- Home

- »

- Advanced Interior Materials

- »

-

Lost Foam Casting Market Size & Share Report, 2026-2033GVR Report cover

![Lost Foam Casting Market (2026 - 2033)Report]()

Lost Foam Casting Market (2026 - 2033)

Size, Share & Trends Analysis Report By Metal (Iron, Aluminum, Steel), By End-use (Automotive, Industrial Machinery, Agriculture Equipment, Aerospace & Defense), By Region, And Segment Forecasts

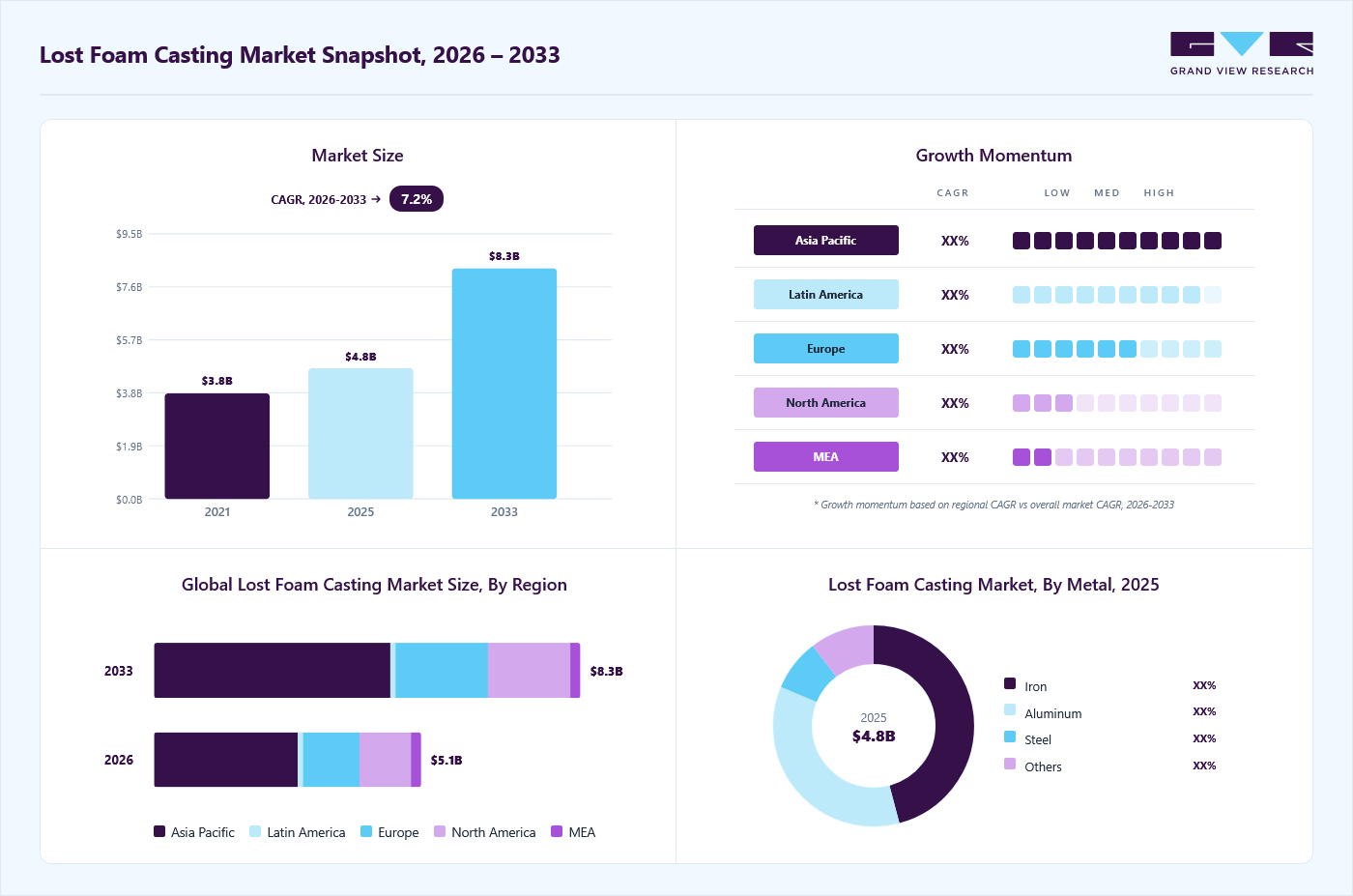

Market Size, 2025

$4.8BMarket Estimate, 2026

$5.1BMarket Forecast, 2033

$8.3BCAGR, 2026–2033

7.2%Lost Foam Casting Market Summary

The global lost foam casting market size was valued at USD 4.8 billion in 2025 and is projected to grow from USD 5.1 billion in 2026 to USD 8.3 billion by 2033, at a CAGR of 7.2% from 2026 to 2033. The market in Asia Pacific dominated with a revenue share of 54.0% in 2025. The growing production of electric vehicles and fuel-efficient automobiles has further accelerated the need for lightweight aluminum castings, supporting market expansion.

Key Market Trends & Insights

- By end-use: Automotive segment held the largest market share of 68.0% in 2025.

- By metal: Iron segment held the largest market share of 45.0% in 2025.

Regional Highlights

- Largest regional market: Asia Pacific (54.0% revenue share, 2025)

- By country: China held the largest market share in 2025

Market Size & Forecast

- Market size in 2025: USD 4.8 Billion

- Estimated market size in 2026: USD 5.1 Billion

- Projected market size by 2033: USD 8.3 Billion

- CAGR (2026-2033): 7.2%

Lost foam casting is a metal-casting process in which a foam pattern, usually made of polystyrene, is coated with a refractory material and embedded in sand before molten metal is poured. The molten metal vaporizes the foam pattern and fills the cavity, producing complex and precise metal components with minimal machining requirements. Automakers are adopting these castings for manufacturing engine blocks, cylinder heads, transmission housings, and other intricate parts due to their ability to produce near-net shape components with reduced material wastage.")

According to the International Energy Agency, global electric car sales surpassed 21 million units in 2025, up more than 20% year on year, with electric vehicles accounting for nearly one in four new cars sold globally.

Rising industrial automation and advancements in manufacturing technologies are also contributing significantly to market growth. These castings enable high-dimensional accuracy, smooth surface finish, and reduced assembly requirements, making it suitable for automated production environments. Industries are increasingly integrating advanced simulation software, robotic pouring systems, and precision molding technologies to improve productivity and reduce operational costs, thereby enhancing the adoption of lost foam casting processes.

