- Home

- »

- IT Services & Applications

- »

-

Data Center Processor Market Size And Share Report, 2033GVR Report cover

![Data Center Processor Market Size, Share & Trends Report]()

Data Center Processor Market (2026 - 2033) Size, Share & Trends Analysis Report By Processor Type (Central Processing Unit, Graphics Processing Unit), By Data Center Type (Hyperscale Data Centers, Colocation Data Centers), By Deployment, By Application, By End Use, By Region, And Segment Forecasts

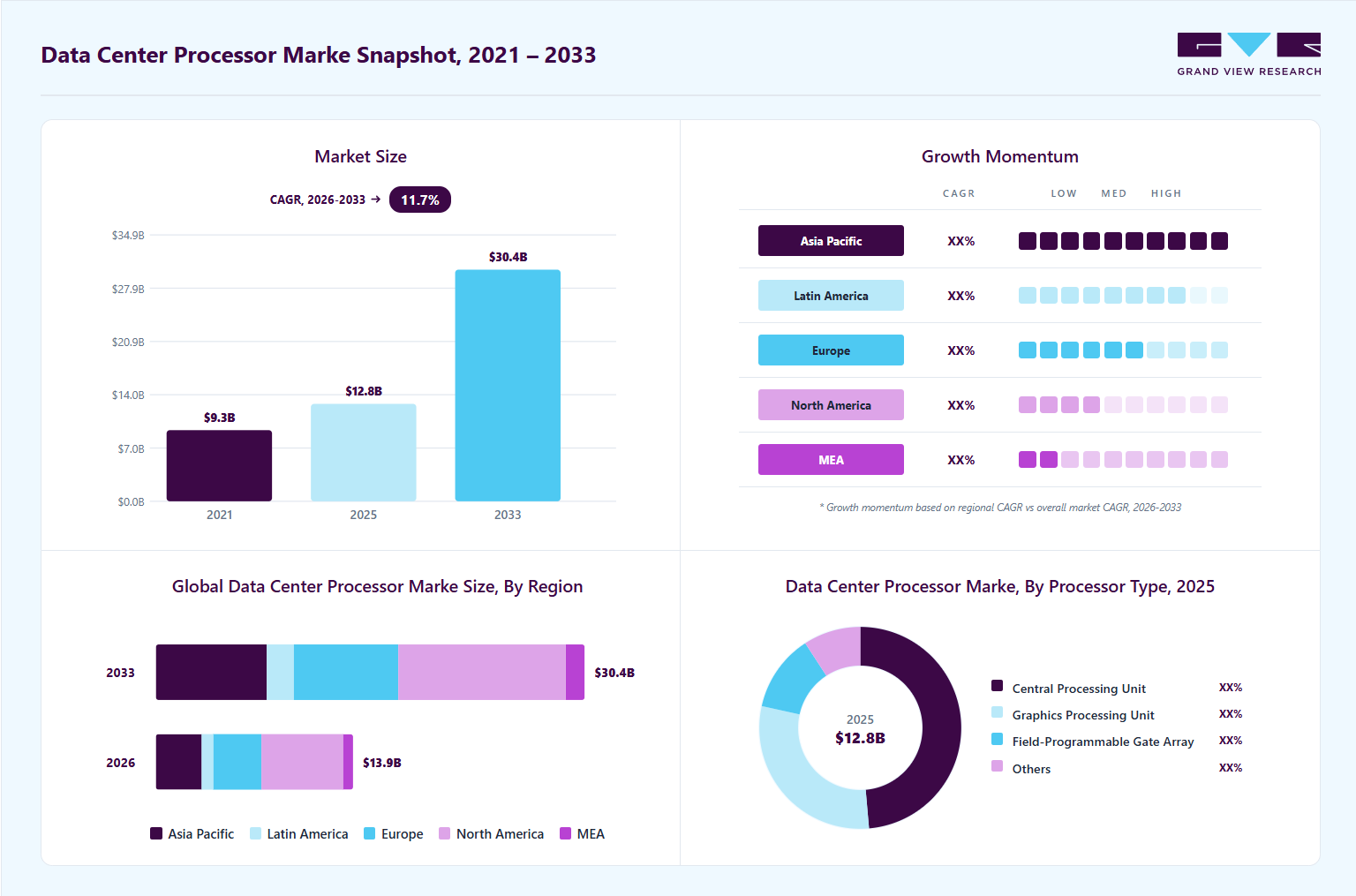

Market Size, 2025

$12.8BMarket Estimate, 2026

$14.0BMarket Forecast, 2033

$30.4BCAGR, 2026–2033

11.7%Data Center Processor Market Summary

The global data center processor market size was estimated at USD 12.8 billion in 2025 and is projected to grow from USD 14.0 billion in 2026 to USD 30.4 billion by 2033, at a CAGR of 11.7% from 2026 to 2033. North America held over 41.0% revenue share of the data center processor market in 2025. The market is experiencing strong growth driven by the rapid expansion of cloud computing, increasing adoption of artificial intelligence (AI) and machine learning (ML), rising data generation across industries, and growing demand for high-performance and energy-efficient computing infrastructure.

Key Market Trends & Insights

- By processor type: Central processing unit segment held the largest revenue share of over 48.0% in 2025.

- By data center type: Hyperscale data centers segment dominated the data center processor industry in 2025

- By application: Artificial intelligence & machine learning segment dominated the data center processor industry in 2025.

- By end-use: Retail & e-commerce segment is anticipated to register the fastest CAGR during the forecast period.

- By deployment: Cloud-based segment dominated the data center processor market in 2025.

Regional Highlights

- Largest regional market: North America (41.0% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

- The U.S. data center processor industry is growing due to the rapid expansion of hyperscale data centers driven by major cloud service providers, which is significantly increasing demand for high-performance processors across the country.

Market Size & Forecast

- Market size in 2025: USD 12.8 Billion

- Estimated market size in 2026: USD 14.0 Billion

- Projected market size by 2033: USD 30.4 Billion

- CAGR (2026-2033): 11.7%

The market is experiencing strong growth driven by the rapid expansion of cloud computing, increasing adoption of artificial intelligence (AI) and machine learning (ML), rising data generation across industries, and growing demand for high-performance and energy-efficient computing infrastructure. The accelerating adoption of AI and ML workloads across industries is one of the key drivers of the data center processor market. Enterprises are increasingly deploying advanced analytics, automation tools, and generative AI models, all of which require high computational power. This has significantly increased demand for high-performance processors, particularly GPUs and specialized accelerators, as traditional CPUs alone are not sufficient to meet parallel processing requirements. As organizations continue to integrate AI into core business operations, the need for advanced data center processors is expected to rise further.")

