- Home

- »

- Next Generation Technologies

- »

-

Generative AI Server Market Size & Share Report 2026-2033GVR Report cover

![Generative AI Server Market (2026 - 2033)Report]()

Generative AI Server Market (2026 - 2033)

Size, Share & Trends Analysis Report By Processor Type, By Function (Unit Testing, System Testing), By Form Factor, By Deployment Mode (On-Premises, Cloud), By Organization Size, By Application, By End-user, By Region, And Segment Forecasts

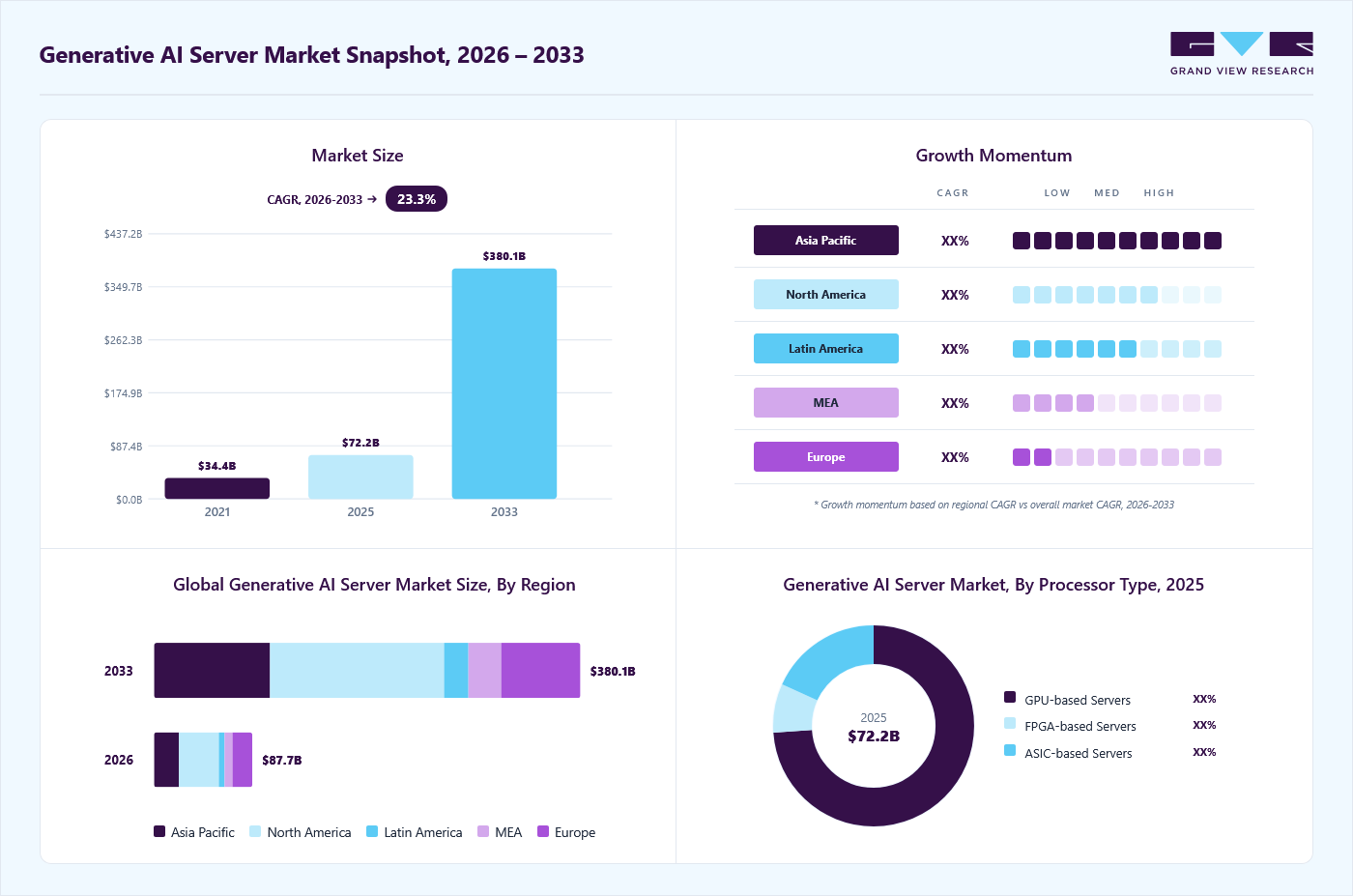

Market Size, 2025

$72.2BMarket Estimate, 2026

$87.7BMarket Forecast, 2033

$380.1BCAGR, 2026–2033

23.3%Generative AI Server Market Summary

The global generative AI server market size was valued at USD 72.2 billion in 2025 and is projected to grow from USD 87.7 billion in 2026 to USD 380.1 billion by 2033, at a CAGR of 23.3% from 2026 to 2033. The market in North America dominated with a revenue share of 40.5% in 2025. The market is witnessing rapid expansion, driven by the surge in demand for large language models (LLMs), multimodal AI systems, and AI-powered content generation across industries.

Key Market Trends & Insights

- By processor type: GPU-based servers segment held the largest market share of 73.9% in 2025.

- By form factor: Rack-mounted servers segment held the largest market share in 2025.

- By application: Content generation segment held the largest market share in 2025.

- By end-user: Media & entertainment segment held the largest market share in 2025.

- By deployment: Cloud segment held the largest market share in 2025.

Regional Highlights

- Largest regional market: North America (40.5% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

- By country: The U.S. held the largest market share in 2025

Market Size & Forecast

- Market size in 2025: USD 72.2 Billion

- Estimated market size in 2026: USD 87.7 Billion

- Projected market size by 2033: USD 380.1 Billion

- CAGR (2026-2033): 23.3%

These servers form the backbone of generative AI infrastructure, enabling high-performance training and inference workloads through advanced GPUs, accelerators, and high-bandwidth memory architectures. The market is currently in a high-growth phase, supported by significant capital investments from hyperscalers and enterprises to build scalable AI infrastructure.Growth is primarily fueled by increasing adoption of generative AI applications such as content generation, virtual assistants, recommendation systems, and computer vision, along with the expanding cloud services market, which enables scalable computing infrastructure, high-performance data processing, and efficient deployment of AI workloads. Industries including media & entertainment, BFSI, healthcare, and IT & telecom are leading adoption due to the high value derived from automation, personalization, data-driven decision-making, and cloud-based AI integration capabilities.

