- Home

- »

- IT Services & Applications

- »

-

Embedded Software Market Size & Share Report, 2026-2033GVR Report cover

![Embedded Software Market (2026 - 2033)Report]()

Embedded Software Market (2026 - 2033)

Size, Share & Trends Analysis Report By Operating System (General Purpose Operating System, Real-time Operating System), By Vertical (Automotive, Manufacturing), By Functionality, By Region, And Segment Forecasts

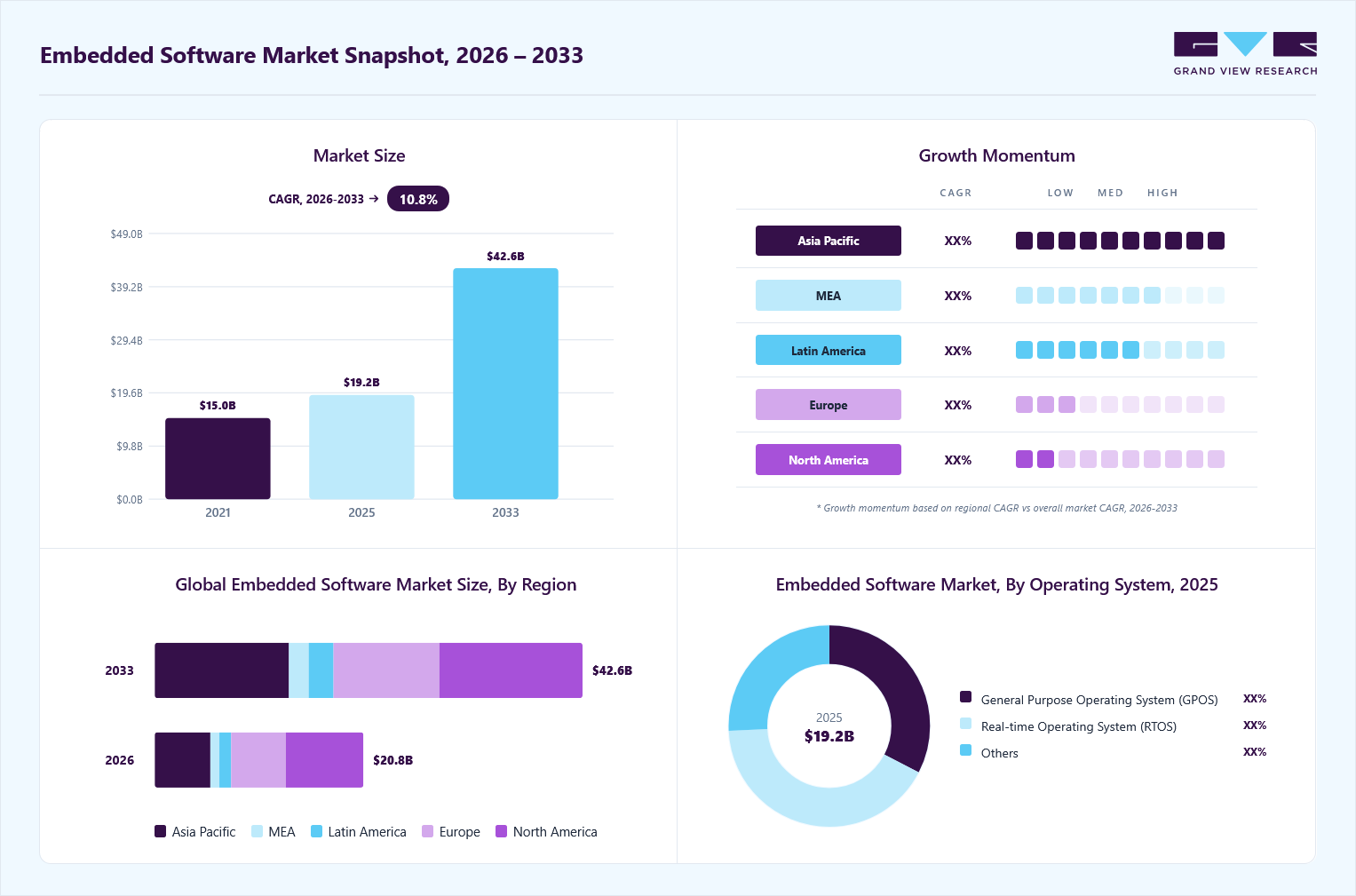

Market Size, 2025

$19.2BMarket Estimate, 2026

$20.8BMarket Forecast, 2033

$42.6BCAGR, 2026–2033

10.8%Embedded Software Market Summary

The global embedded software market size was valued at USD 19.2 billion in 2025 and is projected to grow from USD 20.8 billion in 2026 to USD 42.6 billion by 2033, at a CAGR of 10.8% from 2026 to 2033. North America dominated the embedded software market with the largest revenue share of 37.7% in 2025. The market is driven by the accelerating adoption of connected devices, increasing integration of software-defined functionalities across automotive and industrial systems, rising deployment of IoT-enabled applications, and growing demand for real-time processing, automation, and edge computing solutions across multiple industries.

Key Market Trends & Insights

- By operating system: Real-time Operating System (RTOS) segment dominated the market, with a revenue share of 41.6% in 2025.

- By functionality: Real-time embedded systems segment held the largest market share of 37.1% in 2025.

- By vertical: Consumer Electronics segment held the largest revenue share in 2025.

Regional Highlights

- Largest regional market: North America (37.7% revenue share, 2025)

- Fastest growing regional market: Asia Pacific (highest CAGR, 2026-2033)

- By country: The U.S. held the largest market share in 2025.

Market Size & Forecast

- Market size in 2025: USD 19.2 Billion

- Estimated market size in 2026: USD 20.8 Billion

- Projected market size by 2033: USD 42.6 Billion

- CAGR (2026-2033): 10.8%

In addition, industries like automotive and telecommunications require advanced embedded software to power autonomous vehicles, Advanced Driver Assistance Systems (ADAS), and 5G-enabled devices. The widespread adoption of smart city initiatives, including traffic management and energy systems, further underscores the importance of embedded software in managing complex urban infrastructure efficiently.The increasing digitization across industries and advancements in AI and machine learning enhance the capabilities of embedded systems, making them more intelligent and efficient. The growing adoption of Electric Vehicles (EVs) also contributes to this growth, as embedded software is essential for battery management systems, motor control, and vehicle-to-grid communication. Furthermore, the adoption of 5G technology is expected to accelerate demand for embedded software in connected devices, enabling real-time data processing and seamless communication.

