- Home

- »

- Medical Devices

- »

-

Viral Vector Bioanalytical Testing Services Market Report, 2026-2033GVR Report cover

![Viral Vector Bioanalytical Testing Services Market (2026 - 2033)Report]()

Viral Vector Bioanalytical Testing Services Market (2026 - 2033)

Size, Share & Trends Analysis Report By Test (Titer & Quantification Testing, Safety Testing, Purity & Impurity Analysis), By Viral Vector (Lentiviral Vector, AAV), By Development Stage (Preclinical, Clinical), By End-use, By Region, and Segment Forecasts

Market Size, 2025

$578.5MMarket Estimate, 2026

$625.5MMarket Forecast, 2033

$1,155.7MCAGR, 2026–2033

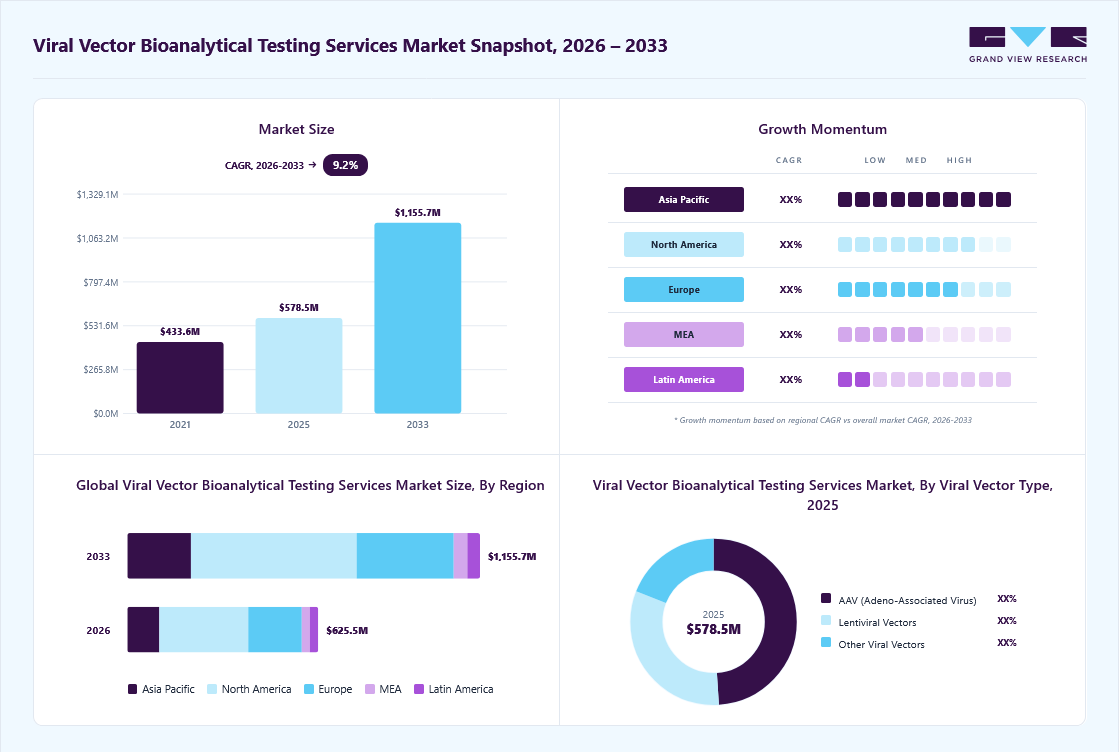

9.2%Viral Vector Bioanalytical Testing Services Market Summary

The global viral vector bioanalytical testing services market size was valued at USD 578.5 million in 2025 and is projected to grow from USD 625.5 million in 2026 to USD 1,155.7 million by 2033, at a CAGR of 9.2% from 2026 to 2033. The North America held the largest share of 46.6% of the global market in 2025. The market growth is attributed to an increasing number of gene and cell therapy pipelines, rising regulatory focus on safety and potency validation, growing demand for AAV and lentiviral vectors, increasing clinical trial activity, and the expansion of biologics and advanced therapeutics, which are increasing testing volumes and outsourcing, in turn, boosting the demand for viral vector bioanalytical testing services.

