- Home

- »

- Plastics, Polymers & Resins

- »

-

LED Packaging Market Size And Growth Report, 2026-2033GVR Report cover

![LED Packaging Market (2026 - 2033)Report]()

LED Packaging Market (2026 - 2033)

Size, Share & Trends Analysis Report By Materials (Epoxy Resin, Silicone Resin, Ceramic Materials, Metal Lead Frames & Copper Materials, Plastic Materials), By Packaging Type, By Application, By Region, And Segment Forecasts

Market Size, 2025

$1.7BMarket Estimate, 2026

$1.8BMarket Forecast, 2033

$2.3BCAGR, 2026–2033

4.0%LED Packaging Market Summary

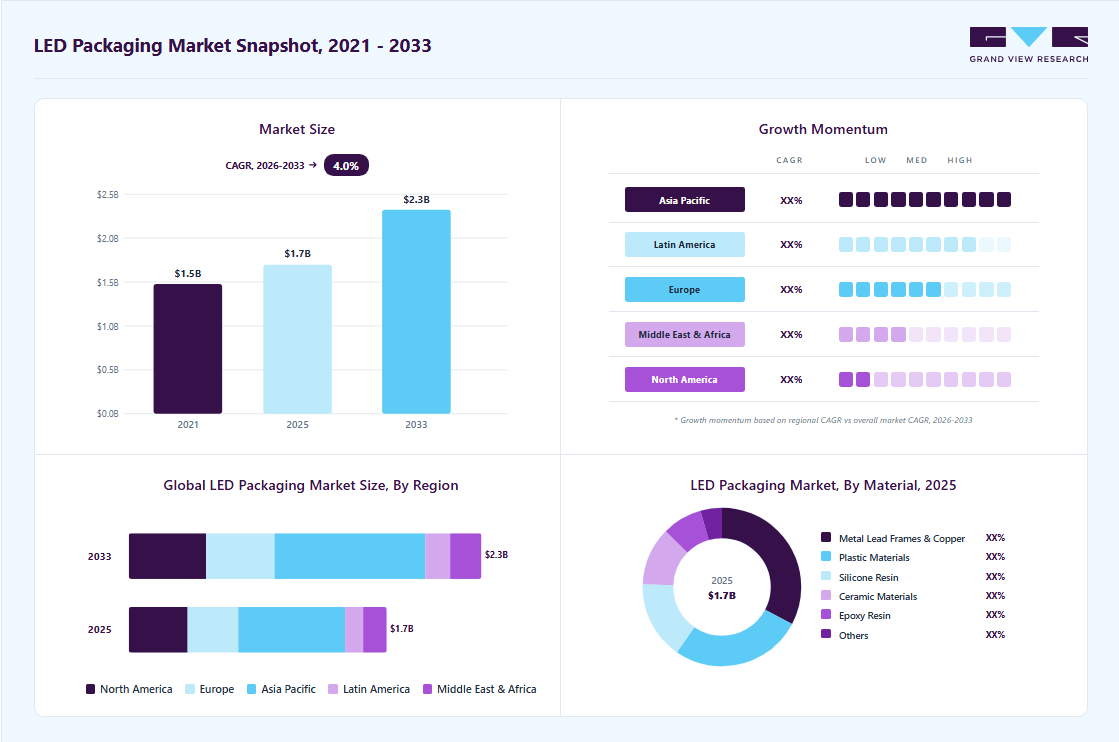

The global LED packaging market size was valued at USD 1.7 billion in 2025 and is projected to grow from USD 1.8 billion in 2026 to USD 2.3 billion by 2033, at a CAGR of 4.0% from 2026 to 2033. Asia Pacific dominated the market with the largest revenue share of 41.4% in 2025 and is expected to grow at the fastest CAGR of 4.5% from 2026 to 2033. The market is driven by rising demand for energy-efficient lighting, smart lighting systems, and automotive LED applications.

Key Market Trends & Insights

- By material: Metal lead frames & copper materials segment dominated the market in 2025, accounting for 32.7% of the total revenue share.

