- Home

- »

- Plastics, Polymers & Resins

- »

-

Cell Therapy Packaging Market Size & Share Report, 2033GVR Report cover

![Cell Therapy Packaging Market Size, Share & Trends Report]()

Cell Therapy Packaging Market (2026 - 2033) Size, Share & Trends Analysis Report By Packaging Type (Primary Packaging, Secondary Packaging, Tertiary Packaging), By Material (Cryogenic Plastics, Glass), By Cell Therapy Type (Stem Cell Therapy, NK Cell Therapy), By Region, And Segment Forecasts

- Report Summary

- Table of Contents

- Segmentation

- Methodology

- Download FREE Sample

-

Download Sample Report

Download Sample Report

- Buy Now

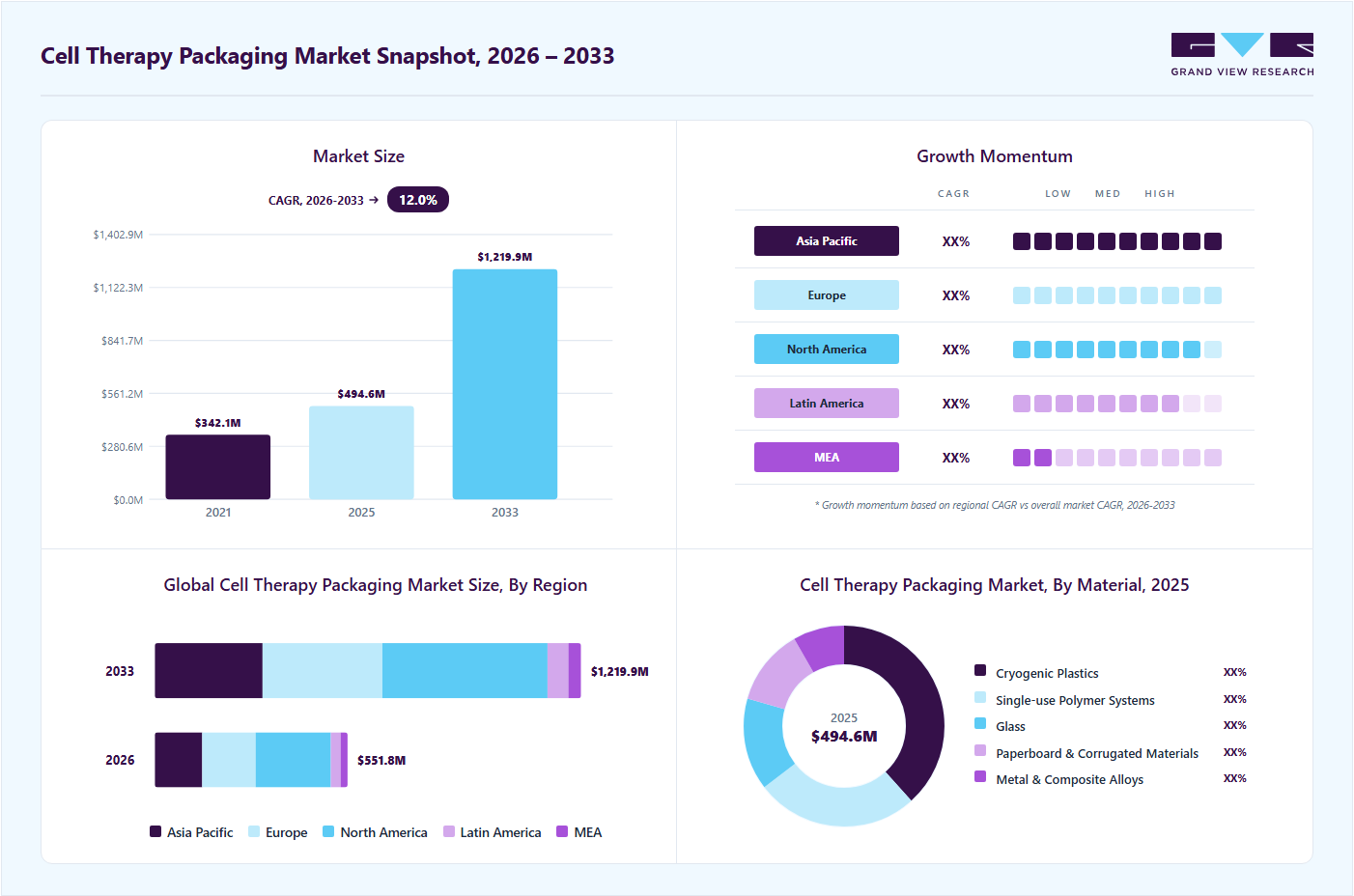

Market Size, 2025

$494.7MMarket Estimate, 2026

$551.8MMarket Forecast, 2033

$1,219.9MCAGR, 2026–2033

12.0%Cell Therapy Packaging Market Summary

The global cell therapy packaging market was valued at USD 494.7 million in 2025 and is projected to grow from USD 551.8 million in 2026 to USD 1,219.9 million in 2033, at a CAGR of 12.0% from 2026 to 2033. North America held the largest global revenue share of 39.0% in 2025. Cell therapy packaging is used to safely store, protect, and transport living cells to hospitals, laboratories, and patients.

Key Market Trends & Insights

- By packaging type: Primary packaging segment dominated the cell therapy packaging market, accounting for a revenue share of 42.3% in 2025.

- By cell therapy type: CAR-T cell therapy segment accounted for the largest share of 35.63% in 2025.

- By material: Cryogenic plastics segment dominated the cell therapy packaging industry in 2025 contributing 38.2% of overall revenue.

Regional Highlights

- Largest regional market: North America (39.0% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

- The U.S. cell therapy packaging industry held the largest share of North America in 2025.

Market Size & Forecast

- Market size in 2025: USD 494.7 Million

- Estimated market size in 2026: USD 551.8 Million

- Projected market size by 2033: USD 1,219.9 Million

- CAGR (2026-2033): 12.0%

The packaging helps maintain a suitable temperature to preserve stem cells, CAR-T cells, and for various cell therapies. Rising demand for cell and gene therapies, increasing commercialization of CAR-T and stem cell therapies, rising investments in regenerative medicine, and growing adoption of high-barrier packaging materials are among the key factors driving market growth.

")

Cell therapies comprise living cells that are highly sensitive to environmental conditions. Specialized packaging solutions are necessary to maintain cell viability, sterility, and product integrity throughout the storage and transportation phases. The growing number of clinical trials and regulatory approvals for advanced cell therapies is accelerating demand for recognized packaging systems that are capable of supporting complex supply chains from manufacturing facilities to treatment centers.

