- Home

- »

- Advanced Interior Materials

- »

-

Technical Glass Market Size And Share Report, 2026-2033GVR Report cover

![Technical Glass Market (2026 - 2033)Report]()

Technical Glass Market (2026 - 2033)

Size, Share & Trends Analysis Report By Type (Display Glass, Optical Glass, Borosilicate Glass, Specialty Glass), By Application (Automotive, Building & Construction, Electronics, Aerospace), By Region, And Segment Forecasts

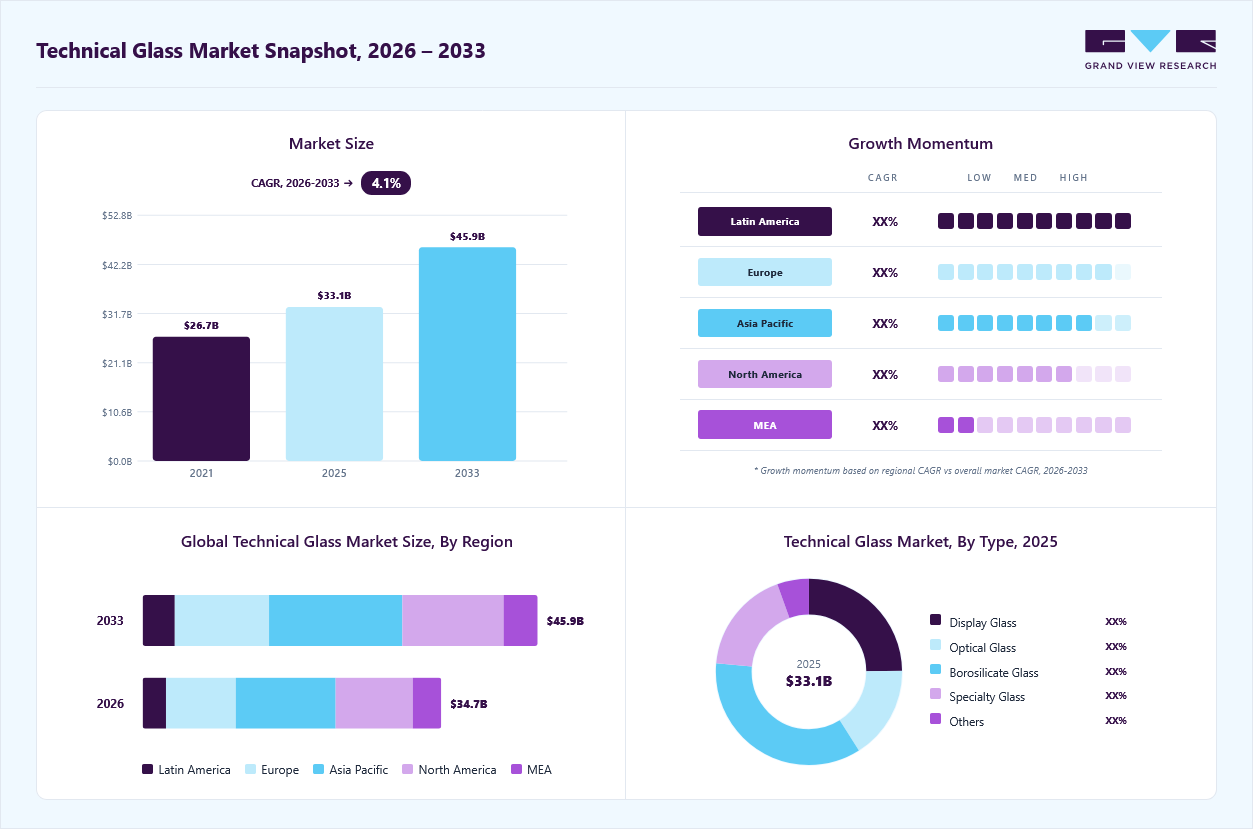

Market Size, 2025

$33.1BMarket Estimate, 2026

$34.7BMarket Forecast, 2033

$45.9BCAGR, 2026–2033

4.1%Technical Glass Market Summary

The global technical glass market size was valued at USD 33.1 billion in 2025 and is projected to grow from USD 34.7 billion in 2026 to USD 45.9 billion by 2033, at a CAGR of 4.1% from 2026 to 2033. The Asia Pacific held the largest share of 33.4% of the global market in 2025. The rapid expansion of the consumer electronics industry primarily drives the market growth.

