- Home

- »

- Semiconductors

- »

-

RF Front End Module Market Size, Share Report, 2026-2033GVR Report cover

![RF Front End Module Market (2026 - 2033)Report]()

RF Front End Module Market (2026 - 2033)

Size, Share & Trends Analysis Report By Type (Power Amplifier, Low-Noise Amplifier, Filters, Switches), By Technology (Wi-Fi, Bluetooth), By End-use (IT & Telecom, Smart Phones & Consumer Electronics), By Region, And Segment Forecast

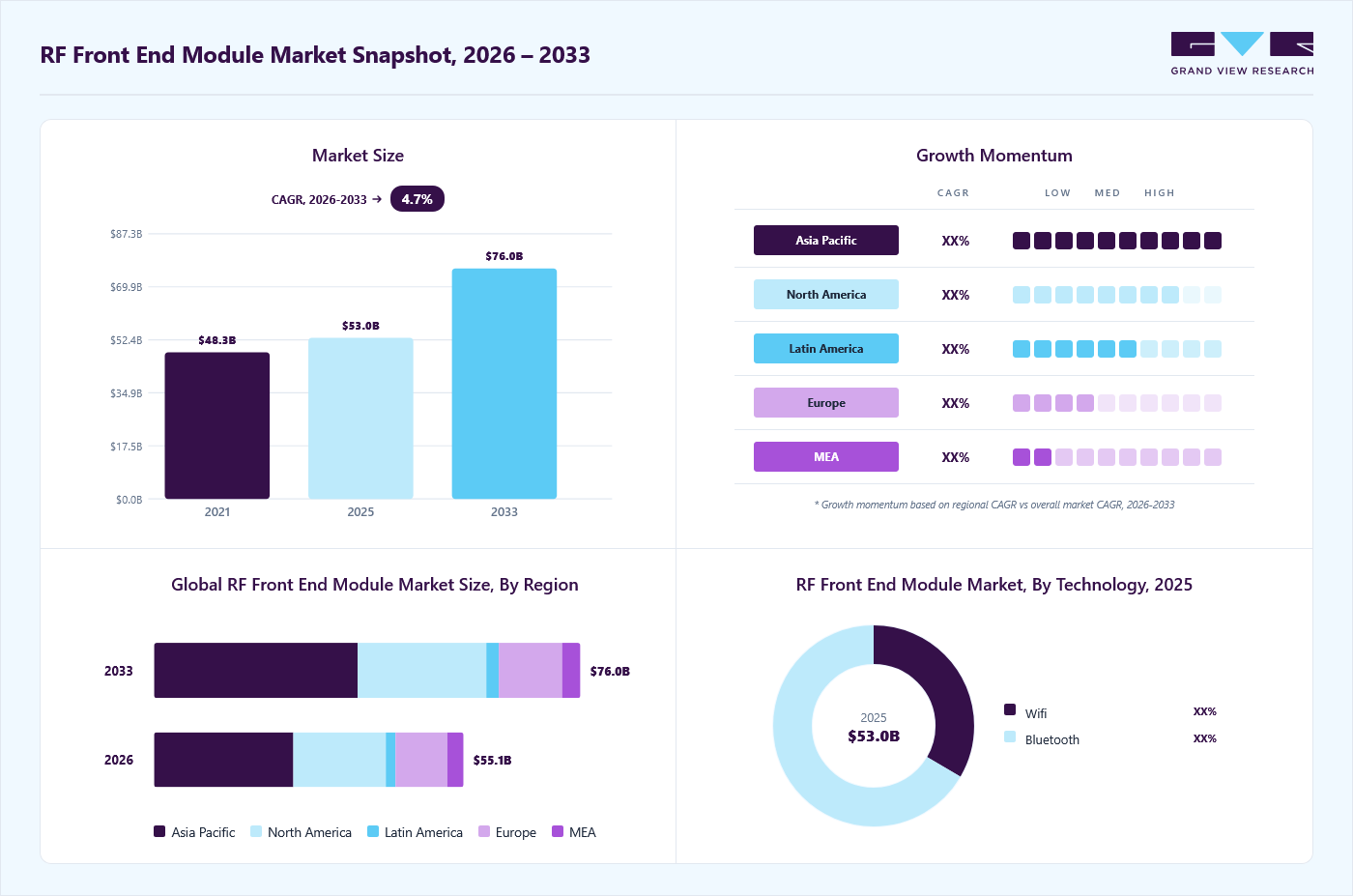

Market Size, 2025

$53.0BMarket Estimate, 2026

$55.1BMarket Forecast, 2033

$76.0BCAGR, 2026–2033

4.7%RF Front End Module Market Summary

The global RF front end module market size was valued at USD 53.0 billion in 2025 and is projected to grow from USD 55.1 billion in 2026 to USD 76.0 billion by 2033, at a CAGR of 4.7% from 2026 to 2033. The market in Asia Pacific dominated with a revenue share of 44.3% in 2025.

Growing due to dense, high-bandwidth urban networks and the accelerating shift toward 6G is driving the radio frequency (RF) front end module market.

Key Market Trends & Insights

- By type: Filters segment dominated the RF front-end module market with revenue share of 37.5% in 2025.

- By technology: Bluetooth segment held the largest market share of 66.6% in 2025.

- By end-use: Smartphones & consumer electronics segment held the largest revenue share of 65.8% in 2025.

Regional Highlights

- Largest regional market: Asia Pacific (44.3% revenue share, 2025)

- By country: The China held the largest market share in 2025.

Market Size & Forecast

- Market size in 2025: USD 53.0 billion

- Estimated market size in 2026: USD 55.1 billion

- Projected market size by 2033: USD 76.0 billion

- CAGR (2026-2033): 4.7%

The rapid proliferation of wireless audio devices, including true wireless earbuds, Bluetooth headsets, portable speakers, and integrated smart earphones, is significantly driving the RF front-end market. Consumers are among the most tech-savvy in the world, with strong adoption rates for premium consumer electronics, including high-quality audio products. These devices rely heavily on RF front-end modules to maintain uninterrupted connectivity, support high-fidelity audio streaming, and optimize energy efficiency. Wireless audio devices require power amplifiers, low-noise amplifiers, switches, and filtering types that deliver high linearity and low insertion loss while operating within