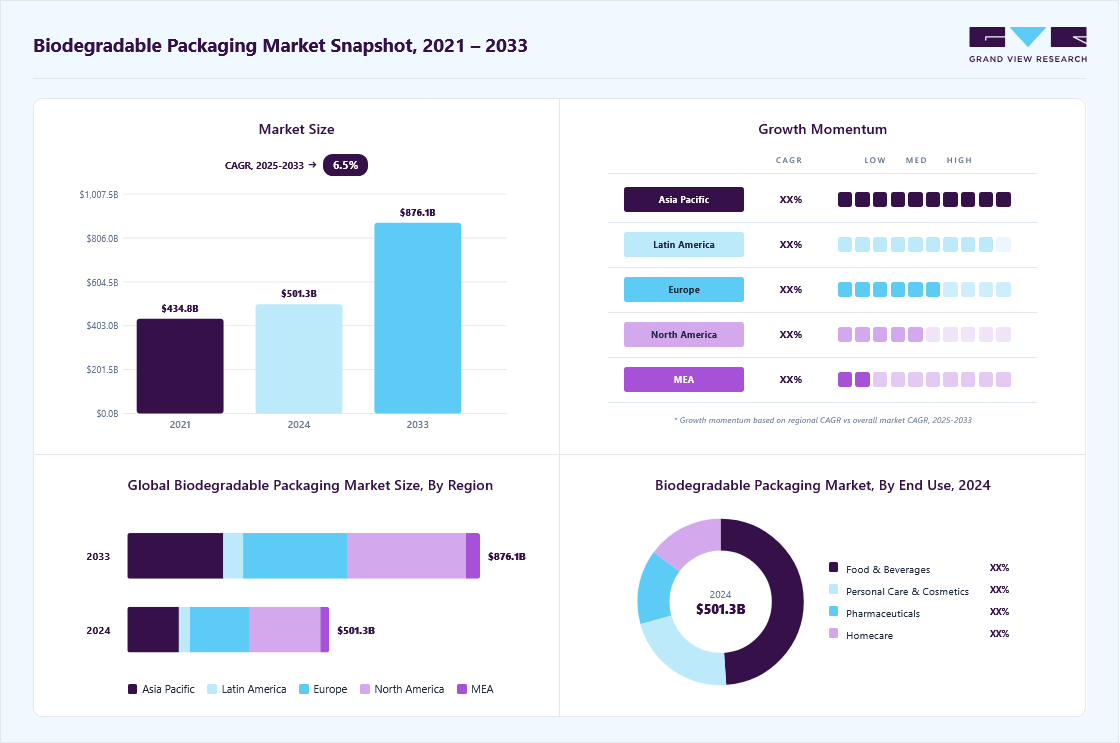

The global biodegradable packaging market size was valued at USD 501.27 billion in 2024 and is expected to reach USD 876.05 billion by 2033, growing at a CAGR of 6.5% from 2025 to 2033. The industry is driven by rising environmental concerns and stringent regulations promoting sustainable alternatives to conventional plastics.

Key Market Trends & Insights

- North America dominated the biodegradable packaging market with the largest revenue share of over 34.0% in 2024.

- The biodegradable packaging market in China is expected to grow at a substantial CAGR of 7.4% from 2025 to 2033.

- By material, the paper & paperboard segment is expected to grow at a fastest CAGR of 7.3% from 2025 to 2033 in terms of revenue.

- By product format, the films & wraps segment is expected to grow at a fastest CAGR of 7.1% from 2025 to 2033 in terms of revenue.

- By end use, the food & beverages segment is expected to grow at a considerable CAGR of 7.9% from 2025 to 2033 in terms of revenue.