- By packaging type: Surface mount device (SMD) segment dominated the market in 2025, accounting for 40.7% of the total revenue share.

- By application: General lighting segment dominated the market in 2025, accounting for 33.0% of total demand.

Regional Highlights

- Largest regional market: Asia Pacific (41.4% revenue share, 2025)

- By country: The China held the largest market share in 2025.

Market Size & Forecast

- Market size in 2025: USD 1.7 Billion

- Estimated market size in 2026: USD 1.8 Billion

- Projected market size by 2033: USD 2.3 Billion

- CAGR (2026-2033): 4.0%

Market growth is further supported by expanding mini/micro-LED technologies, increasing electronics production, and strong manufacturing expansion across Asia-Pacific. The market is experiencing strong growth with the increasing global adoption of energy-efficient lighting systems across residential, commercial, industrial, and public infrastructure sectors. Government regulations promoting energy conservation and the gradual phase-out of conventional lighting technologies are accelerating LED deployment worldwide. LED Packaging technologies such as SMD, COB, and CSP improve brightness, thermal performance, and product lifespan, supporting wider adoption across lighting applications.")

The growing implementation of smart lighting systems and IoT-enabled infrastructure is further supporting market growth. Modern lighting solutions require compact, high-performance LED packages capable of supporting features such as dimming, color tuning, and wireless connectivity. Increasing investments in smart buildings, commercial automation, and connected urban infrastructure are creating strong demand for advanced and miniaturized LED packaging technologies.

The automotive industry is emerging as a key demand generator for LED packaging solutions. Automakers are increasingly integrating LEDs into headlights, taillights, interior lighting, and digital display systems to improve energy efficiency, vehicle aesthetics, and safety performance. Rising production of electric vehicles and premium automobiles is also increasing demand for compact, high-brightness, and thermally efficient LED package formats such as CSP and flip-chip LEDs.

The market is also benefiting from rising demand for consumer electronics and next-generation display technologies. Mini-LED and micro-LED displays used in televisions, smartphones, laptops, and gaming devices require highly precise and compact LED packaging solutions. In addition, expanding applications of UV LEDs in sterilization, medical equipment, and horticulture lighting are creating new growth opportunities, while strong manufacturing expansion across Asia-Pacific continues to strengthen industry production capacity and innovation.

Market Dynamics

The rising demand for energy-efficient lighting solutions is a major driver of the LED packaging market, as LEDs consume significantly less power and offer longer operational life compared to conventional incandescent and fluorescent lighting technologies. Increasing focus on reducing energy consumption and carbon emissions has encouraged governments, businesses, and consumers to adopt LED-based lighting systems across residential, commercial, industrial, and outdoor infrastructure applications. Advanced LED packaging technologies improve thermal management, luminous efficiency, and product reliability, making LEDs more effective and cost-efficient for large-scale lighting deployments.

Rapid urbanization, infrastructure modernization, and growing investments in smart city projects are further accelerating the adoption of energy-efficient LED lighting worldwide. Rising electricity costs and increasing environmental awareness are encouraging consumers and industries to replace traditional lighting systems with high-performance LED solutions in offices, retail spaces, factories, highways, and public buildings. In addition, supportive government regulations, energy-efficiency standards, and subsidy programs across major economies are strengthening demand for advanced LED packaging solutions capable of delivering higher brightness, durability, and energy savings.

Raw material price volatility is a significant restraint for the LED packaging market, as manufacturers heavily rely on semiconductor wafers, sapphire substrates, phosphors, rare earth materials, metals, and specialty resins for production. Fluctuations in the prices of these materials, driven by supply chain disruptions, geopolitical tensions, trade restrictions, and changing global demand, directly increase manufacturing costs and create pressure on profit margins. In addition, unstable raw material pricing makes it challenging for companies to maintain consistent product pricing and long-term supply agreements, particularly in highly competitive and price-sensitive markets. Small- and mid-sized manufacturers are particularly affected due to their limited bargaining power and lower financial flexibility, which can negatively impact production planning and overall operational efficiency.

