- Home

- »

- Automotive & Transportation

- »

-

Data Center Logistics Market Size, Share Report, 2026-2033GVR Report cover

![Data Center Logistics Market (2026 - 2033)Report]()

Data Center Logistics Market (2026 - 2033)

Size, Share & Trends Analysis Report By Device Type (Electrical Devices, Mechanical Devices), By Data Center Size, By Service (Transport, Installation, Warehousing & Inventory, Value-added Services), By End Use, By Region, And Segment Forecasts

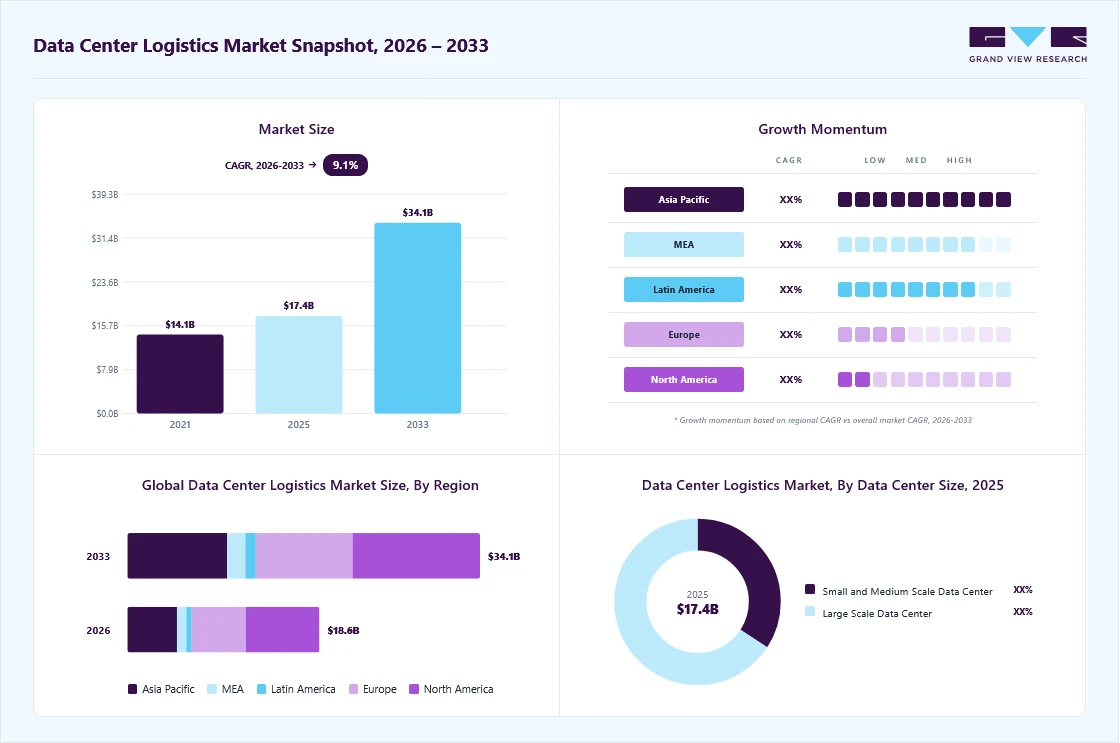

Market Size, 2025

$17.4BMarket Estimate, 2026

$18.6BMarket Forecast, 2033

$34.1BCAGR, 2026–2033

9.1%Data Center Logistics Market Summary

The global data center logistics market size was valued at USD 17.4 billion in 2025 and is projected to grow from USD 18.6 billion in 2026 to USD 34.1 billion by 2033, at a CAGR of 9.1% from 2026 to 2033. The market in North America dominated with a revenue share of 38.7% in 2025. The growth can be attributed to the increasing demand for efficient, specialized logistics solutions, driven by the rapid expansion of digital infrastructure and data center deployments.

Key Market Trends & Insights

- By device type: Electrical devices segment held the largest market share of 68.2% in 2025.

- By service: Transportation segment held the largest market share of 36.5% in 2025.

- By data center size: Large-scale data center segment held the largest market share in 2025.

- By end use: IT and telecommunications segment held the largest market share in 2025.