extremely compact form factors. RF front-end suppliers are increasingly focused on integrating these components into compact modules, balancing high-performance transmission and reception with battery efficiency, a critical requirement given the limited energy capacity of small earbuds and portable devices. The surge in audio streaming services, podcast consumption, and remote working trends has further accelerated the adoption of wireless audio, creating a continuous, high-volume demand for advanced RF front-end components.")

The global expansion of defense and aerospace communication systems is indirectly supporting growth in the RF front-end market, as many of the technologies used are closely linked to commercial RF development. Systems such as radar, satellite communication terminals, secure radios, and electronic warfare platforms rely heavily on high-frequency RF integrated circuits, phased-array antennas, and wideband filters. These components are built using the same semiconductor design, manufacturing, and advanced packaging technologies that are widely used in commercial telecom and wireless infrastructure. Although defense supply chains are highly regulated, RF component suppliers often serve commercial and dual-use customers, creating a stable but less visible source of demand that supports long-term growth of the global RF front-end market.

The rapid expansion of industrial wireless automation is a key factor driving global demand for RF front-end components. As manufacturers in Asia-Pacific, Europe, and North America continue to digitize their operations, wireless connectivity is becoming essential across factories, warehouses, and production sites. Technologies such as wireless sensors, automated guided vehicles, robotics, equipment monitoring, and machine-to-machine communication rely on reliable, low-latency RF connections that can operate effectively in demanding industrial environments. Challenges such as high electromagnetic interference, metal-heavy infrastructure, and extreme temperature conditions are increasing the need for high-performance RF front-end components, including low-noise amplifiers, filtering modules, power amplifiers, and durable antenna systems. As RF suppliers become more deeply integrated into global industrial automation value chains, adoption of industrial-grade RF solutions aligned with Industry 4.0 initiatives continues to grow steadily.

