- Home

- »

- IT Services & Applications

- »

-

Data Center Chip Market Size, Share, Industry Report, 2030GVR Report cover

![Data Center Chip Market Size, Share, & Trends Report]()

Data Center Chip Market (2025 - 2030) Size, Share, & Trends Analysis By Chip Type (Processors, Memory, Networking), By Data Center Type (Small And Medium-Sized Data Centers, Large Data Centers), By Application (Cloud Computing), By End-use, By Region, And Segment Forecasts

Market Size, 2024

$21.2BMarket Estimate, 2026

$23.7BMarket Forecast, 2030

$42.7BCAGR, 2025–2030

12.5%Data Center Chip Market Summary

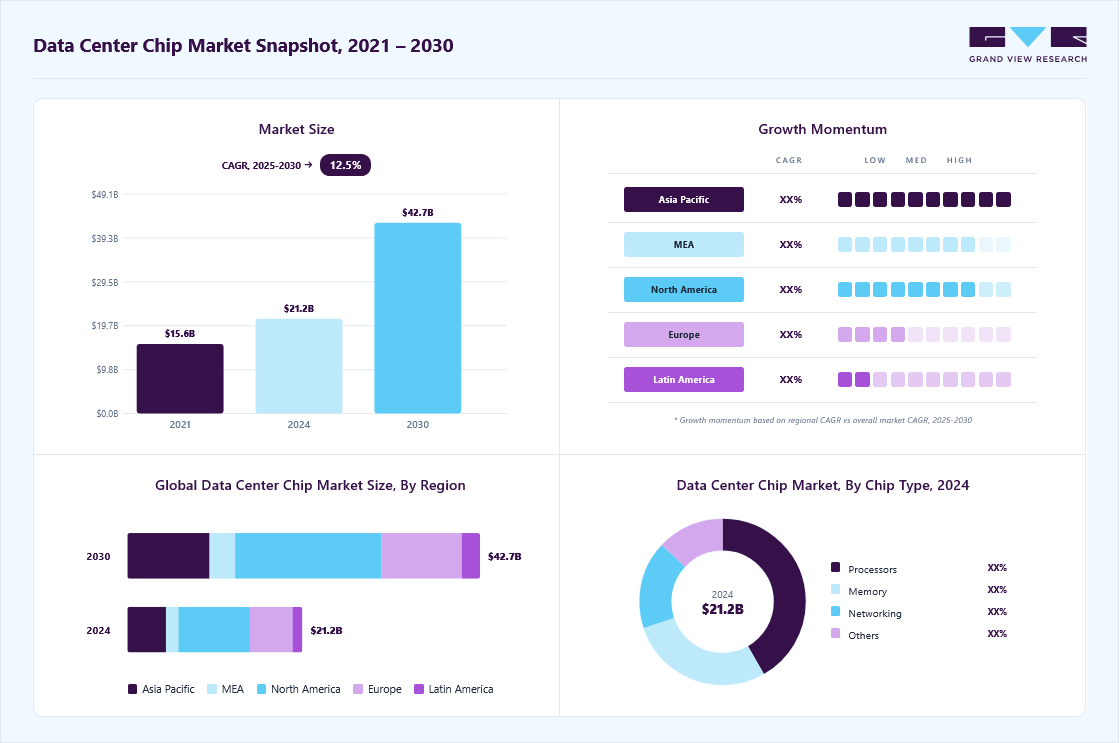

The global data center chip market size was estimated at USD 21.21 billion in 2024 and is projected to reach USD 42.74 billion by 2030, growing at a CAGR of 12.5% from 2025 to 2030. The market is driven by several key factors such as demand for high-performance computing (HPC) and data-intensive applications surges, data centers require more advanced chip technologies to handle massive volumes of data.

Key Market Trends & Insights

- The data center chip market in North America held a significant share of nearly 41.0% in 2024.

