- Home

- »

- Clinical Diagnostics

- »

-

Pan-genomic And Multi-gene Panel Testing Market Report, 2025-2033GVR Report cover

![Pan-genomic And Multi-gene Panel Testing Market (2025 - 2033)Report]()

Pan-genomic And Multi-gene Panel Testing Market (2025 - 2033)

Size, Share & Trends Analysis Report By Test, By Application (Oncology, Cardiology & Cardiomyopathy, Reproductive Carrier Screening), By End-use (Independent Diagnostic Labs, Specialty Genomic Centers), By Region, And Segment Forecasts

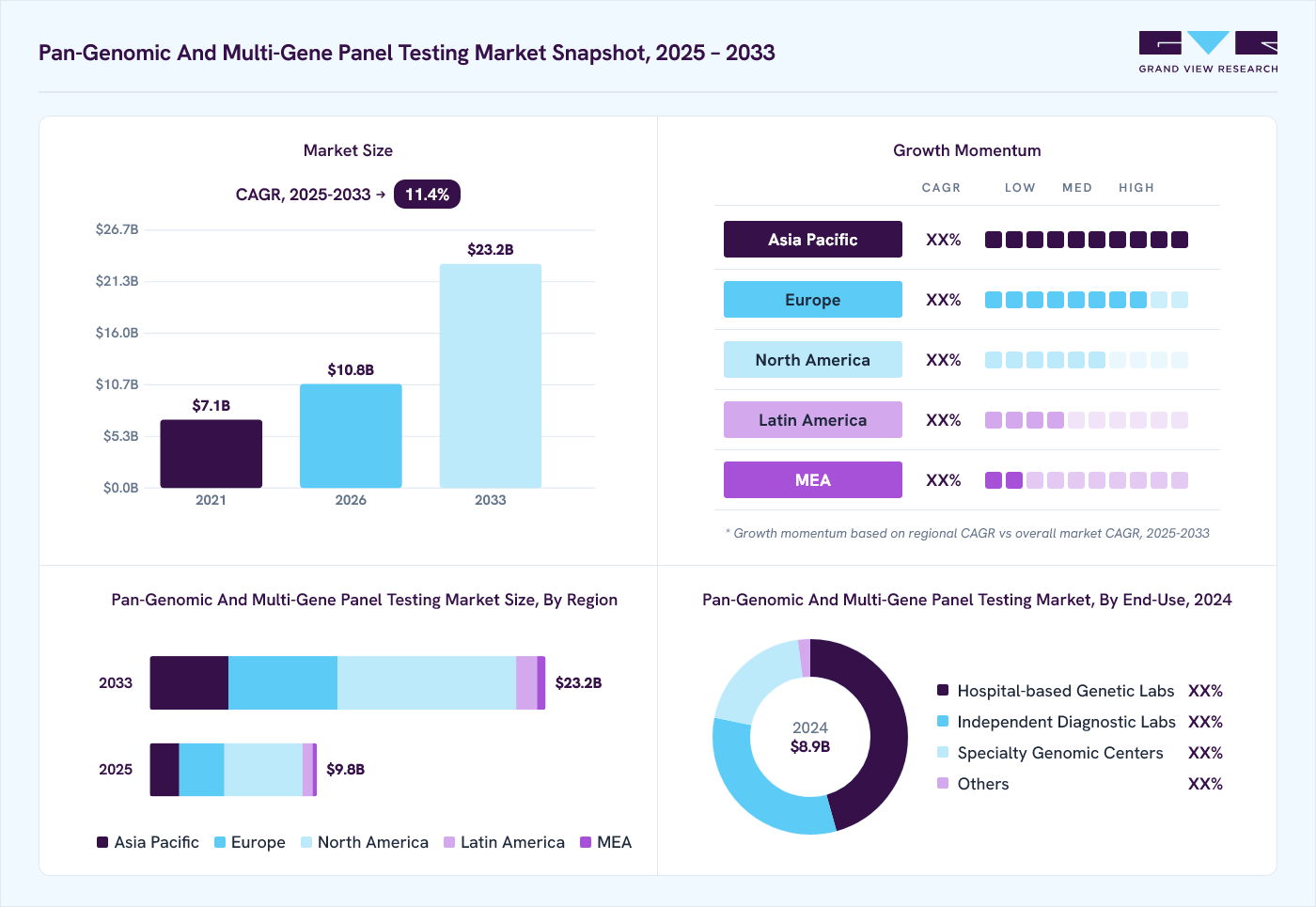

Market Size, 2024

$8.9BMarket Estimate, 2026

$10.8BMarket Forecast, 2033

$23.2BCAGR, 2025–2033

11.4%Pan-genomic And Multi-gene Panel Testing Market Summary

The global pan-genomic and multi-gene panel testing market size was valued at USD 8.9 billion in 2024 and is projected to grow from USD 10.8 billion in 2026 to USD 23.2 billion by 2033, at a CAGR of 11.4% from 2025 to 2033, driven by clinical adoption in oncology and precision medicine and increasing demand for comprehensive genetic insights, rising use of molecular profiling in treatment planning, and advancements in high-throughput sequencing technologies. North America dominated the market, accounting for a revenue share of 46.8% in 2024 Compared to traditional single-gene assays, multi-gene panels that often span dozens to hundreds of cancer-related genes provide deeper and more comprehensive molecular insights.

Key Market Trends & Insights

- The U.S. led the North American market and held the largest revenue share of 82.24% in 2024.

- Based on the test, the oncology multi-gene panels segment dominated the global market with a 55.85% market share in 2024.

- Based on application, theoncology segment held the largest revenue share of 41.38% in 2024.

- Based on end-use, the hospital-based genetic labs segment held the largest revenue share of 45.62% in 2024.

Market Size & Forecast

- 2024 Market Size: USD 8.9 Billion

- 2033 Projected Market Size: USD 23.2 Billion

- CAGR (2025-2033): 11.4%

- North America: Largest Market in 2024

- Asia Pacific: Fastest growing market

