- Home

- »

- Plastics, Polymers & Resins

- »

-

Foldable And Collapsible Container Market Size Report, 2033GVR Report cover

![Foldable And Collapsible Container Market (2026 - 2033)Report]()

Foldable And Collapsible Container Market (2026 - 2033)

Size, Share & Trends Analysis Report By Material (Plastic, Metal, Wood), By Product Type (Bulk Bins, Pallets, Crates), By End Use (Industrial & Automotive, Food & Beverage), By Region, And Segment Forecasts

Market Size, 2025

$1.7BMarket Estimate, 2026

$1.8BMarket Forecast, 2033

$2.3BCAGR, 2026–2033

4.0%Foldable And Collapsible Container Market Summary

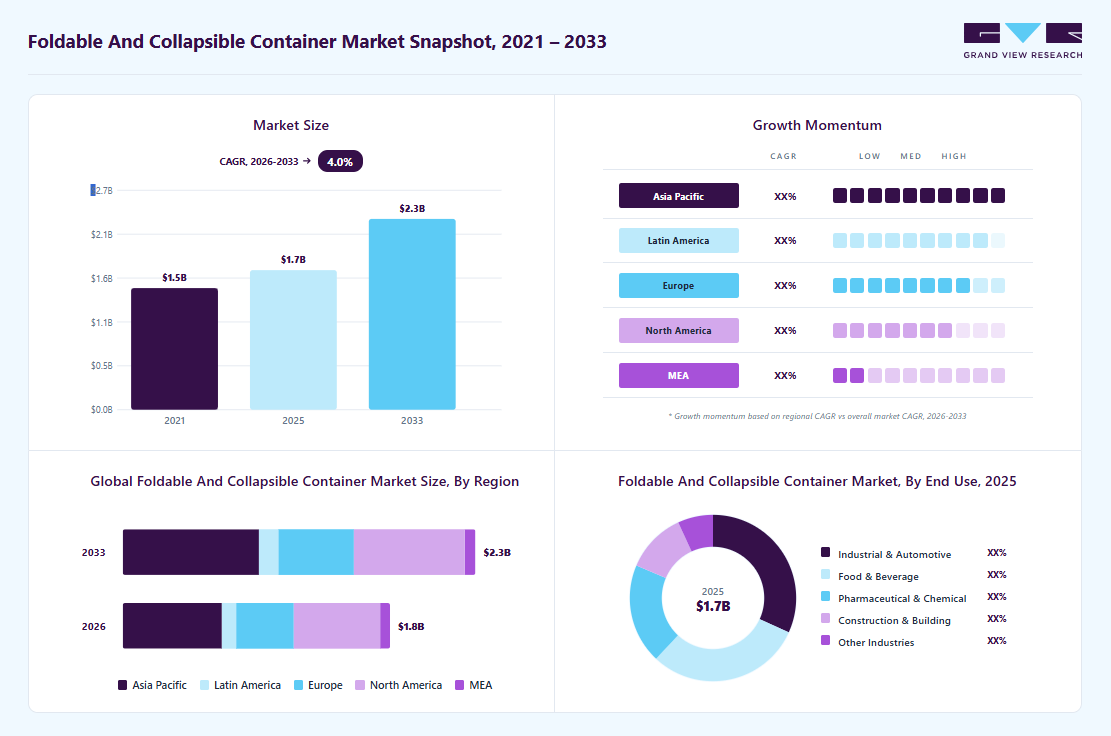

The global foldable and collapsible container market size was valued at USD 1.7 billion in 2025 and is projected to grow from USD 1.8 billion in 2026 to USD 2.3 billion by 2033, at a CAGR of 4.0% from 2026 to 2033. The market in Asia Pacific dominated with a revenue share of 36.8% in 2025. The foldable and collapsible container industry is driven by rising demand for space-saving and cost-efficient storage and transportation solutions.

Key Market Trends & Insights

- By material: Plastic segment held the largest market share of 53.9% in 2025.

- By product type: Bulk bins segment held the largest market share of 25.8% in 2025.

- By end use: Industrial & automotive segment held the largest market share of 31.8% in 2025.