Regional Highlights

- Largest regional market: North America (38.7% revenue share, 2025)

- By country: The U.S. held the largest market share in 2025

Market Size & Forecast

- Market size in 2025: USD 17.4 Billion

- Estimated market size in 2026: USD 18.6 Billion

- Projected market size by 2033: USD 34.1 Billion

- CAGR (2026-2033): 9.1%

As organizations accelerate their adoption of cloud computing, artificial intelligence workloads, and data-intensive applications, there is a rising need for the seamless transportation, handling, and installation of high-value IT equipment. The rising demand for hyperscale and AI-driven data centers is a key factor driving the growth of the data center logistic market. These facilities accommodate large volumes of servers, storage systems, and networking equipment that require precise handling and specialized installation to prevent damage and ensure operational continuity.The increasing density and complexity of AI workloads further amplify the need for rapid, coordinated, and secure logistics solutions. As a result, logistics providers play a critical role in enabling the safe transportation, efficient deployment, and seamless integration of high-performance infrastructure. By supporting large-scale computing environments, these services help end users maximize uptime, enhance processing capabilities, and scale their AI and cloud operations globally.

")

The shift toward hyperscale and edge computing is significantly transforming logistics requirements. Large hyperscale data centers require bulk transportation, synchronized delivery schedules, and heavy-lift capabilities, while edge data centers demand agile, decentralized logistics networks capable of reaching multiple smaller sites. This dual demand structure increases operational complexity, pushing logistics providers to develop flexible solutions that can handle both large-scale shipments and precise last-mile delivery. The growing need for low-latency processing further accelerates edge deployments, amplifying this trend.

A recent industry development highlights the growing importance of specialized logistics in supporting AI-driven data center expansion. For instance, in April 2026, Arvato is expanding its data center logistics operations in the U.S. by opening a new facility in Denton, Texas, to support growing demand from AI-driven data center construction. The site, located in the Dallas Fort Worth area, will provide specialized services such as high-security warehousing, sensitive hardware handling, and white-glove delivery to hyperscale and cloud infrastructure clients. The expansion reflects the rapid scaling of the data center market, where deployment speed and uptime are increasingly dependent on logistics performance. Similarly, DHL has announced a major expansion of its North American data center logistics network, including multiple planned warehouse sites. Overall, rising investments in AI infrastructure are significantly boosting demand for advanced, secure, and coordinated logistics solutions.

Technological integration within logistics operations is also reshaping the market landscape. Automation in warehousing, digital freight management platforms, and AI-driven route optimization are improving efficiency and reducing turnaround times. These technologies enable better coordination between manufacturers, logistics providers, and data center operators, ensuring timely delivery and installation. As project timelines for data center construction become more compressed, such digital capabilities are becoming essential for maintaining a competitive advantage.

Sustainability considerations are emerging as a strong influence on logistics strategies. With increasing scrutiny on the environmental impact of data centers, logistics providers are adopting greener practices such as optimizing transport routes, using energy-efficient vehicles, and reducing packaging waste. Additionally, reverse logistics, such as the safe removal, recycling, or refurbishment of outdated IT equipment, are gaining importance. This focus on sustainability not only helps meet regulatory expectations but also aligns with the broader environmental goals of data center operators and their clients.

Device Type Insights

The electrical devices segment led the data center logistics industry, accounting for the largest share of 68.2% in 2025. The growth can be attributed to the increasing deployment of high-performance computing infrastructure across hyperscale and AI-driven data centers. Equipment such as servers, power distribution units (PDUs), uninterruptible power supply (UPS) systems, and networking hardware requires highly controlled logistics environments due to their sensitivity to shock, temperature variations, and electrostatic discharge. As data center operators prioritize uptime and rapid deployment, there is a growing need for specialized logistics services that offer precision handling, real-time tracking, and secure transportation. Additionally, the rising complexity and density of electrical systems in modern data centers are driving demand for white-glove delivery, on-site configuration support, and integrated logistics solutions, thereby accelerating segment growth.

The mechanical devices segment is expected to grow at a significant CAGR during the forecast period. The segment growth is driven by the increasing emphasis on advanced cooling and infrastructure systems required to support high-density data center operations. Mechanical equipment such as cooling units, HVAC systems, liquid-cooling solutions, and server racks is often bulky, heavy, and complex to install, necessitating specialized logistics capabilities, including heavy-lift transportation, rigging, and coordinated on-site deployment. With the growing adoption of liquid cooling and energy-efficient thermal management systems, logistics providers are required to handle more sophisticated and customized equipment.

Data Center Size Insights

The large-scale data center segment accounted for the largest share of the data center logistics market in 2025. The segment dominates the market, driven by the rapid expansion of hyperscale and enterprise cloud infrastructure globally. These facilities are increasingly being developed by major cloud and AI providers to support high-density computing, generative AI workloads, and large-scale data storage requirements. The complexity and scale of these projects involve the deployment of thousands of servers, advanced power systems, and sophisticated cooling infrastructure, creating strong demand for specialized logistics services. This includes secure transportation, coordinated warehousing, staged deliveries, and precise on-site installation of critical IT and mechanical equipment.