Demand for cell therapy packaging is fueled by the increasing adoption of cryopreserved cell therapies, which require very low temperature storage, maintaining chain-of-identity, and cold-chain logistics. Advanced packaging formats, such as cryogenic containers, insulated shippers, sterile bags, and temperature-monitoring systems, are becoming increasingly important as manufacturers expand their global distribution networks. For instance, in November 2025, Cencora announced its plan to invest USD 1 billion to expand its cold-chain infrastructure and specialty pharmaceutical distribution capabilities to support the growing transportation and storage requirements of advanced cell therapies.

Furthermore, strict regulatory requirements for cell tracking, product safety, and quality assurance are encouraging healthcare providers, biopharmaceutical companies, and logistics providers to invest in innovative cell therapy packaging solutions. These trends, along with advancements in IoT-enabled monitoring and cold-chain technologies, are supporting the market growth.

Market Dynamics

The growing adoption of cell therapies is a major factor driving the cell therapy packaging market. As more CAR-T, stem cell, and gene-modified therapies receive regulatory approvals and move from clinical trials to commercial production, there is an increase in the need for specialized packaging solutions. Commercial-scale distribution requires validated cryogenic containers, sterile packaging systems, and chain-of-custody monitoring to ensure product integrity throughout the supply chain. The expansion of manufacturing facilities and rising investments in advanced therapy medicinal products (ATMPs) across North America, Europe, and Asia Pacific are further supporting demand for cell therapy packaging solutions.

Challenges in maintaining a constant desired temperature and appropriate storage conditions are negatively impacting market growth. Cell therapy utilizes an array of cells that are sensitive to deformation and melting, resulting in loss of efficacy when exposed to adverse environmental conditions. The therapy formulations require calibrated storage and transportation facilities to maintain their stability and therapeutic potency. Maintaining desired storage and transportation conditions involves high-cost logistics and cold-chain management borne by pharmaceutical manufacturers and distributors. Dynamic environmental changes and inadequate healthcare infrastructure are also termed as key restraining factors.