Key Market Trends & Insights

- By test: Safety testing segment held the largest market share in 2025.

- By viral vector: AAV segment held the largest market share in 2025.

- By development stage: Preclinical segment held the largest share in 2025.

- By end-use: Biopharmaceutical companies segment held the largest share in 2025.

Regional Highlights

- Largest regional market: North America (46.6% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

- By country: The U.S. led the North America market in 2025.

Market Size & Forecast

- Market size in 2025: USD 578.5 Million

- Estimated market size in 2026: USD 625.5 Million

- Projected market size by 2033: USD 1,155.7 Million

- CAGR (2026-2033): 9.2%

The increasing number of clinical pipelines for cell and gene therapies, the rise in stringency in terms of regulatory requirements for characterization of viral vectors, increased use of AAV and lentivirus vectors in gene and cell therapies respectively, growing use of outsourcing by companies for their clinical and preclinical studies, advances in analytical techniques such as digital PCR and NGS, and complexities associated with the development of more complex and sensitive potencies and safety assays contribute towards increased demand for viral vector bioanalysis testing services. Furthermore, with the expansion of clinical pipelines, the need for more repetitive testing and a high volume of testing during clinical phases has increased revenue contribution from clinical phase testing processes.")

In addition, regulatory authorities impose stringent requirements for safety, potency, and purity testing, which would result in increased expenditure for companies developing gene and cell therapies, with a focus on outsourcing testing services through long-term contracts. The aforesaid factors are expected to drive market growth over the forecast period. Additionally, innovations like digital PCR and next-generation sequencing (NGS) help boost sensitivity and efficiency, thus allowing detection of impurities even in very small concentrations while providing better compliance. Thus, the shift from regular assays to valuable testing services is likely to increase the demand for bioanalytical services. Also, outsourcing activities amongst small and medium biotech organizations creates greater reliance on CROs owing to limited capacity within these companies, thus making these companies outsource more frequently.

Nevertheless, the higher prices of bioanalytical testing, along with the lack of uniformity across assays, hinder the use of such technologies by startup companies, and differences in regulatory requirements across regions complicate operations for service providers. Thus, these factors are collectively impacting the market growth of the viral vector bioanalytical testing services industry.

Opportunity Analysis

An increasing number of programs using viral vectors in cell and gene therapy, stringent regulations on vector characterization, and outsourcing activities by small- and medium-scale biopharmaceutical companies are providing numerous opportunities for the growth of the market for viral vector bioanalytical testing services. This is due to increased testing frequency as drugs and metabolites move from preclinical to clinical phases, where biodistribution and immunogenicity tests are mandatory. The late-phase clinical trials also involve batch release and comparability studies, leading to increased revenue per program and the establishment of long-term service contracts. Moreover, the use of cutting-edge analytical systems, such as digital PCR and NGS, has enabled service providers to accurately detect vector genomes, thereby making their testing services more expensive and differentiating them from competitors. Additionally, investment in high-containment laboratory facilities, like BSL-2 and BSL-3 labs, is enabling service providers to conduct viral safety studies that require stringent compliance.

Moreover, an increase in AAV- and lentivirus-based pipeline products for rare disease and cancer treatment applications is driving continuous demand for potency and purity analysis services. Additionally, geographical diversification of clinical trials into regions like the Asia Pacific and the Middle East is enabling regional testing alliances and laboratory growth. Furthermore, comprehensive services that integrate development assistance with analytical testing are contributing to the growing market reach for contract research organizations (CROs) and contract development and manufacturing organizations (CDMOs). Additionally, regulatory harmonization in key regions is promoting multi-region clinical trials, which are enhancing repeat testing across multiple batches. Thus, these factors are likely to open several new opportunities for the viral vector bioanalytical testing service providers.

Impact of U.S. Tariffs on the Viral Vector Bioanalytical Testing Services Market

The tariffs imposed by the U.S. on lab equipment, bioprocessing supplies, and reagents are elevating operating expenses at viral vector test labs, causing upward pressure on prices in the market, with pricing models modified to compensate for the increase. The higher expenses associated with the purchase of PCR reagents, chromatography columns, and cell culture media are impacting pricing related to assays, with rising cost per sample becoming evident for biodistribution and potency analyses.