The growing adoption of ultra-wideband (UWB) location technology is a significant driver of growth for the global RF front end market. UWB use is expanding across consumer electronics, logistics, smart manufacturing, automotive applications, and asset-tracking systems, supported by growing demand for digital car keys, indoor positioning, proximity detection, warehouse automation, and real-time location tracking. These applications require specialized RF front-end components that can deliver very low latency, high accuracy, and reliable performance across wide frequency ranges. Semiconductor foundries and advanced packaging providers worldwide play a critical role in supporting UWB chipset production by ensuring stable performance and precise timing. As leading smartphone, IoT, and automotive manufacturers increasingly adopt UWB as a standard feature, demand for UWB-specific RF front-end modules, such as precision filters, power amplifiers, and integrated antenna solutions, continues to grow, supporting the long-term expansion of the global RF front-end market.

Type Insights

The filters segment dominated the RF front-end module market with revenue share of 37.5% in 2025, driven by the rapid expansion of IoT devices, connected vehicles, and automotive infotainment systems worldwide. Connected and autonomous vehicles require high-performance RF filters that can operate reliably in complex electromagnetic environments while supporting applications such as V2X communication, GPS navigation, radar sensing, advanced driver-assistance systems (ADAS), telematics, and in-vehicle infotainment. At the same time, the growing adoption of smart factories and industrial IoT is increasing demand for filters capable of supporting multi-band operation without signal degradation in environments characterized by high RF noise and dense device deployments. In addition, the expansion of smart infrastructure and Industry 4.0 initiatives, including automated warehouses, connected logistics hubs, and digitally enabled manufacturing facilities, is creating additional demand for advanced filtering solutions that ensure signal clarity and stability across high-speed wireless networks. These factors are positioning RF filters as a critical growth segment within the global RF front-end market over the forecast period.

The power amplifier (PA) segment is projected to grow at a significant CAGR from 2026 to 2033, driven by the growing demand from next-generation wireless standards and the expanding 5G deployments worldwide. The rapid adoption of Wi-Fi 6E and Wi-Fi 7 in consumer electronics is increasing the need for high-performance PAs that can operate efficiently at higher frequencies, particularly in the 6 GHz band, while supporting wide bandwidths and advanced modulation schemes such as 4096-QAM. At the same time, continued rollout of 5G New Radio across sub-6 GHz and millimeter-wave bands is increasing performance requirements for PAs used in smartphones, CPEs, fixed wireless access devices, and small cells, which must handle high peak-to-average power ratios, wide instantaneous bandwidths, and complex carrier aggregation. These factors collectively support the PA segment’s position within the global RF front-end market and support its sustained growth.

Technology Insights

The Bluetooth segment dominated the market share of 66.6% in 2025, supported by the widespread adoption of Bluetooth technology across consumer electronics, IoT devices, and smart accessories worldwide. Bluetooth has become a standard connectivity solution for smartphones, wireless earbuds, wearables, smart home devices, medical devices, and industrial sensors due to its low power consumption, cost efficiency, and reliable short-range performance. The growing demand for true wireless stereo (TWS) earbuds, smartwatches, fitness trackers, and connected healthcare devices has significantly increased the need for compact and highly integrated RF front-end modules optimized for Bluetooth operation. Increasing adoption of Bluetooth in smart factories, asset tracking, retail beacons, and automotive infotainment systems is also strengthening demand for efficient RF front-end solutions, supporting the Bluetooth segment’s position in the global RF front-end module market.

The Wi-Fi segment is projected to grow at the fastest CAGR from 2026 to 2033, driven by the rapid expansion of high-speed wireless connectivity across consumer, enterprise, and industrial applications worldwide. The increasing demand for bandwidth-intensive applications such as video streaming, cloud gaming, remote work, and AR/VR is accelerating the adoption of advanced Wi-Fi standards, including Wi-Fi 6, Wi-Fi 6E, and Wi-Fi 7, which require more complex and higher-performance RF front-end modules. The increasing deployment of Wi-Fi in smartphones, laptops, tablets, smart TVs, home routers, enterprise access points, and public hotspots is further strengthening segment growth. In addition, the expansion of smart homes, connected buildings, and Industry 4.0 environments is driving demand for reliable, low-latency Wi-Fi connectivity, increasing the need for advanced power amplifiers, filters, switches, and integrated antenna solutions.

