- Home

- »

- Next Generation Technologies

- »

-

Simulators Market Size, Share, Trends, Industry Report 2033GVR Report cover

![Simulators Market Size, Share & Trends Report]()

Simulators Market (2025 - 2033) Size, Share & Trends Analysis Report By Solution, By Type (Airborne, Ground, Marine), By Application, By Technique (Live, Virtual, Constructive, Hybrid), By End-use, By Region, And Segment Forecasts

Market Size, 2024

$13.0BMarket Estimate, 2026

$14.2BMarket Forecast, 2033

$25.2BCAGR, 2025–2033

7.4%Simulators Market Summary

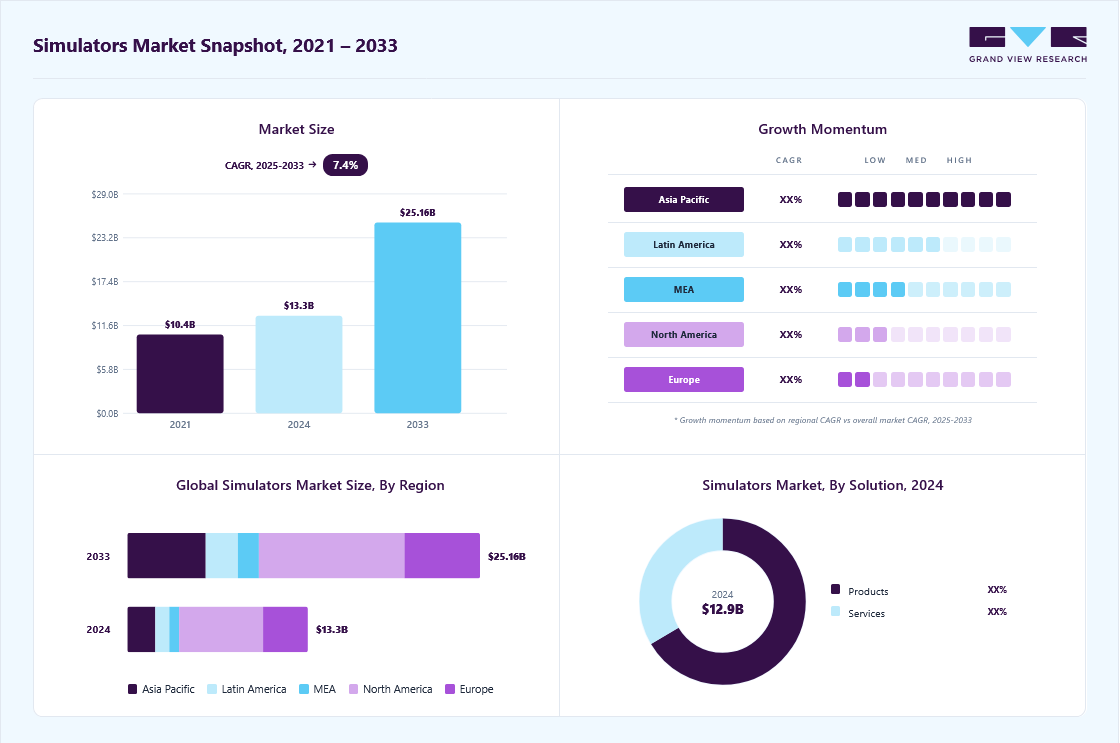

The global simulators market size was estimated at USD 13.03 billion in 2024 and is projected to reach USD 25.16 billion by 2033, growing at a CAGR of 7.4% from 2025 to 2033. The market growth is primarily driven by the increasing adoption of VR/AR in training environments, demand for cost-effective and risk-free skill development, use of simulation in healthcare and automotive testing, and integration of AI and real-time data for more immersive experiences.

Key Market Trends & Insights

- North America dominated the global simulators market with the largest revenue share of 46.2% in 2024.

- The simulators market in the U.S. led North America, with the largest revenue share in 2024.

- By solution, the products segment led the market, holding the largest revenue share of 66.5% in 2024.

- By type, the airborne segment held a dominant market position, with a revenue share of 55.5% in 2024.

- By end use, the healthcare segment is expected to grow at the fastest CAGR of 10.7% from 2025 to 2033.

