- Home

- »

- Advanced Interior Materials

- »

-

Semiconductor Packaging Materials Market Report 2026-2033GVR Report cover

![Semiconductor Packaging Materials Market (2026 - 2033)Report]()

Semiconductor Packaging Materials Market (2026 - 2033)

Size, Share & Trends Analysis Report By Product (Organic Substrates, Bonding Wires, Leadframes), By Application (Consumer Electronics, Automotive, Healthcare), By Region, And Segment Forecasts

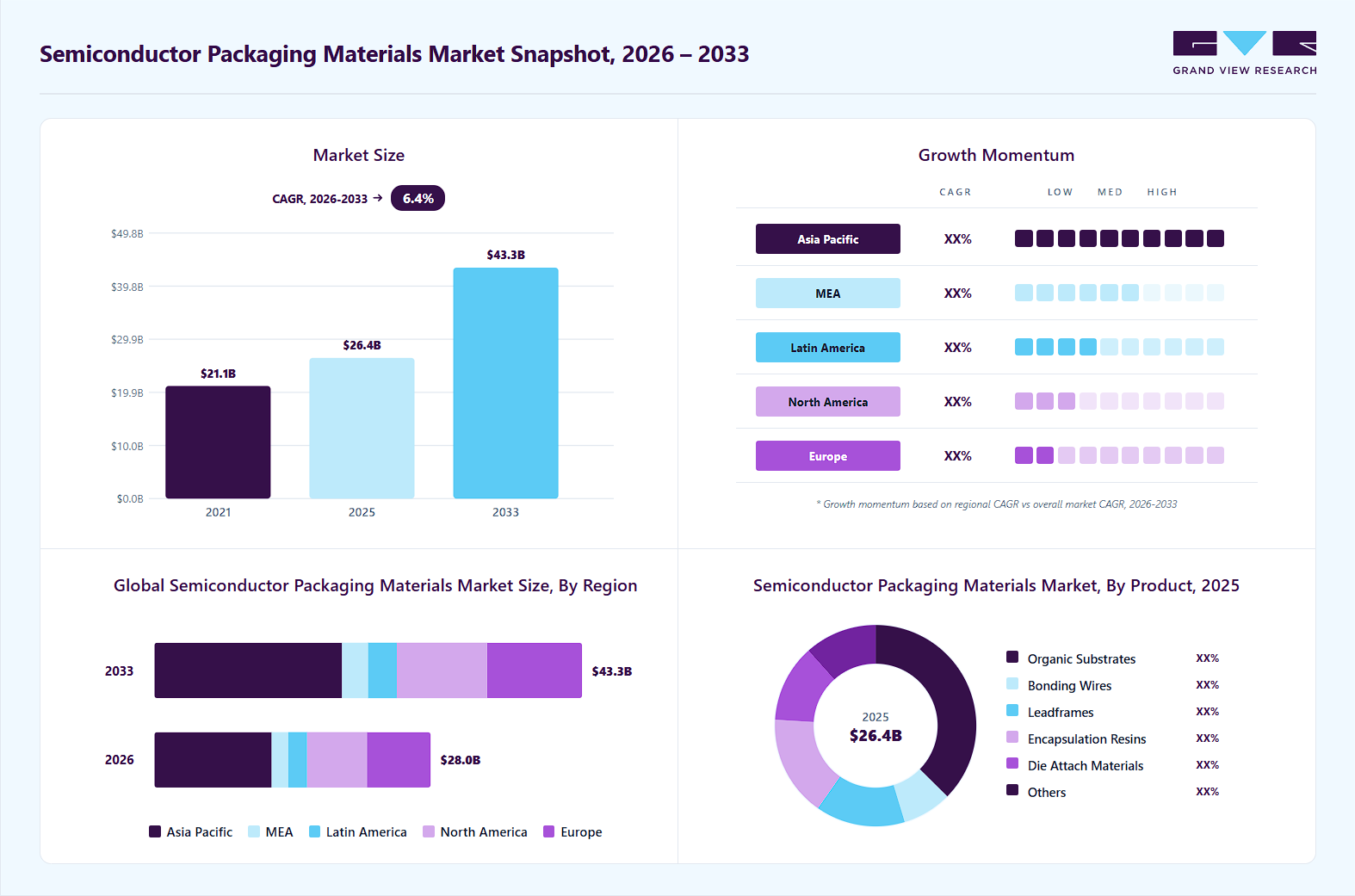

Market Size, 2025

$26.4BMarket Estimate, 2026

$28.0BMarket Forecast, 2033

$43.3BCAGR, 2026–2033

6.4%Semiconductor Packaging Materials Market Summary

The global semiconductor packaging materials market size was valued at USD 26.4 billion in 2025 and is projected to grow from USD 28.0 billion in 2026 to USD 43.3 billion by 2033, at a CAGR of 6.4% from 2026 to 2033. Asia Pacific dominated the global industry with the largest revenue share of 42.2% in 2025. The market for semiconductor packaging materials is witnessing strong growth due to rising demand for advanced semiconductor devices across consumer electronics, automotive, industrial automation, and telecommunications sectors.

Key Market Trends & Insights

- By product: Organic substrates segment held the largest revenue share of 37.4% in 2025

- By application: Consumer electronics segment held the largest market share of 35.9% in 2025.

Regional Highlights

- Largest regional market: Asia Pacific (42.2% revenue share, 2025)

- By country: China held the largest market share in 2025.

Market Size & Forecast

- Market size in 2025: USD 26.4 Billion

- Estimated market size in 2026: USD 28.0 Billion

- Projected market size by 2033: USD 43.3 Billion

- CAGR (2026-2033): 6.4%

The increasing production of smartphones, wearable electronics, AI-enabled devices, and high-performance computing systems is accelerating the need for advanced packaging solutions that enhance chip protection, connectivity, and thermal management. Miniaturization of semiconductor components is also driving demand for sophisticated packaging materials capable of supporting compact and high-density integrated circuits. The rapid adoption of electric vehicles and autonomous driving technologies is further contributing to market expansion. Modern vehicles require advanced semiconductor packages for power management, infotainment systems, battery management systems, and ADAS functionalities. Packaging materials such as leadframes, substrates, bonding wires, encapsulation resins, and thermal interface materials are increasingly used to ensure durability and high performance under extreme operating conditions. Automotive semiconductor demand is therefore significantly strengthening the need for reliable packaging materials.")

