- Home

- »

- Paints, Coatings & Printing Inks

- »

-

Coating Additives Market Size & Share Report, 2026-2033GVR Report cover

![Coating Additives Market (2026 - 2033)Report]()

Coating Additives Market (2026 - 2033)

Size, Share & Trends Analysis Report By Additive (Defoamers, Dispersants, Thickeners, Opacifiers), By Formulation (Water-Based, Solvent-Based), By Application, By Region, And Segment Forecasts

Market Size, 2025

$11.4BMarket Estimate, 2026

$12.1BMarket Forecast, 2033

$18.8BCAGR, 2026–2033

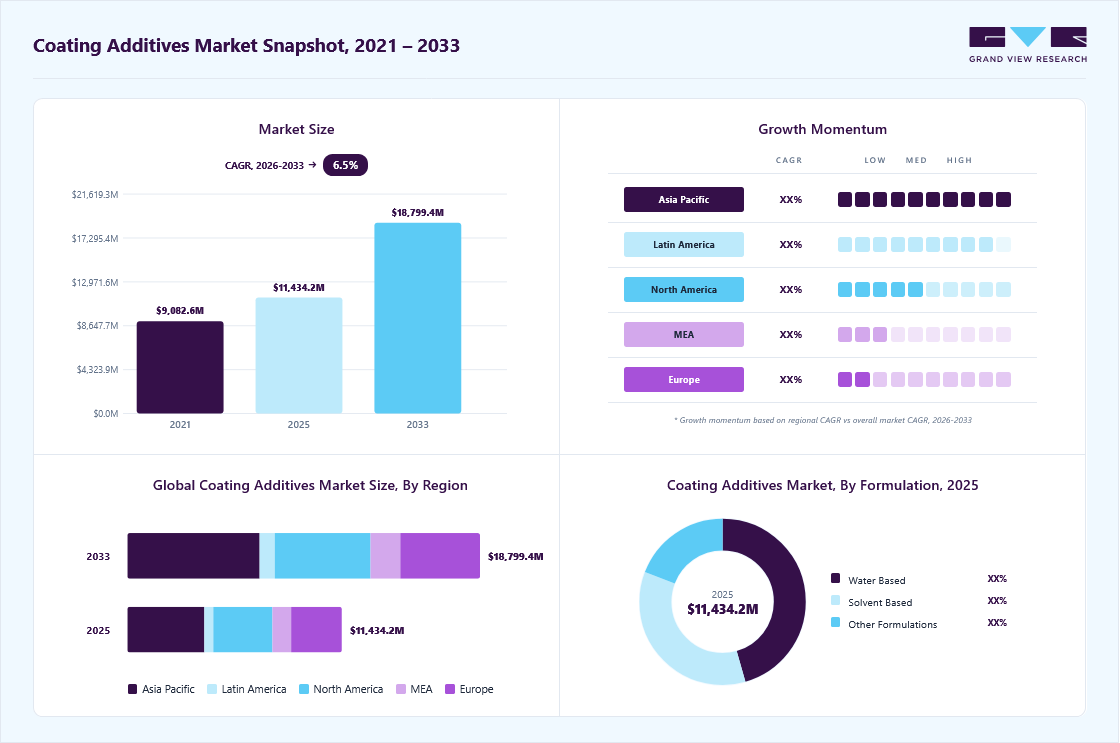

6.5%Coating Additives Market Summary

The global coating additives market size was valued at USD 11.4 billion in 2025 and is projected to grow from USD 12.1 billion in 2026 to USD 18.8 billion by 2033, at a CAGR of 6.5% from 2026 to 2033. Asia Pacific held the largest revenue share of 35.9% of the global market in 2025. Market growth is driven by a rising focus on sustainable coatings and environmentally friendly formulations.

Key Market Trends & Insights

- By additive: Thickeners segment held the largest market share of 37.6% in 2025.

- By formulation: Water-based segment held the largest market share of 45.5% in 2025.

- By application: Architectural coating additives segment held the largest market share of 53.5% in 2025.