Clinically validated assays, such as FoundationOne CDx (approximately 324 genes) and MSK-IMPACT (468 genes), are now routinely used in CLIA-certified laboratories to identify actionable genomic alterations. This has improved therapeutic matching, enabling clinicians to identify rare but targetable variants through a single, comprehensive analysis, rather than relying on sequential, time-consuming individual tests. As a result, major cancer centers are incorporating multi-gene and pan-genomic testing into their oncology workflows. Real-world results demonstrate the quantifiable impact of this adoption. A November 2024 study from the American Society of Clinical Oncology (ASCO) found that 36% of patients who underwent pathologist-directed comprehensive genomic profiling (CGP) received a targeted therapy (TT) or immuno-oncology (IO) agent simply because of biomarker findings in their genomic profile.")

Moreover, the one of the key factors propelling the growth of the pan-genomic and multi-gene panel testing market is the swift and ongoing decrease in sequencing costs. The National Human Genome Research Institute (NHGRI) reports that significant advancements in next-generation sequencing (NGS) technologies have enabled the cost of sequencing a human genome to decrease from nearly USD 100 million in 2001 to approximately USD 600 in 2024. Comprehensive multi-gene testing was once a specialized and expensive process, but thanks to this significant decrease, it is now a readily available and reasonably priced tool for both patients and diagnostic laboratories. As a result, hereditary cancer testing has shifted from being used primarily in specialized genetics centers to becoming a standard component of preventive care and oncology workflows.

The rising global prevalence of genetic disorders, both inherited and newly occurring, has become one of the strongest drivers of the pan-genomic and multi-gene panel testing market. An estimated 400 million people worldwide suffer from rare genetic disorders, and 3-5% of all newborns are impacted by congenital or inherited genetic conditions. Healthcare systems are quickly incorporating extensive multi-gene and pan-genomic testing into standard protocols for early diagnosis, carrier screening, therapeutic decision-making, and long-term disease management as the genetic basis of more diseases becomes more apparent. Adoption in oncology is being greatly increased by the growing recognition of hereditary cancer syndromes, such as Lynch syndrome, Li-Fraumeni syndrome, and BRCA-associated breast/ovarian cancer. With 5-10% of all cancers classified as hereditary, and BRCA1/2 mutations increasing breast cancer risk by up to 70% and ovarian cancer risk by up to 40%, the need for proactive and comprehensive genomic screening has never been more compelling.