Market Concentration & Characteristics

The LED packaging industry is characterized by continuous advancements in high-density and compact packaging architectures designed for automotive, industrial, and specialty lighting applications. Increasing integration of LEDs into advanced vehicle systems, including adaptive headlights and intelligent rear-lighting modules, is supporting demand for high-performance LED packages with superior thermal efficiency and reliability. Companies such as ams-OSRAM AG and Nichia Corporation are actively strengthening their automotive LED portfolios. In February 2025, ams-OSRAM announced series production of its OSRAM XLS LR6 LED light source for next-generation automotive rear-lighting applications, reflecting rising adoption of advanced LED packaging in the global automotive sector. Similarly, TOYODA GOSEI Co., Ltd. continues expanding high-brightness LED solutions for automotive and industrial applications to enhance performance and durability standards.

A key industry characteristic is the increasing focus on premium display technologies and high-efficiency visual applications across televisions, gaming displays, AR/VR devices, and commercial signage. Manufacturers are increasingly investing in Mini-LED and Micro-LED packaging technologies to improve brightness, contrast, and energy efficiency in advanced display systems. In August 2025, Lumileds Holding B.V. entered a major acquisition agreement with San’an Optoelectronics, aimed at strengthening technological capabilities and expanding global LED packaging operations. Meanwhile, Samsung Electronics and Seoul Semiconductor Co., Ltd. continued introducing advanced display-oriented LED technologies targeting premium consumer electronics and digital signage applications, reinforcing competitive innovation across the industry.

Material Insights

The metal lead frames & copper materials segment dominated the market in 2025, accounting for 32.7% of the total revenue share, primarily supported by the superior electrical conductivity, thermal dissipation capabilities, and cost efficiency of copper-based lead frame materials, making them highly suitable for high-volume LED manufacturing. These materials are widely utilized in automotive lighting, general illumination, and consumer electronics applications where effective heat management and long operational life are critical performance requirements. In addition, increasing adoption of high-power LEDs in automotive headlamps, industrial lighting systems, and outdoor displays continues to strengthen demand for advanced copper lead-frame packaging solutions among major LED manufacturers.

The ceramic materials segment is gaining traction in the market due to the rising demand for high-performance LED packages capable of operating under extreme thermal and environmental conditions. Ceramic materials provide excellent thermal conductivity, mechanical stability, corrosion resistance, and optical reliability, making them increasingly preferred for UV LEDs, Mini-LEDs, Micro-LEDs, automotive lighting, and specialty medical or industrial applications. Furthermore, ongoing advancements in high-brightness and compact LED designs are encouraging manufacturers to shift toward ceramic-based substrates and packaging structures to improve durability, miniaturization, and long-term efficiency in premium applications.

Packaging Type Insights

The surface mount device (SMD) segment dominated the market in 2025, accounting for 40.7% of the total revenue share, due to its compact size, high luminous efficiency, low power consumption, and suitability for automated assembly processes. SMD LEDs are extensively used across general lighting, automotive lighting, display backlighting, signage, and consumer electronics due to their superior brightness uniformity and design flexibility. In addition, increasing demand for slim and energy-efficient lighting systems in residential, commercial, and industrial sectors continues to strengthen adoption of SMD-based LED packages. Manufacturers are also focusing on improving thermal performance and miniaturization capabilities of SMD packaging to support high-density lighting and display applications.

The flip-chip & mini/micro LED segment is gaining momentum and is projected to expand at the fastest CAGR over the forecast period. Growth is being driven by increasing adoption of advanced display technologies in premium televisions, smartphones, wearable devices, automotive displays, and AR/VR applications. Flip-chip packaging offers advantages such as improved heat dissipation, higher current handling capacity, reduced package size, and enhanced optical efficiency, making it highly suitable for next-generation Mini-LED and Micro-LED products. Furthermore, rising investments by leading LED manufacturers in ultra-fine pixel pitch displays and high-brightness applications are accelerating commercialization of Mini-LED and Micro-LED packaging technologies across both consumer and industrial markets.