The small and medium-scale data center segment is expected to grow at the fastest CAGR over the forecast period.The segment is emerging as a key growth area in the market, supported by the rising adoption of edge computing and localized data processing requirements. These facilities are increasingly being deployed closer to end users to reduce latency and improve service efficiency, particularly in sectors such as retail, healthcare, BFSI, and telecom. Their distributed nature creates frequent, fragmented logistics requirements, driving demand for agile, cost-efficient, and time-sensitive solutions. Services such as short-distance transportation, rapid installation, and modular equipment handling are becoming essential to support these deployments.

Service Insights

The transportation segment accounted for the largest share of the data center logistic industry in 2025 and is expected to grow at the fastest CAGR over the forecast period. The increasing need for secure, timely, and specialized transport of high-value IT infrastructure is driving the segment growth. For instance, in March 2026, DHL Group announced a major expansion of its North America data center logistics infrastructure, adding 10 dedicated warehouse sites with over 7 million sq ft of capacity to support the rapid deployment of hyperscale and colocation data centers. These facilities are designed to provide white-glove handling, rack pre‑configuration, and specialized warehouse‑to‑site transportation for high-value IT hardware such as servers, power modules, and networking systems. DHL aims to reduce on‑site complexity, safeguard equipment, and help data center operators maintain build speed amid compressed schedules and global supply chains.

The installation segment is expected to grow at a significant CAGR during the forecast period, driven by its critical role in enabling the deployment of hyperscale, colocation, and edge data centers. Within data center logistics, installation services involve the precise positioning, assembly, and integration of servers, power systems, cooling units, and networking infrastructure at the site. These services require high levels of coordination and technical expertise to ensure minimal downtime and seamless system functionality. As data centers become more complex due to AI workloads and high-density computing, the demand for accurate and time-efficient installation is increasing. Additionally, the growing adoption of turnkey and full-lifecycle logistics solutions, which include installation as a core offering, is further driving the growth of this segment.

End Use Insights

The IT and telecommunications segment accounted for the largest market share in 2025 and is expected to grow at a significant CAGR during the forecast period. The segment dominates the market, driven by the rapid expansion of cloud computing, hyperscale infrastructure, and digital connectivity services. Major cloud service providers and telecom operators are continuously scaling their data center capacity to support increasing data traffic, AI workloads, and edge computing applications. This ongoing expansion is generating strong demand for specialized logistics services, including the transportation, warehousing, installation, and commissioning of high-value IT equipment such as servers, networking systems, and power infrastructure. Additionally, the rollout of 5G networks and growing adoption of hybrid IT architectures are increasing deployment frequency and complexity, further strengthening the need for secure, time-sensitive, and highly coordinated logistics solutions across the IT and telecommunications ecosystem.

The healthcare segment held a significant share of the data center logistic market in 2025. It is emerging as a significant end-user segment, supported by the rapid digitalization of healthcare services and the increasing reliance on data-driven medical technologies. Hospitals, research institutions, and telemedicine platforms are increasingly adopting electronic health records (EHRs), AI-based diagnostics, and medical imaging systems, all of which depend on robust data center infrastructure. This is driving demand for logistics services that support the deployment and maintenance of critical IT systems, including secure transportation, precise installation, and handling of sensitive computing and networking equipment.

Regional Insights

The North America data center logistics industry dominated the market, accounting for 38.7% share in 2025. The market is witnessing strong growth driven by the rapid expansion of hyperscale cloud infrastructure and increasing adoption of AI and data-intensive applications across enterprises. The region hosts a high concentration of leading cloud service providers and technology companies, which are continuously investing in new data center construction and upgrades to support growing workloads and digital transformation initiatives. This large-scale expansion is generating significant demand for specialized logistics services, including the secure transportation, warehousing, installation, and commissioning of high-value IT and mechanical equipment such as servers, cooling systems, and power infrastructure. Additionally, the increasing complexity of deployments, coupled with compressed timelines and stringent uptime requirements, is pushing logistics providers to adopt advanced tracking, coordinated delivery models, and white-glove handling services.

