- Home

- »

- Next Generation Technologies

- »

-

Multiagent Systems Market Size & Share Report, 2026-2033GVR Report cover

![Multiagent Systems Market (2026 - 2033)Report]()

Multiagent Systems Market (2026 - 2033)

Size, Share & Trends Analysis Report By Component (Platforms/Software, Services), By Deployment (Cloud, On-premises) By Application, By End-use (BFSI, IT & Telecommunication), By Region, And Segment Forecasts

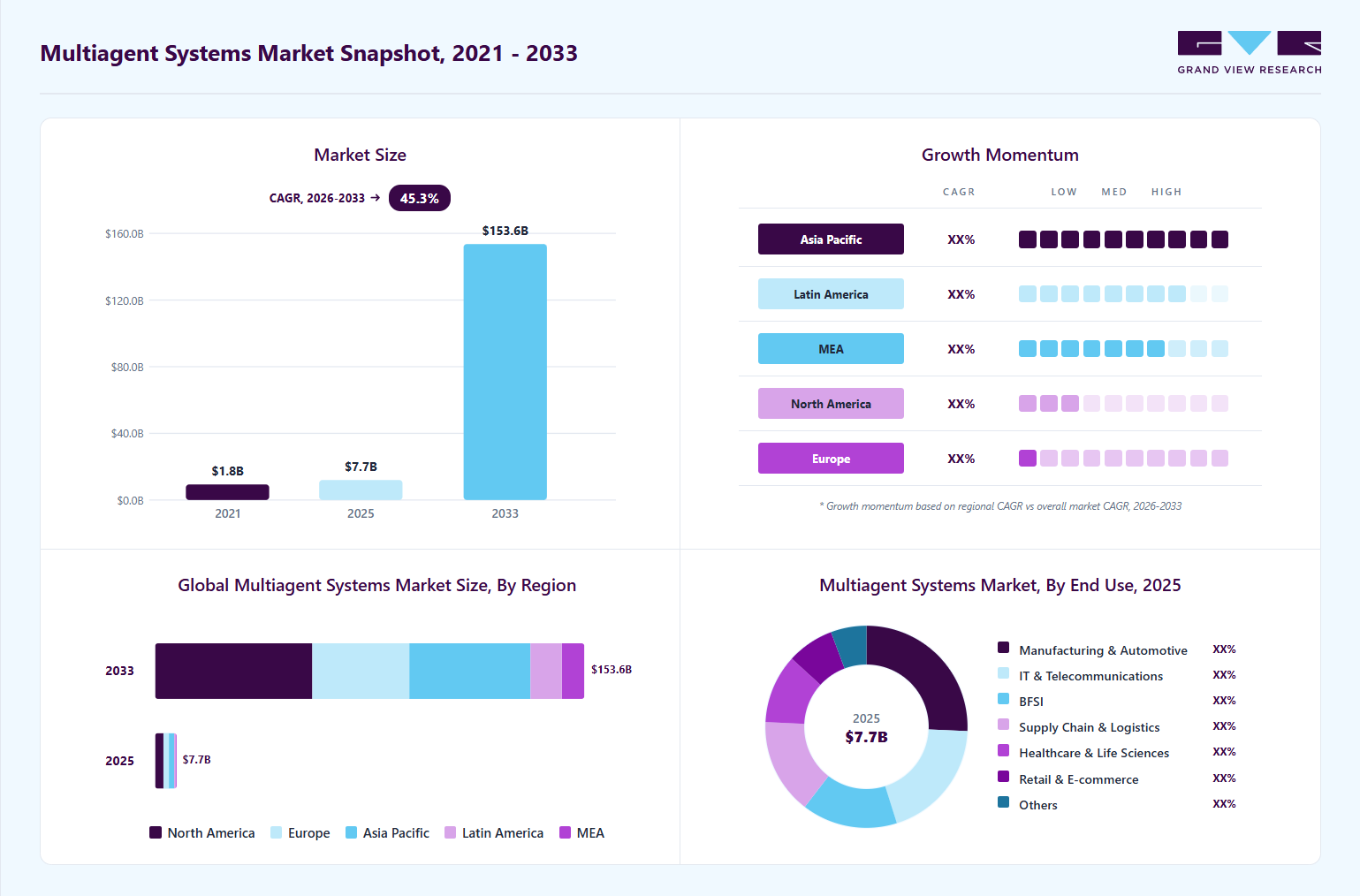

Market Size, 2025

$7.7BMarket Estimate, 2026

$11.3BMarket Forecast, 2033

$153.6BCAGR, 2026–2033

45.3%Multiagent Systems Market Summary

The global multiagent systems market size was valued at USD 7.7 billion in 2025 and is projected to grow from USD 11.3 billion in 2026 to USD 153.6 billion by 2033, at a CAGR of 45.3% from 2026 to 2033. The market in North America dominated with a revenue share of 38.0% in 2025. The market is driven by the rising adoption of autonomous AI agents across enterprise workflows, increasing demand for real-time decision-making and distributed intelligence systems, growing integration of multiagent architectures in robotics and industrial automation, expanding use of collaborative AI in cybersecurity and defense applications, accelerating deployment of smart transportation and logistics optimization solutions, and the increasing need for scalable AI-driven coordination in cloud and edge computing environments.

Key Market Trends & Insights

- By component: Platforms/software segment held the largest market share of 63.0% in 2025.

- By deployment: Cloud segment held the largest market share of 67.0% in 2025.

- By application: Workflow and process orchestration segment held the largest market share of 30.6% in 2025.

- By end-use: Manufacturing & automotive segment held the largest market share of 25.7% in 2025.

Regional Highlights

- Largest regional market: North America (38.0% revenue share, 2025)

- By country: The U.S. held the largest market share in 2025

Market Size & Forecast

- Market size in 2025: USD 7.7 Billion

- Estimated market size in 2026: USD 11.3 Billion

- Projected market size by 2033: USD 153.6 Billion

- CAGR (2026-2033): 45.3%