The rapid growth of cloud computing is another major factor supporting market expansion. Cloud service providers are continuously scaling their infrastructure to meet increasing demand for digital services, storage, and computing power. Hyperscale data centers are expanding globally, requiring large volumes of processors to support virtualization, containerization, and distributed workloads. This trend is further supported by the shift of enterprises from on-premises infrastructure to cloud-based and hybrid environments, driving consistent demand for next-generation processors.

The exponential increase in data generation is also contributing significantly to market growth. With the widespread adoption of IoT devices, digital platforms, streaming services, and online transactions, organizations are generating and processing vast amounts of data. This has increased the need for efficient data processing, real-time analytics, and storage optimization, thereby increasing demand for advanced processors capable of handling high data throughput with low latency.

Furthermore, the growing demand for high-performance computing (HPC) across sectors such as scientific research, healthcare, financial services, and government is accelerating processor adoption. Applications such as weather forecasting, genomic analysis, risk modeling, and simulation require powerful computing systems supported by advanced processors. As industries increasingly rely on data-driven decision-making and complex simulations, investment in high-performance data center infrastructure continues to grow. According to the U.S. Department of Energy, in November 2025, a USD 625 million funding initiative was announced to advance the next phase of national quantum information science. It highlights continued government investment in advanced computing technologies, which indirectly drives demand for high-performance processors in data centers.

In addition, the market is benefiting from ongoing advancements in processor technologies focused on performance optimization and energy efficiency. Manufacturers are developing processors with higher core counts, improved architectures, and better power management capabilities to address rising energy consumption concerns in data centers. Meanwhile, the emergence of custom silicon and application-specific processors is enabling organizations to optimize workloads more effectively. These technological developments are expected to play a crucial role in sustaining long-term market growth.

Market Dynamics

The expansion of hyperscale data centers is a major driver of the data center processor industry, as leading cloud providers continue to build large-scale facilities to support artificial intelligence, machine learning, cloud computing, and data analytics workloads. These hyperscale campuses contain tens of thousands of servers and require high-performance CPUs, GPUs, and custom accelerators to deliver the computing power needed for increasingly complex applications. As enterprises and consumers generate more data and adopt AI-driven services, cloud providers are significantly increasing infrastructure investments, which directly increases demand for advanced data center processors with higher core counts, greater memory bandwidth, and improved energy efficiency.