Key Market Trends & Insights

- By type: Borosilicate glass segment held the largest market share of 35.4% in 2025.

- By application: Electronics segment held the largest market share of 32.1% in 2025.

Regional Highlights

- Largest regional market: Asia Pacific (33.4% revenue share, 2025)

- Fastest-growing regional market: Latin America (highest CAGR, 2026-2033)

- By country: China held the largest share in 2025

Market Size & Forecast

- Market size in 2025: USD 33.1 Billion

- Estimated market size in 2026: USD 34.7 Billion

- Projected market size by 2033: USD 45.9 Billion

- CAGR (2026-2033): 4.1%

With the increasing adoption of smartphones, tablets, wearable devices, and advanced display technologies, there is a strong demand for high-performance glass that offers superior optical clarity, scratch resistance, and durability. The rise of technologies such as flexible displays, augmented reality, and virtual reality has further accelerated the need for specialized technical glass in screens, sensors, and optical components. This continuous innovation in electronics acts as a core engine for market expansion.")

Technical glass products such as low-emissivity glass, insulated glazing, and electrochromic glass are widely used to enhance energy efficiency by regulating heat and light transmission. With stricter environmental regulations and the global push toward green buildings, developers are increasingly adopting advanced glass solutions. Urbanization and large-scale infrastructure development in emerging economies are further boosting demand in this segment.

Modern vehicles, especially electric vehicles, require lightweight, durable, and high-strength glass for applications such as windshields, sunroofs, heads-up displays, and sensors. Similarly, aircraft manufacturing increasingly relies on advanced glass materials for cockpit displays, windows, and instrumentation systems. The shift toward electric mobility and advanced driver-assistance systems is significantly increasing the use of specialty glass, thereby supporting market growth.

These glasses are widely used in laboratory apparatus, diagnostic devices, pharmaceutical packaging, and medical imaging equipment such as X-ray and CT scan systems. Its chemical resistance, thermal stability, and optical precision make it essential in these applications. The increasing demand for high-quality healthcare infrastructure and diagnostic accuracy is driving the adoption of specialized glass materials in the medical sector.

Drivers, Opportunities & Restraints

The technical glass market is primarily driven by strong demand across electronics, construction, automotive, and renewable energy sectors. Rapid advancements in consumer electronics, including high-resolution displays, foldable devices, and sensor-based technologies, are significantly increasing the need for high-performance glass with superior optical and mechanical properties.

Opportunities in the technical glass industry are expanding with technological innovation and emerging applications. The increasing penetration of solar energy systems is creating substantial demand for specialized glass used in photovoltaic modules and solar panels. Additionally, the development of smart glass, electrochromic glass, and flexible glass technologies is opening new avenues in both commercial and consumer applications.

Despite strong growth prospects, the market faces several restraints that could limit expansion. High production and processing costs associated with advanced technical glass, particularly specialty and coated variants, can restrict adoption in price-sensitive markets. The manufacturing process is energy-intensive, making it vulnerable to fluctuations in energy prices and increasing environmental regulations.

Type Insights

The borosilicate glass segment led the market with the largest revenue share of 35.4% in 2025. The rigorous demands of the pharmaceutical and life sciences industries primarily propel the growth of borosilicate glass. The global shift toward biologics, biosimilars, and mRNA-based therapies has intensified the need for Type I borosilicate glass, which is prized for its superior chemical inertness and high hydrolytic resistance. Unlike standard glass, borosilicate prevents the leaching of alkali ions into sensitive drug formulations, ensuring long-term stability and patient safety.

The display glass segment is anticipated to grow at the fastest CAGR during the forecast period. The display glass segment is witnessing strong growth driven by the rapid expansion of the consumer electronics industry. Increasing global demand for smartphones, tablets, laptops, and televisions has significantly boosted the need for high-performance display glass with superior clarity, scratch resistance, and durability. Advancements in display technologies such as OLED, AMOLED, and flexible displays are further accelerating the adoption of specialized glass substrates that offer enhanced thinness, strength, and optical performance.