The multiagent systems industry is experiencing significant growth, driven by the increasing adoption of autonomous AI agents that facilitate collaborative decision-making within enterprise environments. Organizations are deploying multiagent frameworks to automate complex workflows, enhance operational efficiency, and minimize human intervention in large-scale business processes. The integration of generative AI with multiagent architectures supports intelligent task orchestration, contextual reasoning, and adaptive problem-solving across various industries. Technology providers are investing in advanced agent communication protocols and decentralized intelligence models to improve interoperability among AI systems. These developments are accelerating enterprise transformation initiatives in sectors such as banking, financial services, and insurance (BFSI), healthcare, manufacturing, and logistics.")

The adoption of multiagent systems in cybersecurity and defense operations is becoming a prominent market trend, driven by the increasing complexity of cyber threats and digital warfare strategies. Organizations are employing autonomous AI agents for continuous threat detection, network surveillance, incident response, and adaptive security management. Defense agencies are integrating multiagent intelligence platforms into autonomous surveillance systems, battlefield simulations, and mission planning. The collaborative capabilities of multiple AI agents to respond to evolving threats in real time are enhancing operational resilience. These developments are generating substantial growth opportunities for AI-driven security orchestration and defense modernization initiatives.

The market is advancing due to the increased implementation of multiagent systems in smart mobility, transportation, and logistics optimization. Enterprises utilize collaborative AI agents for fleet management, traffic optimization, autonomous vehicle coordination, and enhanced supply chain visibility. The growth of connected infrastructure and smart city initiatives is promoting the deployment of distributed intelligent systems. Multiagent platforms enable real-time route optimization, energy-efficient transportation management, and rapid adaptation to changing traffic conditions. These trends improve logistics efficiency, lower operational costs, and support the development of autonomous mobility ecosystems.