Governments worldwide are actively supporting semiconductor ecosystem development through subsidies, manufacturing incentives, and strategic investment programs. In the United States, initiatives under the CHIPS and Science Act are encouraging domestic semiconductor manufacturing and packaging expansion. Funding support for advanced packaging research and semiconductor fabrication facilities is expected to increase the consumption of semiconductor packaging materials across the country. Similar initiatives are also being introduced in Europe to enhance regional semiconductor independence.

The semiconductor packaging industry is witnessing rapid innovation driven by the transition toward advanced packaging technologies. High-density interconnect substrates and fan-out wafer-level packaging materials are gaining significant traction due to their ability to improve device performance while reducing package size. Material suppliers are increasingly developing ultra-thin substrates and low-dielectric materials to support high-speed semiconductor applications.

Sustainability is emerging as a major trend within the industry. Semiconductor manufacturers are increasingly focusing on environmentally friendly packaging materials with lower carbon footprints and reduced hazardous substance content. Lead-free solder materials, halogen-free encapsulants, and recyclable substrate technologies are witnessing growing adoption due to stricter environmental regulations and sustainability commitments from electronics manufacturers.

Market Dynamics

One of the major drivers for the semiconductor packaging materials industry is the continuous advancement in chip architecture and packaging technologies. Semiconductor manufacturers are increasingly adopting heterogeneous integration, 2.5D/3D IC packaging, and chiplet-based architectures to improve performance and reduce power consumption. These advanced packaging formats require highly specialized materials with superior thermal conductivity, electrical insulation, and mechanical reliability. Consequently, suppliers are focusing on developing innovative substrates, die attaching materials, and encapsulation compounds to meet evolving industry requirements.

The semiconductor packaging materials industry faces a major restraint in the form of rising costs associated with advanced semiconductor packaging technologies. Modern packaging approaches such as 2.5D/3D IC packaging, fan-out wafer-level packaging, and chiplet integration require highly sophisticated materials with superior thermal, electrical, and mechanical properties.

The development and production of advanced substrates, underfills, encapsulation compounds, and thermal interface materials involve significant research and manufacturing investments. Smaller semiconductor manufacturers and OSAT providers often face challenges in adopting these technologies due to high capital expenditure requirements and complex process integration.