")

GPU-based servers currently dominate the market owing to their flexibility and strong ecosystem support, particularly for training large models. However, ASIC-based servers are expected to witness the fastest growth over the forecast period due to their efficiency advantages in inference workloads. In terms of form factor, rack-mounted servers account for the largest share due to their widespread use in hyperscale data centers, while blade servers are gaining momentum as organizations prioritize higher density and modularity.

Consequently, the market is expected to grow at a strong CAGR through 2033, slightly outpacing the broader AI server market in the near term. The penetration of generative AI workloads within total AI infrastructure will continue to rise, although growth will gradually stabilize as non-generative AI applications expand and efficiency improvements reduce compute intensity. Overall, the market is transitioning from an early, hype-driven expansion phase to a more balanced and diversified growth trajectory, with generative AI remaining a central driver of global AI infrastructure investments.

Processor Type Insights

The GPU-based servers segment dominated the market, accounting for a 73.9% revenue share in 2025 due to its superior ability to handle highly parallel and computing-intensive workloads required for training and running large generative AI models. GPUs are specifically designed for massive matrix operations and high-bandwidth memory processing, making them far more efficient than other processor types for large language models and multimodal AI systems. In addition, the strong software ecosystem and widespread developer support enable faster deployment and scaling of generative AI infrastructure across enterprises and hyperscale data centers. For instance, in September 2025, Edgecore Networks launched the AGS8600 high-performance GPU AI server designed for AI and HPC workloads, highlighting the industry’s focus on building GPU-dense systems optimized for generative AI applications. This reflects the broader trend of server vendors accelerating innovation in GPU-based infrastructure to support rising demand for model training and inference at scale. Overall, the combination of performance advantages, ecosystem maturity, and continuous hardware innovation has firmly established GPU-based servers as the dominant market segment.