Market Size & Forecast

- 2024 Market Size: USD 501.27 Billion

- 2033 Projected Market Size: USD 876.05 Billion

- CAGR (2025-2033): 6.5%

- North America: Largest Market in 2024

- Asia Pacific: Fastest growing Market

Growing consumer demand for eco-friendly packaging in food, beverages, and e-commerce further fuels market growth. Governments across regions are implementing stringent regulations against single-use plastics, forcing industries to adopt sustainable alternatives. For instance, the European Union’s Single-Use Plastics Directive bans products like cutlery and plates made from conventional plastics, creating a direct demand shift toward biodegradable packaging. Similarly, India’s nationwide ban on single-use plastics in 2022 has accelerated adoption across the FMCG and food service sectors. These regulations not only penalize non-compliance but also incentivize companies to innovate with biodegradable solutions.Consumer awareness and preference for eco-friendly packaging are reshaping purchase behaviors. Millennials and Gen Z, in particular, are willing to pay a premium for sustainable products, creating market pressure on brands to adapt. For example, multinational players like Unilever and Nestlé have announced sustainability targets that include expanding biodegradable packaging options. This shift in demand makes biodegradable packaging a strategic differentiator for companies seeking to enhance brand loyalty and appeal to eco-conscious customers.

")

The rapid expansion of food delivery services, quick-service restaurants (QSRs), and e-commerce platforms is fueling the demand for biodegradable packaging. Single-use items such as trays, cutlery, cups, and delivery boxes have been among the biggest contributors to plastic pollution, making biodegradable alternatives highly attractive. For instance, companies such as Zomato and Swiggy in India, and Uber Eats globally, are exploring biodegradable and compostable food containers to align with both consumer expectations and government norms. In e-commerce, giants like Amazon have started introducing biodegradable mailers, reflecting how packaging innovation is becoming integral to supply chain sustainability.

Advances in material science are making biodegradable packaging more cost-effective, durable, and versatile, thus widening its applications. Innovations in biopolymers such as PLA (Polylactic Acid) and PHA (Polyhydroxyalkanoates) allow for packaging that mimics the functionality of plastics but decomposes naturally. At the same time, global brands are pledging to achieve 100% sustainable packaging targets within the next decade. For instance, PepsiCo is testing compostable snack packaging to meet its PepsiCo Positive (pep+) goal of making all packaging recyclable, compostable, biodegradable, or reusable by 2025. These initiatives not only create new growth opportunities but also set industry benchmarks, encouraging smaller players to adopt biodegradable packaging solutions.

Market Dynamics

The global biodegradable packaging market is experiencing rapid growth due to increasing environmental concerns regarding plastic pollution and the growing demand for sustainable packaging alternatives across industries. Governments, consumers, and businesses are actively seeking packaging solutions that reduce landfill waste, lower carbon emissions, and support circular economy initiatives. As a result, biodegradable packaging materials derived from renewable sources such as starch, cellulose, polylactic acid (PLA), bagasse, seaweed, and paper-based materials are gaining significant traction in food & beverages, personal care, healthcare, retail, and e-commerce applications. Rising consumer awareness regarding environmentally responsible consumption and the growing preference for eco-friendly products are encouraging brands to adopt biodegradable packaging as part of their sustainability commitments and corporate environmental strategies.

Another major market driver is the implementation of stringent government regulations and bans on single-use plastics across several countries. Regulatory authorities in North America, Europe, and Asia Pacific are increasingly promoting compostable, recyclable, and biodegradable packaging solutions to reduce environmental damage caused by conventional plastic waste. This regulatory pressure is accelerating investments in biodegradable material innovation, sustainable packaging technologies, and advanced compostable packaging formats. In addition, major global brands are integrating sustainable packaging targets into their long-term business strategies, creating strong demand for biodegradable flexible packaging, food containers, films, pouches, trays, and protective packaging solutions. Technological advancements improving material durability, moisture resistance, shelf life, and printability are also supporting broader commercial adoption of biodegradable packaging products globally.

One of the major restraints impacting the global biodegradable packaging market is the relatively high production cost associated with biodegradable raw materials and specialized manufacturing processes. Compared to conventional petroleum-based plastics, biodegradable packaging materials often require more expensive feedstocks, advanced processing technologies, and lower-volume production systems, leading to higher product prices. This cost gap can limit adoption among price-sensitive industries and consumers, particularly in developing economies. Additionally, certain biodegradable materials may have limitations related to barrier properties, durability, temperature resistance, and shelf life when compared with traditional plastic packaging solutions.