In addition, fluctuations in raw material prices and supply chain disruptions further increase operational costs for packaging material manufacturers. Materials such as copper, specialty resins, rare metals, and advanced laminates are subject to price volatility and geopolitical supply risks.

Market Concentration & Characteristics

The semiconductor packaging materials industry is moderately consolidated, with a mix of global material suppliers and regional specialty manufacturers competing across different product segments. Large multinational companies dominate advanced substrate materials, encapsulation compounds, and bonding technologies due to their extensive R&D capabilities and established relationships with semiconductor manufacturers. However, regional players in Asia Pacific also hold strong market positions owing to localized supply chains and cost advantages.

Competition within the market is highly innovation-driven, particularly in advanced packaging materials required for AI, automotive, and high-performance computing applications. Companies are focusing on strategic collaborations with semiconductor manufacturers and OSAT providers to strengthen technology development and secure long-term contracts. Mergers, acquisitions, and joint ventures are also increasing as companies seek to expand material portfolios and global manufacturing capabilities.

The threat of substitutes in the semiconductor packaging materials industry remains moderate due to the specialized nature of semiconductor packaging applications. Different materials can sometimes replace conventional packaging components depending on cost, thermal requirements, and electrical performance. For instance, copper bonding wires are increasingly replacing traditional gold bonding wires because of lower costs and improved electrical conductivity.

Alternative packaging technologies may also influence material demand patterns. Wafer-level packaging and fan-out packaging approaches reduce dependence on certain conventional leadframe and substrate materials while increasing demand for advanced polymers and redistribution layer materials. Such technology transitions are reshaping material consumption trends across the semiconductor packaging industry.

Product Insights

The organic substrates segment held the largest revenue share of 37.4% in 2025, due to its widespread usage in advanced semiconductor packaging applications including flip-chip ball grid array (FCBGA), chip-scale packaging, and system-in-package technologies. Organic substrates offer advantages such as lightweight structure, cost efficiency, superior electrical performance, and compatibility with high-density interconnect designs.

Increasing demand for high-performance processors, AI chips, smartphones, and networking devices has significantly accelerated the adoption of advanced organic substrates. Their ability to support miniaturization and enhanced signal transmission has further strengthened their dominance across consumer electronics and high-performance computing applications.

The die attach materials segment is expected to grow at a CAGR of 6.7% over the forecast period, owing to rising demand for reliable thermal and electrical connectivity in advanced semiconductor packages. Die attach materials play a critical role in bonding semiconductor dies to substrates and improving heat dissipation in high-power devices.

Increasing adoption of electric vehicles, AI processors, 5G infrastructure, and industrial automation systems is driving demand for advanced conductive and non-conductive die attach solutions. Manufacturers are increasingly focusing on high-performance silver sintering materials, epoxy adhesives, and advanced thermal interface compounds to improve semiconductor reliability, durability, and operational efficiency in next-generation electronic devices.

Application Insights

The consumer electronics segment held the largest market share of 35.9% in 2025, due to the massive production volume of smartphones, laptops, tablets, gaming consoles, wearable devices, and smart home electronics worldwide. Semiconductor packaging materials are extensively utilized in these products to ensure miniaturization, thermal management, and electrical protection of semiconductor components.

Rapid technological advancements in mobile processors, memory chips, and high-speed communication devices continue to increase the requirement for advanced packaging materials. Growing consumer demand for compact, high-performance, and energy-efficient electronic devices has therefore maintained the strong dominance of the consumer electronics segment in the market.

The automotive segment is expected to grow at a CAGR of 7.4% over the forecast period, due to increasing semiconductor adoption in electric vehicles, autonomous driving systems, battery management systems, and advanced driver assistance systems (ADAS). Modern vehicles require high-performance semiconductor packages capable of operating under extreme temperature and reliability conditions. This is driving demand for advanced packaging materials including thermal interface materials, encapsulants, ceramic substrates, and high-reliability die attach materials. The global transition toward vehicle electrification and connected mobility solutions is further accelerating semiconductor content per vehicle, creating strong long-term growth opportunities for semiconductor packaging material manufacturers.

Regional Insights

Asia Pacific semiconductor packaging materials industry dominated the global market and accounted for the largest revenue share of 42.2% in 2025, due to the strong presence of semiconductor manufacturing ecosystems across China, Taiwan, South Korea, Japan, and Southeast Asia. The region hosts major semiconductor foundries, OSAT companies, and electronics manufacturers, creating significant demand for packaging substrates, encapsulation materials, and bonding solutions. Governments across the region continue to support semiconductor investments through subsidies and infrastructure development programs.