- The data center chip market in the U.S. is expected to grow significantly at a CAGR of 12.0% from 2025 to 2030.

- Based on chip type, the processors segment dominated the market and accounted for the revenue share of nearly 42.0% in 2024.

- Based on data center type, the large data centers segment dominated the market in 2024.

- Based on application, the artificial intelligence (AI) segment dominated the market in 2024.

Market Size & Forecast

- 2024 Market Size: USD 21.21 Billion

- 2030 Projected Market Size: USD 42.74 Billion

- CAGR (2025-2030): 12.5%

- North America: Largest market in 2024

- Asia Pacific: Fastest growing market

The increasing adoption of cloud computing, big data analytics, and artificial intelligence (AI) has fueled the need for efficient, high-capacity data center chips. These chips need to meet the processing power demands of modern applications while offering improved energy efficiency, scalability, and performance. The continuous evolution of chip architectures, with innovations such as ARM-based processors and specialized AI chips gaining prominence in the data center chip industry. ARM-based chips are gaining traction due to their energy efficiency, which is critical for large-scale data centers seeking to minimize operational costs. Moreover, the growing adoption of AI and machine learning (ML) workloads in data centers is driving the demand for chips that can handle parallel processing and complex computations with high throughput.")

In addition, the proliferation of edge computing is creating a need for distributed computing resources closer to the data source, further driving demand for data center chips that offer low latency, high processing power, and reduced energy consumption. For instance, in January 2025, ZEDEDA, a U.S.-based company in edge management and orchestration, announced the opening of its new headquarters in Abu Dhabi, UAE. The move is supported by strategic investments from Alpha Wave Incubation and Prosperity7, a subsidiary of Aramco. This growth is driven by the rising demand for edge computing and AI solutions across the Middle East. The increasing reliance on 5G networks, which require robust data center infrastructure for real-time processing and low-latency communication, is also contributing to market growth.

The shift towards hybrid and multi-cloud environments is pushing the demand for more advanced data center infrastructure. Companies require flexible, scalable solutions to manage workloads across various platforms, which in turn increases the demand for high-performance chips that can seamlessly integrate with diverse cloud environments. The rising need for robust cybersecurity solutions in data centers is also spurring innovation in chip designs that offer enhanced security features, such as hardware-based encryption and secure boot mechanisms.

Market Dynamics

Increasing deployment of high-performance computing (HPC) infrastructure is a key growth driver for the data center chip market. HPC systems require extremely powerful processors, GPUs, and specialized accelerators to handle complex simulations, modeling, and data-intensive workloads. These include applications in scientific research, weather forecasting, drug discovery, financial risk modeling, and engineering design. As organizations demand faster and more accurate computational results, investment in HPC clusters is rising across governments, research institutions, and enterprises. This trend significantly boosts demand for advanced chips such as GPUs, AI accelerators, and high-bandwidth memory. It also accelerates innovation in chip architectures, interconnect technologies, and energy-efficient designs to maximize performance at scale.

The increasing deployment of HPC infrastructure is being accelerated by sovereign AI initiatives, as seen in Alibaba’s China-based AI data center using 10,000 in-house Zhenwu chips to reduce reliance on foreign GPUs and scale domestic high-performance compute capacity. The system is designed for large-scale AI training and inference workloads, supporting models with hundreds of billions of parameters and scalable to 100,000 chips. It reflects China’s push for semiconductor self-reliance amid restricted access to advanced Nvidia GPUs. The deployment strengthens domestic AI infrastructure, reduces reliance on foreign chips, and accelerates competition in AI computing ecosystems focused on sovereign cloud and national AI capacity building.

High capital intensity and cost pressures are significant restraints in the data center chip market. Developing advanced chips requires multi-billion-dollar investments in R&D, design tools, and semiconductor fabrication facilities, making entry highly capital-intensive and limiting competition to a few large players. AI accelerators and GPUs are also extremely expensive, which increases the total cost of ownership for hyperscalers, cloud providers, and enterprises deploying large-scale AI infrastructure. In addition, rising costs of high-bandwidth memory (HBM), advanced packaging technologies, and increasing power consumption further strain profitability. These factors collectively slow down adoption, delay large-scale deployments, and create financial pressure across the AI and high-performance computing ecosystem.