Regional Highlights

- Largest regional market: Asia Pacific (36.8% revenue share, 2025)

- By country: China held the largest market share in 2025

Market Size & Forecast

- Market size in 2025: USD 1.7 Billion

- Estimated market size in 2026: USD 1.8 Billion

- Projected market size by 2033: USD 2.3 Billion

- CAGR (2026-2033): 4.0%

In addition, the growing focus on sustainability and reusable packaging in logistics and warehousing is fueling market growth. The foldable and collapsible container industry is primarily driven by the rising demand for efficient space utilization in warehousing and logistics. As e-commerce, manufacturing, and retail industries expand, the pressure on warehousing facilities to optimize space and reduce idle storage grows. Foldable containers address this need by allowing businesses to store more goods in the same footprint when in use and significantly reduce volume during return logistics or storage when not in use. For example, IKEA and Amazon have adopted collapsible container systems to streamline reverse logistics, cutting costs and improving operational efficiency.")

The growing emphasis on sustainability and circular economy principles is also contributing to market growth. Collapsible containers are typically reusable and made from recyclable or long-lasting materials such as HDPE or metal alloys, reducing the need for single-use packaging. With increasing regulatory pressure and consumer awareness of environmental footprints, industries are shifting from disposable packaging to more durable, environmentally friendly alternatives. For instance, automotive and electronics manufacturers are transitioning to foldable packaging to reduce plastic waste and align with ESG (Environmental, Social, and Governance) targets.

The market is also benefiting from technological advancements in material science and product design. Innovations have enabled the creation of lightweight yet strong containers with features such as quick-lock systems, integrated RFID tracking, and ergonomic designs for safer handling. This enhances the usability of collapsible containers across sectors like pharmaceuticals, agriculture, and chemicals.

Moreover, cost reduction in transportation and labor is accelerating market adoption. Foldable containers drastically reduce return-trip costs by reducing the volume of empty containers, resulting in lower fuel use and fewer trips. This is especially relevant in long-haul transportation and global trade. In addition, these containers often feature modular, standardized designs compatible with automated handling systems, reducing labor costs and damage during material handling. For instance, logistics companies in Europe and Asia are replacing wooden pallets and rigid boxes with collapsible plastic containers to increase fleet efficiency and reduce the total cost of ownership.

Market Characteristics & Concentration

The foldable and collapsible container industry is heavily influenced by developments in the logistics, automotive, retail, and manufacturing sectors. As these sectors adopt more sophisticated and environmentally conscious logistics solutions, demand for foldable containers rises. For example, growth in cross-border e-commerce has led to increased demand for returnable, space-saving packaging options to lower transport costs and improve handling efficiency.

Material innovation and product customization are critical to capturing market share. Companies that offer custom-fit, durable, lightweight, and ergonomic solutions tend to have a competitive edge. Moreover, the integration of IoT and smart tracking systems is reshaping the industry, adding digital value to a traditionally physical product.

Material Insights

The plastic segment led the market with the largest revenue share of 53.88% in 2025. Plastic foldable and collapsible containers are the most widely used type due to their lightweight nature, corrosion resistance, and high strength-to-weight ratio. These containers are typically made from high-density polyethylene (HDPE) or polypropylene (PP), making them durable for repeated use in supply chains across end-use industries. Their ability to withstand chemicals and moisture makes them ideal for both indoor and outdoor logistics applications. Moreover, the ongoing transition to circular-economy practices is prompting manufacturers to use recycled plastics, boosting sustainability and demand.

Metal foldable and collapsible containers are known for their heavy-duty strength, load-bearing capacity, and resistance to extreme temperatures. They are commonly used in industrial and manufacturing applications, especially for transporting heavy machinery parts, bulk materials, and automotive components. Steel and aluminum are the primary metals used, offering excellent longevity and structural integrity. The demand for metal containers is primarily driven by industries that require robust material-handling solutions, such as automotive, aerospace, and defense.

The other materials segment is expected to grow at the fastest CAGR of 4.5% during the forecast period. This category includes containers made from fabric, composite materials, or paperboard. Fabric containers are widely used in the textile industry and for light-duty applications, while paperboard-based foldable boxes serve retail and e-commerce sectors. These materials offer lightweight and highly customizable solutions for specific niche requirements. The rise of e-commerce, fashion, and last-mile delivery services is driving demand for foldable, eco-conscious alternative container materials.

Product Type Insights

The bulk bins segment led the market with the largest revenue share of 25.82% in 2025. Bulk bins are large-capacity containers designed for transporting and storing bulk materials such as agricultural produce, industrial components, and chemicals. The demand for bulk bins is driven by increasing logistics efficiency requirements across sectors such as agriculture and food processing. In addition, the rise in cross-border agri-trade and the need for hygienic and durable storage solutions are further boosting the use of collapsible bulk bins.