A major challenge in the biodegradable packaging market is achieving the balance between sustainability, product performance, and commercial scalability. Packaging manufacturers must develop biodegradable materials that provide adequate strength, moisture resistance, oxygen barriers, heat stability, and shelf-life protection while maintaining environmental compliance and cost competitiveness. Many industries, particularly food & beverages and healthcare, require high-performance packaging standards that can be difficult to achieve consistently using certain biodegradable materials.

Market Concentration & Characteristics

The industry is strongly shaped by environmental regulations and government policies. Bans on single-use plastics, extended producer responsibility (EPR) schemes, and strict waste management directives create a compliance-driven ecosystem. This regulatory dependency makes the industry sensitive to policy shifts but also ensures a steady demand for sustainable alternatives.

The industry is experiencing robust growth; however, cost remains a critical factor. Biodegradable alternatives are typically more expensive than conventional plastic packaging, which limits adoption in price-sensitive markets. However, falling raw material costs, economies of scale, and rising consumer willingness to pay for eco-friendly options are gradually offsetting this challenge, positioning the market for long-term expansion.

Material Insights

The bio-plastic segment recorded the largest revenue share of over 51.0% in 2024. Bio-plastics are derived from renewable biomass sources such as cornstarch, sugarcane, and cellulose. They are designed to break down naturally under industrial composting conditions. Examples include polylactic acid (PLA) cups, trays, and films, as well as polyhydroxyalkanoates (PHA) used in flexible packaging. Bio-plastics are increasingly used in food packaging, grocery bags, and disposable cutlery. The bio-plastic segment is primarily driven by environmental regulations that limit fossil-based plastics and the growing adoption of circular economy principles in packaging.

The paper & paperboard segment is expected to grow at the fastest CAGR of 7.3% during the forecast period. Paper and paperboard are the most widely used materials in biodegradable packaging due to their renewability, recyclability, and compostable nature. They are commonly used for packaging food, beverages, consumer goods, and pharmaceuticals. Examples include kraft paper bags, paper cups, cartons, and corrugated boxes. The material’s lightweight nature, versatility in printing, and ability to maintain product integrity make it a preferred choice for brands seeking eco-friendly packaging solutions.

Product Format Insights

The pouches & bags segment recorded the largest market revenue share of over 26.0% in 2024. Biodegradable pouches and bags are widely used in retail, food service, and e-commerce. These packaging formats are designed to replace conventional polyethylene or polypropylene bags and pouches, often used for groceries, snacks, and small consumer goods. For instance, eco-friendly grocery bags in supermarkets are increasingly switching to compostable variants. The primary drivers include strict regulations on single-use plastics, rising consumer demand for sustainable alternatives, and the need for brands to showcase environmental responsibility.

The films & wraps segment is expected to grow at the fastest CAGR of 7.1% during the forecast period. Biodegradable films and wraps are mainly applied in food packaging to preserve freshness while reducing environmental impact. They include cling films, shrink wraps, and stretch films made from PLA, cellulose, or other bio-polymers. For example, fresh produce and bakery items are increasingly wrapped in biodegradable films to reduce plastic waste. Rising awareness of plastic pollution, coupled with advancements in biodegradable polymer technology that maintain strength and barrier properties, fuels market growth.

End-use Insights

The food & beverages segment recorded the largest market share of over 42.0% in 2024 and is projected to grow at the fastest CAGR of 6.9% during the forecast period. This positive outlook is due to the growing demand for sustainable solutions in food service, QSRs (quick-service restaurants), and packaged foods. Biodegradable films, trays, and pouches made from PLA (polylactic acid), starch blends, and bagasse are replacing traditional plastics in takeaway boxes, water bottles, and snack packaging. Brands such as Coca-Cola and Nestlé are investing in biodegradable bottles and compostable flexible packaging to meet consumer expectations and regulatory norms.