In addition, small testing labs are experiencing compressed margins due to their smaller scale of operation, driving consolidation towards larger CROs and CDMOs. The U.S.-based service providers are expediting supply chain localization by emphasizing domestic sourcing to mitigate tariffs and ensure supply continuity, but temporarily incurring increased procurement costs. In addition, companies are opting for longer-term contracts to secure pricing and testing fees from fluctuations, providing stable income generation for service providers.

Moreover, the tariff rate will affect the outsourcing strategy adopted by pharmaceutical firms when comparing the costs associated with conducting tests in-house and outsourcing them to an external firm. The capital investment required to establish a laboratory that meets regulatory requirements, which involves purchasing equipment at relatively high prices, acts as an entry barrier for new firms entering the market. In addition, international companies are restructuring their testing processes to achieve the most cost-effective structure, including offshoring some non-critical test operations.

The technological environment of the viral vector bioanalytical testing services market is undergoing changes in line with the growing use of sensitive molecular tests, cell-based functional tests, and analyzers, driven by demand for efficient vector characterization across various developmental phases. The real-time quantitative PCR and digital PCR are common tools for quantifying vector genomes, with digital PCR receiving greater interest owing to its superior sensitivity and absolute quantification capabilities, which ensure accurate dosing. NGS is increasingly used to analyze vector genome integrity and contamination profiles to detect rare mutations that affect product quality. In addition, cell-based assays have become important in assessing the potency of viral vectors, with regulatory bodies mandating functional testing in addition to physio-chemical testing.

Also, immunoassays are useful for immunogenicity testing and host-cell protein detection in safety assessments across different clinical phases. The automation and high-throughput methods are being used to increase the efficiency of sample analysis and decrease turnaround time in large-scale clinical research. The integration of bioinformatics techniques is enabling more thorough interpretation of data from sequencing and biomarker studies, providing a better understanding of vector performance. Thus, these technological advancements in the fields of the bioanalytical testing industry are likely to impact the specialized viral vector services.

The pricing models of the market operate mainly under a Fee-for-Service system, in which each test, including but not limited to titer, potency, and biodistribution, has different charges depending on the study’s complexity and regulatory compliance needs. The more complex the study, the higher the cost incurred, especially for viral shedding and long-term persistence tests, since they have high costs associated with infrastructure and lengthy testing periods.

The project-based pricing is widely used in the market, where testing costs remain consistent across project phases, providing certainty and convenience for biopharmaceutical companies that engage in multiple-phase projects. Similarly, the full-time equivalent model type is another pricing model gaining momentum in the industry, in which service providers allocate dedicated scientific teams for long-term contracts.

Moreover, there has been an increase in the adoption of a hybrid service pricing model that includes both analytical testing and development services. The variations in prices within different regions depend on factors such as labor costs, regulatory compliance, and infrastructure. Nevertheless, the high price of advanced assays and testing equipment has led to premium pricing, whereas competitive pressures favor standardized assays.

Market Concentration & Characteristics

The market growth stage is medium, and growth is accelerating. The market is characterized by the degree of innovation, level of M&A activities, regulatory impact, service expansion, and regional expansion.

The development in the viral vector bioanalytical testing services industry is taking place due to innovations in the use of highly sensitive analytical technologies such as digital PCR, NGS, and potent cell-based assays that help in understanding the characteristics of vectors at various stages of development. The automation and high-throughput screening equipment are significant, as they reduce the time required to conduct tests in large-scale clinical trials.

Stringent regulations enforced by organizations like the FDA and EMA have influenced the market by making it mandatory to conduct extensive characterization of vectors such as biodistribution, shedding, and immunogenicity studies. This has increased the complexity of testing procedures, leading to greater demand for laboratories that comply with GLP and GMP guidelines.

The industry witnesses growing frequency of mergers and acquisitions as companies try to increase their analytical capacities, expand their technological platforms, and enlarge their geographical footprint by acquiring small niche laboratories that specialize in conducting tests related to viral safety, potency, and gene therapy, allowing service providers to diversify their services and compete effectively in an environment with limited capacities.