Rising demand for consumer electronics, electric vehicles, and telecommunication equipment is further strengthening regional market growth. China and Taiwan remain key hubs for advanced semiconductor packaging operations, while Southeast Asian countries are emerging as important assembly and testing centers. The availability of cost-effective labor and integrated supply chains also supports Asia Pacific’s leadership position in the market.

In the Asia Pacific semiconductor packaging materials market, China accounted for the largest revenue share of 38.7% in 2025. China semiconductor packaging materials industry is rapidly expanding its production capabilities to reduce dependency on imported semiconductor technologies. Government-backed investments in semiconductor manufacturing and advanced packaging facilities are significantly driving demand for substrates, leadframes, and encapsulation compounds. Domestic companies are increasingly focusing on developing local material supply chains for AI chips, automotive semiconductors, and consumer electronics applications.

The country is also witnessing rising adoption of advanced packaging technologies such as wafer-level packaging and system-in-package solutions. Expansion of OSAT operations and semiconductor fabrication plants continues to strengthen material consumption across China. In addition, increasing R&D investments in high-performance thermal interface materials and advanced laminates are supporting technological advancements within the market.

North America Semiconductor Packaging Materials Market Trends

North America semiconductor packaging materials industry is witnessing strong growth in demand due to rising investments in domestic semiconductor manufacturing and packaging infrastructure. The region is focusing heavily on advanced packaging technologies for AI processors, high-performance computing systems, and defense applications. Government support through semiconductor funding programs is encouraging material innovation and local production expansion.

The growing electric vehicle industry is also creating demand for advanced semiconductor packaging materials with superior thermal management capabilities. Companies are investing in next-generation substrate technologies and advanced encapsulation materials to improve chip reliability and performance. Increased collaboration between semiconductor firms and research institutions is further supporting innovation within the regional market.

U.S. Semiconductor Packaging Materials Market Trends

The U.S. semiconductor packaging materials industry is expanding due to strong investments in semiconductor reshoring initiatives and advanced chip manufacturing projects. Demand for advanced packaging materials is increasing across AI, cloud computing, aerospace, and defense applications. Semiconductor companies are focusing on heterogeneous integration and chiplet architectures, which require highly advanced packaging substrates and thermal management materials.

The country is also emphasizing domestic supply chain resilience, encouraging local sourcing of semiconductor materials and packaging components. Increased adoption of electric vehicles and autonomous technologies is further driving demand for high-reliability semiconductor packaging solutions. Research activities focused on 3D packaging technologies and sustainable semiconductor materials are additionally supporting market growth.

Europe Semiconductor Packaging Materials Market Trends

Europe semiconductor packaging materials industry is strengthening its semiconductor packaging ecosystem through strategic investments in advanced semiconductor technologies and local manufacturing capabilities. Demand for packaging materials is increasing across automotive electronics, industrial automation, and renewable energy applications. European semiconductor manufacturers are focusing on high-reliability packaging solutions for electric vehicles and industrial control systems.

Sustainability regulations are encouraging the adoption of environmentally friendly semiconductor packaging materials, including lead-free and halogen-free compounds. Governments across the region are also supporting semiconductor R&D initiatives aimed at improving packaging efficiency and thermal performance. The growing emphasis on energy-efficient electronics and smart manufacturing technologies is expected to further support market expansion.

Germany semiconductor packaging materials industry plays a significant role within the European market due to its strong automotive and industrial manufacturing sectors. The rising production of electric vehicles and advanced driver assistance systems is driving demand for high-performance semiconductor packages and thermal management materials. German companies are investing in advanced packaging research to support next-generation automotive semiconductors and industrial automation systems.

Central and South America Semiconductor Packaging Materials Market Trends

Central and South America semiconductor packaging materials industry is gradually emerging as a developing market due to growing electronics manufacturing activities and increasing adoption of connected technologies. Demand for semiconductor packaging materials is primarily supported by consumer electronics, automotive assembly, and industrial automation sectors. Countries such as Brazil and Mexico are witnessing investments in electronics production facilities that require semiconductor assembly and packaging support. The expansion of telecommunication infrastructure and smart manufacturing initiatives is also contributing to market growth.