Market Concentration & Characteristics

The data center chip market is highly concentrated at the top end of the value chain, particularly in AI accelerators and advanced GPUs, while remaining moderately fragmented in adjacent segments such as networking silicon, CPUs, and memory. A small number of dominant vendors led by NVIDIA, AMD, Intel, and leading hyperscaler custom silicon providers such as Google, AWS, and Microsoft control a disproportionate share of high-performance compute workloads. This concentration is especially pronounced in AI training workloads, where NVIDIA’s CUDA ecosystem and GPU acceleration stack create strong platform dominance and ecosystem lock-in.

The data center chip market is highly technology-intensive and rapidly evolving, driven by the acceleration of AI workloads. Product cycles are shortening as GPU architectures, AI-specific accelerators (XPUs), chiplet-based designs, and the integration of high-bandwidth memory advance. The industry is shifting away from general-purpose CPUs toward workload-optimized silicon designed specifically for AI training and inference efficiency. Demand is primarily driven by the rapid growth of generative AI and large language models, as well as large-scale hyperscaler capital investments from AWS, Microsoft Azure, Google Cloud, and Meta. Additional demand comes from enterprise AI adoption, cloud-native application expansion, high-performance computing and simulation workloads, and increasing sovereign AI initiatives and national digital infrastructure programs aimed at strengthening local compute capacity and technological independence.

Chip Type Insights

The processors segment dominated the market and accounted for the revenue share of nearly 42.0% in 2024, driven by innovations in processor architecture, such as those developed by companies like Intel, AMD, and ARM, are constantly improving computational efficiency, enabling faster processing speeds while reducing energy consumption. This technological advancement plays a crucial role in the adoption of these processors, as data centers seek energy-efficient solutions to lower operating costs. With the growing complexity of applications, such as edge computing, IoT, and virtualized environments, the processors segment in the data center chip market is positioned for sustained growth as these technological demands continue to evolve. The processors segment is further segmented into central processing units (CPUs), Graphics Processing Units (GPUs), field-programmable gate arrays (FPGAs), application-specific integrated circuits (ASICs), and others

The networking segment is anticipated to grow at a CAGR of 14.0% during the forecast period, driven by the adoption of disaggregated and software-defined networking (SDN) architectures, which rely on programmable chips to enhance flexibility and scalability. Open-source initiatives like SONiC (Software for Open Networking in the Cloud) are accelerating this trend, fostering demand for programmable ASICs and FPGAs that enable dynamic traffic management. The rise of edge data centers further amplifies the need for compact, power-efficient networking chips capable of real-time processing for applications like autonomous vehicles and industrial IoT. The networking segment is further segmented intonetwork interface cards (NICs)/network adapters, and interconnects.

Data Center Type Insights

The large data centers segment dominated the market in 2024 due to the exponential demand for hyperscale computing infrastructure. As cloud service providers like AWS, Microsoft Azure, and Google Cloud expand their global footprints to support digital transformation, they require increasingly powerful and efficient chips to manage massive workloads. This has led to a surge in demand for high-performance server CPUs, GPUs, and custom ASICs optimized for virtualization, containerization, and distributed computing. The shift toward AI-as-a-Service (AIaaS) and big data analytics further necessitates advanced silicon capable of handling parallel processing and real-time decision-making at scale.

The small and medium-sized data centers segment is expected to grow at a significant CAGR over the forecast period, driven by the increasing decentralization of computing power and the rise of edge-native applications. Unlike hyperscale facilities, SMDCs prioritize space efficiency, modular scalability, and cost-effective performance, creating a unique demand for chips that balance power with compact designs. The proliferation of IoT devices, Industry 4.0 automation, and real-time analytics is pushing these facilities to adopt system-on-chip (SoC) solutions and low-power ARM-based processors, which deliver high throughput without excessive energy consumption.