The ASIC-based servers segment is expected to grow at the fastest CAGR in the market due to their higher energy efficiency, lower cost per compute, and optimization for large-scale AI inference workloads. As generative AI adoption scales, hyperscalers are increasingly shifting toward custom silicon to reduce dependence on GPU-intensive infrastructure and improve performance per watt. For instance, in February 2026, Molex introduced its Impress co-packaged copper solutions designed to enable high-speed, near-ASIC connectivity for next-generation AI systems, supporting ultra-high data rates and improved signal integrity in AI data centers. This reflects the broader industry shift toward ASIC-centric architectures to meet escalating generative AI compute and networking demands.

Function Insights

The unit testing segment dominated the market by function, accounting for the largest revenue share in 2025, due to its high frequency of execution and strong reliance on automation for validating code and model outputs during AI-driven development cycles. Generative AI is widely used to automatically generate test cases, validate code behavior, and improve software quality, which makes unit testing the most consistently utilized workload across development pipelines. Its dominance is further supported by enterprise adoption of AI-assisted software development practices, where unit testing is integrated into continuous integration and continuous deployment (CI/CD) workflows. This leads to significantly higher usage volume compared to other testing stages, such as system or user acceptance testing, thereby driving greater demand for underlying AI compute infrastructure and server resources.

The integration testing segment is expected to grow at a significant CAGR over the forecast period due to the rapid expansion of complex, interconnected software ecosystems built on microservices, APIs, and cloud-native architectures. As modern applications increasingly rely on multiple third-party services and distributed components, ensuring seamless interaction between systems has become more critical and challenging, driving strong demand for advanced testing solutions. Generative AI is significantly enhancing integration testing by automating test scenario generation, simulating real-world system interactions, and identifying interface-level inconsistencies that are difficult to detect through traditional testing methods. In addition, enterprises are accelerating digital transformation initiatives across industries such as BFSI, healthcare, retail, and IT services, further increasing the need for robust integration validation before deployment. The adoption of CI/CD pipelines and DevOps practices is also amplifying the frequency of integration testing cycles, requiring scalable and intelligent automation tools powered by generative AI. As a result, the segment is expected to witness sustained high growth, supported by the rising complexity of software environments and the need for faster, more reliable end-to-end system validation.

Form Factor Insights

The rack-mounted servers segment dominated the market in 2025 due to its superior ability to support high-density GPU configurations, scalable compute architectures, and efficient thermal management required for large-scale AI training and inference workloads. In addition, rack-mounted systems are widely adopted in hyperscale data centers and enterprise environments because they offer flexibility, easier maintenance, and seamless integration with existing IT infrastructure, making them the preferred form factor for generative AI deployments. Another key driver is the increasing focus of server vendors on developing optimized rack-based AI infrastructure to meet the rising computational demands of generative AI applications. For instance, in June 2024, Advantech’s launch of edge AI server solutions designed for generative AI workloads, the company emphasized rack-optimized architectures capable of supporting high-performance computing requirements for artificial intelligence (AI) and HPC applications. This reflects the broader industry trend of accelerating innovation in rack-mounted systems to enhance scalability and efficiency in AI-driven data centers. Overall, these advantages have firmly established rack-mounted servers as the dominant form factor in the market.

The blade servers segment is expected to grow at the fastest CAGR over the forecast period due to its high-density computing design, modular architecture, and strong suitability for GPU-accelerated AI and HPC workloads. Blade servers enable organizations to scale compute resources efficiently within a compact footprint while optimizing power consumption, cooling efficiency, and interconnect performance, making them increasingly relevant for generative AI training and distributed inference environments. For instance, in August 2025, Gigabyte highlighted advancements in its blade server platforms designed for high-performance computing and AI workloads, reflecting the industry’s push toward more modular and scalable infrastructure solutions for next-generation AI applications. This aligns with the broader trend of data center operators adopting blade-based architectures to support growing generative AI demands. Overall, the combination of scalability, efficiency, and optimized performance is driving the strong CAGR growth of blade servers in the market.

Deployment Mode Insights

The cloud segment dominated the generative AI server industry in 2025, accounting for the largest revenue share, driven by its scalability, elastic compute access, and ability to support large-scale training and inference of generative AI models without requiring heavy upfront infrastructure investment. Cloud platforms enable organizations to rapidly scale GPU-intensive workloads, optimize resource utilization, and accelerate the deployment of AI applications, making them the preferred choice for enterprises and hyperscalers adopting generative AI. For instance, in May 2025, Red Hat highlighted enhancements to its AI Inference Server designed to enable generative AI deployment across hybrid cloud environments, supporting any model on any accelerator across diverse cloud infrastructures. This reflects the broader industry trend of cloud providers and ecosystem players strengthening support for flexible, scalable AI workloads. Overall, these advantages have reinforced the cloud’s dominance in the market as the primary deployment mode.