Application Insights

The electronics segment led the market with the largest revenue share of 32.1% in 2025. These glasses are widely used in components such as display panels, substrates, optical fibers, and protective covers due to their high optical clarity, thermal stability, and electrical insulation properties. The surge in demand for smartphones, wearables, laptops, and advanced computing devices has significantly increased the consumption of specialized glass materials that enable miniaturization, improved performance, and enhanced durability.

The automotive segment is anticipated to register at the fastest CAGR over the forecast period, supported by the increasing integration of advanced glass solutions in modern vehicles. Technical glass is widely used in applications such as infotainment displays, instrument clusters, heads-up displays, and advanced driver assistance systems, where high optical clarity, durability, and resistance to temperature fluctuations are essential. The shift toward connected and autonomous vehicles has accelerated the adoption of high performance display glass and sensor integrated glass components, enabling enhanced driver experience and safety features.

Regional Insights

The technical glass market in North America is strongly driven by the increasing adoption of energy-efficient and sustainable building materials across the construction sector. Stringent regulatory frameworks such as LEED certifications, federal energy codes, and state-level efficiency mandates are pushing developers to incorporate advanced glazing solutions, including low-emissivity and smart glass. This regulatory push, combined with rising awareness of reducing heating and cooling costs, has significantly accelerated the demand for high-performance architectural glass.

U.S. Technical Glass Market Trends

The technical glass industry in the U.S. is largely driven by strong demand from the construction and infrastructure sector, particularly in the context of energy-efficient and sustainable building practices. Increasing adoption of green building standards, along with federal and state regulations aimed at reducing energy consumption, is accelerating the use of advanced glazing solutions such as low-emissivity and smart glass.

Asia Pacific Technical Glass Market Trends

Asia Pacific dominated the global technical glass industry with the largest revenue share of 33.4% in 2025. The Asia Pacific market is primarily driven by rapid urbanization and large-scale infrastructure development across key economies such as China, India, and Southeast Asia. Expanding construction activity, including smart cities, commercial complexes, and high-rise residential buildings, has significantly increased the demand for high-performance and energy-efficient glass solutions. Governments across the region are actively promoting green building standards and sustainable infrastructure, which is accelerating the adoption of advanced technical glass products such as low-emissivity and smart glass.

Europe Technical Glass Market Trends

The technical glass industry in Europe is primarily driven by the region’s strong regulatory push toward sustainability and energy efficiency. Strict frameworks such as the EU Energy Performance of Buildings Directive and broader climate goals under the European Green Deal are accelerating the adoption of advanced glazing solutions, including low-emissivity, triple-glazed, and solar-integrated glass. These regulations are encouraging both new construction and retrofitting activities to reduce carbon emissions and improve thermal insulation, significantly boosting demand for high-performance technical glass across residential and commercial buildings.

Latin America Technical Glass Market Trends

The technical glass industry in Latin America is anticipated to grow at the fastest CAGR during the forecast period, primarily supported by expanding industrialization and the gradual development of regional manufacturing hubs, particularly in countries such as Brazil and Argentina. These economies are witnessing increased investments in infrastructure, construction, and industrial production, which is driving demand for high-performance glass in architectural and industrial applications.

Key Technical Glass Company Insights

Some of the key players operating in the market include AGC Inc., Corning Incorporated, and others

-

AGC Inc., headquartered in Tokyo, Japan, is a glass and materials company and a core member of the Mitsubishi Group. Founded in 1907, the company has evolved from being Japan’s first sheet glass manufacturer into a global leader in glass, electronics materials, chemicals, and ceramics. With a strong international footprint, AGC operates across multiple industries, including construction, automotive, electronics, and life sciences, supported by advanced manufacturing technologies and continuous R&D investments.

-

Corning Incorporated, based in Corning, New York, USA, is a global technology company specializing in glass, ceramics, and advanced materials. Founded in 1851, the company has a long history of innovation in specialty glass and has played a critical role in the development of modern glass technologies. Corning operates through multiple business segments including display technologies, optical communications, environmental technologies, specialty materials, and life sciences, serving industries ranging from telecommunications to consumer electronics.