Market Size & Forecast

- 2024 Market Size: USD 13.03 Billion

- 2033 Projected Market Size: USD 25.16 Billion

- CAGR (2025-2033): 7.4%

- North America: Largest market in 2024

- Asia Pacific: Fastest growing market

The simulator industry is rapidly evolving through the integration of VR and AR, offering highly realistic and immersive training environments. These technologies allow users to practice critical tasks in simulated environments that closely mimic real-world scenarios. This reduces the risk and cost associated with live training while enhancing learning retention and engagement. Industries like aviation, defense, and medical training are key adopters of immersive simulators. The growing accessibility of VR/AR hardware and software continues to be a major boost for the simulator market.The rise of cloud computing is pushing the Simulator industry toward Simulation-as-a-Service (SaaS) delivery models. Organizations now have scalable, subscription-based access to advanced simulation tools without high infrastructure investments. This flexibility is ideal for industries with remote teams or distributed operations such as healthcare and aviation. SaaS platforms also allow real-time updates, collaboration, and integration with analytics dashboards. The SaaS trend is driving widespread adoption and democratizing simulation training across the enterprise and educational sectors.

")

The automotive sector is driving growth in the simulator market by using advanced simulation tools for testing autonomous vehicles and ADAS features. These simulations offer a safe and cost-effective alternative to real-world testing, especially for complex edge cases and weather scenarios. Virtual environments can replicate millions of miles of driving conditions without physical wear or risk. Regulatory bodies are also encouraging simulation-based testing to accelerate innovation timelines. This trend is vital to the development of next-gen mobility and intelligent transportation systems.

The simulator industry is expanding in manufacturing, oil & gas, and utilities due to the need for safe, skilled workforce training. Industrial simulators support operator training, process optimization, and hazardous scenario handling in controlled virtual setups. They reduce downtime and improve safety compliance while offering real-time feedback for continuous improvement. Remote and VR-enabled simulations are becoming essential as these sectors face workforce shortages and high safety risks. This trend is closely tied to broader digital transformation and Industry 4.0 adoption.

Hybrid simulation is emerging as a major trend in the market, combining live (real actors), virtual (VR/AR), and constructive (computer-generated) elements. This approach delivers holistic training that mirrors complex, real-world conditions with greater flexibility. It is particularly valuable in defense, emergency services, and aviation, where interoperability and coordination are crucial. Hybrid models allow simultaneous training of multiple teams across platforms and geographies. As complexity in operations increases, demand for integrated, multi-domain hybrid simulation is accelerating.

Solution Insights

The products segment dominated the simulators market with a revenue share of over 66% in 2024, driven by strong demand for high-fidelity hardware systems in aviation, defense, and automotive training. These systems offer realistic, hands-on experiences essential for mission-critical applications like pilot certification and combat preparation. However, the growth rate is moderate as organizations increasingly adopt software-based and cloud-delivered simulation models for flexibility and cost savings. Still, the Simulator industry continues to see steady investment in advanced hardware simulators where tactile realism and regulatory compliance are crucial.

The services segment is expected to register the fastest CAGR of over 10% from 2025-2033, driven by the rising demand for simulation maintenance, upgrades, and training support. Organizations are increasingly turning to managed and cloud-based services to reduce capital expenditure and enhance scalability. This shift enables continuous updates, remote accessibility, and integration with analytics and AI-based feedback systems. As training requirements become more dynamic and distributed, the Simulator industry is evolving toward service-centric models that offer greater flexibility and efficiency. This trend is especially prominent in sectors like healthcare, aviation, and corporate training, where real-time support and customization are critical.

Type Insights

The airborne segment dominated the market in 2024, primarily driven by high demand for pilot training and flight simulation across both military and commercial aviation sectors. Flight simulators offer a cost-effective and safe alternative to live flight training, helping reduce operational risks and fuel expenses. The segment is also benefiting from advancements in motion platforms, VR integration, and regulatory requirements for recurrent training. However, growth is becoming more moderate, as many countries and major airlines have already made substantial simulator investments. Still, the Simulator industry continues to prioritize innovation in airborne simulation to support next-gen aircraft, UAV pilot training, and multi-aircraft coordination.

The marine segment is expected to grow at the fastest CAGR in the coming years, driven by increasing demand for maritime safety, navigation, and operational training. As global trade expands and naval modernization accelerates, ship operators, coast guards, and defense forces are investing in advanced simulation solutions. These simulators replicate real-world marine conditions such as rough seas, port operations, and emergency scenarios, enhancing crew readiness and reducing risks. The adoption of simulation is also supported by stringent maritime regulations and the need for compliance training. As a result, the Simulator industry is increasingly focusing on developing high-fidelity marine simulators for both commercial shipping and naval defense applications.