Regional Highlights

- Largest regional market: Asia Pacific (35.9% market share, 2025)

- Fastest-growing regional market: Asia Pacific

- By country: China held the largest market share in 2025.

Market Size & Forecast

- Market size in 2025: USD 11.4 Billion

- Estimated market size in 2026: USD 12.1 billion

- Projected market size by 2033: USD 18.8 billion

- CAGR (2026-2033): 6.5%

Manufacturers and end-users are increasingly seeking to reduce the use of hazardous chemicals, lower carbon emissions, and transition away from fossil-based raw materials. This shift is further supported by national environmental regulations, corporate sustainability initiatives, and growing demand for safer, biodegradable, and renewable coating additives across industries such as automotive, construction, and industrial applications.

")

A key application driving the growth of the coating additives industry is architectural and industrial coatings, closely linked with the broader paints coatings additives market as demand rises for high-performance and sustainable formulations. With increasing emphasis on reducing VOC emissions and improving coating performance, manufacturers are rapidly adopting advanced additives that enhance dispersion, flow, leveling, and surface protection. Additives such as rheology modifiers, wetting agents, dispersants, and defoamers are being widely used to improve durability, gloss retention, and application efficiency in waterborne and high-solid coatings. Leading construction, automotive, and industrial coating producers are actively collaborating with additive suppliers to develop formulations that meet evolving regulatory standards and sustainability goals. As a result, architectural and industrial coatings remain among the most dynamic and commercially impactful application segments within the coating additives industry, while adjacent segments such as the wood coating additives continue to benefit from similar performance-driven innovations.

In the automotive and industrial manufacturing sectors, specialty coating additives are increasingly utilized to enhance surface performance and long-term protection. These additives play a critical role in improving scratch resistance, corrosion protection, UV stability, and chemical resistance of coatings applied to metal, plastic, and composite substrates. Anti-settling agents, adhesion promoters, slip additives, and technologies associated with defoaming coating additives are particularly important for ensuring consistent film formation and superior finish quality. Their ability to improve coating efficiency while reducing material consumption and rework aligns well with sustainability-driven manufacturing practices. Consequently, coating additives support resource efficiency, extended product life cycles, and compliance with environmental regulations across diverse end-use industries, including applications related to packaging coating additives.

The marine and energy sectors are also witnessing increased adoption of high-performance coating additives driven by the need for enhanced durability under extreme operating conditions. Advanced additives are being developed to improve anti-fouling properties, thermal stability, and resistance to moisture, chemicals, and abrasion. These innovations help reduce maintenance cycles, lower lifecycle costs, and minimize environmental impact by extending coating service life. Additionally, the development of multifunctional additives supports simplified formulations and reduced additive loadings, contributing to sustainable coating systems used across industries such as infrastructure, marine, and applications involving paper coating additives. Such advancements align with global efforts to improve asset protection while advancing environmentally responsible coating technologies.

Market Dynamics

The growing demand for advanced coatings with enhanced durability, scratch resistance, UV stability, rheology control, wetting performance, and anti-foaming properties is significantly driving the coating additives market. Coating additives play a critical role in improving coating functionality, application efficiency, surface appearance, and long-term performance across architectural, automotive, industrial, wood, packaging, and marine coatings.

In addition, rising environmental regulations and sustainability initiatives are accelerating the transition toward low-VOC, waterborne, powder, and bio-based coatings, thereby increasing the need for specialized additives compatible with environmentally friendly formulations. Manufacturers are increasingly investing in innovative additive chemistries to support high-performance coatings while meeting evolving regulatory and customer requirements.

The coating additives market is highly dependent on petrochemical-derived raw materials and specialty chemical intermediates, making manufacturers vulnerable to fluctuations in crude oil prices, feedstock availability, and energy costs. Variations in pricing for acrylics, silicones, fluorochemicals, and other specialty additive components can significantly impact production economics and profit margins.