Application Insights

The artificial intelligence (AI) segment dominated the market in 2024 due to the rapid adoption of machine learning, deep learning, and generative AI workloads across industries. These applications require specialized processing capabilities that go beyond traditional CPUs, driving demand for GPUs, TPUs, and AI-accelerator chips optimized for matrix operations, parallel computing, and high-speed inference. The deployment of AI in areas such as predictive analytics, autonomous systems, natural language processing, and image recognition is increasing the need for high-performance chips capable of handling massive datasets in real time.

The cloud computing segment is expected to grow at a significant CAGR over the forecast period owing to the global shift from on-premises IT infrastructure to cloud-based platforms. Enterprises across all sectors are increasingly embracing Infrastructure-as-a-Service (IaaS), Platform-as-a-Service (PaaS), and Software-as-a-Service (SaaS) solutions to gain flexibility, reduce capital expenditure, and scale operations rapidly. This transition demands robust and versatile chips that can efficiently manage diverse cloud workloads such as database processing, container orchestration, and serverless computing.

End-use Insights

The IT segment dominated the market in 2024 due to the evolution of DevOps, responsive methodologies, and continuous integration/continuous deployment (CI/CD) pipelines, which require substantial computational power and real-time responsiveness. These demands are fueling the adoption of chips that optimize workload orchestration, virtualization, and containerization. Moreover, the increasing reliance on data-intensive services such as backup and recovery, IT monitoring, and digital workspace management further amplifies the need for efficient, scalable chip solutions.

")

The energy segment is expected to grow at a significant CAGR over the forecast period driven by the increasing adoption of smart grid technologies, digital twins, and real-time energy management systems. As energy companies modernize their infrastructure, they rely heavily on data centers to process vast volumes of operational data for grid monitoring, predictive maintenance, and energy forecasting. This transformation necessitates advanced chips capable of handling time-sensitive and data-intensive workloads, particularly for edge computing scenarios where fast local processing is critical.

Regional Insights

The data center chip market in North America held a significant share of nearly 41.0% in 2024 by the region’s dominance in cloud computing, artificial intelligence (AI), and big data analytics. With major companies such as Amazon, Google, and Microsoft leading the digital transformation, there is a growing demand for advanced data center chips capable of handling large-scale computing workloads. Moreover, the rapid growth of the Internet of Things (IoT) and 5G technologies is accelerating the need for high-performance, energy-efficient chips that can support the increasing data traffic in the region.

U.S. Data Center Chip Industry Trends

The data center chip market in the U.S. is expected to grow significantly at a CAGR of 12.0% from 2025 to 2030 due to the heavy investments in AI/ML, and autonomous systems, which require cutting-edge data center chips. The U.S. continues to invest in next-generation data centers that leverage powerful processors, including specialized AI chips, for enhanced computational capabilities. For instance, in January 2025, Microsoft announced its plans to invest USD 80 billion in AI-powered data centers during 2025, with over half of the funding directed toward projects in the U.S. These new facilities feature cutting-edge technologies, including GPUs and AI accelerator chips, to significantly enhance computing power and support the growing demand for AI-driven solutions.

Europe Data Center Chip Industry Trends

The data center chip market in Europe is anticipated to register a considerable growth from 2025 to 2030, driven by the region's strong push toward digitalization and sustainability. Many European companies are modernizing their data centers with energy-efficient chips to align with green initiatives and carbon-neutral goals. Moreover, the adoption of advanced computing technologies such as AI, blockchain, and cloud computing is fueling the demand for high-performance processors.

The U.K. data center chip market is expected to grow rapidly in the coming years due to the rapid adoption of cloud data center type, digital transformation, and 5G network rollout. The U.K. has been increasingly focusing on improving its infrastructure to support high-speed data processing and storage, which in turn drives the need for advanced data center chips.