Application Insights

The general lighting segment dominated the market in 2025, accounting for 33.0% of total demand, supported by widespread adoption of LED-based residential, commercial, industrial, and outdoor lighting systems due to their high energy efficiency, long operational lifespan, and reduced maintenance requirements. Rapid urbanization, infrastructure modernization, and increasing replacement of conventional lighting technologies with LED solutions continue to drive demand for advanced LED packaging products in general illumination applications. In addition, smart city projects, connected lighting systems, and intelligent building infrastructure are further supporting the deployment of high-performance LED packages across streets, offices, retail spaces, and public facilities worldwide.

The UV sterilization & disinfection application segment is witnessing the fastest growth over the forecast period, due to the rising awareness regarding hygiene, infection control, and water and air purification which is accelerating the adoption of UV-C LED technologies across healthcare, consumer electronics, industrial, and municipal applications. LED packaging manufacturers are increasingly developing compact and thermally efficient UV LED solutions capable of delivering higher irradiation performance and longer operating life. Furthermore, growing implementation of UV disinfection systems in hospitals, transportation hubs, food processing facilities, and smart home appliances is creating strong demand for advanced UV LED packaging technologies, particularly in compact and portable sterilization equipment.

Regional Insights

Asia Pacific LED packaging market dominated the global market with a revenue share of 41.4% in 2025, due to the strong presence of semiconductor and electronics manufacturing hubs across China, South Korea, Taiwan, and Japan. The region benefits from large-scale production capabilities, cost-efficient supply chains, rising demand for consumer electronics and automotive lighting, and increasing investments in advanced display technologies such as Mini-LED and Micro-LED. In addition, rapid urbanization, expanding smart city projects, and growing adoption of energy-efficient lighting solutions across commercial and industrial sectors continue to strengthen regional market leadership.

China LED Packaging Market Trends

LED packaging market in China represents a key market within the Asia Pacific region, driven by its massive electronics manufacturing ecosystem, strong domestic demand for LED displays and lighting products, and government support for semiconductor localization initiatives. The country continues to witness rapid expansion in high-resolution display manufacturing, smart infrastructure projects, and automotive electronics production, which collectively support increasing demand for advanced LED packaging solutions across both domestic and export-oriented industries.

North America LED Packaging Market Trends

LED packaging market North America accounted for 22.8% of the market in 2025, supported by growing demand for high-performance LEDs in automotive lighting, healthcare applications, premium consumer electronics, and specialty industrial systems. The region also benefits from rising investments in smart lighting infrastructure, UV-C disinfection technologies, and next-generation display applications, while strong research and development capabilities continue to accelerate innovation in advanced LED packaging technologies.

U.S. plays a central role in regional market growth, driven by increasing adoption of LED technologies in automotive systems, aerospace, medical devices, and digital signage applications. Strong technological expertise, early adoption of advanced display technologies, and the presence of key semiconductor and lighting companies continue to support demand for high-value LED packaging solutions. In addition, growing investments in smart buildings, energy-efficient infrastructure, and connected lighting systems are further contributing to market expansion across the country.

Europe LED Packaging Market Trends

Europe accounted for 19.7% of the market in 2025, supported by stringent energy-efficiency regulations, increasing penetration of automotive LED lighting systems, and rising adoption of sustainable lighting technologies across commercial and industrial sectors. The region’s strong automotive manufacturing base, particularly in Germany and other Western European countries, continues to drive demand for advanced LED packaging solutions used in adaptive lighting, interior vehicle displays, and intelligent mobility applications.

Key LED Packaging Company Insights

The competitive environment of the market is moderately consolidated, characterized by the presence of leading LED manufacturers, semiconductor companies, and specialized optoelectronics solution providers. Key players compete on the basis of technological innovation, luminous efficiency, thermal management performance, product miniaturization, and LED Packaging capabilities. The market is witnessing increasing consolidation through strategic partnerships, acquisitions, production capacity expansions, and investments in next-generation technologies such as Mini-LED, Micro-LED, chip-scale packaging (CSP), and automotive LED solutions, which continue to shape the competitive landscape globally.