The on-premises segment is expected to grow at the fastest CAGR during the forecast period due to increasing demand from enterprises for greater control over data, enhanced security, and compliance with stringent regulatory requirements. As generative AI workloads become more deeply integrated into critical business functions, organizations in sectors such as BFSI, healthcare, and government are prioritizing on-premises deployments to ensure data sovereignty, reduce dependency on external cloud providers, and manage sensitive information within secure internal environments. In addition, on-premises infrastructure is gaining traction as enterprises seek to optimize long-term costs associated with large-scale AI inference and continuous model usage. This deployment model also offers improved latency performance and greater customization flexibility for organization-specific AI applications. Overall, the combination of regulatory pressure, data security concerns, and cost optimization needs is expected to drive the fastest market growth.

Organization Size Insights

Large enterprises dominated the market in 2025 primarily because they possess the financial capacity, scalable digital infrastructure, and strategic urgency to deploy AI at enterprise-wide scale. These organizations also benefit from large proprietary datasets, strong cloud adoption, and the ability to integrate generative AI into core business functions such as customer engagement, software development, and decision-making workflows, which significantly boosts productivity and revenue potential. In addition, their early-mover advantage and access to advanced AI talent and partnerships with hyperscalers further reinforce their dominant market share in AI investments. A key accelerating driver is the rising need for AI-driven infrastructure resilience and compute scalability, as enterprises increasingly require high-performance systems to support growing generative AI workloads. For instance, in March 2026, the launch of rack-adjacent HVDC technology aimed at securing AI power sovereignty highlights how enterprise-scale AI adoption is directly driving demand for advanced, reliable, and energy-efficient infrastructure capable of sustaining large generative AI deployments at scale. This convergence of enterprise investment strength and supporting infrastructure innovation explains why large enterprises accounted for the largest revenue share in the generative AI market in 2025, and this dominance is expected to continue as AI becomes central to enterprise digital transformation.

The SMEs segment is projected to register the fastest CAGR during the forecast period mainly because generative AI solutions are becoming more affordable, accessible, and purpose-built for resource-constrained businesses, enabling SMEs to adopt advanced capabilities that were earlier limited to large enterprises. SMEs are rapidly embracing AI to improve productivity, automate repetitive tasks, enhance customer engagement, and reduce dependency on large skilled teams, which significantly boosts operational efficiency and competitiveness. In addition, the rise of plug-and-play and “AI-in-a-box” solutions are removing traditional barriers such as high infrastructure costs, technical complexity, and long deployment cycles, making AI adoption much easier for smaller firms. For instance, in April 2025, PRE Security unveiled its GenAI EDR and MiniSOC “SOC-in-a-box” solution, specifically designed for SMEs and MSSPs, delivering enterprise-grade AI-driven cybersecurity capabilities in a compact, scalable, and cost-efficient format that eliminates the need for expensive GPU-heavy infrastructure and enables rapid deployment of advanced security operations. This reflects how vendors are increasingly tailoring generative AI offerings for SMEs, accelerating adoption across this segment. Overall, the combination of affordability, ease of deployment, and high operational value is driving SMEs to adopt generative AI at the fastest rate, resulting in the highest CAGR during the forecast period.

Application Insights

Content generation dominated the market in 2025 by application segment primarily because it is the most widely applicable and immediately monetizable use case of generative AI across industries, including marketing, media, e-commerce, education, and corporate communications. Organizations are increasingly leveraging AI to produce high volumes of text, images, videos, and personalized marketing content at scale, which significantly reduces time, cost, and dependency on manual creative resources. In addition, the growing demand for hyper-personalization and real-time content delivery across digital platforms has further strengthened adoption, making content generation a core entry point for enterprise AI deployment. A strong supporting driver is the rapid integration of generative AI into existing productivity and creative tools, enabling seamless content creation workflows without requiring major infrastructure changes. Overall, its versatility, cost efficiency, and strong demand across multiple end-use industries have made content generation the dominant market segment.