In addition to performing only analytical tests, service providers provide comprehensive solutions, including assay development, method validation, regulatory affairs, and long-term stability studies, as well as specialized services, such as viral shedding, genome integrity testing, and cell-based functional assays, which have become more popular due to the stringent regulations and complexities of viral vectors.

The geographical locations continue to play an important role in expansion, since testing companies expand their operations into countries such as India and China that provide lower costs and more regulatory compatibility, thus making it more engaging to outsource their bioanalytical testing processes, which improves the availability of test subjects in these locations.

Test Insights

Based on test, the safety testing segment dominated the market with the largest revenue share of 31.7% in 2025, owing to the presence of stringent regulations concerning the safety of viruses, including replication-competent virus testing, adventitious agents, and viral clearance studies, which are required throughout the entire gene therapy pipeline process. In addition, the growing complexity of viral vectors, such as AAV and lentiviral vectors, is expected to drive the demand for advanced safety testing platforms. Furthermore, the growing need to assess patients' long-term responses and vector shedding has generated a constant demand for post-approval follow-up safety testing, especially for in vivo gene therapy vectors for systemic delivery. Similarly, the growing deployment of innovative capsid designs and hybrid vectors will create a greater need for customized safety tests to detect off-target effects and immunological responses. The globalization of multicenter studies will increase the need for safety testing in line with region-specific regulatory requirements.

The potency assays segment is expected to witness noteworthy growth over the forecast period, driven by a shift towards assessing the functionality of viral vectors, which requires cell-based assays to demonstrate biological activities and efficacy. In addition, the number of late-stage clinical trials has increased, driving demand for potency assays, which are essential for batch release and comparability studies. Furthermore, the increased focus on characterizing the dose-response and transgene expression profiles will result in an increased demand for high sensitivity and reproducibility from potency assays throughout the development process. Innovations such as cell-based and reporter gene assays are allowing for more accurate assessment of vector efficacy, encouraging their wider adoption in clinical and preclinical research. Multi-mechanistic therapies, such as gene-modified cell therapies, will generate a demand for specialized potency assays. These factors are collectively impacting the segment’s growth over the forecast period.

Viral Vector Insights

Based on viral vector, the AAV (Adeno-Associated Virus) product segment accounted for the largest revenue share in 2025. This is attributed to the growing use of AAV vectors in approved and late-stage gene therapies, especially those for rare diseases and neurological disorders, which necessitate extensive bioanalysis, including genome quantification, impurity analysis, and biodistribution analysis. The safety features and low immunogenicity associated with AAV vectors, when compared to other viral vectors, have been fueling their adoption for therapeutic applications, resulting in increased demand for testing services.

The lentiviral vectors segment is likely to grow at a notable CAGR, considering the increasing use of lentiviral vectors in ex vivo gene therapy, including the use of CAR-T and genetically engineered cells. The lentiviral vectors are used when stable gene integration and persistent protein expression are required. The clinical trials for the treatment of cancer and hematological disorders will drive demand for testing services, like insertional mutagenesis testing, replication-competent lentivirus testing, and potency testing. Thus, outsourcing these services will be the major driver for the market segment’s growth.

Development Stage Insights

Based on development stage, the preclinical segment accounts for the largest share of the market over the forecast period, owing to the large number of preclinical gene therapy candidates under development, screening procedures involved for the characterization of vectors, and optimization procedures performed before the candidate can be submitted for IND approval. Other factors driving growth in the preclinical segment include the need for repeat tests in biodistribution, shedding, and dose-range determination, as well as the rise in outsourcing discovery-stage analytics to external service providers. In addition, the different vector designs and manufacturing techniques require constant validation, thereby resulting in an increase in tests at the preclinical level.

The clinical segment is projected to have the fastest CAGR over the forecast period, attributed to the growing shift of viral vector-based drugs from Phase I to III studies, increased regulatory pressure on safety and potency tests, and increased complexity of testing per program. Furthermore, the rising popularity of late-stage pipeline and commercial research programs has led to an increase in the need for GMP-certified bioanalytical testing services, resulting in faster growth of this segment. In addition, regulatory bodies mandate uniform, reproducible, and stability testing over prolonged periods, thereby necessitating more extensive testing across various stages of clinical trials.