Key LED Packaging Companies:

The following key companies have been profiled for this study on the LED packaging market.

- NICHIA CORPORATION

- ams-OSRAM AG.

- SAMSUNG

- Lumileds Holding B.V.

- Seoul Semiconductor Co., Ltd.

- MLS CO, LTD

- Bridgelux, Inc.

- Penguin Solutions

- TOYODA GOSEI Co., Ltd.

- LITE-ON Technology, Inc.

Competitive Benchmarking

Operating Strategies

Competitive Edge

Weaknesses

Mature Players: NICHIA CORPORATION; ams-OSRAM AG.; SAMSUNG; Lumileds Holding B.V.; Seoul Semiconductor Co., Ltd.; MLS CO. LTD

- Mature players focus on large-scale production, vertical integration, and long-term OEM partnerships to maintain stable global demand.

- Continuous investment in Mini LED, Micro LED, high-efficiency packaging, and smart lighting technologies, while expansions in production capacities.

- Strong R&D capabilities and broad patent portfolios support high-performance and energy-efficient LED solutions.

- Established global networks and strong financial strength enable large-volume production and faster commercialization.

- High capital and operational costs increase pressure on profit margins during price fluctuations.

- Intense competition from low-cost Asian manufacturers limits differentiation in standard LED packaging products.

Emerging Players: Bridgelux, Inc.; Penguin Solutions; Luminus Devices, Inc.; Harvatek Corporation; Refond Optoelectronics Co., Ltd.; Edison Opto Corporation

- Emerging players focus on niche applications such as Mini LED, automotive LEDs, UV LEDs, and display packaging solutions.

- Emphasize partnerships, customized products, and regional expansion to strengthen market presence.

- Higher operational flexibility enables faster response to changing customer and technology requirements.

- Competitive pricing and specialized LED packaging solutions support market penetration in emerging applications.

- Limited financial resources restrict investments in advanced manufacturing and global expansion activities.

- Lower brand recognition and smaller supply networks reduce competitiveness in large-scale contracts.

Recent Developments

-

In April 2026, San’an Optoelectronics officially withdrew its USD 239 million acquisition bid for Lumileds after regulatory resistance, highlighting increasing geopolitical scrutiny in semiconductor and LED technologies.

-

In February 2026, Seoul Semiconductor introduced a new generation of high-power LEDs with improved chip architecture and phosphor technology to enhance efficiency and reliability in advanced lighting applications.

-

In October 2025, Nichia and ams-OSRAM expanded their long-standing intellectual property and patent cross-licensing alliance covering GaN LED and laser technologies, supporting future LED packaging innovation.

LED Packaging Market Report Scope

Report Attribute

Details

Market size in 2025

USD 1.7 billion

Estimated Market size in 2026

USD 1.8 billion

Projected Market size by 2033

USD 2.3 billion

Growth Rate

CAGR of 4.0% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Material, packaging type, application, region

Regional Scope

North America; Europe; Asia Pacific; Latin America; Middle East & Africa

Country Scope

U.S.; Canada; Mexico; Germany; France; UK; Italy; Spain; China; India; Japan; Australia; South Korea; Brazil; Argentina; Saudi Arabia; UAE; South Africa

Key companies profiled

NICHIA CORPORATION; ams-OSRAM AG.; SAMSUNG; Lumileds Holding B.V.; Seoul Semiconductor Co., Ltd.; MLS CO, LTD; Bridgelux, Inc.; Penguin Solutions; TOYODA GOSEI Co., Ltd.; LITE-ON Technology, Inc.