Market Dynamics

The rising enterprise adoption of agentic AI and autonomous decision-making systems is significantly accelerating the growth of the multiagent systems industry across global industries. Organizations are increasingly deploying AI agents that can independently analyze data, coordinate workflows, and execute complex operational tasks with minimal human intervention. Growing pressure to improve operational efficiency, reduce response times, and optimize enterprise productivity is encouraging businesses to integrate autonomous AI frameworks into core business functions. Enterprises across BFSI, healthcare, manufacturing, retail, and telecommunications use multi-agent systems to automate customer interactions, enable predictive analytics, support cybersecurity operations, and coordinate supply chains. In addition, rapid advancements in large language models, reasoning capabilities, and contextual AI processing are strengthening the ability of autonomous agents to manage dynamic enterprise environments more effectively.

Technology providers are continuously expanding enterprise AI ecosystems with orchestration platforms, autonomous workflow engines, and collaborative AI frameworks designed to support large-scale multi-agent deployments. Increasing investments in cloud AI infrastructure, generative AI integration, and intelligent automation platforms are enabling enterprises to scale autonomous decision-making capabilities across distributed operations. Organizations are also prioritizing adaptive AI systems that can coordinate multiple agents in real time to improve business continuity, operational resilience, and enterprise agility. The growing use of AI copilots, digital workers, and autonomous enterprise assistants is further accelerating the adoption of agentic AI architectures within modern business environments. As enterprises continue shifting toward intelligent, self-optimizing operational models, demand for advanced multiagent systems is expected to grow steadily over the forecast period.

High infrastructure and deployment costs remain a significant barrier to adopting multiagent systems in enterprises. Implementing these architectures requires substantial investment in high-performance computing, cloud resources, data storage, and advanced networking to enable real-time coordination among agents. Many organizations, especially small and medium-sized enterprises, face financial challenges when deploying scalable AI ecosystems for complex, distributed workloads. Integrating generative AI models, orchestration frameworks, and automation systems further increases operational expenses for customization, maintenance, and optimization. Ongoing hardware upgrades, GPU acceleration, and large-scale computational needs add to the overall cost burden for enterprises adopting advanced multiagent technologies.

The complexity of integrating multiagent systems with existing enterprise and legacy infrastructure further intensifies deployment challenges. Organizations often face additional costs for cybersecurity, AI governance, compliance, and ensuring interoperability across distributed systems. Maintaining real-time synchronization, low-latency communication, and reliable performance among autonomous agents requires ongoing investment in IT infrastructure and technical expertise. Enterprises in regulated industries may also need to invest in secure deployment models, private AI infrastructure, and robust data management to address regulatory and operational risks. These financial and operational constraints continue to limit adoption among cost-sensitive organizations and hinder large-scale commercialization of multiagent systems.

The integration of multi-agent systems in smart manufacturing is driving significant global market growth. Manufacturers are adopting autonomous AI agents to optimize production planning, monitor equipment, coordinate robotics, and enhance real-time decision-making. The adoption of Industry 4.0 strategies and factory modernization is increasing demand for decentralized AI architectures that support adaptive and self-coordinated operations. Multi-agent systems help manufacturers improve efficiency, reduce downtime, enhance predictive maintenance, and increase production flexibility. Investments in automation, connected sensors, digital twins, and AI-powered analytics are further expanding the commercial potential of multi-agent technologies in manufacturing.Opportunities are growing with the increased use of collaborative robotics, autonomous material handling, and intelligent supply chain coordination. Enterprises are adopting AI-driven frameworks to synchronize machines, production units, and robotics in real time, improving productivity and resource use. The expansion of edge AI, industrial IoT, and cloud-connected platforms is enabling broader adoption of scalable multi-agent environments. Manufacturers are also implementing autonomous decision-making systems to address labor shortages, enhance quality control, and accelerate operational responsiveness. As digital transformation and intelligent automation remain priorities, demand for advanced multi-agent coordination technologies is expected to rise.