The marketing & advertising segment is projected to register the fastest CAGR during the forecast period primarily due to the rapid shift toward hyper-personalized, data-driven, and real-time campaign execution, where generative AI significantly enhances customer targeting, content creation, and campaign optimization. Marketers are increasingly adopting AI tools to generate tailored advertisements, automate creative design, and optimize messaging across multiple digital channels, which improves engagement rates while substantially reducing time-to-market and operational costs. In addition, the growing dominance of digital platforms and performance-based advertising models is accelerating the need for scalable content generation and continuous audience personalization, further fueling AI adoption in this segment. A key driving factor is also the increasing pressure on brands to maximize ROI from advertising spend by leveraging predictive insights and automated decision-making capabilities offered by generative AI. Consequently, the combination of personalization demand, efficiency gains, and digital advertising expansion is driving the marketing & advertising segment to register the fastest CAGR during the forecast period.

End-user Insights

The media & entertainment segment dominated the market by end user primarily because this industry generates and processes extremely large volumes of high-resolution, data-intensive content, such as 4K-12K video, visual effects, streaming assets, and real-time graphics, all of which require high-performance AI servers for rendering, editing, indexing, and content optimization. In addition, media workflows are increasingly being transformed by generative AI for tasks such as automated editing, video summarization, localization, and real-time content creation, which significantly increase compute and storage demands across production pipelines. The sector also benefits from strong AI integration across the entire content lifecycle from creation to distribution, making it one of the earliest and most aggressive adopters of AI-driven infrastructure.

For instance, in April 2026, PROMISE Technology highlighted AI-optimized storage and high-performance infrastructure solutions at NAB Show 2026, emphasizing how media and entertainment workflows are being driven by ultra-high-resolution formats, generative AI tools, and cloud collaboration needs that require low-latency, high-throughput server and storage systems to support real-time production environments. This reflects that AI-powered production ecosystems are becoming central to the industry, with broadcasters, studios, and streaming platforms increasingly relying on AI-optimized servers to handle editing, indexing, and content delivery on scale. Overall, the combination of massive data workloads and deep AI integration across creative workflows has made media & entertainment the dominant end-user segment.

The healthcare segment is projected to be the fastest-growing segment from 2026 to 2033, primarily due to the rapid convergence of generative AI, advanced computing infrastructure, and increasing demand for precision, data-driven clinical decision-making across the healthcare ecosystem. Healthcare organizations are increasingly adopting generative AI for applications such as medical imaging analysis, clinical documentation, drug discovery, and personalized treatment planning, all of which significantly improve diagnostic accuracy, operational efficiency, and patient outcomes.

In addition, the availability of secure, HIPAA-compliant AI platforms, foundation models, and high-performance computing environments is reducing traditional barriers such as data privacy concerns, limited computational resources, and a lack of AI expertise, thereby accelerating adoption in this sector. A key driving factor is the growing integration of AI-accelerated infrastructure and foundation models specifically designed for medical imaging and clinical workflows, which enables faster development and deployment of healthcare-grade AI solutions.

For instance, in March 2026, HOPPR AI Foundry expanded its medical imaging AI capabilities using NVIDIA accelerated computing and foundation models, enabling developers to build, fine-tune, and deploy advanced imaging AI systems within a secure, compliant environment while also generating synthetic medical imaging data and improving diagnostic reasoning workflows. Overall, the combination of strong clinical demand, rapid advancements in AI-enabled medical imaging and diagnostics, supportive regulatory-compliant infrastructure, and increasing investment in healthcare AI ecosystems is driving the healthcare segment to register the fastest CAGR during the forecast period from 2026 to 2033.

Regional Insights

The generative AI server market in North America dominated the global market with the largest revenue share of 40.5% in 2025, primarily due to the region’s early and large-scale adoption of AI technologies, strong hyperscaler ecosystem, and concentration of leading AI and cloud infrastructure providers. The presence of major technology companies and cloud service providers enables the rapid deployment of high-performance AI servers across enterprises, driving significant infrastructure demand. In addition, North America benefits from substantial investments in AI data centers, advanced semiconductor availability, and strong R&D capabilities, which collectively accelerate generative AI server adoption across industries such as IT, BFSI, healthcare, and media & entertainment. The region also has a highly mature digital economy and a strong enterprise base that prioritizes AI-driven automation, analytics, and content generation, further boosting server demand. Moreover, supportive government initiatives and private-sector funding for AI innovation continue to strengthen the region’s leadership position. Overall, North America’s dominance is driven by its advanced digital infrastructure, strong cloud and AI ecosystem, high enterprise AI penetration, and continuous investment in next-generation computing capabilities, making it the largest revenue-generating region.