End-use Insights

The smartphones & consumer electronics segment dominated the market with a share of 65.8% in 2025, supported by the central role of Wi-Fi connectivity in everyday digital devices. Wi-Fi remains a core technology across smartphones, tablets, laptops, smart TVs, gaming consoles, and home networking equipment, driving sustained demand for compact and highly integrated RF front-end modules. Increasing device complexity, driven by multi-band and multi-antenna designs, is increasing the need for advanced RF components that can deliver stable performance, low power consumption, and seamless connectivity across crowded wireless environments. Additionally, the increasing use of connected consumer devices for online entertainment, digital payments, smart home control, and cloud-based services is driving up Wi-Fi usage density, placing greater performance demands on RF front-end solutions.

The IT & telecom segment is expected to grow at the fastest rate from 2026 to 2033, supported by ongoing global investments in modern communication infrastructure and growing data traffic across wireless and wired networks. The continued rollout of 5G networks, growth of fixed wireless access, and increasing use of small cells and distributed antenna systems are driving strong demand for high-performance RF front-end modules. At the same time, telecom operators and cloud service providers are upgrading their networks to handle the higher usage of cloud services, video streaming, and other low-latency applications, which increases the need for RF solutions with improved signal quality, wider bandwidth, and enhanced energy efficiency. These factors position the IT & telecom segment as a key contributor to growth in the global RF front-end module market.

Regional Insights

The Asia Pacific RF front end module industry is the largest segment held 44.3% revenue share, and is expected to grow at the fastest CAGR over the forecast period, supported by the region’s large population base, rapid urbanization, and expanding digital ecosystems. Strong growth in affordable and mid-range smartphones, increasing rollout of private 5G networks for industrial use, and growing demand for RF front-end modules in smart manufacturing, smart cities, and connected transportation projects. The region also benefits from its role as a global electronics manufacturing hub, with continuous investments in semiconductor fabrication, assembly, and testing capabilities strengthening local supply chains and accelerating market expansion.

China RF Front End Module Trends

The RF front end module market in China is projected to grow significantly during the forecast period, driven by strong domestic demand and large-scale deployment of wireless technologies. Growth in China is supported by high volumes of 5G smartphone shipments, expansion of industrial and enterprise connectivity, and increased use of RF modules in electric vehicles, intelligent factories, and public infrastructure. Ongoing efforts to localize semiconductor production and reduce dependence on imports are further supporting the steady growth of the RF front end module market in the country.

North America RF Front End Module Trends

The RF front end module industry in North America is expected to grow significantly during the forecast period, driven by strong demand from 5G infrastructure expansion, consumer electronics, and advanced connectivity applications. Continued investment in 5G network densification, growing adoption of Wi-Fi 6E and early Wi-Fi 7 devices, and rising demand for high-performance RF modules in smartphones, wearables, and connected home devices drive the market. Increased deployment of fixed wireless access, private 5G networks, and edge computing infrastructure in North America is increasing demand for RF front-end solutions with higher linearity, wider bandwidth, and improved energy efficiency. Strong presence of leading telecom operators, device manufacturers, and semiconductor companies further supports market growth.

The U.S. RF front end module industry is projected to grow significantly during the forecast period, supported by large-scale 5G rollouts, rapid adoption of next-generation wireless standards, and sustained demand from consumer electronics and telecom infrastructure. Continued investments in network upgrades, small cell deployments, and cloud-driven connectivity, along with growing use of RF modules in automotive, IoT, and enterprise connectivity solutions, are expected to drive steady market expansion in the country.