The crates segment is expected to grow at the fastest CAGR of 4.4% during the forecast period. Collapsible crates are used across a wide range of industries, including retail, agriculture, automotive, and pharmaceuticals. These containers are designed to provide strength and stackability when in use and compactness when folded. They are often ventilated and made of durable plastic materials. The growing demand for efficient returnable packaging in grocery retail, especially in fresh produce and dairy segments, is a major driver. Seasonal storage needs and improved supply chain agility further enhance the appeal of collapsible crates.

End Use Insights

The industrial & automotive segment led the market with the largest revenue share of 31.78% in 2025. The industrial and automotive sectors are dominant end-use segments for foldable and collapsible containers, as these containers are widely used to transport heavy-duty components, machinery parts, and automotive assemblies. Their stackability, reusability, and folding when not in use provide considerable space and cost savings, especially in return logistics. OEMs and Tier 1 suppliers across the automotive value chain increasingly use these containers for streamlined warehousing and line-side inventory handling.

The pharmaceutical & chemical segment is projected to grow at the fastest CAGR of 4.4% during the forecast period. The pharmaceutical and chemical industries rely on foldable and collapsible containers for the secure, contamination-free transportation of raw materials, intermediate products, and packaged drugs or chemicals. These containers are often designed to be tamper-evident and chemically resistant, and are crucial for maintaining product integrity and regulatory compliance throughout the supply chain. Rising global pharmaceutical production, especially in India, China, and the U.S., and growing international trade in chemicals and active pharmaceutical ingredients (APIs) are key growth factors.

Regional Insights

Asia Pacific dominated the global foldable and collapsible container market with the largest revenue share of 36.81% in 2025 and is expected to grow at the fastest CAGR of 4.7% over the forecast period. The growth is due to rapid industrialization, booming e-commerce, and expanding manufacturing sectors. Countries such as China, India, and Japan are leading the demand, with logistics companies adopting these containers to optimize storage and transportation costs. For example, China’s massive export industry relies on collapsible containers to reduce empty return shipments, while India’s growing e-commerce sector uses them for efficient last-mile deliveries. In addition, government initiatives promoting sustainable logistics, such as green freight programs, further accelerate adoption. The region’s focus on cost efficiency and space-saving solutions in congested urban hubs such as Singapore and Hong Kong also fuels market growth.

North America Foldable and Collapsible Container Market Trends

The foldable and collapsible container market in North America is driven by advanced supply chain networks, high retail and e-commerce penetration, and stringent sustainability regulations. The U.S. and Canada are key adopters, with major retailers such as Amazon and Walmart using collapsible containers to streamline warehouse operations and reduce carbon footprints. The region’s emphasis on reusable packaging in industries such as automotive (e.g., Ford and GM using foldable containers for parts logistics) also boosts demand. Furthermore, the rise of omnichannel retailing and the need for efficient reverse logistics contribute to market expansion. Innovations in container materials, such as lightweight, high-strength plastics, are further enhancing adoption in North America.

Europe Foldable and Collapsible Container Market Trends

The foldable and collapsible container market in Europe is anticipated to grow at a significant CAGR over the forecast period, driven by stringent environmental regulations, circular-economy policies, and a strong manufacturing base. The EU’s push for reusable packaging under the Single-Use Plastics Directive has accelerated demand, particularly in Germany, France, and the Netherlands. For instance, automotive giants such as Volkswagen and BMW use collapsible containers for just-in-time parts delivery, reducing waste and transportation costs. In addition, Europe’s well-developed intermodal transport systems (combining road, rail, and sea freight) favor the use of foldable containers for efficient logistics. The growth of urban logistics in cities like London and Paris, where space constraints are a challenge, further drives the adoption of collapsible solutions.

Key Foldable and Collapsible Container Company Insights

The competitive environment of the foldable and collapsible container industry is moderately fragmented, with the presence of several global and regional players competing on product innovation, material strength, cost-efficiency, and customization. Companies are increasingly investing in lightweight, recyclable materials and modular designs to gain a competitive edge, while strategic collaborations, expansions, and mergers & acquisitions are prevalent to expand market reach and production capacity. This competitive dynamic is driving rapid innovation and technological advancements in the sector.

Key Foldable And Collapsible Container Companies:

The following key companies have been profiled for this study on the foldable and collapsible container market.