Market Concentration & Characteristics

The cell therapy packaging market is influenced by a moderately concentrated environment, with the presence of well-established companies engaged in pharmaceutical packaging, cold-chain logistics, and bioprocessing. Major players such as Thermo Fisher Scientific, Cryoport Systems, Catalent, CSafe, Sartorius, and BioLife Solutions dominate the market through extensive cold-chain infrastructure, cryogenic technologies, and global distribution capabilities. The market also includes a growing number of emerging providers focused on cryogenic containers, cell therapy bags, and temperature-controlled shipping systems.

The cell therapy packaging industry demonstrates a high degree of innovation, driven by the need to preserve the viability of living cells during storage and transportation. Companies are investing in advanced cryogenic packaging, reusable liquid nitrogen dry vapor shippers, IoT-enabled temperature monitoring, GPS tracking, RFID-based traceability, and digital chain-of-custody platforms. Innovation is focused on supporting autologous cell therapies, where patient-specific products require precise identification and handling throughout the supply chain. The industry has also witnessed an increase in strategic partnerships and acquisitions as companies seek to strengthen end-to-end cell therapy logistics capabilities. For example, in November 2023, Cryoport acquired Tec4med LifeScience GmbH to strengthen its temperature-controlled packaging, monitoring, and supply chain capabilities across Europe, supporting the growing demand for advanced logistics solutions for cell therapy packaging.

Regulatory requirements significantly influence market dynamics, as cell therapy packaging must comply with Good Manufacturing Practice (GMP), Food and Drug Administration (FDA), European Medicines Agency (EMA), and Advanced Therapy Medicinal Products (ATMPs) guidelines on sterility, traceability, labeling, and low-temperature storage. These regulatory barriers increase the importance of validated packaging systems for cell therapy, supporting the market growth.

Packaging Type Insights

The primary packaging segment dominated the cell therapy packaging market, accounting for a revenue share of 42.3% in 2025. This is due to its direct contact with therapeutic cells and its critical role in maintaining product viability, sterility, and stability throughout collection, processing, storage, and administration. Primary packaging includes cryobags, vials, syringes, sterile containers, specimen collection containers, and single-use closed-system storage vessels. These components are essential at every stage of the cell therapy process. The growing use of autologous and allogeneic cell therapies, improved cell preservation techniques, and stringent regulatory requirements for contamination control and product integrity are driving the demand for advanced primary packaging solutions. Manufacturers are increasingly using high-performance, biocompatible materials and closed-system packaging formats. These help ensure accurate dosing, traceability, and compliance with changing regulations, which strengthens the position of this segment.

The tertiary packaging segment is expected to grow at the fastest CAGR over the forecast period, driven by the rapid expansion of global cell therapy supply chains and the increasing cross-border transportation of temperature-sensitive therapies. This segment includes cryogenic shipping containers, dry-vapor liquid nitrogen shippers, vacuum-insulated transport containers, palletized shipping systems, reusable thermal transport boxes, protective outer transport cases, and other shipping solutions. The growth of the cell and gene therapies market is driving the demand for specialized bulk transport solutions for clinical trials and commercial-scale distribution. In addition, tertiary packaging is benefiting from increasing investments in cold-chain logistics infrastructure, particularly for international shipments of personalized therapies that require strict chain-of-identity, chain-of-custody, and ultra-low-temperature control. The globalization of cell therapy manufacturing networks is also expected to surge the demand for advanced tertiary packaging solutions, resulting in a higher growth rate of this segment over the coming years.

Material Insights

The cryogenic plastics segment dominated the cell therapy packaging industry in 2025 contributing 38.2% of overall revenue, owing to the widespread use of this material in primary packaging applications that directly store and preserve living cells at ultra-low temperatures. This category consists of ethylene-vinyl acetate (EVA), fluorinated ethylene-propylene (FEP), polypropylene (PP), cyclo-olefin polymer (COP), and cyclo-olefin copolymer (COC). Cryogenic plastics are widely used in cryobags, cryovials, storage containers, and closed-system packaging. These materials offer high flexibility, chemical resistance, low gas permeability, superior break resistance, and compatibility with cryogenic temperatures, making them ideal for maintaining cell viability during storage and transportation. The increasing commercialization of CAR-T, stem cell, and allogeneic therapies, and the rising adoption of cryopreservation technologies, further strengthen the demand for cryogenic plastics in the market.