End-use Insights

Based on end-use, biopharmaceutical companies accounted for the largest revenue share in 2025. The growth of this segment can be attributed to the growing number of gene and cell therapy pipelines within companies, consistent demand for analysis across development phases, and improved management of quality attributes and regulatory filings. Furthermore, biopharmaceutical giants have their specific set of bioanalytical testing services for high-priority projects, including commercialized drugs, which is anticipated to boost the demand for bioanalytical testing services. In addition, the rise in the availability of proprietary technology and viral vector modification technology is expected to fuel internal demand for bioanalytical testing services.

The outsourced service providers (CROs, CMOs, CDMOs) market segment is anticipated to grow at the fastest pace during the analysis period, owing to the increasing trend of outsourcing complex, resource-intensive analysis processes to these external providers. The growth in this segment will be further supported by the increasing needs of small- and mid-size biotech companies, which cannot maintain internal infrastructure and must rely on specialized outsourcing partners to develop and validate tests. In addition, outsourced services provide scalability and access to the latest technology and GMP-compliant testing methods, making them suitable for both early-stage and clinical studies.

Regional Insights

North America viral vector bioanalytical testing services market accounted for the largest revenue share in the global market, accounting for 46.6% in 2025. The region's growth is attributed to the high density of gene and cell therapy developers, the presence of specialized CROs/CDMOs, and the developed infrastructure for testing biologics. North America possesses a well-developed ecosystem of companies developing innovative viral vectors, contract service providers, and academia conducting research on viral vector innovations. Also, there is an increased focus on conducting clinical trials for AAVs and lentiviruses, thus creating a consistent need for bioanalytical testing services.

Furthermore, the availability of advanced technologies and expertise for testing has increased, making the process more efficient and effective. In addition, a favorable funding landscape and a higher number of capital investments are promoting early-stage programs, thereby increasing the volume of testing services.

U.S. Viral Vector Bioanalytical Testing Services Market Trends

The U.S. viral vector bioanalytical testing services industry is the largest market in North America and is projected to hold a significant share over the forecast period. This growth is driven by the growing pipeline of viral vector-based drug products, along with the increased regulatory emphasis on safety, efficacy, and quality of drugs. The U.S. holds a dominant position in terms of the number of clinical trials carried out for gene therapy drugs, which drives steady demand for effective and compliant testing services.

Besides, the presence of key players and specialized service providers contributes to improved access to integrated bioanalytical services. Similarly, outsourcing by the smaller biopharma organizations continues to fuel the market growth in the country. Furthermore, rising expectations from regulators regarding effective testing for validation and comparability add to market complexity. Increased sample volumes in late-stage trials and commercial production lead to a rise in the need for efficient processing in the country’s market.

The Canada viral vector bioanalytical testing services market is expected to grow at a significant CAGR during the forecast period, driven by increased investment in cell and gene therapy research and development and the growing number of early-stage programs. The growing scientific research base, as well as various government initiatives offering funds for research related to advanced therapies and translational research in the country, is likely to impact the demand for bioanalytical testing services. Furthermore, collaboration among the research institutes, universities, and biotechs is resulting in an increase in demand for bioanalytical testing services.

Similarly, the emergence of biotech start-ups with underdeveloped analytical capacity is contributing to the increase in outsourcing services to CROs and CDMOs. In addition, favorable regulatory pathways for innovation and clinical development of treatments based on viral vectors are fueling the demand for such services in the country.

Europe Viral Vector Bioanalytical Testing Services Market Trends

Europe’s viral vector bioanalytical testing services market is experiencing steady expansion, driven by its strong base of gene and cell therapy product developers and an established regulatory environment for advanced therapies. The presence of biotech clusters in major European countries such as Germany, the United Kingdom, and France helps sustain steady pipeline expansion in the market.

Furthermore, the growing number of clinical trials for viral vector-based therapeutic products is driving demand for bioanalytical testing services. Similarly, there is an improvement in service availability due to the presence of expert CROs and CDMOs that can provide bioanalytical testing services following Good Manufacturing Practice (GMP). In addition, there is a need for standardized guidelines for analyzing advanced therapies, given strict regulation by central regulatory bodies. Funding from both public and private sectors for advanced therapeutics increases the research, thus creating demand for bioanalytical services.