U.S Data Center Logistics Market Trends

The U.S. data center logistics industry held a significant revenue share in 2025, supported by the country’s high concentration of hyperscale cloud service providers such as Amazon Web Services, Microsoft Azure, and Google Cloud. These companies continue to expand data center capacity and edge computing networks to meet the growing demand for cloud computing, AI workloads, and digital services. This sustained expansion is driving large-scale infrastructure deployment, increasing supply chain complexity, and generating strong demand for specialized logistics services. Activities such as the transportation, staging, installation, and commissioning of high-value IT and mechanical equipment are becoming more critical as deployment timelines shorten. As a result, the need for secure, time-sensitive, and highly coordinated data center logistics solutions continues to rise across the U.S.

Europe Data Center Logistics Market Trends

The Europe data center logistics industry held a significant revenue share in 2025. The rapid expansion of cloud computing, AI-enabled workloads, and the increasing enterprise adoption of hybrid IT infrastructure across the region drive steady growth. Key hubs such as Frankfurt, London, Amsterdam, and Paris continue to attract significant data center investments due to strong digital connectivity, advanced fiber networks, and proximity to major enterprise and financial clients. This expansion is generating strong demand for specialized logistics services, including the transportation, warehousing, installation, and commissioning of high-value IT, power, and cooling equipment. In addition, Europe’s complex regulatory environment, particularly in data protection, sustainability, and cross-border operations, is increasing the need for highly compliant, well-coordinated logistics solutions.

The UK data center logistics market held a significant revenue share in 2025. The UK market is witnessing steady growth, driven by strong demand for cloud computing, financial services digitization, and increasing adoption of AI-enabled applications across enterprises. London and surrounding regions continue to serve as key data center hubs, attracting investments that require specialized logistics support for the movement, installation, and integration of high-value IT infrastructure.

Asia Pacific Data Center Logistics Market Trends

The Asia Pacific data center logistics industry held a significant revenue share in 2025, due to the accelerated adoption of cloud computing, artificial intelligence, and digital transformation initiatives across industries. Countries such as China, India, Japan, and Singapore are driving the market with large-scale hyperscale data center investments and rapid infrastructure expansion. The proliferation of 5G networks and edge computing deployments is driving demand for advanced data center logistics services to ensure efficient deployment, low-latency performance, and seamless integration of IT infrastructure across distributed locations.

The China data center logistics market is expected to grow significantly over the forecast period. The China market is growing rapidly, supported by large-scale hyperscale infrastructure expansion and the rapid adoption of AI and cloud computing. Strict data localization requirements and ongoing domestic data center buildouts are driving demand for secure, highly coordinated logistics services.

The data center logistics market in Japan is expected to grow at a significant CAGR over the forecast period. The market growth is driven by increasing investments in AI, robotics, and high-performance computing infrastructure, particularly in urban hubs like Tokyo and Osaka. The growing demand for resilient, energy-efficient data centers is driving the need for precise, high-security logistics for the deployment of advanced IT equipment.

The India data center logistics market is expected to grow at the fastest CAGR over the forecast period. The market is expanding rapidly due to strong growth in digital services, cloud adoption, and government-led digitalization initiatives. Rising hyperscale investments and edge data center deployments are driving demand for scalable and cost-efficient logistics solutions across multiple cities.

Key Data Center Logistics Company Insights

Some of the key companies in the data center logistics market include DHL Group; Expeditors International of Washington, Inc.; GXO Logistics Inc.;Kuehne+Nagel; and Logistics Plus Inc. These companies focus on product innovation, R&D, and strategic initiatives, including new product launches, business expansions, partnerships, collaborations, and mergers and acquisitions.

-

DHL Group offers end-to-end solutions that support the rapid expansion of hyperscale and enterprise data centers globally. The company provides specialized services, including secure transportation, white-glove delivery, warehousing, and on-site installation support for high-value IT and infrastructure equipment. With the increasing complexity of data center deployments driven by AI and cloud computing, DHL is strengthening its dedicated data center logistics capabilities to enable faster deployment cycles and improved supply chain coordination.

-

Expeditors International of Washington, Inc. plays a significant role in the data center logistics market by providing highly customized freight forwarding and supply chain solutions for critical IT infrastructure. The company focuses on managing complex global logistics flows, including air and ocean freight, customs brokerage, and time-sensitive delivery of servers, networking systems, and electrical equipment. As data center investments worldwide increase, Expeditors is supporting hyperscale and colocation operators by precisely coordinating cross-border shipments and meeting just-in-time delivery requirements.

Key Data Center Logistics Companies:

The following key companies have been profiled for this study on the data center logistics market.

- Deutsche Post AG

- Winning Solutions, Inc.

- Schneider Electric

- Expeditors International of Washington, Inc.

- GXO Logistics, Inc.

- MG Moving Services

- Logistics Plus Inc.