Market Concentration & Characteristics

The multiagent systems industry is characterized by moderate-to-high concentration, with major cloud providers, enterprise AI companies, workflow automation vendors, and emerging agentic AI startups competing in areas such as intelligent automation, autonomous orchestration, and enterprise decision-making applications. Leading participants consolidate their positions through investments in generative AI, large language models, cloud-native orchestration platforms, and enterprise AI ecosystems that enable scalable multi-agent coordination. Established companies leverage extensive enterprise customer networks, advanced computing infrastructure, and integrated AI development platforms to support large-scale deployment across industries including banking, financial services, and insurance (BFSI), manufacturing, healthcare, retail, and logistics. In contrast, emerging vendors differentiate themselves by focusing on specialized AI agent frameworks, low-code orchestration platforms, and industry-specific automation capabilities to address the needs of rapidly evolving enterprise environments. The increasing adoption of agentic AI, autonomous workflows, AI copilots, and collaborative digital workforce technologies is intensifying market competition and accelerating global innovation.

Multiagent systems compete with conventional enterprise automation software, robotic process automation tools, standalone AI assistants, and legacy workflow management platforms that may offer lower implementation complexity and infrastructure requirements. Many enterprises continue to rely on traditional automation systems and centralized decision-making architectures due to concerns about deployment costs, integration challenges, cybersecurity risks, and governance complexity associated with autonomous AI environments. In addition, limited interoperability across enterprise systems and the shortage of skilled professionals capable of managing advanced multi-agent ecosystems may restrain adoption among certain organizations. However, multiagent systems provide significant advantages, including adaptive decision-making, real-time coordination, autonomous task execution, scalable workflow optimization, and improved operational intelligence across distributed enterprise operations. Growing investments in generative AI infrastructure, intelligent automation, smart manufacturing, and enterprise digital transformation strategies are expected to support long-term demand for advanced multi-agent technologies worldwide.

Component Insights

The platforms/software segment dominated the market in 2025, accounting for over 63% of revenue, primarily supported by the growing enterprise shift toward autonomous AI ecosystems capable of coordinating multiple intelligent agents across operational environments. Continuous advancements in agent orchestration software, generative AI integration, and real-time workflow automation have encouraged enterprises to modernize legacy systems with scalable multi-agent platforms. Technology vendors are increasingly introducing enterprise-ready solutions featuring adaptive reasoning, collaborative AI capabilities, and secure cloud-native deployment models to strengthen business productivity and operational agility. Rising adoption of intelligent digital workers, AI copilots, and decentralized decision-making architectures across large enterprises is further accelerating the long-term expansion of the segment.

The services segment is anticipated to grow significantly in the coming years, owing to the increasing enterprise focus on AI integration, agent orchestration optimization, and customized deployment support for autonomous business operations. Market activity indicates rising adoption of consulting and managed services as organizations seek assistance with workflow automation, generative AI implementation, cybersecurity management, and interoperability across complex enterprise environments. In addition, enterprises are increasingly outsourcing multi-agent system configuration, model training, and governance management to specialized service providers to reduce deployment complexity and accelerate operational efficiency. Growing demand for scalable AI transformation strategies, continuous performance monitoring, and industry-specific implementation expertise is expected to further support long-term expansion of the segment globally.

Deployment Insights

The cloud segment accounted for the largest market revenue share in 2025, as enterprises increasingly shifted toward centralized AI ecosystems capable of supporting large-scale agent collaboration, intelligent automation, and dynamic workload management. Strong momentum in cloud-based generative AI adoption encouraged organizations to deploy multi-agent systems through hyperscale infrastructure environments that offer greater computing flexibility and faster scalability. Technology providers also expanded integrated AI cloud offerings with embedded orchestration tools, governance frameworks, and low-code development capabilities, making cloud deployment more attractive for enterprise customers. Growing reliance on remote operations, real-time analytics, and cross-functional AI coordination continues to strengthen the commercial adoption of cloud-based multi-agent architectures across global industries.