The data center chip market in Germany held a substantial market share in 2024, driven by the industrial sector's push toward digitalization and Industry 4.0, which relies on data centers to process real-time data generated by smart factories and automation systems. Germany's automotive industry, in particular, is embracing AI and IoT technologies that require high-performance chips to support autonomous driving and manufacturing processes.

Asia Pacific Data Center Chip Industry Trends

Asia Pacific is expected to register the fastest CAGR of 13.5% from 2025 to 2030, due to the region's booming digital economy and the increasing number of data centers being established to cater to the growing internet user base. Countries such as India and South Korea are witnessing significant investments in data center infrastructure, driving demand for advanced chips capable of supporting massive data processing, cloud computing, and AI applications. The rise of smart cities and IoT in this region is further contributing to the need for efficient, high-performance data center chips.

The data center chip market in Japan is expected to grow rapidly in the coming years. The country’s high reliance on automation in manufacturing and the ongoing adoption of smart technologies are creating a demand for data center chips that can handle complex tasks such as real-time data processing and machine learning. Moreover, Japan’s commitment to reducing energy consumption is encouraging the use of energy-efficient chips in data centers to meet sustainability goals in the country.

The China data center chip market held a substantial market share in 2024. The government's support for the development of a domestic semiconductor industry, combined with the rapid growth of cloud computing, big data, and 5G infrastructure, leads to demand for advanced chips for data centers. Moreover, the increasing adoption of AI and smart devices across various industries, including e-commerce, telecommunications, and manufacturing, is driving the need for efficient processing power.

Key Data Center Chip Company Insights

Key players operating in the data center chip industry are NVIDIA Corporation, Micron Technology, Inc., STMicroelectronics, and Sensirion AG. The companies are focusing on various strategic initiatives, including new product development, partnerships & collaborations, and agreements to gain a competitive advantage over their rivals. The following are some instances of such initiatives.

-

In February 2025, Intel Corporation introduced the Intel Xeon 6 processors, featuring performance cores optimized for delivering top-tier performance in data centers, including up to twice the performance in AI processing. In addition, these new processors, designed for network and edge applications, incorporate Intel vRAN Boost, which enhances capacity by up to 2.4 times for radio access network (RAN) workloads.

-

In February 2025, STMicroelectronics introduced a new computer chip designed for the growing AI in data center developed in partnership with Amazon Web Data center type (AWS). Utilizing photonics technology, the chip relies on light instead of electricity, enhancing speed while reducing power consumption in AI-driven data centers. These advanced chips are expected to play a key role in transceivers, essential components in data center infrastructure.

-

In October 2024, NVIDIA unveiled the NVIDIA Grace CPU, a high-performance data center processor designed to deliver exceptional energy efficiency while being optimized for large-scale data center performance. This new CPU aims to revolutionize the data center industry by offering enhanced energy efficiency and performance at scale.

Key Data Center Chip Companies:

The following are the leading companies in the data center chip market. These companies collectively hold the largest market share and dictate industry trends.

- Advanced Micro Devices, Inc.

- Alibaba

- Arm Holdings

- Broadcom Inc.

- Huawei Technologies Co., Ltd.

- IBM Corporation

- Intel Corporation

- Marvell

- Micron Technology, Inc.

- NVIDIA Corporation

- Qualcomm

- SAMSUNG

- STMicroelectronics

- Texas Instruments Incorporated

Competitive Benchmarking

Operating Strategies

Competitive Edge

Weakness

Mature Players: NVIDIA; AMD; Intel; Samsung Electronics; SK Hynix; Micron Technology

- Building full-stack AI computing ecosystems that combine processors, networking, software frameworks, and developer tools to create end-to-end platforms.

- Investing heavily in next-generation GPU architectures, AI accelerators, chiplet designs, advanced packaging, and high-bandwidth memory integration.