The single-use polymer systems segment is expected to grow at the fastest CAGR during the forecast period, driven by the growing preference for closed, disposable, contamination-free packaging in cell therapy production. This segment primarily comprises single-use polymer films, disposable bioprocessing bags, sterile transfer bags, single-use cryogenic containers, tubing assemblies, and flexible storage systems. These materials are used for cell collection, processing, storage, and transport. As cell therapy manufacturing moves from clinical trials to commercial production, more companies are opting for single-use packaging systems. These systems save the time involved in cleaning, lower the risk of cross-contamination, make operations more flexible, and help meet regulatory standards. The growing focus on personalized and autologous therapies, which require packaging and handling for each patient, is further accelerating the growth of the single-use polymer systems segment.

Cell Therapy Type Insights

The CAR-T cell therapy segment accounted for the largest share of the cell therapy packaging market capturing 35.63% of the total market share due to the rapid commercialization of CAR-T therapies, increasing regulatory approvals, expanding treatment indications, and the highly complex logistics for autologous cell therapies. CAR-T products require specialized cryogenic packaging, temperature-controlled shipping containers, sterile single-use bags, vials, and identity tracking systems to maintain cell viability throughout collection, manufacturing, storage, and patient delivery. Furthermore, most commercial CAR-T therapies rely on cryopreservation and long-distance transportation, which require advanced packaging and cold-chain solutions, contributing to the segment growth. In March 2026, AstraZeneca announced its plan to establish a dedicated cell therapy manufacturing and supply base in Shanghai focused on CAR-T therapies. This trend highlights growing investment in large-scale CAR-T production and distribution infrastructure, leading to rising demand for specialized packaging systems.

The stem cell therapy segment is expected to grow at the fastest CAGR over the forecast period, due to the rapid expansion of regenerative medicine applications, rising stem cell clinical trials, growing investments in stem cell manufacturing facilities, and rising demand for cell banking and cryopreservation services. Stem cell therapies require highly specialized packaging solutions, including cryogenic vials, biobags, and temperature-controlled shippers to preserve cell integrity during storage and transportation. The need for reliable packaging and logistics infrastructure is accelerating due to increasing stem cell manufacturing on a commercial level.

In addition, the growing adoption of allogeneic stem cell therapies and stem cell-based treatments for orthopedic, neurological, cardiovascular, and autoimmune disorders is supporting the growth of the stem cell therapy segment. The growing investments in stem cell production and infrastructure further support the growth of stem cell therapy packaging solutions. For instance, in January 2026, Hope Biosciences received a USD 1 million expansion incentive to expand its stem cell manufacturing capacity and clinical development activities.

Regional Insights

The North America cell therapy packaging market accounted for the largest revenue share of 39.0% in 2025, supported by the rapid expansion of cell and gene therapy (CGT) manufacturing, increasing commercialization of CAR-T and stem cell therapies, and growing demand for advanced cold-chain logistics. The region continues to benefit from a strong pipeline of clinical trials, rising investments in regenerative medicine, and the need for specialized cryogenic packaging, temperature-controlled shippers, and real-time monitoring systems that maintain cell viability during transport. In addition, the growing number of approved cell and gene therapies and the expansion of CGT manufacturing facilities across North America have strengthened demand for packaging systems capable of supporting complex supply chains.

U.S. Cell Therapy Packaging Market Trends

The U.S.cell therapy packaging industry held the largest share of North America in 2025, driven by a favorable regulatory environment, rising FDA approvals, and continued investment in advanced therapy manufacturing infrastructure. The FDA approvals of cellular and gene therapy products are the primary growth driver, driving the need for compliant cryogenic storage and transportation solutions throughout the therapy lifecycle. These factors, combined with continued growth in U.S. cell therapy development and manufacturing capacity, are expected to support significant growth of the market.

Europe Cell Therapy Packaging Market Trends

The Europe cell therapy packaging industry accounted for a significant share in 2025, supported by expanding cell and gene therapy (CGT) manufacturing capacity, increasing clinical trial activity, and strong regulatory support for advanced therapies. The region has witnessed growing investments in bioprocessing infrastructure, cryogenic storage systems, and specialized cold-chain logistics to support the transport of temperature-sensitive cellular products. The European Medicines Agency (EMA) continues to encourage the development of ATMPs, while the commercialization of CAR-T and stem cell therapies increases demand for validated cryogenic containers, sterile packaging solutions, and real-time temperature-monitoring technologies.

The Germany cell therapy packaging market is expected to grow significantly due to its strong biopharmaceutical manufacturing base, growing regenerative medicine sector, and increasing investments in cell and gene therapy production facilities. The market benefits from expanding collaborations between biotechnology companies, research institutes, and manufacturing organizations focused on advanced cell therapy production. Investments in cell therapy manufacturing and bioprocessing facilities across Germany further support the market growth for advanced cell therapy packaging in the country.