Middle East & Africa Semiconductor Packaging Materials Market Trends

The Middle East & Africa semiconductor packaging materials industry is experiencing gradual growth driven by increasing digital transformation initiatives and investments in electronics infrastructure. The rising adoption of smart technologies, renewable energy systems, and telecommunications networks is driving semiconductor demand across the region.

Countries in the Gulf region are investing in advanced technology ecosystems and data center infrastructure, supporting the need for semiconductor components and associated packaging materials. The automotive and industrial sectors are also increasingly using semiconductor devices for automation and energy-efficiency applications.

Key Semiconductor Packaging Materials Company Insights

Some of the key players operating in the market include Henkel AG & Co. KGaA and KYOCERA Corporation

-

Henkel AG & Co. KGaA is a leading supplier of semiconductor packaging materials including die attach adhesives, underfills, encapsulants, and thermal interface materials. The company focuses on advanced packaging solutions for automotive electronics, AI processors, and high-performance semiconductor applications, supported by strong R&D capabilities and global manufacturing operations.

-

KYOCERA Corporation is a major provider of advanced ceramic packages, semiconductor substrates, and electronic components used in high-reliability semiconductor packaging applications. The company has strong expertise in thermal management technologies and serves automotive, industrial, telecommunication, and aerospace semiconductor markets.

Tanaka Holdings and Amkor Technology, Inc. are some of the emerging market participants in the semiconductor packaging materials industry.

-

Tanaka Holdings specializes in precious metal materials and bonding wire technologies used in semiconductor packaging. The company plays an important role in supplying high-performance conductive materials for advanced IC packaging and next-generation electronic devices.

-

Amkor Technology, Inc. is one of the world’s leading outsourced semiconductor assembly and test (OSAT) providers, offering advanced packaging technologies such as flip-chip, wafer-level packaging, and system-in-package solutions. The company supports semiconductor manufacturers across consumer electronics, automotive, AI, and 5G infrastructure applications.

Key Semiconductor Packaging Materials Companies:

The following key companies have been profiled for this study on the semiconductor packaging materials market.

-

Henkel AG & Co. KGaA

-

KYOCERA Corporation

-

Sumitomo Chemical

-

DuPont

-

Resonac Corporation

-

LG Chem

-

Toray Industries

-

Tanaka Holdings

-

Siliconware Precision Industries Co., Ltd.

-

Amkor Technology, Inc.

Competitive Benchmarking

Operating Strategies

Competitive Edge

Weakness

Mature Players: Henkel AG & Co. KGaA; KYOCERA Corporation; DuPont; Resonac Corporation

- Focus on long-term supply contracts with semiconductor foundries and OSAT companies.

- Invest heavily in advanced packaging R&D, including 2.5D/3D IC packaging materials.

- Expand manufacturing facilities globally to strengthen supply chain resilience.

- Strong global distribution networks and diversified semiconductor material portfolios.

- High technological expertise in thermal management, substrates, and encapsulation materials.

- Established relationships with major chip manufacturers provide long-term revenue stability.

- High dependency on cyclical semiconductor demand and capital-intensive R&D operations.

- Complex global supply chains expose companies to raw material price fluctuations.

- Slower adaptability due to large-scale operational structures.

Emerging Players: Tanaka Holdings; Siliconware Precision Industries Co., Ltd.; Amkor Technology, Inc.

- Focus on expanding advanced packaging service capabilities and strategic partnerships.

- Increase investments in high-growth packaging technologies such as fan-out wafer-level packaging.

- Target fast-growing AI and automotive semiconductor applications.

- Greater flexibility in adopting new packaging technologies and process innovations.

- Strong positioning in outsourced semiconductor assembly and testing operations.

- Ability to rapidly scale packaging capacity for emerging semiconductor applications.

- Comparatively limited material innovation capabilities versus established chemical giants.

- Dependence on third-party suppliers for advanced packaging materials.

- Higher exposure to competitive pricing pressure and customer concentration risks.

Recent Developments

-

In April 2024, Henkel AG & Co. KGaA commercialized its Loctite Eccobond UF 9000AE capillary underfill encapsulant designed for advanced AI and high-performance computing semiconductor packages. The material supports large body advanced packaging designs, including FCBGA, HD-FO, and 2.5D packaging architectures.