In addition, the increasing complexity of genomic data, particularly from whole-genome and large multi-gene panel tests, poses a significant challenge because interpreting millions of variants necessitates extensive clinical genomics and bioinformatics expertise. Many laboratories struggle to find enough molecular geneticists, clinical geneticists, and bioinformaticians to handle the workload. According to a global adoption framework for NGS in oncology published in PMC, a shortage of well-trained personnel, such as clinical molecular geneticists and genomic analysts, impedes widespread implementation. Moreover, infrastructural gaps in sequencing and bioinformatics pipelines exacerbate the issue, making it difficult to maintain consistent quality across laboratories.

Market Concentration & Characteristics

The pan-genomic & multi-gene panel testing industry is characterized by a high level of innovation, which is fueled by rapid advances in sequencing efficiency, expanded genomic coverage, and improved computational analytics. Emerging platforms now allow for more accurate variant detection and deeper interpretation across complex gene networks. Continuous improvements to bioinformatics pipelines, automation, and cloud-based genomic data processing improve scalability and reliability. These innovations are gradually reducing turnaround times and increasing clinical adoption, particularly in oncology and rare disease diagnostics, bolstering the market's reputation as a technologically advanced, high-innovation domain.

The level of M&A activities is medium, with companies strategically acquiring technology developers, sequencing platform providers, and specialized genomic laboratories to broaden capabilities. While consolidation is taking place, it is not as aggressive as in other diagnostic segments due to the technical complexity and regulatory considerations involved with genetic testing. Many deals focus on strengthening bioinformatics capabilities, enhancing assay portfolios, or expanding geographic presence. Partnerships and strategic alliances are still more common than full acquisitions, indicating a balanced and consistent level of market consolidation.

The regulatory impact on this market is significant, as multi-gene panel testing must adhere to stringent quality, analytical validity, and clinical validity standards. Regulatory bodies continue to improve frameworks for genomic data accuracy, test validation, and patient safety. Evolving guidelines for clinical decision-making with next-generation sequencing have a significant impact on product development timelines and market entry strategies. Compliance standards for laboratory accreditation, data privacy, and reporting transparency all influence competitive dynamics. As governments implement more structured genomic regulations, companies must comply with stringent oversight, making regulatory influence extremely important.

Product expansion is high in the market, driven by rising demand for broader, more comprehensive gene panels across oncology, hereditary disorders, pharmacogenomics, and reproductive health. Companies are continually expanding test menus to include rare variant detection, expanded carrier screening, and tumor profiling solutions. Sequencing technology advancements allow for deeper coverage and higher diagnostic yield, promoting greater product diversity. Growing awareness of personalized medicine and the need for multi-analyte genomic insight support rapid expansion, with firms launching more clinically actionable panels to meet diverse healthcare needs.

This industry exhibits a medium level of regional expansion, which is characterized by consistent growth in developing areas while remaining mostly concentrated in developed markets with sophisticated genomic infrastructures. Due to their robust reimbursement systems, advanced laboratory networks, and increased patient awareness, North America and Europe continue to maintain a dominant position. As genomic medicine gains popularity, its expansion into the Asia-Pacific, the Middle East, and Latin America is growing; however, obstacles such as uneven regulatory maturity, limited sequencing capacity, and cost barriers impede its rapid penetration. Regional expansion is anticipated to progress at a steady and sustainable rate as global investments in precision medicine continue to increase.

Test Insights

On the basis of test, the oncology multi-gene panels segment held the largest share of 55.85% in 2024. Multi-gene panels for cancer, such as tissue-based CGP and liquid-biopsy ctDNA assays, continue to be essential tools in precision oncology. Actionable somatic mutations, fusions, gene signatures, and copy-number alterations associated with targeted therapies and immunotherapy selection are detected by these tests. Stronger clinical-outcome datasets, more drug labels linked to specific genomic biomarkers, and a greater reliance on molecular profiling for clinical trial enrollment all contribute to their widespread adoption. By allowing for non-invasive monitoring, relapse detection, and minimal residual disease assessment across solid tumors, liquid biopsy innovations further accelerate segment traction. In March 2024, OGT launched its SureSeq Myeloid Fusion Panel, an RNA-based NGS assay that detects over 30 fusion genes implicated in acute myeloid leukemia (AML), including rare and novel fusion partners, using a partner-agnostic design.