")

The embedded software industry is positioned for sustained growth due to its critical role in enabling innovation across multiple sectors. Industries such as healthcare are leveraging embedded software for medical devices that require precision and reliability, while consumer electronics manufacturers rely on it to enhance device functionality and user experience. For instance, GlobalLogic develops industry-specific embedded software and hardware solutions that seamlessly integrate IT with industrial systems. As industries continue to embrace automation and connectivity, the demand for robust and scalable embedded software solutions is expected to grow significantly, supporting technological advancements globally.

Market Dynamics

The embedded software landscape is driven by increasing adoption of IoT devices, industrial automation, connected vehicles, and smart electronics requiring real-time processing and control. Demand for edge computing and AI-enabled embedded systems is expanding the scope of advanced software capabilities. High development costs, complex hardware-software integration, and strict certification requirements in safety-critical applications are limiting faster deployment. Rising cybersecurity risks in connected environments are increasing the need for secure architectures and continuous updates. In addition, the shortage of skilled embedded software engineers and growing system complexity are adding pressure on development cycles and cost structures.

Increasing deployment of connected and autonomous systems is driving demand for embedded software that can support continuous data exchange between sensors, devices, and control units. These systems depend on real-time processing to analyze incoming data streams and execute actions within strict timing requirements. As system interdependence increases, embedded software must manage multiple inputs simultaneously while maintaining consistent performance across different operating conditions. This requirement is particularly important in environments where delays or errors can affect system reliability and operational outcomes.

This development is increasing the requirement for scalable and reliable embedded solutions that can function across distributed and complex architectures. Embedded software must ensure stable performance, fault tolerance, and seamless coordination between hardware components and communication layers. Growing system complexity also requires software that can be updated and maintained efficiently without disrupting ongoing operations. As adoption expands across industries, emphasis is placed on maintaining long-term operational consistency and integration across diverse platforms.