The expanding demand from the aerospace and heavy machinery sectors is another major growth driver for the market. Aerospace manufacturers require highly precise, lightweight metal components with complex geometries, which can be efficiently produced via lost-foam casting. Similarly, construction equipment, mining machinery, and agricultural machinery manufacturers are utilizing the process to produce durable cast components with reduced machining requirements and improved structural integrity.

Growing infrastructure development and industrialization in emerging economies such as China, India, Brazil, and Southeast Asian countries are supporting the expansion of foundry industries, thereby driving demand for the market. Increasing investments in transportation, energy, and industrial manufacturing projects have created substantial demand for cast metal components across multiple applications. Favorable government initiatives promoting domestic manufacturing and industrial output are further strengthening market growth in these regions.

Drivers, Opportunities & Restraints

The growth of the lost foam casting market is primarily driven by the increasing demand for lightweight and complex metal components across the automotive and transportation industries. Automakers are increasingly adopting lightweight aluminum and magnesium castings to improve fuel efficiency, reduce emissions, and enhance the range of electric vehicles.

Significant opportunities are emerging from the rapid expansion of electric vehicle manufacturing, industrial machinery production, and infrastructure development in emerging economies. Lost foam casting offers advantages such as near-net-shape manufacturing, reduced material waste, lower assembly requirements, and improved surface finish, which are increasingly valued by manufacturers seeking cost-efficient production methods.

However, the market faces several restraints, including high initial tooling and pattern development costs, particularly for low-volume production runs. Foam patterns used in the process are delicate and susceptible to distortion or damage during handling, which can negatively affect casting quality. In addition, maintaining process consistency and controlling gas-related defects during metal pouring remain technical challenges for manufacturers.

Metal Insights

Iron held the largest revenue share of over 45.0% in 2025. Iron-based lost-foam castings are preferred for manufacturing engine blocks, brake components, pump housings, transmission cases, and structural machinery parts due to their high strength, wear resistance, thermal stability, and cost-effectiveness. The growing global production of passenger vehicles, commercial vehicles, and industrial equipment is substantially increasing the demand for precision iron castings.