Customization scope

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail of customized purchase options to meet your exact research needs. Explore purchase options

Global LED Packaging Market Report Segmentation

This report forecasts revenue growth at the regional, and country levels and provides an analysis on the latest industry trends and opportunities in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global LED packaging market report based on material, packaging type, application, and region:

-

Material Outlook (Revenue, USD Million, 2021 - 2033)

-

Epoxy Resin

-

Silicone Resin

-

Ceramic Materials

-

Metal Lead Frames & Copper Materials

-

Plastic Materials

-

Others

-

-

Packaging Type Outlook (Revenue, USD Million, 2021 - 2033)

-

Flip-Chip & Mini/Micro LED

-

Glue-on-Board (GOB) & Display Packaging

-

Chip Scale Package (CSP)

-

Chip-on-Board (COB)

-

Surface Mount Device (SMD)

-

Others

-

-

Application Outlook (Revenue, USD Million, 2021 - 2033)

-

UV Sterilization & Disinfection

-

Display Screens & Video Walls

-

Automotive Lighting

-

Backlighting

-

General Lighting

-

Others

-

-

Regional Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

France

-

UK

-

Italy

-

Spain

-

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

Australia

-

-

Latin America

-

Brazil

-

Argentina

-

-

Middle East & Africa

-

Saudi Arabia

-

UAE

-

South Africa

-

-

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

Regional Segmentation Analysis

Detailed assessment of the LED packaging market across various regions, including country-level demand analysis for China, Japan, South Korea, India, the U.S., and Germany, covering production capacity, consumption trends, regulations, and demand across general lighting, automotive, display, and backlighting applications.

Identify high-growth regional markets and investment hotspots. Support regional expansion, distributor alignment, and localization strategies. Enable prioritization of countries based on manufacturing ecosystem, import dependency, and growth potential.

Competitive Benchmarking

Benchmarking of major LED packaging manufacturers based on product portfolio, financial performance, regional presence, technology capabilities, R&D focus, and strategy mapping. Comparative analysis of companies such as NICHIA CORPORATION, ams-OSRAM AG., SAMSUNG, Lumileds Holding B.V., and Seoul Semiconductor Co., Ltd.

Enable competitive positioning and differentiation strategy development. Identify market gaps, technology advantages, and benchmarking opportunities for operational efficiency, innovation, and market penetration.

Opportunity Assessment

Identification of high-growth opportunities across smart lighting, automotive lighting, mini and micro-LEDs, UV LEDs, display technologies, and energy-efficient infrastructure projects. Assessment of whitespace opportunities, emerging applications, technology adoption trends, and investment attractiveness across regions and application areas.

Support strategic investment planning and market entry decisions. Enable identification of emerging revenue streams, innovation opportunities, and high-potential customer segments for long-term business growth.

Frequently Asked Questions About This Report

The global LED packaging market was estimated at around USD 1.7 billion in the year 2025 and is expected to reach around USD 1.8 billion in 2026.

The global LED packaging market is expected to grow at a compound annual growth rate of 4.0% from 2026 to 2033 to reach around USD 2.3 billion by 2033.

General lighting segment dominated the market with 33.0% of total demand in 2025.

The key players in the LED packaging market include NICHIA CORPORATION, ams-OSRAM AG., SAMSUNG, Lumileds Holding B.V., Seoul Semiconductor Co., Ltd., MLS CO, LTD, Bridgelux, Inc., Penguin Solutions, TOYODA GOSEI Co., Ltd., and LITE-ON Technology, Inc.

The LED packaging market is driven by rising demand for energy-efficient lighting, smart lighting systems, and automotive LED applications. Market growth is further supported by expanding mini/micro-LED technologies, increasing electronics production, and strong manufacturing expansion across Asia-Pacific.

Asia Pacific dominated the market with the largest revenue share of 41.4% in 2025 and is expected to grow at the fastest CAGR of 4.5% from 2026 to 2033.

Surface mount device (SMD) segment dominated the market with a share of 40.7% in 2025.

Metal lead frames & copper materials segment dominated the market with a share of 32.7% in 2025.

About the Author(s)

Plastics, Polymers & Resins Research Team

Bulk Chemicals · Plastics, Polymers & ResinsThis report was authored by the plastics, polymers & resins research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the plastics, polymers & resins segment of the bulk chemicals industry. All findings are based on proprietary bulk chemicals databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.