For instance, in June 2025, Amazon Web Services, Inc. announced plans to invest approximately USD 20 billion to establish new cloud and AI innovation campuses in Pennsylvania, marking the largest private-sector investment in the state's history. The project includes the development of advanced data center infrastructure designed to support generative AI and next-generation cloud services. Such large-scale investments highlight the accelerating expansion of hyperscale data centers and demonstrate how new facility construction translates into substantial procurement of server processors and AI accelerators, thereby driving growth in the global data center processor market.

Export controls and geopolitical restrictions represent a significant restraint for the data center processor industry, as governments increasingly regulate the transfer of advanced semiconductor technologies for national security and strategic reasons. High-performance CPUs, GPUs, and AI accelerators are often subject to licensing requirements and performance thresholds that restrict shipments to specific countries and organizations. These measures can reduce the addressable market for processor vendors, disrupt established customer relationships, and create uncertainty in long-term sales planning. In addition, trade tensions and sanctions may compel companies to redesign products, modify supply chains, and allocate additional resources to compliance and legal oversight.

These restrictions also accelerate market fragmentation by prompting affected countries to invest in domestic semiconductor development and alternative technology ecosystems. Processor manufacturers may face delayed orders, reduced revenue opportunities, and increased operational complexity as they navigate changing regulatory frameworks across multiple jurisdictions. For data center operators, geopolitical uncertainty can limit access to the latest processors and delay infrastructure expansion plans. As a result, export controls and geopolitical tensions continue to constrain the global growth of the data center processor market by restricting international trade, increasing compliance costs, and reshaping competitive dynamics.

The expansion of sovereign AI and national supercomputing initiatives represents a significant opportunity for the data center processor market, as governments around the world are investing in domestic computing infrastructure to strengthen technological independence, national security, and innovation capacity. These initiatives involve the deployment of high-performance computing (HPC) clusters and AI supercomputers that require large number of advanced CPUs, GPUs, and specialized accelerators. Public-sector investments in sovereign compute infrastructure also support research institutions, startups, and strategic industries, creating long-term demand for cutting-edge processors and associated system technologies.

For instance, in April 2026, the Government of India highlighted that its IndiaAI Mission, with an outlay of USD 1,112.4 million, had onboarded more than 38,000 GPUs to provide affordable AI compute capacity to startups and academic institutions across the country. This initiative is designed to build domestic AI capabilities and reduce reliance on foreign infrastructure, directly increasing demand for high-performance processors used in AI training and inference workloads. Similar programs are being implemented globally, including the UK’s Sovereign AI Unit and National Supercomputing initiatives, supporting the role of government-backed computing infrastructure as a major growth opportunity for the data center processor industry.

Market Concentration & Characteristics

The data center processor market is concentrated because a small number of companies control the design and supply of high-performance CPUs, GPUs, and specialized accelerators used in servers. Developing competitive processors requires multibillion-dollar investments in architecture design, software ecosystems, and access to advanced semiconductor manufacturing. These high entry barriers significantly limit the number of viable competitors. In addition, long qualification cycles and the need for reliability, security, and compatibility encourage customers to rely on established suppliers, supporting the concentrated structure of the market.

The data center processor industry exhibits a very high degree of innovation, driven by the explosive growth of artificial intelligence, cloud computing, and high-performance computing. Vendors are introducing new architectures based on chiplet designs, advanced packaging, high-bandwidth memory, and energy-efficient cores to improve performance and reduce power consumption. Continuous innovation in AI accelerators, domain-specific processors, and custom silicon developed by hyperscale cloud providers is transforming data center infrastructure and making technological leadership a critical competitive differentiator in this market.

Processor Type Insights

The central processing unit (CPU) segment accounted for the largest revenue share of over 48.0% in 2025 in the data center processor market. The dominance of CPUs is primarily driven by their critical role in handling general-purpose computing, virtualization, database management, and enterprise workloads across data centers. CPUs remain the backbone of server infrastructure, supporting a wide range of applications that require sequential processing and system control functions. Their widespread adoption in cloud computing, enterprise IT environments, and hybrid deployments continues to sustain strong demand. In addition, ongoing improvements in multi-core architectures, performance efficiency, and workload optimization are further enhancing CPU capabilities. The continued reliance on CPUs for core computing tasks ensures their leading position in the market despite the rising adoption of specialized processors.