Market Concentration & Characteristics

The coating additives market is moderately fragmented, with market leadership concentrated among several large, globally integrated chemical manufacturers. These key players leverage economies of scale, in-house formulation capabilities, and access to advanced raw materials, including specialty polymers, surfactants, and functional resins, to maintain a competitive advantage. Their integration across the coating additives value chain, from raw material synthesis and additive formulation to application testing and technical services, enables improved cost efficiency, consistent product performance, and reliable supply. This strategic positioning enables them to effectively serve a wide range of end-use industries, including architectural coatings, automotive, industrial manufacturing, marine, and construction, thereby reinforcing their market presence and supporting the adoption of high-performance, sustainable coating solutions.

At the same time, emerging players in Asia Pacific and the Middle East are steadily expanding their presence, particularly across segments such as paints and coatings additives, packaging coating additives, and paper coating additives, by leveraging cost-competitive manufacturing bases, improving technical capabilities, and responding to rising regional demand for advanced coating solutions. These producers are supported by targeted investments in additive formulation facilities and application laboratories located within major industrial and economic corridors. Their focus is on delivering scalable, performance-oriented additives for high-growth segments such as architectural coatings, industrial finishes, and construction materials and specialized solutions such as wood coating additives and defoaming coating additives. This evolving landscape marked by consolidation among established multinational suppliers alongside regional capacity expansion, continues to reshape competitive dynamics within the global coating additives industry.

However, the market also faces key challenges, including increasing environmental and regulatory scrutiny of certain additive chemistries used in coatings, such as specific surfactants, amine-based dispersants, and functional modifiers. Regulatory authorities in North America and Europe are placing greater emphasis on evaluating ecotoxicity, long-term persistence, and potential health impacts, even for additives designed to improve coating sustainability. These factors highlight the growing importance of regulatory compliance, continuous R&D innovation, and transparent risk assessment in supporting long-term market growth.

Additive Insights

Thickeners represent the dominant segment in the coating additives industry, accounting for the largest revenue share of 37.6% in 2025, primarily due to their critical role in controlling viscosity, flow behavior, and application performance of coatings. These additives are widely used across waterborne, solvent-borne, and high-solid coating systems to ensure uniform film thickness, prevent sagging, and improve stability during storage and application. Commonly used thickener chemistries include cellulosic thickeners, associative thickeners, and synthetic polymer-based systems, each offering tailored rheological control for specific coating formulations. Their widespread adoption across architectural, industrial, and automotive coatings continues to support strong demand, particularly as manufacturers increasingly shift toward low-VOC and water-based formulations that require advanced rheology modification.

In addition to thickeners, the coating additives market encompasses a broad range of functional additives that play essential roles in formulation performance. Defoamer coating additives are widely used to eliminate surface foam and entrapped air during manufacturing and application, ensuring smooth finishes and defect-free coatings. Dispersants enhance pigment stability and color consistency by preventing agglomeration, while opacifiers improve hiding power and brightness, particularly in architectural and decorative coatings. Other additives including wetting agents, slip modifiers, adhesion promoters, and anti-settling agents further optimize coating behavior, durability, and application efficiency. Together, these additives form an integrated formulation toolkit that enables coating manufacturers to meet increasingly stringent performance, regulatory, and sustainability requirements.

Formulation Insights

Water-based formulations dominate the market, accounting for the largest revenue share of 45.5% in 2025, driven by the global shift toward low-VOC, environmentally compliant coating systems. These formulations rely heavily on advanced additives such as dispersants, thickeners, wetting agents, and defoamers to achieve optimal stability, flow, and film performance in aqueous environments. Water-based coatings are widely adopted across architectural, automotive refinishing, industrial, and wood coating applications due to their reduced environmental impact, improved workplace safety, and compliance with increasingly stringent air quality regulations. Ongoing R&D efforts are focused on enhancing water resistance, corrosion protection, and drying efficiency, further supporting the continued dominance of water-based formulations.

Solvent-based formulations continue to maintain a significant presence in the coating additives market, particularly in applications requiring superior chemical resistance, fast curing, and high-performance finishes. These systems are commonly used in heavy-duty industrial, marine, and protective coatings, where exposure to harsh environments necessitates robust performance characteristics. Additives used in solvent-based formulations are designed to improve pigment dispersion, surface wetting, and film uniformity while minimizing defects such as cratering and orange peel. Although regulatory pressure has moderated growth, innovation in low-solvent and high-solid systems is helping sustain demand in specialized end-use segments.