The pharmacogenomics (PGx) panels segment is expected to depict a notable CAGR during the forecast period, supported by increasing use in perioperative medicine, cardiology, psychiatry, oncology, and supportive care as medical professionals work to enhance safety and maximize dosage. Preemptive PGx testing is increasingly viewed by health systems as a cost-effective way to reduce adverse drug reactions and hospitalizations, as PGx results are lifelong and applicable across multiple therapeutic areas. By incorporating practical prescribing advice at the point of care, EHR-based clinical-decision support enhances the value of PGx. Major opportunities lie in system-level pre-emptive PGx programs, HLA-inclusive panels to prevent severe immune-mediated reactions, and integrated pharmacist-led interpretation services. Hospitals are piloting PGx-based formularies and medication-management pathways. Meanwhile, AI-enabled genotype-to-phenotype interpretation tools are emerging, helping laboratories streamline reporting and reduce ambiguity in phenotype assignment. Expansion into point-of-care PGx devices and rapid genotyping platforms also broadens the clinical reach of this segment.

Application Insights

Based on application, the oncology segment accounted for the largest market share of 41.38% in 2024. Multi-gene tumor profiling, liquid biopsy assays, and companion diagnostics enable clinicians to match patients with targeted therapies, inform immunotherapy decisions, and optimize clinical trial eligibility. Market adoption is being driven by an expanding pipeline of biomarker-linked drugs, increasing payer acceptance when tests influence treatment decisions, and the maturation of real-world evidence demonstrating improved outcomes. With cancer incidence rising globally and oncology clinical trials shifting to genomically stratified designs, the demand for broad, high-resolution genomic data remains extremely high across hospitals, academic centers, and integrated oncology networks. Furthermore, in September 2024, Natera released new MRD data that further validated the sensitivity of its recurrence-monitoring platform. In addition, in May 2025, Labcorp expanded its precision oncology portfolio with new solid-tumor and hematologic NGS panels and enhanced its OmniSeq INSIGHT platform with HRD testing, thereby improving therapeutic matching potential.

In addition, the rare & undiagnosed genetic diseases segment is the fastest-growing segment during the forecast period, owing to national rare-disease programs, newborn genome projects, large-scale sequencing consortia, and cross-border collaborations focused on variant discovery. Advances in structural-variant detection, RNA sequencing, and AI-driven interpretation are increasing diagnostic yield, while longitudinal reanalysis services continue to be clinically useful. Laboratories that offer comprehensive multi-omics, quick turnaround times, and clinician-friendly reporting are poised to win institutional contracts, particularly in pediatric tertiary care facilities. For instance, in June 2024, Myriad Genetics launched the Universal Plus Panel for the Foresight Carrier Screen. This expanded panel includes additional rare genetic conditions, providing a more comprehensive assessment for individuals planning a family.

End-use Insights

Hospitals-based genetic laboratories dominated the pan-genomic & multi-gene panel testing industry in 2024, accounting for a 45.62% share. Hospital-based genetic laboratories remain the foundation of clinical genomics, serving as testing hubs for large tertiary centers, academic medical institutions, and integrated health systems. These labs benefit from direct access to patient histories, multidisciplinary teams, and immediate clinical decision-making pathways, which allow for faster interpretation and more personalized reporting. Their use of genomic technologies is growing rapidly as exome and genome testing become the norm in critical care pediatrics, oncology workups, and the management of complex multisystem disorders. Hospitals are also increasingly developing in-house capabilities to reduce outsourcing costs, improve turnaround times, and integrate genomic data into electronic health records. With national health systems investing in in-hospital genomic infrastructure and training, hospital-based labs are expected to play an even larger role in the mainstreaming of precision medicine, particularly in newborn screening, hereditary disease evaluation, and oncology.

The specialty genomic centers segment is expected to witness the fastest growth during the forecast period, driven by the continued innovation in complex rare-disease and pediatric genomics, supported by clinical collaborations and national pilots. In September 2025, BGI Genomics published large-scale newborn genomic screening results, showing significantly higher detection rates than standard biochemical methods, which reinforces the value of high-end specialty centers in population screening. In October 2025, Australia’s Murdoch Children’s Research Institute announced outcomes from the BabyScreen+ genomic pilot, revealing high diagnostic yield and strong parental acceptance within specialty pediatric programs.