- Securing long-term supply agreements with hyperscalers and expanding partnerships with foundries and memory suppliers to ensure production capacity.

- Developing integrated hardware-software optimization platforms to maximize AI training and inference performance.

- Extensive software ecosystems, mature product portfolios, and large developer communities create significant switching costs and customer retention.

- Proven capability to support hyperscale AI clusters, enterprise data centers, and mission-critical HPC environments at scale.

- Strong financial resources enable sustained R&D investment, access to advanced manufacturing nodes, and long-term supply commitments.

- Established relationships with hyperscalers, OEMs, enterprises, and government organizations provide stable demand and market leadership.

- Dependence on limited advanced foundry capacity, packaging technologies, and HBM supply can create production constraints.

- Premium pricing of advanced AI accelerators increases deployment costs for enterprises and smaller cloud providers.

- Large organizational structures may slow adaptation to disruptive architectural innovations and emerging niche workloads.

- Exposure to geopolitical tensions, export controls, and regional semiconductor regulations can impact growth opportunities.

Emerging Players: Cerebras Systems, Marvell, Tenstorrent, Enfabrica, Astera Labs

- Developing purpose-built AI accelerators optimized for generative AI, LLM inference, and specialized HPC workloads.

- Leveraging innovative architectures such as wafer-scale processors, domain-specific accelerators, chiplet-based designs, and high-speed interconnect technologies.

- Building open and flexible software ecosystems that integrate with existing cloud and enterprise infrastructure.

- Focusing on performance-per-watt optimization and lower total cost of ownership to challenge incumbent architectures.

- Faster innovation cycles allow rapid commercialization of disruptive AI hardware technologies.

- Superior performance and energy efficiency for targeted AI workloads compared with many general-purpose processors.

- Agile organizational structures enable quicker adaptation to evolving AI models and customer requirements.

- Strong expertise in addressing specific challenges such as memory bottlenecks, networking congestion, and inference optimization.

- Limited manufacturing scale and ecosystem maturity compared with established semiconductor vendors.

- Smaller software ecosystems and developer communities can hinder enterprise adoption and workload migration.

- Dependence on external funding, strategic partnerships, and third-party foundries creates business and operational risks.

- Limited sales reach and support infrastructure can restrict participation in large multi-year hyperscaler contracts.

Data Center Chip Market Report Scope

Report Attribute

Details

Market size value in 2025

USD 23.71 billion

Revenue forecast in 2030

USD 42.74 billion

Growth rate

CAGR of 12.5% from 2025 to 2030

Historical data

2018 - 2024

Forecast period

2025 - 2030

Quantitative units

Revenue in USD million/billion and CAGR from 2025 to 2030

Report data center type

Revenue forecast, company share, competitive landscape, growth factors, and trends

Segments covered

Chip type, data center type, application, end-use, and region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; U.K.; Germany; France; China; India; Japan; Australia; South Korea; Brazil; UAE; Kingdom of Saudi Arabia; South Africa

Key companies profiled

Advanced Micro Devices, Inc.; Alibaba; Arm Holdings; Broadcom Inc.; Google; Huawei Technologies Co.; Ltd.; IBM Corporation; Intel Corporation; Marvell; Micron Technology Inc.; NVIDIA Corporation; Qualcomm; SAMSUNG; STMicroelectronics; Texas Instruments Incorporated

Customization scope

Free report customization (equivalent to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Data Center Chip Market Report Segmentation

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2018 to 2030. For this study, Grand View Research has segmented the global data center chip market report based on game chip type, data center type, application, end-use, and region:

-

Chip Type Outlook (Revenue, USD Billion, 2018 - 2030)

-

Processors

-

Central Processing Units (CPUs)

-

Graphics Processing Units (GPUs)

-

Field-Programmable Gate Arrays (FPGAs)

-

Application-Specific Integrated Circuits (ASICs)