Application Insights

Architectural coating additives dominated the coating additives industry, accounting for a revenue share of 53.5% in 2025, supported by sustained growth in residential, commercial, and infrastructure construction. These additives are essential for improving the application performance, durability, and aesthetics of architectural coatings, particularly in water-based and low-VOC systems. Key functions include viscosity control, enhanced dispersion, improved flow and leveling, color development, and long-term resistance to weathering and abrasion. The increasing focus on sustainable construction materials and energy-efficient buildings has further accelerated demand for advanced additives that enable compliance with environmental regulations while maintaining high coating performance. Continuous renovation activity, urbanization, and rising consumer preference for durable, visually appealing finishes continue to reinforce the dominance of architectural coating additives in the overall market.

Other application segments, including automotive and OEM, wood finishes, general industrial finishes, and marine coatings, also contribute significantly to market demand, driven by their specialized performance requirements. Automotive and OEM coatings rely on additives to enhance surface smoothness, scratch resistance, corrosion protection, and UV stability, while wood finishes require additives that improve penetration, clarity, and moisture resistance without compromising natural appearance. General industrial finishes utilize additives to ensure consistent film formation, chemical resistance, and operational efficiency across diverse substrates. Meanwhile, marine coatings demand highly specialized additives to withstand harsh environments, including saltwater exposure and fouling. Collectively, these applications highlight the critical role of coating additives in enabling performance, durability, and sustainability across a broad range of end-use industries.

General industrial finishes represent the second-largest application segment in the global coating additives market, driven by rising demand for durable, high-performance coatings across manufacturing, infrastructure, and heavy industrial applications. Industries are increasingly focused on extending asset life, improving operational efficiency, and meeting stringent environmental and safety standards, which has accelerated the adoption of advanced coating additives. These additives are widely used in coatings applied to machinery, equipment, metal structures, pipelines, and fabricated components, where they enhance corrosion resistance, abrasion durability, chemical stability, and surface uniformity. The shift toward water-based, high-solid, and low-VOC industrial coatings has further increased reliance on functional additives such as dispersants, thickeners, wetting agents, and defoamers to maintain performance under demanding operating conditions.

Additionally, general industrial finishes benefit from ongoing innovation in additive technologies that support lightweight materials, energy-efficient production, and sustainable manufacturing practices. Additives play a critical role in enabling consistent film formation, faster curing, and reduced material waste, helping manufacturers lower total coating costs while improving environmental performance. The growing use of automated and high-speed coating processes in industrial settings has also increased demand for additives that ensure process stability and defect-free finishes. Beyond traditional industrial equipment, demand is expanding across renewable energy infrastructure, transportation assets, and industrial maintenance coatings. As regulatory requirements tighten and industries prioritize lifecycle efficiency, general industrial finishes continue to play a pivotal role in driving innovation and sustained growth.

Regional Insights

The Asia Pacific region dominated the global coating additives market, accounting for a 35.9% revenue share in 2025, driven by rapid industrialization, urbanization, and strong growth in construction, automotive, and manufacturing activities. The region is a major hub for the production of architectural, industrial, and automotive coatings, driving sustained demand for performance-enhancing additives. Rising adoption of water-based and low-VOC coating systems across Asia Pacific aligns closely with regional environmental objectives focused on reducing emissions and improving workplace safety. Coating additives play a critical role in enabling these transitions by improving dispersion, rheology control, film formation, and durability in environmentally compliant formulations.

In addition, supportive regulatory frameworks, infrastructure investment, and expanding manufacturing ecosystems across key economies such as China, India, Japan, and Southeast Asia are accelerating market growth. Governments in the region are increasingly promoting sustainable construction practices and cleaner industrial production, encouraging coating manufacturers to adopt advanced additive technologies. Strong local production capabilities, combined with ongoing R&D investments by both multinational and regional suppliers, further enhance Asia Pacific’s competitive position. These factors, along with rising demand for high-performance coatings in residential, commercial, and industrial applications, continue to reinforce the region’s leadership in the global market.