High development costs in embedded software arise due to the extensive effort required for system design, coding, testing, and validation in environments where reliability is critical. Safety-critical applications such as automotive control units, medical devices, industrial automation systems, and aerospace platforms require extremely high levels of accuracy and stability. These systems must be tested across multiple operating conditions, failure scenarios, and edge cases to ensure consistent performance without malfunction. As a result, development requires advanced simulation tools, hardware-in-the-loop testing setups, and specialized verification frameworks.

In addition, strict certification and regulatory compliance requirements significantly increase the cost burden. Developers must adhere to multiple industry standards and complete detailed documentation, audit processes, and repeated validation cycles before deployment approval. This process often involves iterative redesigns and extended testing phases, which further increase timelines and resource requirements. The need for highly skilled embedded engineers and continuous debugging of hardware-software interactions also adds to operational expenses, making overall development significantly more costly compared to conventional software systems.

The embedded software landscape is driven by increasing adoption of IoT devices, industrial automation, connected vehicles, and smart electronics requiring real-time processing and control. Demand for edge computing and AI-enabled embedded systems is expanding the scope of advanced software capabilities. High development costs, complex hardware-software integration, and strict certification requirements in safety-critical applications are limiting faster deployment. Rising cybersecurity risks in connected environments are increasing the need for secure architectures and continuous updates. In addition, the shortage of skilled embedded software engineers and growing system complexity are adding pressure on development cycles and cost structures

This development also enables devices to perform tasks such as pattern recognition, predictive maintenance, and adaptive control without constant human intervention. As a result, embedded systems become more efficient and capable of operating in complex environments with minimal external input. The integration of AI into embedded platforms is increasing demand for more powerful processors, optimized software frameworks, and energy-efficient designs.

Market Concentration & Characteristics

The embedded software market shows a moderate level of concentration because a few large technology and semiconductor companies hold strong positions in core areas such as real-time operating systems, automotive software platforms, and industrial embedded solutions. These established players benefit from long-term contracts, strong R&D capabilities, and deep integration with hardware ecosystems, which makes it difficult for new entrants to compete at the same scale.

At the same time, the market is not fully concentrated because many specialized and niche vendors operate across different application areas such as IoT devices, consumer electronics, healthcare systems, and industrial automation. This creates a distributed competitive structure where leadership varies by use case rather than a single dominant player controlling the entire market. As a result, the market remains balanced between consolidation in key segments and fragmentation across specialized applications.

Analyst Perspective

The embedded software market is experiencing strong momentum driven by the rapid proliferation of connected devices, software-defined systems, and intelligent edge computing applications across industries. Increasing adoption of advanced driver assistance systems (ADAS), industrial automation platforms, and IoT-enabled infrastructure is accelerating demand for scalable and secure embedded software solutions. Market participants are investing heavily in real-time operating systems, embedded cybersecurity, and AI-enabled software architectures to address growing requirements for performance, reliability, and connectivity. The transition toward software-defined vehicles, smart manufacturing environments, and next-generation communication networks is creating significant opportunities for innovation and long-term revenue expansion. Strategic collaborations between semiconductor manufacturers, software developers, and OEMs are further strengthening ecosystem development and accelerating technology deployment. As organizations prioritize digital transformation and intelligent automation, the embedded software market is expected to witness sustained growth supported by continuous advancements in edge intelligence, connectivity, and system integration technologies.

Operating System Insights

Based on operating system, the Real-time Operating System (RTOS) segment led the market with the largest revenue share of 41.6% in 2025. RTOS is essential for applications requiring precise timing and reliability, such as aerospace, automotive control systems, and industrial automation. The need for systems to perform real-time processing and handle critical tasks drives RTOS adoption.The growth of IoT and connected devices requires efficient and responsive systems to handle real-time data processing and communication. RTOS is crucial for managing the real-time requirements of these devices.

The General Purpose Operating System (GPOS) segment is anticipated to exhibit a significant CAGR over the forecast period. GPOS is used in various applications, such as consumer electronics, computing devices, and general-purpose embedded systems. This broad applicability drives its widespread adoption.GPOS provides a rich set of APIs and development tools that simplify software development and support a wide range of applications, making it a preferred choice for developers in the embedded software industry. The need for advanced multimedia capabilities and connectivity in devices such as smartphones, tablets, and smart TVs drives demand for GPOS, which can efficiently handle these requirements.