Europe RF Front End Module Trends

The RF front end module industry in Europe is expected to grow significantly during the forecast period, supported by increasing investments in digital connectivity, industrial modernization, and automotive electronics. Key trends across the region include rising deployment of private and enterprise 5G networks, growing integration of RF front-end modules in connected vehicles, and increasing demand from industrial automation and smart energy systems. Europe’s strong focus on sustainability, energy efficiency, and high-quality network performance is also driving demand for advanced RF solutions that support reliable communication across dense urban and industrial environments.

The RF front end module market in Germany is growing significantly during the forecast period, driven by the country’s leadership in automotive manufacturing and industrial technology. Ongoing upgrades to telecom infrastructure, including enterprise connectivity and localized 5G networks for manufacturing plants, along with strong collaboration between automotive OEMs and technology providers, are supporting the continued growth of the RF front end module market in the country.

Key RF Front End Module Company Insights

Some of the key companies operating in the market, include Qualcomm Technologies, and Broadcom, among others are some of the leading participants in the RF front end module market.

-

Qualcomm Technologies is a global semiconductor and wireless technology company renowned for its mobile-focused system-on-chips (SoCs) and integrated connectivity solutions. The company’s RF front-end offerings include highly integrated PA, filter, and transceiver modules designed for 4G LTE, 5G NR, Wi-Fi, and Bluetooth applications, enabling optimized performance, reduced power consumption, and compact form factor integration in smartphones, tablets, and IoT devices.

-

Broadcom is a technology company specializing in semiconductor solutions for wired and wireless connectivity, storage, and broadband access. In the RF front-end domain, Broadcom is a prominent supplier of filter technologies, particularly FBAR (Film Bulk Acoustic Resonator) filters used in cellular and Wi-Fi front ends to enable precise frequency selectivity and interference suppression. With operations and customers across North America, Asia-Pacific, and Europe, Broadcom is recognized as a mature, globally integrated provider in the RF front-end ecosystem.

AAC Technologies, and RichWave Technology are some of the emerging market participants in the RF front end module market.

-

AAC Technologies is a China-based provider of advanced acoustic, haptic, and RF components for mobile devices and consumer electronics. The company’s RF front-end offerings include power amplifiers, filters, and antenna modules tailored for smartphones, wearables, and IoT products. Leveraging its strong manufacturing base and integration capabilities, AAC is rapidly expanding its RF module portfolio to serve major OEMs, particularly in Asia. The company has been strengthening its position by aligning with evolving wireless standards, including 5G and Wi-Fi 6/6E, and scaling production to meet demand for compact, high-performance RF solutions.

-

RichWave Technology is a Taiwan-based semiconductor company specializing in RF front-end integrated circuits and modules for mobile communications. The company’s product portfolio includes power amplifiers, multi-mode transceivers, and front-end modules designed to support 4G LTE, 5G NR, and multi-band wireless applications. RichWave’s solutions are targeted at smartphones, IoT devices, and connected products requiring efficient RF performance and compact integration. With growing adoption among regional OEMs and expanding partnerships internationally, RichWave is positioning itself as a competitive emerging supplier in the global RF front-end market.

Key RF Front End Module Companies:

The following are the leading companies in the RF front end module market. These companies collectively hold the largest market share and dictate industry trends.

- AAC Technologies

- Ampleon

- Broadcom

- Murata Manufacturing Co., Ltd.

- Panasonic Industry Co., Ltd.

- Qorvo, Inc.

- Qualcomm Technologies, Inc.

- RFHIC Corporation

- RichWave Technology Corporation

- Samsung Electronics Co., Ltd.

- Spirox Corporation

- Taiyo Yuden Co., Ltd.

- TDK Corporation

- United Microelectronics Corporation

- Walsin Technologies Corporation

Recent Developments

-

In Oct 2025, Qorvo introduced the QPA9510, a new compact RF power amplifier offering wideband coverage from 100 MHz to 1000 MHz with high efficiency and strong output performance, aimed at simplifying sub-1 GHz design challenges in wireless systems such as IoT, public safety, and smart utility applications. The QPA9510 enhances RF front-end flexibility with broad band coverage and strong efficiency for battery-powered devices.