Biodegradable packaging in personal care & cosmetics is gaining momentum as premium brands adopt eco-conscious packaging to align with sustainability goals. Products such as shampoos, lotions, and makeup now come in biodegradable tubes, jars, and refill packs made from paper, molded fiber, and biopolymers. Companies such as L’Oréal and Unilever are actively piloting compostable pouches and biodegradable bioplastic bottles to reduce their plastic footprint.

Region Insights

North America biodegradable packaging market dominated and accounted for the largest revenue share of over 34.0% in 2024. This positive outlook is due to strong regulatory frameworks and consumer demand for sustainable products. The U.S.andCanada have introduced various legislations to reduce plastic waste, such as bans on single-use plastic bags and straws in states such as California and New York. This regulatory landscape has encouraged businesses to adopt biodegradable alternatives in retail, foodservice, and personal care packaging. Major food chains such as McDonald’s and Starbucks in North America are experimenting with compostable packaging, which directly boosts demand.

U.S. Biodegradable Packaging Market Trends

The biodegradable packaging market in the U.S. is driven by a combination of strong consumer demand, state-level regulations, and innovation leadership. The rise of eco-conscious consumers has also pressured major retailers and foodservice providers to adopt sustainable packaging solutions. The country also serves as a hub for innovation and commercialization of biodegradable packaging technologies. U.S.-based companies such as NatureWorks (producer of Ingeo PLA biopolymer) and Elevate Packaging are leading global supply of biodegradable packaging materials and finished products.

Europe Biodegradable Packaging Market Trends

The biodegradable packaging market in Europe is driven by its strong circular economy initiatives and ambitious sustainability targets set by the European Union. The EU’s Single-Use Plastics Directive (SUPD), which restricts items such as cutlery, plates, and straws, has accelerated the transition to biodegradable and compostable packaging. Countries such as Germany, France, and theNetherlands are frontrunners in adopting biodegradable packaging for foodservice, retail, and e-commerce. Europe’s advanced recycling and composting infrastructure further supports the efficient use of biodegradable packaging. Global players like BASF SE and Novamont, headquartered in Europe, are leading innovations in biodegradable polymers such as Ecovio and Mater-Bi®, which are being used across packaging formats like films, trays, and carrier bags.

Asia Pacific Biodegradable Packaging Market Trends

The biodegradable packaging market in Asia Pacific is expected to grow at the fastest CAGR of 7.2% over the forecast period, owing to its large consumer base, rapid urbanization, and government push for sustainable alternatives to single-use plastics. Countries such as China, India, and Japan are enforcing stringent bans on non-biodegradable plastics, which is encouraging industries to adopt biodegradable solutions in foodservice, e-commerce, and retail packaging. Additionally, the fast-growing food delivery and online grocery sectors in Asia Pacific create a huge demand for eco-friendly packaging, as seen with companies such as Zomato and Swiggy in India increasingly shifting to biodegradable alternatives.

Key Biodegradable Packaging Company Insights

Key players operating in the biodegradable packaging market are undertaking various initiatives to strengthen their presence and increase the reach of their products and services. Strategies such as expansion activities and partnerships are key in propelling the market growth.

Established players such as Amcor plc, Smurfit Westrock, Tetra Pak, DS Smith, and Mondi leverage economies of scale, R&D investments, and strategic partnerships to strengthen their market position, while niche players and startups differentiate through specialized product lines, compostable technologies, or region-specific offerings. Intense rivalry is further fueled by rising sustainability commitments from end-user industries, leading to continuous product development, mergers and acquisitions, and collaborations across the value chain to gain a competitive advantage.

-

In October 2024, Accredo Packaging, with Fresh-Lock closures, launched the first 100% bio-based resin pouch with a zipper at PACK EXPO International 2024. Made from Braskem’s sugarcane-derived polyethylene, the mono-material pouch is recyclable, has a negative carbon footprint, and matches traditional PE in durability and flexibility. Produced with 100% wind energy, it features a resealable Fresh-Lock Renewables zipper, offering a sustainable solution for food, personal care, and healthcare packaging.