The field-programmable gate array segment is anticipated to grow at the fastest CAGR during the forecast period. This growth is primarily driven by the increasing demand for flexible and reconfigurable processing solutions in data centers, particularly for AI inference, networking, and real-time data processing workloads. FPGAs offer the advantage of being programmable after manufacturing, enabling data center operators to customize hardware for specific applications, thereby improving performance and reducing latency compared to traditional processors. The rising adoption of edge computing, 5G infrastructure, and data-intensive applications is further accelerating demand for FPGA-based acceleration. In addition, growing integration of FPGAs in cloud platforms for workload optimization and energy-efficient processing is supporting segment expansion, as organizations seek adaptable and cost-effective solutions to handle evolving computational requirements.

Data Center Type Insights

The hyperscale data centers segment dominated the data center processor industry in 2025. This dominance is primarily driven by the rapid expansion of large-scale cloud service providers and increasing deployment of AI and data-intensive workloads, which require massive computing capacity supported by high-performance processors. Hyperscale facilities are designed to handle large volumes of data processing, storage, and networking, making them the primary consumers of advanced CPUs, GPUs, and accelerators. Their ability to scale infrastructure efficiently and support distributed computing environments continues to drive processor demand. In addition, strong investments in hyperscale infrastructure across major markets further reinforce segment growth.

The colocation data centers segment is expected to register a significant CAGR from 2026 to 2033. The growth of this segment is driven by increasing enterprise preference for outsourcing data center infrastructure to reduce capital expenditure, improve scalability, and access high-performance computing environments. Colocation providers offer flexible, cost-effective solutions with advanced connectivity, security, and power management, making them attractive for businesses transitioning to hybrid and cloud-based models. The rising adoption of AI, cloud services, and digital transformation initiatives is further accelerating demand for colocation facilities.

Deployment Insights

The cloud-based segment dominated the data center processor market in 2025. This dominance is primarily driven by the widespread adoption of cloud computing across enterprises seeking scalable, flexible, and cost-efficient IT infrastructure. Cloud platforms support a wide range of workloads, including data storage, application hosting, AI processing, and analytics, all of which require high-performance processors. The continuous expansion of hyperscale data centers and increasing reliance on virtualization and containerization technologies further contribute to strong processor demand in cloud environments. In addition, organizations are increasingly migrating from on-premises systems to cloud platforms to enhance operational efficiency and support digital transformation initiatives, reinforcing the segment’s leading position in the market.

The hybrid segment is expected to register the fastest CAGR from 2026 to 2033. The growth of hybrid deployment models is driven by the need for flexibility, allowing organizations to balance workloads between on-premises infrastructure and cloud environments. Enterprises are adopting hybrid strategies to optimize performance, manage sensitive data securely, and comply with regulatory requirements while still leveraging the scalability of the cloud. This approach increases demand for advanced processors capable of supporting seamless workload integration, data transfer, and real-time processing across environments. Furthermore, the rising complexity of IT operations and the growing need for efficient resource utilization are encouraging organizations to invest in hybrid infrastructure, thereby accelerating processor adoption in this segment.

Application Insights

The artificial intelligence & machine learning segment dominated the data center processor industry in 2025. This dominance is driven by the rapid adoption of AI-driven applications across industries, including automation, predictive analytics, natural language processing, and computer vision. These workloads require high computational power and parallel processing capabilities, significantly increasing demand for advanced processors such as GPUs and AI accelerators. Enterprises and cloud providers are heavily investing in AI infrastructure to support large-scale model training and real-time inference, further boosting processor demand. In addition, the growing integration of AI into core business operations and digital platforms continues to reinforce the segment’s leading position in the market.

The high-performance computing (HPC) segment is expected to register the fastest CAGR from 2026 to 2033. The growth of this segment is primarily driven by increasing demand for advanced computing capabilities in scientific research, weather forecasting, financial modeling, and complex simulations. HPC workloads require powerful processors with high core counts and superior processing speeds to handle large-scale computations efficiently. Governments and research institutions are making significant investments in supercomputing infrastructure to support innovation and national security initiatives, which is expected to drive strong demand for high-performance processors, accelerating growth in the HPC segment.