U.S. Generative AI Server Market Trends

The generative AI server market in the U.S. is expected to grow significantly at a strong CAGR from 2025 to 2033, primarily due to the rapid expansion of AI workloads, increasing deployment of large-scale foundation models, and continuous investment in hyperscale data center infrastructure. U.S. enterprises across industries such as cloud computing, BFSI, healthcare, media & entertainment, and retail are aggressively adopting generative AI, which is driving sustained demand for high-performance GPU- and AI-optimized servers.

In addition, the presence of leading technology giants and hyperscalers, along with strong semiconductor innovation and advanced cloud ecosystems, is accelerating infrastructure scaling at an unprecedented pace. The growing need for real-time inference, AI training, and edge AI deployments is further strengthening server demand across both enterprise and public sector applications. Moreover, continuous advancements in AI chips, energy-efficient server architectures, and increasing focus on AI data center expansion are expected to further support long-term market growth. Overall, strong enterprise adoption, technological leadership, and large-scale infrastructure investments are driving the robust CAGR of the U.S. generative AI server industry from 2026 to 2033.

Europe Generative AI Server Market Trends

The generative AI server market in Europe is anticipated to register considerable growth from 2026 to 2033, primarily due to the accelerating adoption of AI across enterprises, increasing cloud transformation initiatives, and rising demand for secure and compliant AI infrastructure. Organizations across sectors such as manufacturing, automotive, BFSI, healthcare, and public services are increasingly integrating generative AI to enhance productivity, automate workflows, and improve decision-making, which is driving demand for high-performance AI servers. In addition, Europe’s strong focus on data sovereignty, GDPR compliance, and trusted AI frameworks is encouraging the deployment of localized and regulated AI data centers, further boosting server investments. The region is also witnessing growing investments from hyperscalers and cloud providers in expanding AI infrastructure capacity to meet rising enterprise workloads. Furthermore, government-backed digitalization programs and AI innovation initiatives across major economies such as Germany, the UK, and France are supporting ecosystem development. Overall, the combination of regulatory-driven secure AI adoption, enterprise digital transformation, and expanding cloud and data center infrastructure is expected to drive steady growth.

The UK generative AI server market is expected to register strong growth from 2026 to 2033, primarily due to rapid enterprise adoption of generative AI, expanding cloud and hyperscale data center investments, and rising demand for GPU-accelerated computing infrastructure. Key sectors such as BFSI, healthcare, retail, and media & entertainment are increasingly deploying AI workloads, driving higher demand for scalable and high-performance servers. In addition, the UK’s focus on AI sovereignty, data center expansion, and supportive government initiatives for digital transformation is further strengthening market growth. Overall, strong enterprise adoption, infrastructure expansion, and policy support are driving steady growth through 2033.

The generative AI server market in Germanyis expected to register strong and steady growth from 2026 to 2033, primarily due to the rapid expansion of enterprise AI adoption, a strong industrial automation ecosystem, and increasing investments in AI-ready data center infrastructure. Germany’s leadership in advanced manufacturing, automotive, and engineering is driving high demand for generative AI workloads, particularly for use cases such as design optimization, predictive maintenance, and intelligent automation. In addition, growing emphasis on data sovereignty, EU AI Act compliance, and secure cloud infrastructure is encouraging organizations to deploy localized and regulated AI server environments, further boosting market expansion. The rising participation of hyperscalers and technology providers in building GPU-intensive AI infrastructure is also strengthening server capacity across the country.

Asia Pacific Generative AI Server Market Trends

The generative AI server market in the Asia Pacific held a significant share in 2025 primarily due to rapid digital transformation, strong expansion of cloud infrastructure, and increasing adoption of AI across large enterprise ecosystems. Countries such as China, India, Japan, and South Korea are witnessing widespread deployment of generative AI across sectors including IT & telecom, BFSI, manufacturing, and consumer services, which is driving strong demand for high-performance AI servers.