China Coating Additives Market Trends

The China coating additives industry held a substantial share of 41.0% in 2025, driven by the country’s strong presence in coatings manufacturing and its extensive use across construction, automotive, and industrial applications. Coating additives are increasingly used in China to enhance formulation performance, process efficiency, and environmental compliance, particularly in water-based and low-VOC coating systems. These additives support critical functions such as viscosity control, pigment dispersion, surface protection, and film durability while remaining compatible with evolving regulatory and sustainability requirements. Unlike conventional high-solvent formulations, advanced additive-enabled coatings help reduce emissions, improve workplace safety, and extend coating service life. Functional additives such as thickeners, dispersants, defoamers, and wetting agents demonstrate how formulation innovation is replacing traditional chemistries with more efficient, high-performance solutions. Their widespread adoption supports regulatory compliance, improves application consistency, and strengthens the competitive positioning of coating manufacturers operating in China.

North America Coating Additives Market Trends

The North America coating additives industry is witnessing robust growth, accounting for a significant value share of 27.6% in 2025, supported by stringent environmental regulations, strong sustainability commitments by manufacturers, and the increasing adoption of low-VOC and high-performance coating systems across industries. Regulatory oversight from agencies such as the U.S. Environmental Protection Agency (EPA) and Environment and Climate Change Canada is accelerating the transition toward environmentally compliant coating formulations, thereby increasing demand for advanced additives. Coating additives are widely used across architectural, automotive, industrial, packaging, and protective coatings to improve application efficiency, durability, and emission control. The automotive and construction sectors remain key contributors, driven by demand for lightweight materials, corrosion-resistant coatings, and sustainable building solutions. Additionally, strong investments in R&D, advanced formulation technologies, and process optimization are supporting innovation and commercialization of next-generation coating additives. Growing emphasis on sustainable products, regulatory transparency, and supply chain reliability further reinforces North America’s position as a major market for coating additives.

U.S. Coating Additives Market Trends

The U.S. coating additives industry has witnessed notable growth, accounting for a dominant share of 76.7% in 2025, supported by stringent environmental regulations, rising sustainability awareness, and strong demand from construction, automotive, and industrial sectors. Regulatory frameworks enforced by agencies such as the U.S. Environmental Protection Agency (EPA) are accelerating the shift toward low-VOC, water-based, and high-performance coating systems, increasing reliance on advanced additive technologies. Coating additives are widely used to enhance application properties, durability, and surface performance in architectural, automotive OEM, and industrial coatings. Additionally, the expansion of electric vehicle manufacturing, infrastructure development, and refurbishment activities is driving demand for coatings that offer corrosion resistance, thermal stability, and long-term protection. As sustainability and performance become key purchasing criteria for manufacturers and end users, coating additives play a critical role in regulatory compliance, product differentiation, and reducing the overall environmental footprint of the U.S. coatings industry.

Europe Coating Additives Market Trends

The Europe coating additives industry is experiencing steady growth, accounting for a revenue share of 23.6% in 2025, driven by stringent environmental regulations, strong sustainability initiatives, and widespread adoption of advanced coating technologies across industries. Regulatory frameworks such as REACH, the EU Green Deal, and the Circular Economy Action Plan are encouraging manufacturers to replace conventional additives with bio-based, biodegradable, and low-toxicity alternatives. Coating additives are widely used across architectural, automotive, industrial, and protective coatings to enhance performance, durability, and compliance with environmental standards. The automotive and construction sectors, in particular, are increasingly adopting water-based formulations, bio-based polymers, and eco-friendly additives to meet carbon reduction and low-VOC emission targets. Additionally, growing consumer demand for sustainable products, circular manufacturing practices, and transparent supply chains is accelerating market adoption. Supported by strong R&D capabilities, collaborative innovation between industry and research institutions, and policy incentives, Europe continues to play a leading role in shaping the global market.