TheGermany Viral Vector Bioanalytical Testing Services market is expected to witness significant growth, owing to its strong biotechnology base and research infrastructure. An increasing number of gene and cell therapy innovators is generating high demand for testing in the various phases of development. In addition, collaboration between academia and the biopharmaceutical sector will drive the adoption of these tests in innovations and the development of early-stage pipelines. In addition, the presence of dedicated CROs and CDMOs with highly developed analytical capabilities will facilitate access to testing services. Moreover, a supportive regulatory environment and clinical trial activity are propelling market growth in the country.

The UK viral vector bioanalytical testing services market is expected to grow significantly over the coming years. This growth can be attributed to the presence of biotechnology companies and research institutes in the country. The growing number of developments in gene and cell therapies across end users like the biopharmaceutical companies, CROs, CDMOs, CMOs, and research institutes is expected to create opportunities for bioanalytical testing services in the UK. In addition, active clinical trials and funding from government programs will facilitate increased testing and the development of pipelines. The presence of CROs and CDMOs having advanced testing capacities will further fuel growth in this market. Moreover, favorable regulations for novel therapies will support the steady growth of the market in the country.

Asia Pacific Viral Vector Bioanalytical Testing Services Market Trends

The Asia Pacific viral vector bioanalytical testing services market is expanding rapidly, driven by rising investments in the biotech industry and expanding pipelines for cell and gene therapies in countries such as China, Japan, and South Korea. There is an increasing need for outsourcing services in the form of cost-efficiency, backed by an increase in the number of companies offering specialized bioanalytical services.

In addition, advancements in regulatory frameworks and government initiatives to encourage the use of advanced treatments have led to increased clinical trial activity in this region. The rising investment from sponsors in the form of increased clinical trials and the presence of a large pool of skilled professionals, along with low-cost operations, are contributing to the outsourcing of testing services to this region.

China’s viral vector bioanalytical testing services market experiences high growth opportunities for viral vector bioanalytical testing services due to the fast-growing domestic gene and cell therapy pipelines and government initiatives to promote innovation in the biotechnology industry. Furthermore, there is an increasing number of clinical trials in China, which leads to a higher demand for bioanalytical testing services. In addition, the rise of domestic contract research organizations and contract development and manufacturing organizations will facilitate access to affordable, scalable testing services. The regulatory initiatives are promoting the speeding up of development cycles, thus contributing to market growth in the country.

Japan's viral vector bioanalytical testing services market is projected to witness considerable growth during the forecast period. The Japanese market is technologically advanced in the supply of viral vector bioanalytical testing services, owing to its strong regulatory framework and early adoption of regenerative medicine. There is an increase in the development of gene and cell therapies in Japan, resulting in a high demand for quality analytical testing services. Furthermore, expedited approval processes for innovative therapeutic technologies are contributing to clinical translation and higher demand for analytical testing services. The strong presence of pharmaceutical and specialized service providers is enhancing the efficiency of analytical testing services in Japan.

Furthermore, there has been significant investment in precision medicine and rare diseases research in Japan, leading to an upsurge in the use of viral vector-based treatments that require high levels of analytical validation. In addition, the use of novel bioanalytical technologies, including digital PCR and next-generation sequencing across academic institutions and drug research centers, has increased sensitivity and throughput, enabling efficient bioanalytical testing. These aforementioned factors are expected to boost the market growth in the country.

The India viral vector bioanalytical testing services market is projected to grow considerably in the coming years. India has become a developing market for bioanalysis services for viral vectors due to increased investment in biotechnology and the number of nascent projects in gene and cell therapies. The country has seen an increase in demand for affordable analytical services, driven by the enhanced capacities of CROs and CDMOs. In addition, the abundance of highly qualified scientists, along with improved infrastructure, has helped boost the effectiveness of services.

The bioanalytical testing industry for viral vectors in India is also driven by the growing participation in international clinical trials, where foreign sponsors are utilizing local expertise to analyze samples and generate data. Furthermore, the emphasis on biosimilars and complex biologics is helping improve analytical skills, which indirectly promotes the viral vector testing process. In addition, cost benefits and fast processing times are attracting the small and medium-sized companies abroad who prefer outsourcing.