Functionality Insights

Based on functionality, the real-time embedded systems segment led the market with the largest revenue share of 37.1% in 2025. The increasing need for automation and precise control in various industries, such as manufacturing, automotive, and aerospace, drives the demand for real-time embedded systems to manage complex processes and operations. For instance, Tesla’s Autopilot utilizes embedded systems, including radar, cameras, ultrasonic sensors, and AI-driven algorithms, to enable semiautonomous driving capabilities. Moreover, the rise of Industrial Internet of Things (IIoT) technologies, which require real-time data processing and analytics, propels the growth of real-time embedded systems for effective monitoring and control in industrial environments.Real-time embedded systems are essential for applications requiring high reliability and safety, such as medical devices, automotive safety systems, and aerospace systems, where timely and accurate responses are critical.

The mobile embedded systems segment is anticipated to exhibit a significant CAGR over the forecast period. The increasing adoption of smartphones, tablets, and wearable devices drives demand for mobile embedded systems. These systems are essential for managing various functions and user experiences in mobile devices. Continuous advancements in mobile technology, including higher processing power, improved battery life, and enhanced connectivity, drive the need for advanced embedded systems to support these features. Users expect advanced functionality, better performance, and richer multimedia experiences from mobile devices. Mobile embedded systems are crucial for providing enhanced user experience.

Vertical Insights

Based on vertical, the consumer electronics segment led the market with the largest revenue share of 23.1% in 2025. The growing use of smart devices, such as smartphones, tablets, smart TVs, and home appliances, drives demand for embedded software to support their functionality and user interfaces. Ongoing technological advancements, including faster processors, higher resolution displays, and improved connectivity, require advanced embedded software to leverage these capabilities. The integration of voice assistants and AI in consumer electronics requires advanced embedded software to handle natural language processing, voice recognition, and intelligent features.

The automotive segment is expected to experience significant growth due to the increasing demand for advanced embedded software supporting Vehicle-to-Infrastructure (V2I) and Vehicle-to-Vehicle (V2V) communications and the rise of electric and autonomous vehicles. These technologies require specialized software for energy management, autonomous driving algorithms, and Vehicle-to-Everything (V2X) connectivity. In addition, the growing complexity of systems like Advanced Driver-Assistance Systems (ADAS), infotainment, and connected vehicles further drives the need for sophisticated embedded solutions. For instance, in February 2025, Intron Technology partnered with eSOL to advance next-generation Software-Defined Vehicles (SDVs) in China, reflecting the industry's focus on innovation to meet evolving demands.

Regional Insights

North America dominated the embedded software market with the largest revenue share of 37.7% in 2025. Rapid innovations in various fields, such as IoT, AI, and machine learning, create new opportunities and applications for embedded software. Supportive government policies and funding for technological research and development drive the growth of the embedded software industry in the region.

U.S. Embedded Software Market Trends

The embedded software market in the U.S. held the largest share in the North America region in 2025. Increasing awareness and the growing implementation of cybersecurity measures for embedded systems drive the development of more secure software solutions. Moreover, the growing market for smart home devices, wearables, and entertainment systems demands advanced embedded software to deliver enhanced features and user experiences.

Europe Embedded Software Market Trends

Europe embedded software market is expected to witness significant growth over the forecast period. The European Union's strict regulations related to safety, environmental impact, and data protection necessitate the development of highly reliable and compliant embedded software, especially in industries such as automotive, healthcare, and industrial automation. In addition, the growing adoption of Industry 4.0, which focuses on smart factories, automation, and data exchange in manufacturing technologies, is a significant driving force for the embedded software industry in Europe.

Asia Pacific Embedded Software Market Trends

Asia Pacific embedded software market is anticipated to grow at a CAGR of 12.2% during the forecast period. The region's rapid industrialization and increase in adoption of advanced technologies across the automotive, healthcare, and consumer electronics industries are key drivers. In addition, the integration of 5G technology in embedded systems is transforming industries like telecommunications and manufacturing, enabling real-time applications and large-scale IoT deployments. Countries such as China, India, and South Korea are experiencing a surge in smart device adoption due to improved economic conditions and digitization efforts, further fueling the demand for embedded software.

China embedded software market dominated the regional market in 2024. The country is the largest global producer of mobile phones and consumer electronics, which heavily rely on embedded software for their functionality. Moreover, China's focus on smart city projects and IoT-based solutions has created a significant market for embedded software in urban development initiatives. Leading companies in China are also investing heavily in embedded system development to cater to both domestic and international markets, further solidifying their dominance in this sector.