-

In January 2024, Sealed Air introduced its first biobased, industrial compostable protein packaging tray at IPPE 2024. The CRYOVAC tray, made from USDA-certified wood cellulose resin with 54% biobased content, matches EPS trays in performance and durability. Certified compostable and biodegradable by BPI and TÜV Austria, it breaks down without toxic residue, supporting company’s sustainability goals to reduce packaging waste and increase renewable content.

Key Biodegradable Packaging Companies:

The following are the leading companies in the biodegradable packaging market. These companies collectively hold the largest market share and dictate industry trends.

- Mondi

- Smurfit Westrock

- DS Smith

- Stora Enso

- Sonoco Products Company

- Tetra Pak

- Amcor plc

- Elevate Packaging

- Notpla Limited

- Greenhope

- CarePac

- EcoPackables

- Taghleef Industries

- TIPA LTD

Competitive Benchmarking

Operating Strategies

Competitive Edge

Weakness

Mature Players: Mondi; Smurfit Westrock; DS Smith; Amcor plc; Tetra Pak

- • Mature companies are heavily investing in recyclable and compostable packaging technologies, renewable raw materials, and circular economy initiatives.

- These players focus on expanding sustainable product portfolios across food & beverages, healthcare, e-commerce, and consumer goods applications.

- Strategic acquisitions, global manufacturing expansion, and partnerships with sustainability-focused organizations are key operational priorities.

- Established companies benefit from strong global supply chains, extensive R&D capabilities, and large-scale manufacturing infrastructure.

- Strong customer relationships and diversified sustainable packaging portfolios support broad market reach and long-term contracts with multinational brands.

- High investments in sustainable material development and manufacturing transitions can increase operational costs.

- Large-scale operations may face slower adaptability to rapidly changing biodegradable material technologies and evolving environmental regulations.

Emerging Players: Notpla Limited; Elevate Packaging; Greenhope; EcoPackables; TIPA LTD

- • Emerging players focus on innovative biodegradable materials such as seaweed-based packaging, compostable films, and bio-based polymer technologies.

- Many companies prioritize niche sustainable packaging applications, direct-to-consumer solutions, and partnerships with environmentally conscious brands.

- • Emerging companies are generally more agile in adopting breakthrough biodegradable technologies and responding to changing sustainability trends.

- Specialized expertise in compostable and bio-based materials helps create strong differentiation in eco-conscious markets.

- • Limited manufacturing scale and higher production costs may reduce competitiveness against larger multinational packaging companies.

- Dependence on developing composting infrastructure, raw material availability, and evolving regulatory standards can create operational uncertainties and profitability challenges.

Biodegradable Packaging Market Report Scope

Report Attribute

Details

Market size value in 2025

USD 531.14 billion

Revenue forecast in 2033

USD 876.05 billion

Growth rate

CAGR of 6.5% from 2025 to 2033

Historical data

2021 - 2023

Forecast period

2025 - 2033

Quantitative units

Revenue in USD million/billion, and CAGR from 2025 to 2033

Report coverage

Revenue forecast, competitive landscape, growth factors, and trends

Segments covered

Material, product format, end-use, region

Regional scope

North America; Europe; Asia Pacific; Latin America; Middle East & Africa

Country scope

U.S.; Canada; Mexico; Germany; France; UK; Italy; Spain; China; India; Japan; Australia; South Korea; Brazil; Argentina; South Africa; Saudi Arabia; UAE

Key companies profiled

Mondi; Smurfit Westrock; DS Smith; Stora Enso; Sonoco Products Company; Tetra Pak; Amcor plc; Elevate Packaging; Notpla Limited; Greenhope; CarePac; EcoPackables; Taghleef Industries; TIPA LTD

Customization scope

Free report customization (equivalent to 8 analyst’s working days) with purchase. Addition or alteration to country, regional, and segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Biodegradable Packaging Market Report Segmentation