In addition, the region benefits from large-scale data center investments, cost-effective manufacturing capabilities for hardware, and strong government support for AI innovation and digital economy initiatives, all of which contribute to accelerating AI infrastructure development. The growing presence of hyperscalers and regional cloud providers is also further strengthening server deployment across the region. Overall, Asia Pacific’s combination of rapid enterprise AI adoption, expanding digital infrastructure, and strong government and private-sector investments enabled it to hold a significant share in 2025.

Japan generative AI server market is expected to register strong growth from 2026 to 2033, primarily due to rapid enterprise digital transformation, rising adoption of generative AI across industries, and expanding AI-optimized data center infrastructure. Demand is being driven by sectors such as manufacturing, BFSI, healthcare, and IT services, where organizations are deploying generative AI for automation, predictive analytics, and content generation, significantly increasing the need for GPU-accelerated and high-performance AI servers. In addition, Japan’s focus on digital sovereignty, government-backed AI investments, and development of domestic AI hardware and data centers is further strengthening infrastructure deployment. The market is also supported by increasing hyperscaler investments and the scaling of cloud-based AI computing platforms across the country.

The generative AI server market in China is experiencing rapid expansion and strong long-term growth potential from 2026 to 2033, primarily driven by the country’s massive digital economy, large-scale enterprise AI adoption, and aggressive government support for AI infrastructure development. China’s hyperscalers and technology giants are heavily investing in AI data centers, GPU/ASIC-based server deployments, and domestic semiconductor ecosystems to support rising demand for generative AI applications across industries such as e-commerce, manufacturing, healthcare, and financial services.

This surge is intrinsically linked to the evolution of the cloud services market, which acts as the primary delivery platform for AI-as-a-Service (AIaaS), providing enterprises with the elastic compute power and scalable environments necessary to deploy complex models without massive upfront capital expenditures. In addition, the push for technological self-reliance and data sovereignty is accelerating the shift toward locally developed AI chips and servers, reducing dependency on foreign hardware and strengthening a domestic AI server and cloud ecosystem that ensures long-term operational resilience.

Key Generative AI Server Company Insights

Key players operating in the generative AI server industry are NVIDIA, Dell Technologies, Hewlett-Packard Enterprise (HPE), and Lenovo, among others. Companies are focusing on various strategic initiatives, including new product development, partnerships & collaborations, and agreements to gain a competitive advantage over their rivals. The following are some instances of such initiatives.

-

In March 2026, Microsoft collaborated with NVIDIA to strengthen Azure AI infrastructure and Microsoft Foundry for next-generation generative and physical AI workloads. The focus is on enabling enterprises to build, deploy, and scale AI agents and physical AI systems using NVIDIA-accelerated computing integrated with Azure’s cloud platform, including support for simulation, digital twins, and real-time AI workloads.

-

In March 2026, Google Cloud collaborated with NVIDIA to support large-scale generative AI and “AI factory” workloads. It focuses on the expansion of NVIDIA GPU-powered virtual machines (such as A4 and A4X instances based on Blackwell/GB200 systems), enhanced networking via Google’s AI Hypercomputer architecture, and tightly integrated software stacks for training and inference at scale.

-

In October 2025, Supermicro collaborated with NVIDIA to co-develop next-generation AI servers (Blackwell/GB200/GB300 and Vera Rubin platforms) while strengthening compliance, data integrity, and U.S.-based manufacturing for secure AI infrastructure. This directly supports the market by accelerating high-performance, rack-scale AI factory deployments and sovereign/government-ready AI data centers, increasing demand for compliant, scalable GPU server systems.

Key Generative AI Server Companies:

The following key companies have been profiled for this study on the generative AI server market.