Key Embedded Software Company Insights

Some key companies in the embedded software industry include Intel Corporation, Microsoft, and Wind River Systems, Inc. Companies active in the embedded software industry focus aggressively on expanding their customer base and gaining a competitive edge over their rivals. Hence, they pursue various strategic initiatives, including partnerships, mergers & acquisitions, collaborations, and new product/technology development. For instance, in January 2024, BlackBerry Limited launched QNX Everywhere, a new initiative to meet the increasing worldwide need for skilled developers in embedded systems. It includes various features such as autonomous access to QNX software, on-demand training, open-source projects optimized for QNX, and straightforward entry to development tools supported by the cloud. Furthermore, to facilitate developers in designing and experimenting with their software on embedded devices, QNX Everywhere offers support for widely accessible, economical CPU boards.

Key Embedded Software Companies:

The following are the leading companies in the embedded software market. These companies collectively hold the largest market share and dictate industry trends.

- Green Hills Software

- Intel Corporation

- Microchip Technology Inc.

- Microsoft

- NXP Semiconductors

- Renesas Electronics Corporation

- Siemens

- STMicroelectronics

- Texas Instruments Incorporated

- Wind River Systems, Inc.

Competitive Benchmarking

CLIENT REQUEST

CUSTOMIZATION DELIVERED

VALUE ADDS

Embedded Software Technology Adoption & Growth Assessment

- Performed a comprehensive analysis of embedded software market trends, including real-time operating systems (RTOS), software-defined architectures, edge computing, AI-enabled embedded systems, embedded cybersecurity, IoT connectivity, and next-generation automotive software platforms across major industry verticals.

- This assessment enables stakeholders to identify high-growth technology segments, evaluate evolving software adoption patterns, prioritize R&D investments, and strengthen competitive positioning within the rapidly advancing embedded software ecosystem.

Industry-Specific Embedded Software Deployment Analysis

- Assessed demand for embedded software solutions across automotive, industrial automation, consumer electronics, telecommunications, manufacturing, healthcare, and computing device sectors, including intelligent device management, automation control systems, connectivity solutions, and software-defined product innovations.

- Provides strategic insights into industry-specific digitalization initiatives, software integration requirements, and long-term revenue opportunities, supporting market expansion planning and targeted growth strategies.

AI, Edge Computing & Connected Device Opportunity Assessment

- Evaluated adoption trends for AI-powered edge intelligence, software-defined vehicles, industrial IoT platforms, embedded security frameworks, cloud-connected devices, and advanced real-time processing technologies across global markets.

- Supports investment and innovation strategies by identifying emerging technology opportunities, accelerating product development roadmaps, and enabling data-driven decision-making in high-growth segments of the embedded software market.

Recent Developments

-

In May 2024, Wind River Systems, Inc. collaborated with Elektrobit, an automotive software provider, to exhibit core software for autonomous, electric, software-centric vehicles. Wind River Systems, Inc. contributed VxWorks as the real-time operating system, whereas Elektrobit offered its second-generation EB corbos AdaptiveCore software and EB corbos Studio tools and developed a software framework based on the AUTOSAR Adaptive Platform.

-

In April 2024, Microsoft signed an 8-year partnership agreement with Cloud Software Group Inc. The agreement would enhance the collaborative efforts in marketing for the virtual application and desktop platform offered by Citrix, as well as bolster the creation of innovative cloud and AI solutions through a unified product strategy. Moreover, Cloud Software Group Inc. invested USD 1.65 billion to support the Microsoft cloud and its advanced generative AI features.

-

In February 2024, Intel Corporation announced the launch of Altera, its new standalone Field-Programmable Gate Array (FPGA) company. Altera's offerings are optimized to target a wide spectrum of markets and applications, from networking and communications infrastructure to energy-efficient embedded systems.

Embedded Software Market Report Scope

Report Attribute

Details

Market size in 2025

USD 19.2 billion

Estimated market size in 2026

USD 20.8 billion

Projected market size by 2033

USD 42.6 billion

Growth rate

CAGR of 10.8% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Operating system, functionality, vertical, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; Germany; UK; France; China; Japan; India; South Korea; Australia; Brazil; Saudi Arabia; South Africa; UAE

Key companies profiled

Green Hills Software; Intel Corporation; Microchip Technology Inc.; Microsoft; NXP Semiconductors; Renesas Electronics Corporation; Siemens; STMicroelectronics; Texas Instruments Incorporated; and Wind River Systems, Inc.