The aluminum segment is witnessing strong growth in the market due to the increasing demand for lightweight materials across the automotive, aerospace, and transportation industries. Aluminum castings are widely used in engine blocks, transmission housings, wheels, battery enclosures, and structural vehicle components due to their low weight, corrosion resistance, and high thermal conductivity. Automakers are increasingly replacing traditional ferrous components with aluminum parts to comply with fuel-efficiency regulations and emission-reduction targets.

End-use Insights

Automotive held the revenue share of over 68.0% in 2025, driven by rising global vehicle production and the increasing adoption of lightweight metal components. According to the International Organization of Motor Vehicle Manufacturers (OICA), global vehicle production increased from approximately 92.7 million units in 2024 to nearly 96.4 million units in 2025, reflecting a growth of about 3.9%. This production growth is significantly increasing the demand for precision cast components such as engine blocks, cylinder heads, transmission housings, suspension parts, and structural automotive components.

The agricultural equipment segment is emerging as a significant growth area for the market, driven by the worldwide increase in mechanization of farming activities. Rising global food demand, labor shortages in agriculture, and the need for higher farm productivity are driving investments in advanced agricultural machinery, including tractors, harvesters, seed drills, and irrigation equipment.

Regional Insights

Asia Pacific lost foam casting market accounted for the largest revenue share of over 54.0% in 2025 and is emerging as the fastsest-growing region in the market, driven by the rapid expansion of automotive manufacturing, industrial machinery production, and infrastructure development across China, India, Japan, and Southeast Asia. The region accounted for more than 58% of global vehicle production in recent years, creating strong demand for precision-cast components such as engine blocks, transmission housings, cylinder heads, and EV structural parts.

China is a major growth engine for the lost foam casting market, driven by its dominant automotive manufacturing industry and the rapid expansion of electric vehicle production. The country produced more than 34.5 million vehicles in 2025, maintaining its position as the world’s largest automotive producer, while new energy vehicle (NEVs) production exceeded 16 million units.

North America Lost Foam Casting Market Trends

North America is witnessing strong growth in the market due to rising demand for lightweight and high-precision metal components across the automotive, aerospace, and industrial equipment sectors. The rapid expansion of electric vehicle manufacturing in the U.S. and Canada is increasing the need for complex aluminum castings used in battery housings, motor casings, transmission systems, and structural vehicle components.

U.S. Lost Foam Casting Market Trends

The lost foam casting market in U.S. is significantly supported by the rising aircraft manufacturing activity and increasing demand for lightweight precision components. Boeing delivered 600 commercial aircraft in 2025, marking its highest annual delivery total since 2018 and reflecting the recovery of commercial aviation demand and expansion of aircraft production programs.

Europe Lost Foam Casting Market Trends

Europe is witnessing steady growth in the market due to the region’s strong automotive manufacturing base and increasing transition toward electric mobility and lightweight vehicle production. Countries such as Germany, France, Italy, and Spain are investing heavily in electric vehicle manufacturing, battery production facilities, and advanced automotive component technologies. Europe produced more than 14 million passenger cars in 2025, with a growing share of hybrid and electric vehicles requiring lightweight aluminum castings for battery enclosures, motor housings, and structural components.

Latin America Lost Foam Casting Market Trends

Latin America is one of the world’s largest agricultural equipment markets due to extensive farming activity in Brazil and Argentina, increasing the need for high-performance cast parts used in tractors, harvesters, irrigation systems, and processing equipment. Governments across the region are also promoting industrial development and manufacturing competitiveness, encouraging local foundries to improve efficiency and reduce production waste.

Key Lost Foam Casting Company Insights

Some of the key players operating in the market include Alcoa Corporation, Dynacast International Inc., and others

-

Alcoa Corporation is an aluminum producer, headquartered in Pittsburgh, Pennsylvania, with operations spanning bauxite mining, alumina refining, and aluminum smelting. The company serves industries such as automotive, aerospace, construction, packaging, and industrial manufacturing through its vertically integrated aluminum value chain. Alcoa focuses strongly on lightweight and sustainable aluminum solutions that support fuel efficiency and emission reduction targets across transportation and industrial sectors.