The Germany coating additives market is witnessing steady growth, driven by stringent environmental regulations, strong industrial sustainability commitments, and the country’s robust manufacturing and construction sectors. Germany’s automotive, industrial, and protective coatings industries are increasingly adopting water-based formulations, bio-based polymers, and low-toxicity additive technologies to enhance performance, durability, and environmental compliance. Functional additives such as thickeners, dispersants, defoamers, and rheology modifiers are widely used across vehicle coatings, industrial machinery, and architectural applications to improve film formation, corrosion resistance, and surface quality. Regulatory frameworks including REACH and the EU Green Deal further support the shift toward sustainable, low-emission formulations. Additionally, Germany’s emphasis on circular manufacturing, energy-efficient processes, and eco-friendly supply chains is accelerating adoption of high-performance, sustainable coating additives. As environmental responsibility becomes a core priority for both manufacturers and end users, advanced coating additives are playing a pivotal role in enabling regulatory compliance, operational efficiency, and innovation across Germany’s industrial and automotive ecosystems.

Middle East & Africa Coating Additives Market Trends

The Middle East and Africa (MEA) coating additives industry is gradually gaining momentum, driven by infrastructure expansion, sustainability initiatives, and increasing regulatory focus on environmental protection. Governments across the region are encouraging the adoption of water-based, bio-based, and low-toxicity coating additives to reduce reliance on conventional petrochemical formulations and support long-term industrial resilience. Advanced additives are finding growing application in architectural, industrial, automotive, and protective coatings, particularly in countries investing heavily in construction, urban development, and manufacturing. In the Middle East, access to cost-competitive energy and industrial feedstocks supports scalable additive production, while in Africa, rising demand for durable, environmentally compliant coatings in construction, automotive, and consumer goods is driving market adoption. Increasing foreign investment, technology partnerships, and awareness of circular-economy practices are expected to further accelerate the uptake of high-performance, sustainable coating additives across the MEA region.

Latin America Coating Additives Market Trends

The Latin America coating additives industry is experiencing steady growth, supported by abundant renewable feedstock, expanding sustainability initiatives, and increasing regulatory focus on environmental protection. The region benefits from strong availability of biomass, sugarcane, and agricultural residues, which enable the production of bio-based coating additives such as thickeners, dispersants, defoamers, and bio-based polymers. Advanced additives are increasingly adopted across architectural, industrial, automotive, and packaging coatings to improve performance, durability, and environmental compliance. Countries such as Brazil and Mexico are leading adoption, driven by industrial decarbonization efforts, water-based coating initiatives, and sustainable manufacturing programs. Growing investment in bio-refineries, rising consumer awareness of eco-friendly products, and partnerships between local producers and global chemical companies are expected to further strengthen Latin America’s role in the global market.

Key Coating Additives Company Insights

Some of the key players operating in the Coating Additives market include Dow and BASF SE.

-

BASF SE, headquartered in Ludwigshafen, Germany, is a leading and well-established player in the global coating additives market, recognized for its expertise in chemical innovation and sustainable solutions. The company offers a wide-ranging portfolio of coating additives that enhance performance across architectural, automotive, industrial, and protective coatings. BASF’s additives provide key functionalities such as rheology control, dispersing, defoaming, wetting, corrosion protection, and surface modification, catering to diverse end-use industries including construction, automotive OEM, industrial equipment, wood coatings, and specialty coatings. Its vertically integrated global production network ensures consistent product quality, scalable supply, and strong regional adaptability. BASF’s extensive R&D infrastructure in Germany, the U.S., and Asia focuses on developing advanced and eco-friendly technologies, including low-VOC additives, bio-based formulations, and multifunctional solutions that enable high-performance, environmentally compliant coatings while supporting sustainability and regulatory compliance goals.

Key Coating Additives Companies:

The following key companies have been profiled for this study on the coating additives market.

- BASF SE

- Altana AG

- DOW Inc.

- Nouryon

- Evonik Industries AG

- Arkema

- Eastman Chemical Company

- Ashland Inc.

- Clariant AG

- The Lubrizol Corporation

Competitive Benchmarking

Operating Strategies

Competitive Edge

Weaknesses

Mature Players: BASF SE; DOW Inc.; Evonik Industries AG; Arkema, Clariant AG

- These companies are focusing on expanding high-performance coating additive portfolios for architectural, industrial, automotive, wood, packaging, and protective coating applications.