- Schoeller Allibert

- WestRock Company

- A B Sea Container Private Limited

- Vinsum Axpress

- Spectainer

- SAHAY RACKS

- Flexible Packaging Solutions

- Logimarkt

- CHEP

- Flex Container

- RPP Containers

- Corplex

- Shandong Liansheng Prefabricated Construction Co., Ltd.

Recent Development

-

In November 2024, Compact Container Systems (CCS), based in Florida, launched the SeaFold HC 40′, the world’s first five-in-one foldable shipping container. This innovative design is engineered to address major inefficiencies in global logistics, particularly the costly and environmentally damaging movement of empty containers

-

In April 2024, RPP Containers, a major player in reusable bulk packaging solutions, announced the launch of their next-generation 45" x 48" x 50" Collapsible Hopper Bottom Containers. These new containers are the latest addition to the company’s renowned DuraGreen line of premium, sustainable bulk containers.

Foldable And Collapsible Container Market Report Scope

Report Attribute

Details

Market size in 2025

USD 1.7 billion

Market size value in 2026

USD 1.8 billion

Revenue forecast in 2033

USD 2.3 billion

Growth rate

CAGR of 4.0% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion, and CAGR from 2026 to 2033

Report coverage

Revenue forecast, competitive landscape, growth factors, and trends

Segments covered

Material, product type, end use, region

Regional scope

North America; Europe; Asia Pacific; Latin America; Middle East & Africa

Country scope

U.S.; Canada; Mexico; Germany; France; UK; Italy; Spain; China; India; Japan; Australia; South Korea; Brazil; Argentina; South Africa; Saudi Arabia; UAE

Key companies profiled

Schoeller Allibert; WestRock Company; A B Sea Container Private Limited; Vinsum Axpress; Spectainer; SAHAY RACKS; Flexible Packaging Solutions; Logimarkt; CHEP; Flex Container; RPP Containers; Corplex; Shandong Liansheng Prefabricated Construction Co., Ltd.

Customization scope

Free report customization (equivalent up to 8 analyst’s working days) with purchase. Addition or alteration to the country, regional, and segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Foldable and Collapsible Container Market Report Segmentation

This report forecasts revenue growth at a global level and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global foldable and collapsible container market report based on material, product type, end use, and region:

-

Material Outlook (Revenue, USD Million, 2021 - 2033)

-

Plastic

-

Metal

-

Wood

-

Others

-

-

Product Type Outlook (Revenue, USD Million, 2021 - 2033)

-

Bulk Bins

-

Pallets

-

Crates

-

Boxes

-

Cartons

-

Others

-

-

End Use Outlook (Revenue, USD Million, 2021 - 2033)

-

Industrial & Automotive

-

Food & Beverage

-

Pharmaceutical & Chemical

-

Construction & Building

-

Others

-

-

Region Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

France

-

UK

-

Italy

-

Spain

-

-

Asia Pacific

-

China

-

India

-

Japan

-

Australia

-

South Korea

-

-

Latin America

-

Brazil

-

Argentina

-

-

Middle East & Africa

-

South Africa

-

Saudi Arabia

-

UAE

-

-

Frequently Asked Questions About This Report

Plastic segment held the largest market share of 53.9% in 2025, while other materials is the fastest-growing segment.

Bulk bins segment held the largest market share of 25.8% in 2025, while crates is the fastest-growing segment.

Industrial & automotive segment led with a 31.8% revenue share in 2025, while pharmaceutical & chemicals is the fastest-growing segment.

The key players in the foldable and collapsible container market include Schoeller Allibert; WestRock Company; A B Sea Container Private Limited; Vinsum Axpress; Spectainer; SAHAY RACKS; Flexible Packaging Solutions; Logimarkt; CHEP; Flex Container; RPP Containers; Corplex; Shandong Liansheng Prefabricated Construction Co., Ltd.

Key factors include rising demand for space-saving and cost-efficient storage and transportation solutions.

The global foldable and collapsible container market was estimated at around USD 1.7 billion in the year 2025 and is expected to reach around USD 1.8 billion in 2026.

The global foldable and collapsible container market is expected to grow at a compound annual growth rate of 4.0% from 2026 to 2033 to reach around USD 2.3 billion by 2033.

Asia Pacific dominated with a 36.8% revenue share in 2025.

About the Author(s)

Plastics, Polymers & Resins Research Team

Bulk Chemicals · Plastics, Polymers & ResinsThis report was authored by the plastics, polymers & resins research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the plastics, polymers & resins segment of the bulk chemicals industry. All findings are based on proprietary bulk chemicals databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.