Regional Insights

The pan-genomic and multi-gene panel testing industry in North America held the largest share of 46.82% in 2024, as healthcare systems increasingly integrated precision medicine into routine care. These tests enable the simultaneous analysis of dozens to hundreds of genes, helping clinicians gain a deeper understanding of complex conditions such as cancer, cardiovascular disease, and rare genetic disorders. Advanced molecular diagnostic laboratories, well-connected hospital networks, and a strong clinical research environment have all contributed to increased clinical adoption in the United States and Canada. Multi-gene panels are now widely used in oncology, prenatal screening, and the diagnosis of rare diseases because they provide comprehensive genetic insights in a single procedure, thereby avoiding the delays associated with sequential single-gene testing.

U.S. Pan-genomic And Multi-gene Panel Testing Market Trends

The U.S. led the North American market and held the largest revenue share of 82.24% in 2024. The U.S. pan-genomic & multi-gene panel testing industry is expanding steadily, driven by the transition from niche research to mainstream clinical utility as precision oncology and genetic medicine become more integrated into care pathways. Hospitals, reference laboratories, and integrated health systems are increasingly using NGS-based panels to analyze dozens of hundreds of clinically relevant genes in a single workflow, eliminating the need for sequential single-gene testing and shortening diagnostic time. Moreover, clinical disease burden remains a major growth driver. Hereditary cancer syndromes contribute significantly to cancer incidence in the United States, with inherited factors accounting for an estimated 5-10% of colorectal cancer cases. Individuals with Lynch syndrome, for example, have up to an 80% lifetime risk of colorectal cancer and a 60% lifetime risk of endometrial cancer.

Europe Pan-genomic And Multi-gene Panel Testing Market Trends

The pan-genomic & multi-gene panel testing industry in Europe is rapidly expanding as precision medicine gains strong institutional backing and broader clinical adoption. Growth is being reinforced by major public-health initiatives and investments in infrastructure. Major public-health initiatives and infrastructure investments are driving growth. The 1+Million Genomes (1+MG) Initiative aims to build a secure and federated European data infrastructure for genomic and clinical information. Building on this, the European Genomic Data Infrastructure (GDI) facilitates cross-border access to genomic datasets while adhering to privacy, ethical, and national regulatory standards. Simultaneously, the Genome of Europe project has pledged to sequence at least 100,000 genomes from various European populations, resulting in a reference dataset that improves variant interpretation and the clinical validity of pan-genomic and multi-gene panels. In March 2024, a transcontinental collaboration brought together 300 experts from 12 countries to investigate the genetic basis of thousands of unresolved cases of rare diseases. Collectively, these initiatives strengthen the scientific evidence for multi-gene testing and support more accurate, population-specific genomic diagnostics across Europe.

The UK pan-genomic and multi-gene panel testing industry has strengthened considerably as genomics becomes embedded in the National Health Service (NHS) through the Genomic Medicine Service (GMS). The NHS GMS now offers a comprehensive range of multi-gene assays for inherited diseases and cancer, including pan‑cancer panels. These tests enable the simultaneous analysis of multiple genes, allowing clinicians to identify clinically actionable variants quickly. The integration of next-generation sequencing (NGS) across NHS Genomic Laboratory Hubs ensures consistent testing, shorter turnaround times, and wider clinical adoption, particularly in oncology and rare disease diagnostics.

National commissioning and infrastructure support have been critical to driving market growth. The NHS National Genomic Test Directory defines which genomic tests are funded and available to patients, and it is updated on a regular basis to reflect technological and clinical advances. In April 2025, NHS England and NICE published a joint genomic testing pathway that streamlines evaluation, prioritization, and commissioning of new genomic tests, reducing uncertainty for developers and accelerating the adoption of novel multi-gene panels.

The pan-genomic and multi-gene panel testing industry in France is steadily expanding as genomic medicine becomes a cornerstone of national health strategy. The government-backed Plan France Médecine Génomique 2025 (PFMG2025) promotes high-throughput genome sequencing for patients with rare diseases, hereditary cancer risk, and established cancer, changing the way multi-gene panels are used in clinical practice. With this momentum, more diagnostic labs are offering gene panels that include dozens of clinically relevant genes, thereby accelerating diagnosis, guiding therapy, and shortening the time to actionable findings for patients. France Génomique, a national infrastructure network that offers shared sequencing and bioinformatics capacity to both public and private actors, contributes to this growth.