Latin America Viral Vector Bioanalytical Testing Services Market Trends

Latin America represents an emerging market for viral vector bioanalytical testing services, primarily due to steady growth in biotechnology research and international participation in clinical trials. In countries like Brazil, there is growing interest in developing gene and cell therapies, leading to a preliminary need for testing services. In addition, improved healthcare facilities and regulatory harmonization will facilitate market growth at an early stage.

Latin America still relies on testing services offered by North American and European companies due to inadequate advanced analytical services. In addition, growing government collaborations with biotech companies globally will drive steady growth in the region over the coming years.

The Viral Vector Bioanalytical Testing Services market in Brazil is impacted by factors such as the increasing funding towards research & development and greater engagement in clinical trials. The country is showing interest in gene and cell therapy research, generating demand for bioanalytical testing services. Furthermore, the favorable regulatory environment and the existing research infrastructural facilities are enabling growth in this market.

Middle East and Africa Viral Vector Bioanalytical Testing Services Market Trends

The Middle East and Africa viral vector bioanalytical testing services market is witnessing steady growth. This region is at the nascent stage of the markets due to the gradual evolution of biotechnology research and healthcare facilities. There are limited engagements in clinical trials involving advanced therapeutic applications in this region that have led to the creation of the demand for bioanalytical testing services. In addition, there is still a heavy reliance on CROs and CDMOs outside the region due to a lack of expertise in bioanalytical research.

The South Africa Viral Vector Bioanalytical Testing Services market is growing at a steady pace due to the presence of a promising clinical trial environment and growing participation in global trials. South Africa is seeing increasing adoption of advanced drugs, leading to a need for specialized bioanalytical testing. Furthermore, the research institutes and public health care services play a role in establishing the early pipeline in the country, in turn boosting the demand for bioanalytical testing services in South Africa. Moreover, the lack of local capabilities results in the outsourcing of testing services from other regions. However, the growing investment in the country and the increasing number of collaborations are expected to fuel market growth.

The UAE viral vector bioanalytical testing services market is expected to witness significant growth due to increased investments in biotechnology and healthcare innovation. There is an increasing focus on developing advanced research facilities and on attracting global life sciences companies to invest. The rising interest in precision medicine and advanced therapeutic products is further driving the demand for such testing services across the healthcare industry. On the other hand, outsourcing remains a preferred strategy due to the limited level of local specialization in the field of viral vectors.

Key Viral Vector Bioanalytical Testing Services Company Insights

The key players operating across the market are adopting strategic initiatives such as service launches, mergers & acquisitions, partnerships & agreements, and expansions to gain a competitive edge in the market. For instance, in July 2025, ProBio inaugurated a new 128,000 sq. ft. Good Manufacturing Practice (GMP) facility in Hopewell, New Jersey, for manufacturing plasmid DNA and viral vectors like adeno-associated viruses (AAV) and lentiviral vectors to support CGT. The site provides end-to-end capabilities for process development from manufacturing to a commercial scale, supported by proprietary cell lines, plasmid systems, and quality control.

Key Viral Vector Bioanalytical Testing Services Companies:

The following key companies have been profiled for this study on the viral vector bioanalytical testing services market.

- Charles River Laboratories

- Eurofins Scientific

- WuXi AppTec.

- Avance Biosciences Inc.

- SGS SA

- Laboratory Corporation of America Holdings (LabCorp)

- Catalent, Inc.

- Lonza Group

- KBI Biopharma

- Prolytix

Recent Developments

-

In April 2026, the DINAMIQS company received approval from Swissmedic for GMP manufacturing and testing of viral vectors, which led to the release of gene therapy products under regulated conditions. The facility integrates all stages of process development, manufacturing, fill-finish operations, and quality control testing of products. This has strengthened the company's position as one of the key players providing comprehensive solutions for advanced therapies development, including bioanalytical and viral vector testing.

-

In May 2024, Charles River developed a new technology transfer program, including both modular and fast-track approaches, which helps in the overall process and assay transfer. This program enables smooth transitions to the company's center of excellence for viral vectors. In addition, the strategy involves bioanalytical testing activities to ensure the uninterrupted and timely development of gene therapy programs.