Customization scope

Free report customization (equivalent up to 8 analysts' working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Embedded Software Market Report Segmentation

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global embedded software market report based on operating system, functionality, vertical, and region:

-

Operating System Outlook (Revenue, USD Million, 2021 - 2033)

-

General Purpose Operating System (GPOS)

-

Real-time Operating System (RTOS)

-

Others

-

-

Functionality Outlook (Revenue, USD Million, 2021 - 2033)

-

Standalone Systems

-

Real-Time Embedded Systems

-

Mobile Embedded Systems

-

Networked Embedded Systems

-

-

Vertical Outlook (Revenue, USD Million, 2021 - 2033)

-

Computing Devices

-

Consumer Electronics

-

Industrial Automation

-

Automotive

-

Manufacturing

-

Telecommunications

-

Others

-

-

Regional Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

UK

-

Germany

-

France

-

-

Asia Pacific

-

China

-

India

-

Japan

-

Australia

-

South Korea

-

-

Latin America

-

Brazil

-

-

MEA

-

UAE

-

South Africa

-

KSA

-

-

Research Methodology

Segment Definition

Segment - Operating System

Revenue capture definition

General Purpose Operating System (GPOS)

The General Purpose Operating System (GPOS) segment covers embedded software platforms capable of supporting multiple applications, user interactions, and complex processing tasks within connected devices. These operating systems are widely implemented in products that require flexibility, scalability, and broad software compatibility.

Real-time Operating System (RTOS)

This segment represents software environments engineered to deliver deterministic performance and execute operations within strict timing requirements. RTOS platforms are primarily utilized in systems where response predictability and operational reliability are fundamental.

Others

The Others segment includes revenue generated from proprietary, customized, and lightweight operating environments that do not fall under conventional GPOS or RTOS categories. These solutions are typically tailored to meet specific application, performance, or resource requirements.

Segment - Functionality

Revenue capture definition

Standalone Systems

The Standalone Systems segment refers to embedded software integrated into devices that perform dedicated functions without dependence on continuous network connectivity. These systems are designed to operate autonomously while managing localized processing and control activities.

Real-Time Embedded Systems

This segment includes software architectures developed to process information and respond to events within predefined time limits. Their functionality is centered on ensuring timely execution of critical operations across performance-sensitive applications.

Mobile Embedded Systems

The Mobile Embedded Systems segment comprises software embedded in portable electronic devices that require efficient resource utilization and mobility support. These solutions are optimized to enable seamless operation within compact and battery-powered platforms.

Networked Embedded Systems

This segment focuses on software that facilitates communication and data exchange among connected devices through wired or wireless networks. Its scope includes applications that support interoperability, remote access, and connected ecosystem functionality.

Segment - Vertical

Revenue capture definition

Computing Devices

The Computing Devices segment pertains to embedded software deployed within computers, servers, storage equipment, and related hardware systems. The software enables device operation, system coordination, and interaction between hardware and application layers.

Consumer Electronics

This segment consists of embedded software incorporated into consumer-focused products such as smart TVs, gaming consoles, wearables, and household appliances. Its primary role is to support product functionality, connectivity features, and user experiences.

Industrial Automation

The Industrial Automation segment includes software solutions embedded in industrial control equipment, robotics, sensors, and automated machinery. These applications facilitate process execution, equipment coordination, and operational management within industrial environments.

Automotive

This segment covers software embedded within vehicle platforms to manage functions ranging from engine control and infotainment to connectivity and advanced driver assistance systems. It serves as a foundational technology layer supporting modern automotive electronics.

Manufacturing

The Manufacturing segment comprises embedded software utilized across production assets, factory systems, and manufacturing equipment. These solutions contribute to machine control, workflow monitoring, and production process optimization.

Telecommunications

This segment refers to software embedded in networking hardware, communication infrastructure, and telecom devices. Its functionality supports data routing, network operations, signal processing, and communication service delivery.

Others

The Others segment includes embedded software applications deployed across industries such as healthcare, aerospace, defense, transportation, and energy. These solutions are designed to address sector-specific operational requirements and specialized use cases.