-

In Oct 2025, Skyworks Solutions updated its Wi-Fi 7 portfolio by introducing new front-end modules (FEMs) and BAW filters. The Gen 2 FEMs work across 2.4 GHz, 5 GHz, and 6 GHz bands and are compatible with major SoC platforms. Their full-band filters allow multiple bands to operate at the same time, providing faster speeds, wider coverage, and better signal performance for next-generation Wi-Fi devices.

RF Front End Module Market Report Scope

Report Attribute

Details

Market size in 2025

USD 53.0 billion

Market size value in 2026

USD 55.1 billion

Revenue forecast in 2033

USD 76.0 billion

Growth rate

CAGR of 4.7% from 2026 to 2033

Actual data

2021 - 2025

Forecast period

2026 - 2033

Quantitative units

Revenue in USD billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company share, competitive landscape, growth factors, and trends

Segments covered

Type, technology, end-use, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; UK; Germany; France; China; India; Japan; Australia; South Korea; Brazil; UAE; Saudi Arabia; South Africa

Key companies profiled

AAC Technologies; Ampleon; Broadcom; Murata Manufacturing Co., Ltd.; Panasonic Industry Co., Ltd.; Qorvo, Inc.; Qualcomm Technologies, Inc.; RFHIC Corporation; RichWave Technology Corporation; Samsung Electronics Co., Ltd.; Spirox Corporation; Taiyo Yuden Co., Ltd.; TDK Corporation; United Microelectronics Corporation; Walsin Technologies Corporation

Customization scope

Free report customization (equivalent to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global RF Front End Module Market Report Segmentation

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the RF front end module market report based on type, technology, end-use, and region:

-

Type Outlook (Revenue, USD Billion, 2021 - 2033)

-

Power Amplifier (PA)

-

Low-Noise Amplifier

-

Filters

-

Switches

-

Others

-

-

Technology Outlook (Revenue, USD Billion, 2021 - 2033)

-

Wifi

-

Bluetooth

-

-

End-use Outlook (Revenue, USD Billion, 2021 - 2033)

-

Smart Phones & Consumer Electronics

-

Automotive

-

Industrial

-

IT & Telecom

-

Others

-

-

Regional Outlook (Revenue, USD Billion, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

France

-

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

Australia

-

-

Latin America

-

Brazil

-

-

Middle East & Africa

-

UAE

-

Saudi Arabia

-

South Africa

-

-

Frequently Asked Questions About This Report

The global RF front end module market size was valued at USD 53.0 billion in 2025 and is estimated at USD 55.1 billion for 2026.

The global RF front end module market is expected to grow at a CAGR of 4.7% from 2026 to 2033, reaching USD 76.0 billion.

The filters segment led with a 37.5% revenue share in 2025.

Factors such as the accelerating shift toward 6G and increasing trend of multi-function wearable devices, which combine health tracking, mobile payments, music playback, and location services are the key factors driving the market growth.

The Bluetooth technology held the largest share (over 66.6%) in 2025, while Wi-Fi is the fastest-growing segment.

The smartphones & consumer electronics segment led with a 65.8% revenue share in 2025, while IT & telecom is the fastest-growing area.

The Asia Pacific region dominated with a 44.3% revenue share in 2025.

Key players include AAC Technologies; Ampleon; Broadcom; Murata Manufacturing Co., Ltd.; Panasonic Industry Co., Ltd.; Qorvo, Inc.; Qualcomm Technologies, Inc.; RFHIC Corporation; RichWave Technology Corporation; Samsung Electronics Co., Ltd.; Spirox Corporation; Taiyo Yuden Co., Ltd.; TDK Corporation; United Microelectronics Corporation; Walsin Technologies Corporation.

About the Author(s)

Semiconductors Research Team

Semiconductors & Electronics · SemiconductorsThis report was authored by the semiconductors research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the semiconductors segment of the semiconductors & electronics industry. All findings are based on proprietary semiconductors & electronics databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.