Asia Pacific Pan-genomic And Multi-gene Panel Testing Market Trends

The pan-genomic and multi-gene panel testing industry in the Asia Pacific is experiencing rapid growth, driven by a convergence of technological advancements, rising clinical demand, and supportive national initiatives. As next-generation sequencing (NGS) becomes increasingly available, multi-gene panels are being utilized in both clinical and research settings, providing comprehensive genetic insights that inform diagnosis, risk assessment, and treatment decisions. Lower sequencing costs, increased healthcare spending, and advances in bioinformatics and variant interpretation have improved the affordability and clinical utility of these tests, allowing for wider adoption. These factors work together to strengthen the region's precision genomic testing ecosystem and encourage both public and private stakeholders to expand their offerings, resulting in further market growth. National genomics initiatives in China, India, and Japan are key drivers of market growth. In China, the BGI Group utilizes its DNBSEQ sequencing platforms to offer both population-scale and clinically focused panel testing, thereby advancing precision oncology and the diagnosis of rare diseases.

The Japan pan-genomic ad multi-gene panel testing industry has entered a phase of rapid clinical maturation. Comprehensive genomic profiling (CGP) and large hereditary panels are now routinely used in university medical centers and private diagnostic laboratories to identify actionable variants, guide targeted cancer therapies, and aid in the diagnosis of complex or undiagnosed cases. Clinical laboratories use tumor DNA/RNA panels, whole-exome sequencing (WES), and focused germline panels in oncology, pediatric genetics, and cardiovascular genetics. Foundation Medicine (FoundationOne), SRL, BML, LSI Medience, Illumina, Thermo Fisher Scientific, and MGI are major contributors to this ecosystem, offering sequencing platforms, diagnostic assays, reagents, and bioinformatics pipelines. Their presence has increased national testing capacity, shortened turnaround times, and made multigene testing more accessible in routine clinical workflows.

The pan-genomic and multi-gene panel testing market in China is witnessing strong expansion as clinical genomics shifts from research settings into mainstream healthcare. Rising demand from oncology centers, rare disease clinics, and maternal-fetal medicine programs is driving up referrals for panel-based genetic testing in China, reducing diagnostic timelines and improving the rate of actionable findings. According to data from the National Health Commission (NHC), over 780,000 rare disease cases have been officially registered since 2019, indicating that this public health burden is becoming more widely recognized. Large population studies involving over 14 million people have also revealed an unexpectedly high prevalence of rare diseases across the country. By 2023, it was estimated that nearly 20 million people in China would be affected by rare diseases, with genetic and genomic testing becoming increasingly important in early detection and long-term disease management strategies.

Latin America Pan-genomic And Multi-gene Panel Testing Market Trends

The pan-genomic & multi-gene panel testing industry in Latin America is expanding rapidly, driven by increasing cancer incidence, a growing awareness of the large undiagnosed rare-disease population, and the expanding use of targeted therapies has encouraged laboratories to move away from sequential single-gene testing toward broader multi-gene panels that deliver multiple actionable results in a single analysis. Across the region, health authorities and patient advocacy groups have intensified efforts to highlight the burden of rare diseases and push for better diagnostic pathways. Regional collaborations, including initiatives uniting patient organizations, clinicians, researchers, and advocacy groups, are helping to strengthen awareness, data sharing, and access to genetic services for rare disease communities throughout Latin America.

The Brazil pan-genomic and multi-gene panel testing industry is steadily expanding as next-generation sequencing transitions from a research-focused activity into routine clinical application. An estimated 13 million people in Brazil live with rare diseases, many of which have a genetic basis. This estimate aligns with the Brazilian Ministry of Health’s definition of rare diseases, which categorizes a condition as rare when it affects fewer than 65 individuals per 100,000 people. Among the more than 7,000 rare diseases identified globally, approximately 80% are of genetic origin, typically caused by inherited mutations that often follow recessive patterns. These diseases are generally chronic, progressive, and disabling, frequently leading to severe long-term outcomes without early molecular diagnosis.