Key Technical Glass Companies:

The following key companies have been profiled for this study on the technical glass market.

- AGC Inc.

- Corning Incorporated

- Fuyao Glass Industry Group Co., Ltd.

- Guardian Industries

- Nippon Electric Glass Co., Ltd.

- NSG Group

- PPG Industries, Inc.

- Saint-Gobain

- SCHOTT AG

- Xinyi Glass Holdings Limited

Recent Development

-

In December 2025, Nippon Electric Glass Co., Ltd. (NEG), launched the world's first mass production of low-carbon pharmaceutical-grade glass tubing using an all-electric melting furnace at its subsidiary in Selangor, Malaysia.

-

In October 2023, SCHOTT AG launched FIOLAX Pro, a next-generation Type I borosilicate glass tubing designed to address key pharma industry trends, including complex biologics, sustainability, and digitalization.

Technical Glass Market Report Scope

Report Attribute

Details

Market Definition

Market size represents the total annual revenue generated from sale of technical glass used for different applications.

Market size in 2025

USD 33.1 billion

Estimated market size in 2026

USD 34.7 billion

Projected market size by 2033

USD 45.9 billion

Growth Rate

CAGR of 4.1% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative Units

Revenue in USD million/billion, volume in kilotons, and CAGR from 2026 to 2033

Report coverage

Revenue & volume forecast, competitive landscape, growth factors, and trends

Segments covered

Type, application, region

Regional scope

North America; Europe; Asia Pacific; Latin America; Middle East & Africa

Country scope

U.S.; Canada; Mexico; Germany; Italy; France; Russia; China; India; Japan; Brazil; Saudi Arabia; UAE

Key companies profiled

Corning Incorporated; AGC Inc.; Nippon Electric Glass Co., Ltd.; SCHOTT AG; Guardian Industries; Saint-Gobain; NSG Group; Xinyi Glass Holdings Limited; PPG Industries, Inc.; Fuyao Glass Industry Group Co., Ltd.

Customization scope

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Technical Glass Market Report Segmentation

This report forecasts revenue and volume growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global technical glass market report based on the type, application, and region:

-

Type Outlook (Volume, Kilotons; Revenue, USD Million, 2021 - 2033)

-

Display Glass

-

Optical Glass

-

Borosilicate Glass

-

Specialty Glass

-

Others

-

-

Application Outlook (Volume, Kilotons; Revenue, USD Million, 2021 - 2033)

-

Automotive

-

Building & Construction

-

Electronics

-

Aerospace

-

Others

-

-

Regional Outlook (Volume, Kilotons; Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

Italy

-

France

-

Russia

-

-

Asia Pacific

-

China

-

India

-

Japan

-

-

Latin America

-

Brazil

-

-

Middle East & Africa

-

Saudi Arabia

-

UAE

-

-

Frequently Asked Questions About This Report

The global technical glass market size was estimated at USD 33.1 billion in 2025 and is expected to reach USD 34.7 billion in 2026.

The global technical glass market is expected to grow at a compound annual growth rate of 4.1% from 2026 to 2033 to reach USD 45.9 billion by 2033.

The borosilicate glass segment led with a 35.4% revenue share in 2025, while the display glass segment is the fastest-growing.

Some of the key players of the global technical glass market are Corning Incorporated, AGC Inc., Nippon Electric Glass Co., Ltd., SCHOTT AG, Guardian Industries, Saint-Gobain, NSG Group, Xinyi Glass Holdings Limited, PPG Industries, Inc., Fuyao Glass Industry Group Co., Ltd., and others.

The key factor driving the growth of the global technical glass market is the rising demand for high-performance and specialized glass across electronics, automotive, healthcare, and renewable energy applications.

The electronics segment led with a 32.1% revenue share in 2025, while the automotive segment is the fastest-growing.

Asia Pacific dominated with a 33.4% revenue share in 2025.

About the Author(s)

Advanced Interior Materials Research Team

Advanced Materials · Advanced Interior MaterialsThis report was authored by the advanced interior materials research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the advanced interior materials segment of the advanced materials industry. All findings are based on proprietary advanced materials databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.