- NVIDIA

- Dell Technologies

- Hewlett Packard Enterprise (HPE)

- Lenovo

- Super Micro Computer (Supermicro)

- Inspur

- Huawei Technologies

- IBM

- Cisco Systems

- Microsoft

- Amazon Web Services (AWS)

- Google Cloud

- Oracle

- Intel

- AMD

Generative AI Server Market Report Scope

Report Attribute

Details

Market size in 2025

USD 72.2 billion

Estimated market size in 2026

USD 87.7 billion

Projected market size by 2033

USD 380.1 billion

Growth rate

CAGR of 23.3% from 2026 to 2033

Actual data

2021 - 2025

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion and CAGR from 2026 to 2033

Report Coverage

Revenue forecast, company share, competitive landscape, growth factors, and trends

Segments covered

Processor type, function, form factor, deployment mode, organization size, application, end-user, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; UK; Germany; France; China; India; Japan; Australia; South Korea; Brazil; UAE; Saudi Arabia; South Africa

Key companies profiled

NVIDIA; Dell Technologies; Hewlett Packard Enterprise (HPE); Lenovo; Super Micro Computer (Supermicro); Inspur; Huawei Technologies; IBM; Cisco Systems; Microsoft; Amazon Web Services (AWS); Google Cloud; Oracle; Intel; AMD

Customization scope

Free report customization (equivalent to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Generative AI Server Market Report Segmentation

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global generative AI server market report based on processor type, function, form factor, deployment mode, organization size, application, end-user, and region:

-

Processor Type Outlook (Revenue, USD Billion, 2021 - 2033)

-

GPU-based Servers

-

FPGA-based Servers

-

ASIC-based Servers

-

-

Function Outlook (Revenue, USD Billion, 2021 - 2033)

-

Unit Testing

-

System Testing

-

Integration Testing

-

User Acceptance Testing (UAT)

-

Others

-

-

Form Factor Outlook (Revenue, USD Billion, 2021 - 2033)

-

Rack-mounted Servers

-

Blade Servers

-

Tower Servers

-

-

Deployment Mode Outlook (Revenue, USD Billion, 2021 - 2033)

-

On-Premises

-

Cloud

-

-

Organization Size Outlook (Revenue, USD Billion, 2021 - 2033)

-

Large Enterprises

-

SMEs

-

-

Application Outlook (Revenue, USD Billion, 2021 - 2033)

-

Content Generation

-

Virtual Assistants/Chatbots

-

Recommendation Systems

-

Computer Vision/Imaging

-

Gaming & VR/AR

-

Healthcare & R&D

-

Marketing & Advertising

-

Others

-

-

End-user Outlook (Revenue, USD Billion, 2021 - 2033)

-

BFSI

-

Healthcare

-

IT & Telecom

-

Retail & E-commerce

-

Media & Entertainment

-

Automotive & Manufacturing

-

Government & Defense

-

Others

-

-

Regional Outlook (Revenue, USD Billion, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

UK

-

Germany

-

France

-

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

Australia

-

-

Latin America

-

Brazil

-

-

Middle East & Africa

-

UAE

-

Saudi Arabia

-

South Africa

-

-

Frequently Asked Questions About This Report

North America dominated with a 40.5% revenue share in 2025.

Asia Pacific is the fastest-growing region over the forecast period.

The cloud segment held the largest revenue share in 2025, while on-premises is the fastest-growing deployment mode.

The rack-mounted servers segment held the largest revenue share in 2025, while blade servers is the fastest-growing form factor.

Content generation segment held the largest share in 2025, while marketing & advertising is the fastest-growing application.

The global generative AI server market size was valued at USD 72.2 billion in 2025 and is estimated at USD 87.7 billion for 2026.

The GPU-based servers segment dominated the generative AI server market with revenue share of 73.9% in 2025 driven by rising demand for high-performance computing infrastructure to support large language models (LLMs), AI training, and real-time inference workloads.

Key players include NVIDIA; Dell Technologies; Hewlett Packard Enterprise (HPE); Lenovo; Super Micro Computer (Supermicro); Inspur; Huawei Technologies; IBM; Cisco Systems; Microsoft; Amazon Web Services (AWS); Google Cloud; Oracle; Intel; AMD.

Factors such as growing adoption of large language models (LLMs), generative AI applications, and AI-powered automation, rapid expansion of hyperscale data centers and cloud-based AI services play a key role in accelerating the generative AI server market.

The global generative AI server market is expected to grow at a CAGR of 23.3% from 2026 to 2033, reaching USD 380.1 billion by 2033.

About the Author(s)

Next Generation Technologies Research Team

Technology · Next Generation TechnologiesThis report was authored by the next generation technologies research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the next generation technologies segment of the technology industry. All findings are based on proprietary technology databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.