- Major players are investing heavily in sustainable additive technologies, including low-VOC, waterborne, bio-based, and silicone-free formulations, to align with environmental regulations and evolving customer preferences.

- Companies are strengthening global manufacturing networks, technical service capabilities, and strategic collaborations with coating formulators and OEMs to improve market penetration

- Large players possess broad specialty chemical portfolios and strong global distribution infrastructures.

- Advanced R&D capabilities and diversified additive technologies support continuous product innovation and customized formulation development.

- Established relationships with global coating manufacturers and industrial customers strengthen long-term market positioning.

- Dependence on petrochemical-based specialty raw materials exposes companies to feedstock price volatility and supply chain disruptions.

- Strict environmental regulations related to specialty chemicals and fluorinated additives increase compliance and reformulation costs.

- Large organizational structures may reduce flexibility in responding rapidly to niche or highly customized market requirements.

Emerging Players: Altana AG; Nouryon, Eastman Chemical Company; Ashland Inc.; The Lubrizol Corporation

- These companies are focusing on specialty coating additive technologies and application-specific solutions for high-value coating formulations.

- Players are increasingly emphasizing customized additive systems, sustainable chemistries, and performance-driven solutions for premium industrial and specialty coatings.

- Strategic acquisitions, customer-focused innovation, and expansion into high-growth applications such as EV coatings, packaging, and specialty industrial coatings are being prioritized.

- Specialty-focused players benefit from strong formulation expertise and targeted application knowledge in advanced coating systems.

- Faster innovation cycles and flexible operating models support rapid development of customized additive solutions.

- Strong niche positioning in specialty additives enables differentiation in premium and performance-oriented applications.

- Smaller manufacturing scale and narrower product portfolios compared to multinational chemical leaders may limit participation in highly diversified coating segments.

- Dependence on selected end-use industries may increase exposure to cyclical industrial demand fluctuations.

- Lower economies of scale may impact competitiveness in price-sensitive markets and high-volume commodity coating applications.

Recent Developments

-

In June 2025, Evonik Coating Additives launched TEGO Foamex 8051, the latest addition to its TEGO Foamex line of defoamers, designed specifically for waterborne decorative coatings. This highly efficient siloxane-based defoamer offers superior performance, cost-effectiveness, and compliance with strict environmental regulations. By enabling formulators to achieve smoother finishes, reduce defects, and maintain eco-friendly formulations, such innovations enhance product quality and operational efficiency. Developments like TEGO Foamex 8051 drive market growth by increasing the adoption of high-performance, sustainable coating additives across architectural and industrial applications.

Coating Additives Market Report Scope

Report Attribute

Details

Market size value in 2025

USD 11.4 billion

Estimated Market size in 2026

USD 12.1 bllion

Projected Market size by 2033

USD 18.8 billion

Growth rate

CAGR of 6.5% from 2026 to 2033

Base year for estimation

2025

Historical data

2018 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million, volume in kilotons, and CAGR from 2026 to 2033

Report coverage

Revenue forecast, volume forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Additive, formulation, application, region

Regional scope

North America; Europe; Asia Pacific; Middle East & Africa; Latin America

Country scope

U.S.; Canada; Mexico; Germany; UK; France; Italy; Spain; China; India; Japan; South Korea; Saudi Arabia; South Africa; Brazil; Argentina

Key companies profiled

BASF SE; Altana AG; DOW Inc.; Nouryon; Evonik Industries AG; Arkema; Eastman Chemical Company; Ashland Inc.; Clariant AG; The Lubrizol Corporation

Customization scope

Free report customization (equivalent up to 8 analysts’ working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Coating Additives Market Report Segmentation

This report forecasts revenue & volume growth at the global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2018 to 2033. For this study, Grand View Research has segmented the global coating additives market report based on additive, formulation, application, and region:

-

Additive Outlook (Volume, Kilotons; Revenue, USD Million, 2018 - 2033)