Estimation Model

Layer Name

Key Questions

Description

Connected Device & System-Intensive Industry Layer

Who operates embedded system–intensive environments?

Identify industries relying on embedded systems such as automotive electronics, industrial automation, consumer electronics, telecom infrastructure, healthcare devices, aerospace systems, and energy systems. This layer defines the total demand base for embedded software across connected and physical systems.

Software-Enabled Hardware Adoption Layer

Who integrates software-enabled and connected hardware systems?

Apply adoption levels of smart devices, IoT-enabled equipment, connected vehicles, industrial control systems, and smart appliances. This layer estimates the transition from traditional hardware to software-driven embedded architectures.

Advanced Embedded Intelligence Layer

Who deploys AI-enabled and real-time embedded software?

Apply penetration rates for real-time operating systems, edge AI, machine learning inference at the edge, computer vision modules, and secure embedded firmware. This layer captures deployment of advanced embedded intelligence and autonomous system capabilities.

Embedded Software Value Realization Layer

How much value is generated through embedded software deployment?

Estimate revenue by multiplying active deployments by average software spend per device/system, including licensing, RTOS fees, cloud connectivity, integration services, cybersecurity modules, and maintenance contracts. This layer captures total embedded software market revenue generation.

Delivered Customizations

CLIENT REQUEST

CUSTOMIZATION DELIVERED

VALUE ADDS

Embedded Software Technology Adoption & Growth Assessment

Performed a comprehensive analysis of embedded software market trends, including real-time operating systems (RTOS), software-defined architectures, edge computing, AI-enabled embedded systems, embedded cybersecurity, IoT connectivity, and next-generation automotive software platforms across major industry verticals.

This assessment enables stakeholders to identify high-growth technology segments, evaluate evolving software adoption patterns, prioritize R&D investments, and strengthen competitive positioning within the rapidly advancing embedded software ecosystem.

Industry-Specific Embedded Software Deployment Analysis

Assessed demand for embedded software solutions across automotive, industrial automation, consumer electronics, telecommunications, manufacturing, healthcare, and computing device sectors, including intelligent device management, automation control systems, connectivity solutions, and software-defined product innovations.

Provides strategic insights into industry-specific digitalization initiatives, software integration requirements, and long-term revenue opportunities, supporting market expansion planning and targeted growth strategies.

AI, Edge Computing & Connected Device Opportunity Assessment

Evaluated adoption trends for AI-powered edge intelligence, software-defined vehicles, industrial IoT platforms, embedded security frameworks, cloud-connected devices, and advanced real-time processing technologies across global markets.

Supports investment and innovation strategies by identifying emerging technology opportunities, accelerating product development roadmaps, and enabling data-driven decision-making in high-growth segments of the embedded software market.

Frequently Asked Questions About This Report

Some key players operating in the embedded software market include Green Hills Software, Intel Corporation, Microchip Technology Inc., Microsoft, NXP Semiconductors, Renesas Electronics Corporation, Siemens, STMicroelectronics, Texas Instruments Incorporated, and Wind River Systems, Inc.

The rapid expansion of IoT devices, such as smart home products and industrial sensors, drives demand for embedded software that can handle real-time processing, connectivity, and data management.

The global embedded software market size size was valued at USD 19.2 billion in 2025 and is estimated at USD 20.8 billion for 2026.

The global embedded software market is expected to grow at a CAGR of 10.8% from 2026 to 2033 to reach USD 42.6 billion by 2033.

North America dominated the embedded software market with a share of 37.7% in 2025.

Asia Pacific is the fastest-growing region over the forecast period.

Real-time operating system (RTOS) segment dominated the market, with a revenue share of 41.6% in 2025 while general purpose operating system (GPOS) segment is expected to be the fastest-growing market.

Real-time embedded systems segment led the market with the largest revenue share of 37.1% in 2025 while mobile embedded systems segment second fastest growing market.

Consumer electronics segment led the market with the largest revenue share of 23.1% in 2025. The growing use of smart devices, such as smartphones, tablets, smart TVs, and home appliances, drives demand for embedded software to support their functionality and user interfaces.

About the Author(s)

IT Services & Applications Research Team

Technology · IT Services & ApplicationsThis report was authored by the it services & applications research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the it services & applications segment of the technology industry. All findings are based on proprietary technology databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.