-

In January 2024, Amkor Technology, Inc. and GlobalFoundries expanded their strategic cooperation in Portugal to strengthen Europe’s semiconductor packaging supply chain. The partnership included transfer of 300 mm bump and sort production lines for advanced packaging services.

Semiconductor Packaging Materials Market Report Scope

Report Attribute

Details

Market size in 2025

USD 26.4 billion

Estimated Market size in 2026

USD 28.0 billion

Projected Market size by 2033

USD 43.3 billion

Growth rate

CAGR of 6.4% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Product, application, region

Regional scope

North America; Europe; Asia Pacific; Middle East & Africa; Central & South America

Country scope

U.S.; Canada; Mexico; Germany; UK; France; Italy; China; Japan; India

Key companies profiled

Henkel AG & Co. KGaA; KYOCERA Corporation; Sumitomo Chemical; DuPont; Resonac Corporation; LG Chem; Toray Industries; Tanaka Holdings; Siliconware Precision Industries Co., Ltd.; Amkor Technology, Inc.

Customization scope

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Semiconductor Packaging Materials Market Report Segmentation

This report forecasts revenue growth at regional & country levels and provides an analysis on the industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the semiconductor packaging materials market report based on product, application, and region:

-

Product Outlook (Revenue, USD Billion, 2021 - 2033)

-

Organic Substrates

-

Bonding Wires

-

Leadframes

-

Encapsulation Resins

-

Die Attach Materials

-

Others

-

-

Application Outlook (Revenue, USD Billion, 2021 - 2033)

-

Consumer Electronics

-

Automotive

-

Healthcare

-

IT & Telecommunication

-

Aerospace & Defense

-

Others

-

-

Regional Outlook (Revenue, USD Billion, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

UK

-

Germany

-

France

-

Italy

-

-

Asia Pacific

-

China

-

Japan

-

India

-

-

Central and South America

-

Middle East and Africa

-

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

Regulatory Impact Analysis

Detailed assessment of semiconductor industry regulations, environmental compliance standards, export control policies, RoHS and REACH requirements, semiconductor localization policies, packaging material safety regulations, and government semiconductor incentive programs across major regions.

Helps clients understand compliance obligations, reduce regulatory and supply chain risks, optimize expansion strategies, align packaging material development with global semiconductor standards, and identify regions with favorable semiconductor manufacturing policies.

Competitive Landscape Assessment

Comprehensive benchmarking of semiconductor packaging material manufacturers and OSAT companies based on product portfolio, advanced packaging capabilities, pricing strategies, production capacity, partnerships, innovation activities, and regional presence.

Enables clients to evaluate competitive positioning, identify partnership or acquisition opportunities, understand market differentiation strategies, and strengthen long-term business planning.

Sustainability & ESG Assessment

Analysis of sustainable semiconductor packaging materials including lead-free solders, halogen-free compounds, recyclable substrates, low-carbon manufacturing initiatives, and ESG compliance trends within the semiconductor ecosystem.

Supports clients in meeting sustainability targets, improving ESG performance, complying with environmental regulations, and enhancing brand positioning among electronics manufacturers and investors.

Frequently Asked Questions About This Report

Consumer electronics held the largest share (over 35.9%) in 2025.

The organic substrates segment held the highest revenue share of 37.4% in 2025.

The global semiconductor packaging materials market size was estimated at USD 26.4 billion in 2025 and is expected to reach USD 28.0 billion in 2026.

Asia Pacific dominated with a 42.2% revenue share in 2025.

Some key players in the semiconductor packaging materials market include Henkel AG & Co. KGaA, KYOCERA Corporation, Sumitomo Chemical, DuPont, Resonac Corporation, LG Chem, Toray Industries, Tanaka Holdings, Amkor Technology, Inc., and Siliconware Precision Industries Co., Ltd.

Key factors driving the semiconductor packaging materials market include rising demand for AI chips, 5G devices, electric vehicles, advanced semiconductor packaging technologies, high-performance computing systems, and increasing global semiconductor manufacturing investments.

The global semiconductor packaging materials market is expected to grow at a compound annual growth rate of 6.4% from 2026 to 2033 to reach USD 43.3 billion by 2033.

About the Author(s)

Advanced Interior Materials Research Team

Advanced Materials · Advanced Interior MaterialsThis report was authored by the advanced interior materials research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the advanced interior materials segment of the advanced materials industry. All findings are based on proprietary advanced materials databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.