The on-premises segment is expected to grow significantly in the coming years. This is driven by increasing demand for secure, low-latency, and fully controlled AI environments in highly regulated industries such as defense, banking, healthcare, and government. Enterprises managing confidential operational and customer data are investing more in dedicated infrastructure to strengthen cybersecurity resilience, maintain data sovereignty, and comply with evolving regulations. The growing deployment of autonomous AI agents in industrial facilities, critical infrastructure, and private enterprise networks also encourages organizations to prioritize localized computing environments with greater customization flexibility. The rising need for direct oversight of AI workloads, internal governance, and reduced reliance on external cloud services is accelerating investment in private AI infrastructure strategies.

Application Insights

The workflow and process orchestration segment held a significant share of market revenue in 2025, driven by enterprises seeking to automate complex operations with coordinated AI agents for real-time decision-making and task execution. Organizations in BFSI, manufacturing, retail, and telecommunications adopted orchestration frameworks to streamline workflows, enhance operational visibility, and minimize manual intervention. Increased integration of generative AI, intelligent automation platforms, and digital assistants accelerated demand for orchestration solutions that enable adaptive reasoning and interoperability across systems. Ongoing investments in hyper automation and AI-driven process transformation continue to highlight the importance of orchestration technologies in modern enterprises.

The multi-robot & autonomous system coordination segment is predicted to foresee significant growth in the forecast years, driven by increasing adoption of collaborative robotics, autonomous mobility systems, and AI-enabled industrial automation across manufacturing, logistics, warehousing, and defense operations. Enterprises are rapidly deploying coordinated robotic fleets and intelligent autonomous systems to improve operational efficiency, reduce labor dependency, and support real-time adaptive decision-making in complex environments. Rising investments in smart factories, autonomous delivery networks, drone coordination platforms, and AI-powered robotics infrastructure are further accelerating demand for advanced multi-agent coordination technologies. Growing emphasis on real-time communication, decentralized control architectures, and synchronized machine intelligence is reshaping next-generation automation strategies across global industries.

End-use Insights

The manufacturing & automotive segment accounted for a prominent market revenue share in 2025, driven by the increasing deployment of AI-powered automation systems, collaborative robotics, and intelligent production orchestration technologies across industrial environments. Automotive manufacturers and industrial enterprises are rapidly integrating multi-agent systems to optimize supply chain coordination, predictive maintenance, quality inspection, and autonomous production workflows to improve operational efficiency and reduce downtime. Growing investments in smart factory initiatives, Industry 4.0 transformation programs, and connected manufacturing ecosystems are further strengthening adoption of decentralized AI decision-making architectures within production facilities. In addition, rising demand for autonomous mobility technologies, intelligent warehouse operations, and real-time industrial analytics continues to accelerate enterprise spending on advanced multi-agent automation capabilities.

The supply chain & logistics segment is predicted to foresee significant growth in the forecast period, owing to the rising need for intelligent coordination systems capable of managing dynamic inventory operations, warehouse automation, route optimization, and real-time shipment tracking across global logistics networks. Enterprises are increasingly implementing multi-agent technologies to improve supply chain visibility, strengthen operational resilience, and enable faster decision-making in response to fluctuating demand and distribution complexities. Growing adoption of autonomous mobile robots, AI-powered fleet management systems, and predictive logistics analytics is further transforming transportation and fulfillment operations across e-commerce, retail, and manufacturing sectors. Increased focus on reducing delivery delays, optimizing fuel efficiency, and enhancing end-to-end operational agility continues to accelerate investment in AI-driven logistics automation frameworks.