- DP World

- DB SCHENKER

- Kuehne+Nagel

Recent Developments

-

In March 2026, GXO Logistics, Inc. launched a 47,000-square-meter distribution center in the Netherlands to support Benelux data center supply chains by enabling efficient storage and rapid distribution of critical spare parts. This hub addresses the growing need for quick-response logistics amid the region's booming data center sector, supporting hyperscale operators with just-in-time delivery to minimize downtime.

-

In March 2026, DHL Group is expanding its logistics network in North America to support the rapid growth of data center infrastructure driven by AI and cloud computing demand. The company is adding over 7 million square feet of warehouse space and opening 10 new facilities to handle high-value IT equipment, including servers, networking hardware, and cooling systems. These facilities will also offer value-added services such as white-glove handling, rack preconfiguration, and coordinated delivery to reduce deployment time and complexity. Overall, the expansion reflects the increasing role of logistics providers in enabling fast, secure, and efficient data center construction and operations.

Data Center Logistics Market Report Scope

Report Attribute

Details

Market size in 2025

USD 17.4 billion

Estimated market size in 2026

USD 18.6 billion

Projected market size by 2033

USD 34.1 billion

Growth rate

CAGR of 9.1% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company market share, competitive landscape, growth factors, and trends

Segments covered

Device type, data center size, service, end use, and region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; UK; Germany; France; China; India; Japan; South Korea; Australia; Brazil; Kingdom of Saudi Arabia (KSA); UAE; South Africa

Key companies profiled

Deutsche Post AG; Winning Solutions, Inc.; Schneider Electric; Expeditors International of Washington, Inc.; GXO Logistics, Inc.; MG Moving Services; Logistics Plus Inc.; DP World; DB SCHENKER; Kuehne+Nagel

Customization scope

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Data Center Logistics Market Report Segmentation

This report forecasts revenue growth at the global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global data center logistics market report based on device type, data center size, service, end use, and region:

-

Device Type Outlook (Revenue, USD Million, 2021 - 2033)

-

Electrical Devices

-

UPS Systems

-

Servers

-

Storage Devices

-

Others

-

-

Mechanical Devices

-

Cooling Systems

-

Racks

-

Others

-

-

-

Data Center Size Outlook (Revenue, USD Million, 2021 - 2033)

-

Small and Medium-scale Data Center

-

Large-scale Data Center

-

-

Service Outlook (Revenue, USD Million, 2021 - 2033)

-

Transport

-

Installation

-

Warehousing & Inventory

-

Value-added Services

-

-

End Use Outlook (Revenue, USD Million, 2021 - 2033)

-

Banking, Financial Services, and Insurance (BFSI)

-

IT and Telecommunications

-

Government and Defense

-

Healthcare

-

Others

-

-

Regional Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

UK

-

Germany

-

France

-

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

Australia

-

-

Latin America

-

Brazil

-

-

Middle East & Africa (MEA)

-

KSA

-

UAE

-

South Africa

-

-

Frequently Asked Questions About This Report

The global data center logistics market size was valued at USD 17.4 billion in 2025 and is estimated at USD 18.6 billion for 2026.

The global data center logistics market is expected to grow at a CAGR of 9.1% from 2026 to 2033, reaching USD 34.1 billion by 2033.

Key players include Deutsche Post AG; Winning Solutions, Inc.; Schneider Electric; Expeditors International of Washington, Inc.; GXO Logistics, Inc.; MG Moving Services; Logistics Plus Inc.; DP World; DB SCHENKER; Kuehne+Nagel.

The growth of the market can be attributed to the rapid expansion of AI- and cloud-driven data center infrastructure, which is increasing demand for specialized logistics solutions for high-value and sensitive equipment.

The electrical devices segment accounted for the largest share of 68.2% in 2025.The growth of the electrical devices segment can be attributed to the increasing deployment of high-performance computing infrastructure across hyperscale and AI-driven data centers. Equipment such as servers, power distribution units (PDUs), uninterruptible power supply (UPS) systems, and networking hardware require highly controlled logistics environments due to their sensitivity to shock, temperature variations, and electrostatic discharge.

North America dominated with a 38.7% revenue share in 2025.

The large-scale data center segment held the largest revenue share in 2025, while small and medium-scale data center is the fastest-growing segment.

The transportation segment led with a 36.5% revenue share in 2025, and is the fastest-growing service.

IT and telecommunications segment held the largest share in 2025.

About the Author(s)

Automotive & Transportation Research Team

Technology · Automotive & TransportationThis report was authored by the automotive & transportation research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the automotive & transportation segment of the technology industry. All findings are based on proprietary technology databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.