Asia Pacific Cell Therapy Packaging Market Trends

The Asia Pacific cell therapy packaging market is expected to record the fastest CAGR over the forecast period, driven by the rapid growth in cell and gene therapy (CGT) research, increasing investments in biomanufacturing infrastructure, and the rising adoption of regenerative medicine across countries such as China, Japan, South Korea, and Australia. Governments across the region continue to implement policies to strengthen biotechnology innovation and advanced therapy development, leading to a growing demand for cryogenic packaging, sterile single-use systems, temperature-controlled shippers, and real-time monitoring solutions.

The China cell therapy packaging market accounted for a significant share of Asia Pacific in 2025, supported by strong government backing for biotechnology innovations, rapid growth in cell therapy clinical trials, and substantial investments in advanced biomanufacturing facilities. The country is known as one of the world's largest hubs for cell and gene therapy development, particularly in CAR-T and stem cell therapies, creating significant demand for cell therapy packaging products.

Middle East & Africa Cell Therapy Packaging Market Trends

The Middle East & Africa cell therapy packaging market is anticipated to grow over the forecast period, supported by increasing investments in biotechnology, regenerative medicine, and advanced healthcare infrastructure. Governments across the region are focusing on initiatives to strengthen life sciences research, precision medicine, and biopharmaceutical manufacturing, creating new opportunities for cell and gene therapy (CGT) development. In addition, the rise of medical research hubs and innovation-focused healthcare projects across the Gulf region is expected to increase the demand for compliant packaging and logistics systems for cell therapies.

The UAE cell therapy packaging market emerged as a key contributor to the Middle East & Africa, driven by significant investments in biotechnology, advanced healthcare facilities, and regenerative medicine programs. The country has prioritized healthcare innovation through national strategies to strengthen pharmaceutical manufacturing, biomedical research, and precision medicine capabilities. Institutions such as the Dubai Science Park and Abu Dhabi Department of Health have supported the expansion of biotechnology and advanced therapy ecosystems, encouraging long-term growth of the market.

Key Cell Therapy Packaging Company Insights

The competitive environment of the market is moderately fragmented, with the presence of packaging companies, pharmaceutical packaging manufacturers, and specialized healthcare packaging providers. Key players compete by offering innovative products, strong barrier protection, safe packaging, regulatory compliance, and cost-effective manufacturing. Companies are investing more in sustainable materials, advanced packaging solutions, and automation. Strategic partnerships and regional growth are also shaping the competitive landscape.

-

In October 2025, Cryoport Systems launched a 55,000 square-feet Global Supply Chain Center near Paris, France, to provide end-to-end temperature-controlled logistics, biostorage, and packaging support for cell and gene therapies. The facility expanded Cryoport’s European cold-chain infrastructure and strengthened the capacity to handle growing demand for advanced cell therapy packaging and supply chain solutions across global markets.

-

In August 2025, Sartorius Stedim Biotech partnered with Nanotein Technologies and invested up to USD 3 million to advance the manufacturing of immune cells for cell therapies, including CAR -T and NK-based treatments. The collaboration expanded access to next-generation cell activation technologies and supported the development of innovative solutions for the rapidly growing cell and gene therapy packaging market.

Key Cell Therapy Packaging Companies:

This report has been delivered with the following In-depth customizations cell therapy packaging market.

-

CSAFE

-

Cryoport Systems, LLC.

-

Sartorius AG

-

BioLife Solutions Inc.

-

Thermo Fisher Scientific Inc.

-

ThermoSafe

-

Catalent, Inc.

-

Cold Chain Technologies

-

va-Q-tec Thermal Solutions GmbH

-

Azenta US Inc.

Competitive Benchmarking

Operating Strategies

Competitive Edge

Weakness

Mature Players: CSAFE; Cryoport Systems, LLC.; Sartorius AG; Thermo Fisher Scientific Inc.; ThermoSafe; Catalent, Inc.; Cold Chain Technologies.

- Mature players focus on end-to-end cell therapy supply chain solutions, combining packaging, cryogenic storage, logistics, monitoring, and regulatory support.

- These companies expand through acquisitions, strategic partnerships, and global infrastructure investments to strengthen international reach.

- Mature players possess strong global manufacturing infrastructure, extensive distribution networks, and well-established relationships with major manufacturers.