Regional Insights

North America multiagent systems market dominated the market in 2025, accounting for over 38% of global revenue, supported by the strong presence of leading AI technology companies, hyperscale cloud providers, and advanced enterprise automation ecosystems across the region. Enterprises in the U.S. and Canada are rapidly integrating agentic AI platforms, autonomous workflow systems, and intelligent orchestration technologies to improve operational efficiency, cybersecurity management, and real-time business decision-making capabilities. Rising investments in generative AI infrastructure, defense automation, industrial robotics, and large-scale digital transformation initiatives continue to strengthen regional market leadership.

U.S. Multiagent Systems Market Trends

The U.S. multiagent systems industry is gaining strong momentum due to increasing integration of autonomous AI agents into enterprise cybersecurity, defense intelligence, financial analytics, and large-scale cloud computing environments. Organizations are increasingly deploying multi-agent architectures to enhance real-time data processing, automate complex enterprise operations, and improve adaptive business intelligence capabilities. Expanding investments in AI semiconductor infrastructure, enterprise generative AI platforms, and advanced robotics innovation continue to position the U.S. as a major hub for next-generation intelligent system deployment.

Europe Multiagent Systems Market Trends

The Europe multiagent systems industry is experiencing steady expansion as enterprises increasingly prioritize energy-efficient automation, connected industrial ecosystems, and AI-enabled operational resilience strategies. Growing deployment of collaborative robotics, predictive maintenance platforms, and decentralized manufacturing intelligence systems is reshaping industrial digitalization across the region. Increasing emphasis on ethical AI frameworks, enterprise transparency, and secure data management is encouraging wider adoption of controlled and interoperable multi-agent environments.

Asia Pacific Multiagent Systems Market Trends

The Asia Pacific multiagent systems industry is witnessing accelerated growth supported by rapid expansion of smart city projects, industrial robotics adoption, and AI-powered logistics modernization initiatives across emerging and developed economies. Enterprises are increasingly leveraging multi-agent technologies to improve supply chain agility, automate customer engagement, and optimize large-scale industrial operations within highly dynamic business environments. Rising availability of cloud AI platforms, government-backed innovation programs, and expanding investments in autonomous mobility ecosystems continue to strengthen regional technology adoption.

Key Multiagent Systems Company Insights

Some key companies in the multiagent systems industry are Microsoft Corporation, Google LLC, Amazon Web Services Inc., OpenAI L.L.C., and Anthropic PBC

-

Microsoft Corporation operates in the multiagent systems industry through its cloud computing, enterprise software, and AI platform businesses. The company integrates AI agents and orchestration capabilities across Azure AI, Microsoft Copilot, Dynamics 365, and enterprise productivity applications. Its offerings support workflow automation, enterprise decision-making, and multi-agent coordination within cloud-based business environments. Microsoft’s activities in the market are supported by investments in generative AI infrastructure, enterprise AI services, and autonomous system integration.

-

Google LLC participates in the market through its AI research, cloud infrastructure, and enterprise AI software operations. The company develops AI models, orchestration frameworks, and distributes computing technologies used for intelligent automation and multi-agent coordination. Google’s capabilities are integrated across Google Cloud, Gemini AI models, and enterprise data analytics platforms. Its market presence is associated with applications involving real-time data processing, AI-driven workflows, and collaborative AI systems.

Key Multiagent Systems Companies:

The following key companies have been profiled for this study on the multiagent systems market.

- Microsoft Corporation

- Google LLC

- Amazon Web Services Inc.

- OpenAI L.L.C.

- Anthropic PBC

- Automation Anywhere Inc.

- Kore.ai Inc.

- Moveworks Inc.

- Aisera Inc.

- LangChain Inc.

- CrewAI Inc.

- GreyOrange Pte. Ltd.

Competitive Benchmarking

Operating Strategies

Competitive Edge

Weaknesses

Mature Players: Microsoft Corporation, Google LLC, Amazon Web Services Inc., Automation Anywhere Inc.