-

Dynacast International Inc. is a global precision manufacturing company specializing in metal casting and engineered metal components, with manufacturing facilities across North America, Europe, and the Asia Pacific. The company provides precision casting solutions for automotive, consumer electronics, healthcare, industrial machinery, and telecommunications industries. Dynacast is known for its expertise in complex metal component production, tooling design, and advanced manufacturing technologies that enable high-dimensional accuracy and efficient mass production.

Key Lost Foam Casting Companies:

The following key companies have been profiled for this study on the lost foam casting market.

- Alcoa Corporation

- Dynacast International Inc.

- Gibbs Die Casting Corp.

- Grede Holdings LLC

- Gujarat Metal Cast

- Martinrea International Inc.

- Precision Castparts Corp.

- Ryobi Limited

- Steelcast Limited

- Taiyuan Simis Investment Casting Co., Ltd.

Recent Development

-

In October 2025, Dongshan EPS Machinery launched an efficient and energy-saving EPS lost foam casting machine designed to drive intelligent upgrades in the casting industry. This advanced equipment features optimized steam control, precision molding technology, and automation to minimize cycle times, reduce energy waste, and enhance throughput for large-scale foam production across sectors such as packaging, insulation, and automotive components.

Lost Foam Casting Market Report Scope

Report Attribute

Details

Market Definition

Market size represents the total annual revenue generated from sale of lost foam casting used for different end uses.

Market size in 2025

USD 4.8 billion

Estimated market size in 2026

USD 5.1 billion

Projected market size by 2033

USD 8.3 billion

Growth rate

CAGR of 7.2% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion, volume in kilotons, and CAGR from 2026 to 2033

Report coverage

Revenue & volume forecast, competitive landscape, growth factors, and trends

Segments covered

Metal, end-use, region

Regional scope

North America; Europe; Asia Pacific; Latin America; Middle East & Africa

Country scope

U.S.; Canada; Mexico; Germany; Italy; France; Russia; China; India; Japan; Brazil; Saudi Arabia, UAE

Key companies profiled

Precision Castparts Corp.; Alcoa Corporation; Ryobi Limited; Martinrea International Inc.; Dynacast International Inc.; Gibbs Die Casting Corp.; Grede Holdings LLC; Taiyuan Simis Investment Casting Co., Ltd.; Gujarat Metal Cast; Steelcast Limited

Customization scope

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Lost Foam Casting Market Report Segmentation

This report forecasts revenue and volume growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For the purpose of this study, Grand View Research has segmented the global lost foam casting market report on the basis of metal, end-use, and region.

-

Metal Outlook (Revenue, USD Billion; Volume, Kilotons; 2021 - 2033)

-

Iron

-

Aluminum

-

Steel

-

Others

-

-

End-use Outlook (Revenue, USD Billion; Volume, Kilotons; 2021 - 2033)

-

Automotive

-

Industrial Machinery

-

Agriculture Equipment

-

Aerospace & Defense

-

Others

-

-

Regional Outlook (Revenue, USD Billion; Volume, Kilotons; 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

Italy

-

France

-

Russia

-

-

Asia Pacific

-

China

-

India

-

Japan

-

-

Latin America

-

Brazil

-

-

Middle East & Africa

-

Saudi Arabia

-

UAE

-

-

Frequently Asked Questions About This Report

Asia Pacific dominated with a 54.0% revenue share in 2025.

The automotive segment held the largest revenue share (over 68.0%) in 2025.

The global lost foam casting market size was valued at USD 4.8 billion in 2025 and is estimated at USD 5.1 billion for 2026.

The global lost foam casting market is expected to grow at a CAGR of 7.2% from 2026 to 2033, reaching USD 8.3 billion by 2033.

The iron segment dominated the market with a revenue share of over 45.0% in 2025.

Key players include Precision Castparts Corp.; Alcoa Corporation; Ryobi Limited; Martinrea International Inc.; Dynacast International Inc.; Gibbs Die Casting Corp.; Grede Holdings LLC; Taiyuan Simis Investment Casting Co., Ltd.; Gujarat Metal Cast; Steelcast Limited.

The key factor driving the growth of the global lost foam casting market is the rising demand for lightweight and complex metal components across the automotive, aerospace, and industrial machinery sectors.

About the Author(s)

Advanced Interior Materials Research Team

Advanced Materials · Advanced Interior MaterialsThis report was authored by the advanced interior materials research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the advanced interior materials segment of the advanced materials industry. All findings are based on proprietary advanced materials databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.