Middle East and Africa Pan-genomic And Multi-gene Panel Testing Market Trends

The Middle East and Africa pan-genomic & multi-gene panel testing industry is growing steadily, by National and private hospital networks across the Gulf region and South Africa are increasingly integrating multi-gene panels and targeted tumor profiling into routine clinical care, while major reference laboratories continue to expand exome sequencing and panel-based services to meet growing regional demand. Global sequencing technology providers, such as Illumina, Thermo Fisher Scientific, Roche, and BGI/MGI, supply the core platforms and reagents that support much of the region’s genomic testing capacity. Meanwhile, regional diagnostic networks and academic genomics centers manage local sample processing, bioinformatics, and clinical interpretation.

The Saudi Arabia pan-genomic and multi-gene panel testing industry is expanding as clinical genomics transitions from isolated research settings into routine use across major hospitals and reference laboratories. Academic hospital genomics units, national research institutes, and growing public-private partnerships are playing a central role by expanding sequencing capacity, developing local variant curation pipelines, and training clinicians and laboratory professionals. These efforts are making multi-gene panels more accurate and locally relevant by incorporating South Africa’s unique genetic diversity. As a result, variant interpretation is improving, clinical decision-making is becoming more precise, and physician confidence in ordering multi-gene and genomic tests is strengthening across oncology, rare diseases, and inherited disorder care.

Key Pan-genomic And Multi-gene Panel Testing Company Insights

The pan-genomic & multi-gene panel testing market features several key players driving innovation and adoption. Leading companies include Illumina, Inc., Thermo Fisher Scientific, Inc., Fulgent Genetics, Ambry Genetics (Tempus), GeneDx, Baylor Genetics, Natera, Caris Life Sciences, and Foundation Medicine, Inc. (Roche), and Guardant Health. These companies are making significant investments in advancing hematology technologies, driving continuous product innovation, expanding their geographic footprints, and forming strategic alliances to strengthen market presence.

Key Pan-genomic And Multi-gene Panel Testing Companies:

The following are the leading companies in the pan-genomic and multi-gene panel testing market. These companies collectively hold the largest market share and dictate industry trends.

- Illumina, Inc.

- Thermo Fisher Scientific, Inc.

- Fulgent Genetics

- Ambry Genetics (Tempus)

- GeneDx

- Baylor Genetics

- Natera

- Caris Life Sciences

- Foundation Medicine, Inc. (Roche)

- Guardant Health

Recent Developments

-

In November 2025, Paragon Genomics introduced a CleanPlex Pharmacogenomics (PGx) NGS Panel targeting 28 pharmacogenes, enabling high-multiplex, low-error workflows on major sequencing platforms from sample types such as blood or saliva.

-

In September 2025, Quest Diagnostics launched an advanced PGx testing service, covering 17 genes + 4 HLA alleles, along with a report for genotype, phenotype prediction, and clinical decision support (via Coriell/InformedDNA) for drug prescribing.

-

In September 2025, Illumina announced partnerships with multiple global pharmaceutical companies to develop companion diagnostics (CDx) for the KRAS biomarker, leveraging its TruSight Oncology comprehensive genomic profiling platform to broaden precision oncology access.

-

In July 2025, QIAGEN launched its QIAseq xHYB Long Read Panels, a set of target-enrichment assays optimized for long-read sequencing (e.g., PacBio). These panels enable high-resolution analysis of complex genomic regions such as structural variants, repeat expansions, and HLA loci using native long-read technologies. The offering includes fixed panels (hereditary cancer, HLA) and customizable formats, integrated with QIAGEN’s sample prep and bioinformatics pipeline.

-

In May 2025, Labcorp expanded its precision oncology portfolio with new NGS panels for solid tumors and hematologic malignancies, including a rapid AML panel and broader pan-hematologic panels. It also enhanced its OmniSeq INSIGHT test to include HRD (homologous recombination deficiency) testing, thereby increasing its utility in guiding targeted cancer therapies and clinical trials.

-

In April 2025, Baylor Genetics introduced an innovative RNA sequencing test that advances the detection of certain qualified variants, using carefully curated genetic data, expert interpretation, and an AI-driven prediction algorithm criteria. This addition to Whole Exome and Whole Genome Sequencing (WES/WGS) aims to reclassify certain variants, enabling quicker, more actionable diagnoses and treatment.