Application Insights

The commercial training segment dominated the simulators industry in 2024, fueled by the rising need for skilled professionals across aviation, healthcare, automotive, and industrial sectors. Organizations are adopting simulators to reduce training costs, enhance learner safety, and improve operational efficiency. The demand is especially high in aviation for pilot and crew training, and in healthcare for surgical and emergency response simulations. Digital transformation and workforce upskilling initiatives are further accelerating the shift toward simulation-based learning. As a result, the Simulator industry is expanding its offerings to cater to a broader range of commercial applications with scalable, cloud-based, and immersive training solutions.

The military training segment is expected to grow at the fastest CAGR over the forecast period, driven by the need for cost-effective, scalable, and realistic mission preparedness. Armed forces worldwide are investing in high-fidelity simulators for air, land, sea, and cyber warfare to reduce reliance on live drills and enhance combat readiness. These simulations allow for repeatable, complex scenario training while minimizing risk, resource use, and environmental impact. The segment is also seeing strong momentum from multi-domain and joint force training programs that require integrated, networked simulation environments. As global defense modernization intensifies, the industry continues to innovate in virtual combat, tactical decision-making, and AI-enhanced military training platforms.

End-use Insights

The aerospace & defense segment dominated the market in 2024, and the increasing demand for mission-critical training and operational efficiency is driving growth in the aerospace & defense segment of the simulators market. Military and aerospace organizations are turning to high-fidelity simulators to enhance pilot readiness, reduce training costs, and minimize risks associated with live exercises. These simulators support complex combat, navigation, and equipment handling scenarios across air, land, and sea domains. The rise of multi-domain warfare, unmanned systems, and joint force training further amplifies the need for advanced simulation capabilities.

The healthcare segment is expected to grow at the fastest CAGR in the forthcoming years, driven by the increasing demand for realistic medical training solutions. Simulation-based training is being widely adopted in medical schools, hospitals, and research institutions to enhance clinical skills without risking patient safety. High-fidelity mannequins, AR/VR-based surgical simulators, and virtual patient platforms are gaining traction for hands-on practice and emergency response training. Moreover, the integration of AI and real-time feedback systems is revolutionizing medical education by improving accuracy, decision-making, and procedural efficiency.

Technique Insights

The virtual segment dominated the market for simulators in 2024, driven by increasing demand for immersive, flexible, and cost-efficient training environments. Virtual simulators replicate real-world scenarios using computer-generated 3D environments, eliminating the need for expensive physical setups. This segment is gaining strong traction in aviation, healthcare, automotive, and defense for skill-based training and remote learning. The integration of VR headsets, haptics, and AI is further enhancing the realism and adaptability of virtual simulations. As organizations prioritize safety, scalability, and efficiency, the Simulator industry is heavily investing in expanding and refining virtual training platforms.

The constructive segment is expected to grow at the fastest CAGR from 2025 to 2033, owing to its ability to replicate large-scale and complex operational scenarios. The constructive segment is gaining strong traction in the market. It is especially useful in military command, control training, and strategic decision-making exercises where human participants are minimal, but scenario depth is high. The segment supports mission planning and wargaming by simulating multiple variables like terrain, logistics, and adversary actions. As multi-domain operations become more critical, the Simulator industry is advancing constructive simulation technologies with AI and networked systems to meet evolving defense and emergency training needs.

Regional Insights

The North America simulators market dominated with the largest revenue share of over 46.0% in 2024, driven by advanced defense programs, a large aviation sector, and expanding healthcare needs. The region is rapidly adopting AI, VR, and cloud technologies to modernize training systems. Simulation is also playing a growing role in industrial safety and remote workforce development. High government and private sector investments continue to fuel innovation across sectors.

U.S. Simulators Market Trends

The U.S. simulators industry dominated with the largest revenue share of over 65% in 2024, backed by strong military spending, FAA-mandated pilot training, and advanced medical education infrastructure. Simulators are widely used across defense, aviation, and healthcare to reduce risk and cost while enhancing training quality. There’s a growing focus on immersive technologies like AR/VR and real-time analytics for performance assessment. Public and private initiatives are accelerating the shift toward integrated digital training ecosystems..

Europe Simulators Market Trends

The Europe simulators industry is expected to grow at a CAGR of 5.8% from 2025 to 2033, as governments modernize defense capabilities and industries embrace simulation for efficiency and safety. Aviation and healthcare remain key sectors, with rising demand for compliance-based and procedural training. EU-wide digital transformation strategies are encouraging cross-border collaboration in simulation technology development. The focus on sustainability and cost optimization is also driving the adoption of virtual and constructive training tools.