Viral Vector Bioanalytical Testing Services Market Report Scope

Report Attribute

Details

Market size in 2025

USD 578.5 million

Estimated market size in 2026

USD 625.5 million

Projected market size by 2033

USD 1,155.7 million

Growth rate

CAGR of 9.2% from 2026 to 2033

Actual Data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Test, viral vector, development stage, end-use, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; UK; Germany; France; Italy; Spain; Denmark; Sweden; Norway; Japan; China; India; Thailand; South Korea; Australia; Brazil; Argentina; South Africa; Saudi Arabia; UAE; Kuwait; Oman; Qatar

Key companies profiled

Charles River Laboratories; Eurofins Scientific; WuXi AppTec; Avance Biosciences Inc.; SGS SA; Laboratory Corporation of America Holdings (LabCorp); Catalent, Inc.; Lonza Group; KBI Biopharma; Prolytix

Customization scope

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Viral Vector Bioanalytical Testing Services Market Report Segmentation

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global viral vector bioanalytical testing services market based on test, viral vector, development stage, end-use, and region:

-

Test Outlook (Revenue, USD Million, 2021 - 2033)

-

Titer & Quantification Testing

-

Safety Testing

-

Purity & Impurity Analysis

-

Potency Assays

-

Other Tests

-

-

Viral Vector Outlook (Revenue, USD Million, 2021 - 2033)

-

AAV (Adeno-Associated Virus)

-

Lentiviral Vectors

-

Other Viral Vectors

-

-

Development Stage Outlook (Revenue, USD Million, 2021 - 2033)

-

Preclinical

-

Clinical

-

-

End-use Outlook (Revenue, USD Million, 2021 - 2033)

-

Biopharmaceutical Companies

-

Outsourced Service Providers (CROs, CMOs, CDMOs)

-

Others

-

-

Regional Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

UK

-

Germany

-

France

-

Italy

-

Spain

-

Denmark

-

Sweden

-

Norway

-

-

Asia Pacific

-

Japan

-

China

-

India

-

Australia

-

Thailand

-

South Korea

-

-

Latin America

-

Brazil

-

Argentina

-

-

Middle East & Africa

-

South Africa

-

UAE

-

Saudi Arabia

-

Kuwait

-

-

Frequently Asked Questions About This Report

North America dominated with a 46.6% revenue share in 2025.

Asia Pacific is the fastest-growing region over the forecast period.

The AAV (Adeno-Associated virus) product segment held the largest revenue share in 2025.

The preclinical segment held the largest revenue share in 2025, while clinical is the fastest-growing stage.

Biopharmaceutical companies segment held the largest share in 2025, while outsourced service providers (CROs, CMOs, CDMOs) is the fastest-growing segment.

Safety testing held the largest market share of 31.7% share in 2025. The segment growth is attributed to the presence of stringent regulations concerning the safety of viruses, including replication-competent virus testing, adventitious agents, and viral clearance studies, which are required throughout the entire gene therapy pipeline process.

Key players include Charles River Laboratories; Eurofins Scientific; WuXi AppTec; Avance Biosciences Inc.; SGS SA; Laboratory Corporation of America Holdings (LabCorp); Catalent, Inc.; Lonza Group; KBI Biopharma; Prolytix.

The global viral vector bioanalytical testing services market size was valued at USD 578.5 million in 2025 and is estimated at USD 625.5 million for 2026.

The global viral vector bioanalytical testing services market is expected to grow at a CAGR of 9.2% from 2026 to 2033, reaching USD 1,155.7 million by 2033.

Some of the key factors driving market growth include an increasing number of gene and cell therapy pipelines, rising regulatory focus on safety and potency validation, growing demand for AAV and lentiviral vectors, increasing clinical trial activity, and the expansion of biologics and advanced therapeutics, which are increasing testing volumes and outsourcing, further boosting the demand for viral vector bioanalytical testing services.

About the Author(s)

Medical Devices Research Team

Healthcare · Medical DevicesThis report was authored by the medical devices research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the medical devices segment of the healthcare industry. All findings are based on proprietary healthcare databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.