-

In February 2025, Fulgent Genetics received the EU CE Mark for FulgentExome, an in vitro diagnostic medical device software used within the FulgentExome system to analyze genetic information derived from next-generation sequencing. This approval allows Fulgent to offer its exome sequencing services in the European Union.

Pan-genomic And Multi-gene Panel Testing Market Report Scope

Report Attribute

Details

Market size in 2024

USD 8.9 billion

Estimated Market size in 2026

USD 10.8 billion

Projected Market size by 2033

USD 23.2 billion

Growth rate

CAGR of 11.4% from 2025 to 2033

Base year for estimation

2024

Historical data

2021 - 2023

Forecast period

2025 - 2033

Quantitative units

Revenue in USD million/billion and CAGR from 2025 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Test, application, end-use, region

Regional scope

North America; Europe; Asia Pacific; Latin America; Middle East and Africa

Country scope

U.S.; Canada; Mexico; UK; Germany; France; Italy; Spain; Norway; Sweden; Denmark; Japan; China; India; Australia; South Korea; Thailand; Brazil; Argentina; South Africa; Saudi Arabia; UAE; Kuwait

Key companies profiled

Illumina, Inc.; Thermo Fisher Scientific, Inc.; Fulgent Genetics; Ambry Genetics (Tempus); GeneDx; Baylor Genetics; Natera; Caris Life Sciences; Foundation Medicine, Inc. (Roche); Guardant Health

Customization scope

Free report customization (equivalent up to 8 analysts’ working days) with purchase. Addition or alteration to country, regional & segment scope

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Pan-genomic And Multi-gene Panel Testing Market Report Segmentation

This report forecasts revenue growth and provides an analysis of the latest trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global pan-genomic & multi-gene panel testing market report based on test, application, end-use, and region:

-

Test Outlook (Revenue, USD Million, 2021 - 2033)

-

Pan-Genomic / Whole Exome Based Panels

-

Comprehensive Hereditary Disease Panels

-

Oncology Multi-Gene Panels

-

Pharmacogenomics (PGx) Panels

-

-

Application Outlook (Revenue, USD Million, 2021 - 2033)

-

Oncology

-

Cardiology & Cardiomyopathy

-

Neurology and Neurogenetics

-

Rare & Undiagnosed Genetic Diseases

-

Reproductive Carrier Screening

-

Newborn & Pediatric Genomics

-

-

End-use Outlook (Revenue, USD Million, 2021 - 2033)

-

Hospital-based Genetic Labs

-

Independent Diagnostic Labs

-

Specialty Genomic Centers

-

Others

-

-

Regional Outlook (USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

UK

-

Germany

-

France

-

Italy

-

Spain

-

Denmark

-

Sweden

-

Norway

-

-

Asia Pacific

-

Japan

-

China

-

India

-

Australia

-

Thailand

-

South Korea

-

-

Latin America

-

Brazil

-

Argentina

-

-

Middle East & Africa

-

South Africa

-

Saudi Arabia

-

UAE

-

Kuwait

-

-

Frequently Asked Questions About This Report

The global pan-genomic and multi-gene panel testing market size was valued at USD 8.9 billion in 2024 and is estimated at USD 10.8 billion for 2026.

The global pan-genomic and multi-gene panel testing market is expected to grow at a CAGR of 11.4% from 2025 to 2030, reaching USD 23.2 billion by 2033.

North America dominated with a 46.8% revenue share in 2024.

Some key players including Illumina, Inc.; Thermo Fisher Scientific, Inc.; Fulgent Genetics; Ambry Genetics (Tempus); GeneDx; Baylor Genetics; Natera; Caris Life Sciences; Foundation Medicine, Inc. (Roche); Guardant Health

Key factors that are driving the market growth include driven by clinical adoption in oncology and precision medicine and increasing demand for comprehensive genetic insights, rising use of molecular profiling in treatment planning, and advancements in high-throughput sequencing technologies.

About the Author(s)

Clinical Diagnostics Research Team

Healthcare · Clinical DiagnosticsThis report was authored by the clinical diagnostics research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the clinical diagnostics segment of the healthcare industry. All findings are based on proprietary healthcare databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.