- Mature players are increasingly investing in agentic AI orchestration, enterprise automation, and cloud-native multi-agent platforms to strengthen large-scale operational capabilities.

- Leading vendors are expanding partnerships with hyperscalers, enterprise software providers, and AI infrastructure companies to accelerate autonomous system deployment.

- Established companies benefit from strong enterprise ecosystems, extensive cloud infrastructure, and broad customer bases across global industries.

- Mature players possess stronger financial capabilities and R&D resources to support advanced AI model development and enterprise-scale deployments.

- Large organizations often face integration complexity and slower deployment cycles due to legacy infrastructure and enterprise-scale operational structures.

- High operational costs, governance requirements, and increasing regulatory scrutiny may limit deployment flexibility across certain enterprise environments.

Emerging Players: Anthropic PBC, Kore.ai Inc., LangChain Inc., CrewAI Inc.

- Emerging companies are focusing on specialized AI agent frameworks, workflow automation tools, and niche enterprise use cases to differentiate their offerings.

- Startups are increasingly emphasizing low-code AI agent development, decentralized AI architectures, and industry-specific automation platforms to gain market traction.

- Smaller vendors often demonstrate faster innovation cycles and greater flexibility in deploying customized autonomous AI solutions.

- Emerging players can rapidly adapt to evolving enterprise AI demands and integrate new generative AI capabilities more efficiently.

- Emerging companies frequently face limitations in computing infrastructure, enterprise reach, and long-term scalability capabilities.

- Limited financial resources and lower brand recognition may restrict their ability to compete with established technology providers in large enterprise contracts.

Recent Developments

-

In April 2026, SAP and Google Cloud expanded their strategic partnership to deploy multi-agent artificial intelligence (AI) capabilities across enterprise ecosystems. This collaboration enables organizations to automate and optimize marketing workflows at scale. The integration of SAP Engagement Cloud, SAP Customer Experience (CX), Joule Agents, and Gemini Enterprise allows AI agents to securely access unified enterprise data and execute complex campaigns through coordinated multi-agent orchestration. Gemini Enterprise functions as a centralized hub for agent coordination across SAP and Google Cloud environments, supporting real-time decision-making, workflow automation, and continuous campaign optimization. This partnership further advances the adoption of agentic AI in enterprises by enhancing operational efficiency, minimizing manual intervention, and accelerating AI-driven customer experience transformation.

-

In March 2026, Kore.ai introduced its Agent Management Platform (AMP) to enable enterprises to centrally manage and govern AI agents within complex business environments. The platform facilitates interoperability across diverse AI frameworks and cloud ecosystems, allowing organizations to coordinate and optimize multi-agent workflows at scale. Kore.ai stated that the solution offers centralized observability, policy enforcement, and performance monitoring to address increasing enterprise concerns regarding AI governance and operational control. This launch demonstrates the growing adoption of multi-agent systems for autonomous workflow orchestration, enterprise automation, and intelligent decision-making across various industries.

Multiagent Systems Market Report Scope

Report Attribute

Details

Market size in 2025

USD 7.7 billion

Estimated market size in 2026

USD 11.3 billion

Projected market size by 2033

USD 153.6 billion

Growth rate

CAGR of 45.3% from 2026 to 2033

Base Year

2025

Actual data

2021 - 2025

Forecast period

2026 - 2033

Quantitative units

Revenue in USD billion, and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Component, deployment, application, end-use, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; Germany; UK; France; China; Japan; India; South Korea; Australia; Brazil; UAE; Kingdom of Saudi Arabia; South Africa.

Key companies profiled

Microsoft Corporation; Google LLC; Amazon Web Services Inc.; OpenAI L.L.C.; Anthropic PBC; Automation Anywhere Inc.; Kore.ai Inc.; Moveworks Inc.; Aisera Inc.; LangChain Inc.; CrewAI Inc.; GreyOrange Pte. Ltd.