-

Defoamers

-

Dispersants

-

Thickeners

-

Opacifiers

-

Other Additives

-

-

Formulation Outlook (Volume, Kilotons; Revenue, USD Million, 2018 - 2033)

-

Water-Based

-

Solvent-Based

-

Other Formulations

-

-

Application Outlook (Volume, Kilotons; Revenue, USD Million, 2018 - 2033)

-

Architectural

-

Automotive and OEM

-

Wood Finishes

-

General Industrial Finishes

-

Marine

-

Other Applications

-

-

Regional Outlook (Volume, Kilotons; Revenue, USD Million, 2018 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

Italy

-

France

-

UK

-

Spain

-

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

-

Latin America

-

Brazil

-

Argentina

-

-

Middle East & Africa

-

Saudi Arabia

-

South Africa

-

-

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

Regional Segmentation

Detailed regional assessment of coating additives demand across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa, including country-level analysis of architectural, automotive, industrial, wood, packaging, and protective coatings industries. The study further evaluates regulatory trends, the adoption of sustainable coatings, and regional manufacturing dynamics that influence additive consumption.

Identify high-growth regional markets and application hotspots for coating additives. Support regional expansion planning, sales prioritization, distributor strategy development, and investment decisions based on localized coating industry trends and sustainability regulations.

Competitive Benchmarking

Comprehensive benchmarking of coating additive manufacturers based on product portfolio, additive chemistry focus, production capabilities, regional presence, sustainability initiatives, pricing competitiveness, R&D intensity, and end-use industry penetration.

Enable evaluation of competitive positioning, technology leadership, and strategic strengths of major market participants. Support partnership identification, competitive strategy development, and product differentiation planning across specialty and commodity additive segments.

Opportunity Assessment

Identification of emerging growth opportunities across waterborne coatings, powder coatings, EV coatings, industrial maintenance coatings, packaging coatings, wood coatings, and sustainable low-VOC formulations. The assessment includes opportunity mapping by additive type, coating technology, application, and region.

Help stakeholders prioritize the most lucrative application areas and innovation-driven growth segments. Support product development strategy, market entry planning, and long-term business expansion initiatives through targeted opportunity analysis.

Frequently Asked Questions About This Report

Asia Pacific dominated with a 35.9% market share in 2025.

Asia Pacific is expected to remain the fastest-growing region over the forecast period.

The water-based coating additives segment held the largest market share of 45.5% in 2025, while solvent-based formulations continue to maintain a significant market presence.

The architectural coating additives segment held the largest market share of 53.5% in 2025, while other application segments are expected to contribute significantly to market demand.

.The thickeners segment dominated the global coating additives market by product in 2025, accounting for a significant share of 37.6% of overall consumption, driven by their critical role in controlling viscosity, improving stability, and enhancing performance across coatings formulations. Thickeners are extensively used in architectural, industrial, automotive, and wood coatings to ensure smooth application, prevent sagging, improve flow and leveling, and maintain uniform dispersion of pigments and fillers.

.The global coating additives market size was estimated at USD 11.4 billion in 2025 and is expected to reach USD 12.1 billion in 2026.

.Some of the key players operating in the coating additives market include BASF SE, Altana AG, DOW Inc, Nouryon, Evonik Industries AG, Arkema, Eastman Chemical Company, Ashland Inc, Clariant AG, The Lubrizol Corporation.

.The global coating additives market is primarily driven by rising demand from the architectural, automotive, industrial, and protective coatings sectors, supported by increasing focus on sustainability, high-performance formulations, and environmentally friendly production. Growing adoption of thickeners, continuous product innovation, and expanding use of additives in water-based, low-VOC, and bio-based coatings are accelerating market growth.

.The global coating additives market is expected to grow at a compound annual growth rate of 6.5% from 2026 to 2033 to reach USD 18.8 billion by 2033.

About the Author(s)

Paints, Coatings & Printing Inks Research Team

Bulk Chemicals · Paints, Coatings & Printing InksThis report was authored by the paints, coatings & printing inks research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the paints, coatings & printing inks segment of the bulk chemicals industry. All findings are based on proprietary bulk chemicals databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.