The simulators market in Germany is expected to grow at a significant CAGR over the forecast period. It is advancing its use of simulation in engineering, automotive, and aerospace sectors to support precision testing and operator training. The country’s focus on automation and Industry 4.0 is accelerating the use of virtual training systems in manufacturing and logistics. Military modernization programs are also contributing to increased simulator procurement. Simulation is increasingly used to improve workforce skills and reduce operational risks.

The UK simulators market is expected to grow at a significant rate in the coming years. The demand is rising in military, aviation, and medical training, supported by both public funding and private investments. Hybrid training models are gaining popularity across flight schools, defense academies, and hospitals. Virtual learning platforms are being integrated into mainstream education and professional development programs. National efforts to enhance defense readiness and healthcare innovation are key growth drivers.

Asia Pacific Simulators Market Trends

The Asia Pacific simulators industry is expected to grow at the fastest CAGR of 11.9% from 2025 to 2033, owing to rising defense budgets, a booming civil aviation sector, and expanding medical education infrastructure. Countries like India, South Korea, and Australia are scaling their training capabilities with immersive and remote simulation tools. Demand is also growing in industrial sectors for safety training and digital upskilling. Government-backed digital learning and smart training initiatives are fueling widespread adoption.

The China simulators market is rapidly scaling its use of simulation across military, aviation, and healthcare domains as part of its national modernization agenda. Investments are focused on expanding pilot training capacity, medical education, and emergency preparedness. The integration of AI, 5G, and cloud infrastructure is enabling more advanced, networked simulation environments. Domestic technology development and government mandates are accelerating the shift to digital training platforms.

The simulators market in Japan is expanding simulator use in response to workforce challenges, disaster response training, and healthcare precision needs. Automotive and robotics sectors are also leveraging simulation for R&D and operational optimization. Demand for high-accuracy training is rising in hospitals, energy plants, and transport systems. Digital transformation efforts and an aging population are driving the need for efficient, scalable training solutions.

Key Simulators Company Insights

Some of the key players operating in the market include CAE Inc. and L3Harris Technologies, Inc.

-

CAE Inc. is a global leader in simulation and training solutions for the civil aviation, defense, and healthcare sectors. The company provides comprehensive pilot training, synthetic training environments, and mission support systems. Its advanced full-flight simulators and virtual training platforms are widely adopted by military forces and airlines globally. CAE’s strong market presence and deep R&D investment solidify its role as a dominant player in the simulators market.

-

L3Harris Technologies is a major U.S.-based defense contractor that specializes in training and simulation systems for air, land, and sea domains. The company offers high-fidelity simulators, mission rehearsal systems, and immersive training environments. Its solutions are extensively used by military forces, especially in flight and tactical training operations. L3Harris's integration of AI and data analytics enhances its training systems, reinforcing its leadership in next-gen defense simulation.

Simlat Ltd. and VSTEP B.V. are some of the emerging participants in the simulators market.

-

Simlat Ltd., headquartered in Israel, is an emerging leader in Unmanned Aerial Systems (UAS) training simulation. It provides simulation platforms tailored for UAS operators in both defense and commercial sectors. The company’s software is known for its flexibility and integration with various drone models and mission types. As the demand for UAS training grows, Simlat is positioned to expand its footprint significantly in the simulation market.

-

VSTEP B.V., based in the Netherlands, specializes in maritime simulation and training systems. It offers innovative products like NAUTIS, a ship bridge simulator used for training ship crews, ports, and naval units. VSTEP’s systems are known for realism, cost-effectiveness, and modularity, catering to both civilian and military maritime markets. With the rise in global maritime activity and digital transformation, VSTEP is emerging as a promising player in this niche segment.

Key Simulators Companies:

The following are the leading companies in the simulators market. These companies collectively hold the largest market share and dictate industry trends.

- CAE Inc.

- L3Harris Technologies, Inc.

- Thales Group

- Saab AB

- Rheinmetall AG

- Elbit Systems Ltd.

- FlightSafety International Inc.

- General Dynamics Corporation

- Kongsberg Gruppen ASA

- TRU Simulation + Training Inc.

- RUAG AG

- Indra Sistemas S.A.