-

Others

-

-

Memory

-

High Bandwidth Memory (HBM)

-

Double Data Rate (DDR)

-

-

Networking

-

Network Interface Cards (NICs)/Network Adapters

-

Interconnects

-

-

Others

-

-

Data Center Type Outlook (Revenue, USD Billion, 2018 - 2030)

-

Small and Medium-Sized Data Centers

-

Large Data Centers

-

-

Application Outlook (Revenue, USD Billion, 2018 - 2030)

-

Artificial Intelligence (AI)

-

Cloud Computing

-

Big Data Analytics

-

-

End-use Outlook (Revenue, USD Billion, 2018 - 2030)

-

IT

-

Telecom

-

Healthcare

-

BFSI

-

Retail & E-commerce

-

Entertainment & Media

-

Energy

-

Others

-

-

Regional Outlook (Revenue, USD Billion, 2018 - 2030)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

U.K.

-

Germany

-

France

-

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

Australia

-

-

Latin America

-

Brazil

-

-

Middle East & Africa

-

UAE

-

Saudi Arabia

-

South Africa

-

-

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

Data center chip opportunity assessment for a semiconductor vendor

- Assessment of demand across hyperscale, colocation, enterprise, and AI data centers

- Analysis of adoption trends for CPUs, GPUs, AI accelerators (ASICs), DPUs, and HBM-enabled solutions

- Benchmarking of leading vendors, product roadmaps, and technology positioning

- Identified high-growth public safety software segments

- Supported product positioning and expansion strategy

- Highlighted key adoption drivers, restraints, and regulatory trends

Regional expansion assessment for a data center infrastructure provider

- Demand analysis for data center processors and AI chips across the Middle East region

- Evaluation of sovereign AI initiatives, government incentives, and local semiconductor investments

- Assessment of cloud provider and hyperscaler expansion plans

- Identified attractive regional growth opportunities and priority markets

- Supported expansion and partnership strategies

- Highlighted regulatory developments, infrastructure investments, and future demand hotspots

Technology roadmap assessment for an enterprise AI infrastructure provider

- Comparative analysis of next-generation CPUs, GPUs, XPUs, chiplet architectures, and HBM technologies

- Evaluation of performance, power efficiency, and total cost of ownership (TCO)

- Assessment of future technology adoption timelines and commercialization trends

- Supported technology investment and procurement decisions

- Identified emerging disruptive technologies and vendors

- Improved long-term infrastructure planning and competitive positioning

Frequently Asked Questions About This Report

The global data center chip market size was estimated at USD 21.21 billion in 2024 and is expected to reach USD 23.71 billion in 2025.

The global data center chip market is expected to grow at a compound annual growth rate of 12.5% from 2025 to 2030, reaching USD 42.74 billion by 2030.

The data center chip market in North America held a significant share of nearly 41.0% in 2024 by the region’s dominance in cloud computing, artificial intelligence (AI), and big data analytics. With major companies such as Amazon, Google, and Microsoft leading the digital transformation, there is a growing demand for advanced data center chips capable of handling large-scale computing workloads.

Some key players operating in the data center chip market include Advanced Micro Devices, Inc., Alibaba, Arm Holdings, Broadcom Inc., Google, Huawei Technologies Co., Ltd., IBM Corporation, Intel Corporation, Marvell, Micron Technology, Inc., NVIDIA Corporation, Qualcomm, SAMSUNG, STMicroelectronics, Texas Instruments Incorporated

As demand for high-performance computing (HPC) and data-intensive applications surges, data centers require more advanced chip technologies to handle massive volumes of data. The increasing adoption of cloud computing, big data analytics, and artificial intelligence (AI) has fueled the need for efficient, high-capacity data center chips.

About the Author(s)

IT Services & Applications Research Team

Technology · IT Services & ApplicationsThis report was authored by the it services & applications research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the it services & applications segment of the technology industry. All findings are based on proprietary technology databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.