This report forecasts revenue growth at a global, regional, and country level and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global biodegradable packaging market report based on material, product format, end-use, and region:

-

Material Outlook (Revenue, USD Million, 2021 - 2033)

-

Paper & Paperboard

-

Bio-plastic

-

Bagasse

-

-

Product Format Outlook (Revenue, USD Million, 2021 - 2033)

-

Bottles & Jars

-

Boxes & Cartons

-

Cans

-

Trays & Clamshells

-

Cups & Bowls

-

Pouches & Bags

-

Films & Wraps

-

Labels & Tapes

-

Others

-

-

End-use Outlook (Revenue, USD Million, 2021 - 2033)

-

Food & Beverages

-

Personal Care & Cosmetics

-

Pharmaceuticals

-

Homecare

-

Others

-

-

Region Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

France

-

UK

-

Italy

-

Spain

-

-

Asia Pacific

-

China

-

India

-

Japan

-

Australia

-

South Korea

-

-

Latin America

-

Brazil

-

Argentina

-

-

Middle East & Africa

-

South Africa

-

Saudi Arabia

-

UAE

-

-

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

Regional Segmentation

Detailed analysis of the global biodegradable packaging market across North America, Europe, Asia Pacific, Latin America, and Middle East & Africa, including country-level sustainability regulations, plastic ban policies, composting infrastructure analysis, biodegradable material adoption trends, raw material availability, and regional growth outlook.

Identify high-growth regional markets and emerging sustainable packaging manufacturing hubs. Support region-specific expansion strategies, sourcing decisions, and sustainability planning. Enable understanding of regional environmental regulations, waste management capabilities, and competitive intensity across end-use industries.

Cross-Segmentation

Detailed market segmentation analysis by material type, packaging format, product type, end-use industry, application, and distribution channel, including volume and value analysis across key countries and regions. The study also covers compostable packaging trends, bio-based material adoption, and flexible versus rigid biodegradable packaging demand.

Enable identification of high-growth product segments and emerging sustainable packaging applications. Support targeted product development, investment prioritization, and portfolio diversification strategies. Help understand evolving customer preferences and environmental compliance requirements across industries.

Trade Assessment

Analysis of global trade flows, import-export trends, bio-based polymer supply dynamics, compostable material trade, tariff structures, sustainability regulations, and regional supply chain dependencies impacting the biodegradable packaging market. The study further evaluates sourcing trends, agricultural feedstock availability, and logistics challenges associated with sustainable packaging production globally.

Support supply chain risk assessment and sustainable sourcing strategy development. Identify major exporting and importing countries, trade bottlenecks, and raw material sourcing opportunities. Enable informed decisions related to procurement diversification, international expansion, and long-term sustainability investments.

Frequently Asked Questions About This Report

The global biodegradable packaging market was estimated at around USD 501.27 billion in the year 2024 and is expected to reach around USD 531.14 billion in 2025.

The global biodegradable packaging market is expected to grow at a compound annual growth rate of 6.5% from 2025 to 2033 to reach around USD 876.05 billion by 2033.

The food & beverages segment dominates the biodegradable packaging market due to the high demand for single-use and sustainable packaging in QSRs, food delivery, and beverage products, driven by regulatory bans on conventional plastics and growing consumer preference for eco-friendly options.

The key players in the biodegradable packaging market include Mondi; Smurfit Westrock; DS Smith; Stora Enso; Sonoco Products Company; Tetra Pak; Amcor plc; Elevate Packaging; Notpla Limited; Greenhope; CarePac; EcoPackables; Taghleef Industries; and TIPA LTD

Bans on single-use plastics, extended producer responsibility (EPR) mandates, and strict recycling norms in regions such as the EU, India, and North America are accelerating the shift toward biodegradable packaging.

About the Author(s)

Plastics, Polymers & Resins Research Team

Bulk Chemicals · Plastics, Polymers & ResinsThis report was authored by the plastics, polymers & resins research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the plastics, polymers & resins segment of the bulk chemicals industry. All findings are based on proprietary bulk chemicals databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.