Recent Developments

-

In June 2025, Reiser Simulation and Training GmbH (Reiser) and European Heli Center (EHC) announced the commencement of their project with the first meeting held at Berg, Bavaria. The project aims to bring a H135/H145 Level D full-flight simulator to Lelystad Airport, near Amsterdam, in EHC’s planned training center.

-

In April 2025, Airbus, one of the key aircraft manufacturers, announced its commitment to delivering full-flight H160/H175 simulators, designed for training, to Brazil in 2028. These simulators feature Level D training capabilities and are specifically dedicated to addressing the energy sector's training needs in Latin America.

-

In March 2025, TRU Simulation + Training Inc., a subsidiary of Textron Inc., announced that the Naval Air Warfare Center's Training Systems Division (NAWCTSD) had accepted its first Unit Training Device (UTD) simulators as part of the contract associated with the Ground-Based Training System (GBTS).

-

In March 2025, Performance Drone Works (PDW), a drone technology company and manufacturer of C100 Group 2 small UAS, announced the launch of its latest flight simulator, PDW SIM, specifically designed for tactical drone training. This is expected to strengthen its market position in the small robotics category associated with military applications.

Simulators Market Report Scope

Report Attribute

Details

Market size value in 2025

USD 14.16 billion

Revenue forecast in 2033

USD 25.16 billion

Growth rate

CAGR of 7.4% from 2025 to 2033

Base year of estimation

2024

Actual data

2021 - 2023

Forecast period

2025 - 2033

Quantitative units

Revenue in USD million/billion, and CAGR from 2025 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Solution, type, application, technique, end-use, region

Regional scope

North America; Europe; Asia Pacific; Latin America; Middle East & Africa

Country scope

U.S.; Canada; Mexico; Germany; UK; France; China; Japan; India; South Korea; Australia; Brazil; UAE; Saudi Arabia; South Africa

Key companies profiled

CAE Inc.; L3Harris Technologies, Inc.; Thales Group; Saab AB; Rheinmetall AG; Elbit Systems Ltd.; FlightSafety International Inc.; General Dynamics Corporation; Kongsberg Gruppen ASA; TRU Simulation + Training Inc.; RUAG AG; Indra Sistemas S.A.

Customization scope

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Simulators Market Report Segmentation

This report forecasts revenue growth at the global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global simulators market report based on solution, type, application, technique, end-use, and region:

-

Solution Outlook (Revenue, USD Million, 2021 - 2033)

-

Products

-

Services

-

-

Type Outlook (Revenue, USD Million, 2021 - 2033)

-

Airborne

-

Ground

-

Marine

-

-

Application Outlook (Revenue, USD Million, 2021 - 2033)

-

Commercial Training

-

Military Training

-

-

Technique Outlook (Revenue, USD Million, 2021 - 2033)

-

Live

-

Virtual

-

Constructive

-

Hybrid

-

-

End-use Outlook (Revenue, USD Million, 2021 - 2033)

-

Aerospace & Defense

-

Manufacturing

-

Oil & Gas

-

Healthcare

-

Automotive

-

Electrical & Electronics

-

Others

-

-

Regional Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

France

-

-

Asia Pacific

-

China

-

Japan

-

India

-

South Korea

-

Australia

-

-

Latin America

-

Brazil

-

-

Middle East and Africa (MEA)

-

UAE

-

Saudi Arabia

-

South Africa

-

-

Frequently Asked Questions About This Report

The global simulators market size was estimated at USD 13.03 billion in 2024 and is expected to reach USD 14.2 billion in 2025

The global simulators market is expected to grow at a compound annual growth rate of 7.4% from 2025 to 2033 to reach USD 25.16 billion by 2033.

North America dominated the simulators market with a share of 46.2% in 2024, driven by the region's strong presence of defense contractors, advanced training infrastructure, and increased adoption of simulation technologies across aviation and healthcare sectors.

Some key players operating in the simulators market include CAE Inc., L3Harris Technologies, Inc., Thales Group, Saab AB, Rheinmetall AG, Elbit Systems Ltd., FlightSafety International Inc., General Dynamics Corporation, Kongsberg Gruppen ASA, TRU Simulation + Training Inc., RUAG AG, and Indra Sistemas S.A.

Key factors that are driving the market growth include rising demand for cost-effective and risk-free training solutions, increasing use of simulation in military and aviation sectors, and growing adoption of virtual and augmented reality technologies.

About the Author(s)

Next Generation Technologies Research Team

Technology · Next Generation TechnologiesThis report was authored by the next generation technologies research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the next generation technologies segment of the technology industry. All findings are based on proprietary technology databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.