Customization scope

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Multiagent Systems Market Report Segmentation

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global multiagent systems market report based on component, deployment, application, end-use, and region:

-

Component Outlook (Revenue, USD Billion, 2021 - 2033)

-

Platforms/ Software

-

Services

-

-

Deployment Outlook (Revenue, USD Billion, 2021 - 2033)

-

On-premises

-

Cloud

-

-

Application Outlook (Revenue, USD Billion, 2021 - 2033)

-

Workflow & Process Orchestration

-

Multi-robot & Autonomous System Coordination

-

Predictive Analytics

-

Decision Support & Planning

-

Others

-

-

End-use Outlook (Revenue, USD Billion, 2021 - 2033)

-

Manufacturing & Automotive

-

BFSI

-

IT & Telecommunications

-

Supply Chain & Logistics

-

Healthcare & Life Sciences

-

Retail & E-commerce

-

Others

-

-

Regional Outlook (Revenue, USD Billion, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

France

-

-

Asia Pacific

-

China

-

Japan

-

India

-

South Korea

-

Australia

-

-

Latin America

-

Brazil

-

-

Middle East and Africa (MEA)

-

UAE

-

Kingdom of Saudi Arabia

-

South Africa

-

-

Delivered Customization

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

Market Entry & Expansion Assessment

Enterprise AI adoption and regional demand analysis

Multi-agent platform competitive benchmarking

Industry-specific use-case assessment

AI governance and regulatory evaluation

Identified high-growth market opportunities

Supported go-to-market strategy development

Highlighted investment priorities and adoption risks

Enabled data-driven expansion planning

Product Positioning & Competitive Intelligence

AI orchestration platform benchmarking

Workflow automation capability analysis

Enterprise customer preference assessment

Competitor ecosystem and partnership evaluation

Improved product differentiation strategy

Supported pricing and deployment optimization

Identified unmet enterprise automation needs

Enhanced competitive positioning

Technology & Innovation Assessment

Agentic AI and autonomous systems trend analysis

Generative AI integration assessment

Cloud AI infrastructure evaluation

Ecosystem and partnership mapping

Identified future technology growth areas

Supported innovation roadmap planning

Evaluated commercialization potential

Strengthened strategic partnership decisions

Frequently Asked Questions About This Report

The platforms/software segment accounted for the largest share of 63% in 2025, while services is growing significantly.

The cloud segment held the highest market share of 67.0% in 2025. while on-premises is growing significantly.

The workflow and process orchestration segment led with a 30.6% revenue share in 2025, while multi-robot & autonomous system coordination is growing significantly.

The manufacturing & automotive segment held the highest market share of 25.7% in 2025, while supply chain & logistics is growing significantly.

North America dominated the multiagent systems market, accounting for over 38% in 2025.

Some key players operating in the multiagent systems market include Microsoft Corporation, Google LLC, Amazon Web Services Inc., OpenAI L.L.C., Anthropic PBC, Automation Anywhere Inc., Kore.ai Inc., Moveworks Inc., Aisera Inc., LangChain Inc., CrewAI Inc., and GreyOrange Pte. Ltd.

Key factors include the rising adoption of autonomous AI agents across enterprise workflows, increasing demand for real-time decision-making and distributed intelligence systems, growing integration of multiagent architectures in robotics and industrial automation, and expanding use of collaborative AI in cybersecurity and defense applications.

The global multiagent systems market size was estimated at USD 7.7 billion in 2025 and is expected to reach USD 11.3 billion in 2026.

The global multiagent systems market is expected to grow at a compound annual growth rate of 45.3% from 2026 to 2033, reaching USD 153.6 billion by 2033.

About the Author(s)

Next Generation Technologies Research Team

Technology · Next Generation TechnologiesThis report was authored by the next generation technologies research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the next generation technologies segment of the technology industry. All findings are based on proprietary technology databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.