- Broad product portfolios and large-scale manufacturing capabilities enable one-stop solutions for biopharma and cell therapy companies.

- Large organizational structures and complex operational networks can reduce flexibility and lead to slow adaptation to niche or rapidly evolving packaging technologies.

- Mature companies face high operational and compliance costs associated with sustainability initiatives, raw material price fluctuations, and stringent regulations.

Emerging Players: BioLife Solutions Inc.; va-Q-tec Thermal Solutions GmbH; Azenta US Inc.

- Emerging players primarily focus on specialized technologies, including advanced cryopreservation, vacuum-insulated packaging, smart monitoring, and cell & gene therapy logistics.

- These companies invest heavily in innovation, strategic collaborations, and technology-driven service differentiation.

- Emerging players benefit from faster innovation cycles, greater operational flexibility, and the ability to address highly customized packaging requirements.

- Their niche technical expertise promotes greater agility in developing customized solutions for emerging cell therapy applications.

- Emerging players often operate with limited production capacity, smaller global footprints, and comparatively lower financial resources than multinational competitors.

- Limited economies of scale, lower financial resources, and narrower product portfolios can restrict large-scale expansion and market penetration.

Cell Therapy Packaging Market Report Scope

Report Attribute

Details

Market size in 2025

USD 494.7 million

Estimated market size in 2026

USD 551.8 million

Projected market size by 2033

USD 1,219.9 million

Growth rate

CAGR of 12.0% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Packaging type, material, cell therapy type, region

Regional Scope

North America; Europe; Asia Pacific; Latin America; Middle East & Africa

Key companies profiled

CSAFE; Cryoport Systems, LLC.; Sartorius AG; BioLife Solutions Inc.; Thermo Fisher Scientific Inc.; ThermoSafe; Catalent, Inc.; Cold Chain Technologies; va-Q-tec Thermal Solutions GmbH; Azenta US Inc.

Customization scope

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail of customized purchase options to meet your exact research needs. Explore purchase options

Global Cell Therapy Packaging Market Report SegmentationThis report forecasts revenue growth at the global, regional & country levels and provides an analysis on the latest industry trends and opportunities in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global cell therapy packaging market report based on packaging type, material, cell therapy type, and region:

-

Packaging Type Outlook (Revenue, USD Million, 2021 - 2033)

-

Primary Packaging

-

Secondary Packaging

-

Tertiary Packaging

-

-

Material Outlook (Revenue, USD Million, 2021 - 2033)

-

Cryogenic Plastics

-

Single-use Polymer Systems

-

Glass

-

Paperboard & Corrugated Materials

-

Metal & Composite Alloys

-

-

Cell Therapy Type Outlook (Revenue, USD Million, 2021 - 2033)

-

CAR-T Cell Therapy

-

Stem Cell Therapy

-

NK Cell Therapy

-

Dendritic Cell Therapy

-

Other Cell Therapies

-

-

Regional Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

France

-

UK

-

Italy

-

Spain

-

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

Australia

-

-

Latin America

-

Brazil

-

Argentina

-

-

Middle East & Africa

-

Saudi Arabia

-

UAE

-

South Africa

-

-

Frequently Asked Questions About This Report

The global cell therapy packaging market was estimated at around USD 494.7 million in the year 2025 and is expected to reach around USD 551,8 million in 2026.

The global cell therapy packaging market is expected to grow at a compound annual growth rate of 12.0% from 2026 to 2033 to reach around USD 1,219.9 million by 2033.

The stem CAR-T Cell Therapy segment led the cell therapy packaging market in 2025 due to the rapidly increasing adoption of personalized cancer immunotherapies and the expanding commercialization of CAR-T treatments worldwide.

The key players in the cell therapy packaging market include CSAFE, Cryoport Systems, LLC., Sartorius AG, BioLife Solutions Inc., Thermo Fisher Scientific Inc., ThermoSafe, Catalent, Inc, Cold Chain Technologies, va-Q-tec Thermal Solutions GmbH, Azenta US Inc.

The global cell therapy packaging market is growing rapidly due to the increasing commercialization of advanced cell-based therapies, rising investments in regenerative medicine, and expanding clinical research activities worldwide.

About the Author(s)

Plastics, Polymers & Resins Research Team

Bulk Chemicals · Plastics, Polymers & ResinsThis report was authored by the plastics, polymers & resins research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the plastics, polymers & resins segment of the bulk chemicals industry. All findings are based on proprietary bulk chemicals databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Share this report with your colleague or friend.

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.