End Use Insights

The IT & telecom segment accounted for the largest market share of the data center processor market in 2025. This dominance is primarily driven by the continuous expansion of telecom networks, cloud infrastructure, and data traffic across global markets. The increasing deployment of 5G networks, rising internet penetration, and growing demand for digital services are significantly increasing the need for high-performance data processing capabilities. IT and telecom companies operate large-scale data centers to support applications such as network management, real-time communication, and cloud-based services, all of which require advanced processors. In addition, the rapid growth of data consumption and the need for low-latency processing are further driving investments in data center infrastructure, thereby supporting strong demand for processors in this segment.

The retail & e-commerce segment is anticipated to register the fastest CAGR during the forecast period. The growth of this segment is driven by the rapid expansion of online shopping platforms, increasing digital transactions, and rising adoption of data-driven customer engagement strategies. Retailers are leveraging advanced analytics, recommendation engines, and AI-driven personalization to enhance customer experience, which requires high-performance data processing capabilities. In addition, the growing need for real-time inventory management, supply chain optimization, and secure payment processing is further increasing demand for advanced processors in data centers. The continued shift toward omnichannel retailing and the integration of digital technologies are expected to significantly accelerate processor adoption in this segment.

Regional Insights

North America Data Center Processor Market Trends

The data center processor industry in North America accounted for the largest market share of over 41.0% in 2025. This dominance is primarily driven by the strong presence of hyperscale cloud providers, advanced digital infrastructure, and rapid adoption of artificial intelligence and high-performance computing technologies across North America. The increasing demand for cloud services, large-scale data processing, and AI workloads has led to the continuous expansion of data center infrastructure, thereby boosting demand for advanced processors. In addition, supportive government initiatives and investments aimed at strengthening digital and AI infrastructure are further accelerating market growth. For instance, in July 2025, according to the White House, a 2025 executive order was introduced to accelerate federal permitting of data center infrastructure, aimed at enabling faster and more efficient development of large-scale data centers, thereby supporting processor demand across North America.

U.S. Data Center Processor Market Trends

Data center processor industry in the U.S. is projected to grow significantly during the forecast period. This growth is driven by the country’s leadership in cloud computing, strong presence of major technology companies, and rapid adoption of AI-driven applications across industries. The U.S. hosts a large number of hyperscale data centers, creating substantial demand for high-performance processors to support advanced workloads such as AI training, real-time analytics, and large-scale data processing. Furthermore, increasing investments in digital infrastructure and energy systems to support data center operations are contributing to market expansion.

Asia Pacific Data Center Processor Market Trends

The Asia Pacific data center processor industry is expected to grow at the fastest CAGR from 2026 to 2033. This growth is primarily driven by rapid digital transformation across emerging economies, increasing adoption of cloud computing and AI technologies, and strong expansion of hyperscale data center infrastructure in countries such as China, India, and Japan. The region is witnessing significant growth in internet users, e-commerce activity, and mobile data consumption, which is accelerating demand for high-performance data processing capabilities. In addition, favorable government initiatives supporting digital infrastructure development, smart cities, and data localization policies are further increasing the Asia Pacific data center processor market growth.

Data center processor market in China is projected to grow steadily during the forecast period. This growth is driven by the country’s strong focus on digital economy development, increasing investments in data center infrastructure, and rapid adoption of cloud computing and artificial intelligence technologies. China has established itself as a major hub for data center expansion, supported by large-scale government-backed initiatives aimed at strengthening computing capabilities and digital infrastructure. In addition, the presence of domestic technology companies and the rising demand for data-intensive applications are further accelerating processor adoption.

Europe Data Center Processor Market Trends

The data center processor industry in Europe is experiencing steady growth, supported by strong regulatory frameworks around data protection, increasing focus on digital sovereignty, and rising investments in sustainable and energy-efficient data center infrastructure. The region is witnessing growing demand for processors driven by enterprise modernization, expansion of edge computing, and increasing adoption of secure data processing environments across industries. In addition, Europe’s focus on green data centers and carbon neutrality is encouraging the deployment of energy-efficient processors and advanced cooling technologies.

The UK data center processor market is projected to grow significantly during the forecast period. This growth is driven by increasing investments in digital infrastructure, rising demand for data localization, and the country’s position as a key hub for financial services and digital innovation. The expansion of edge computing and the growing adoption of cloud-native applications across enterprises are further contributing to processor demand. In addition, the UK’s strong focus on building a resilient and secure digital economy is encouraging upgrades to advanced computing infrastructure. For instance, in March 2026, according to the UK Government, over USD 2.87 billion has been committed under the National AI Strategy to support AI development and infrastructure, reinforcing demand for high-performance processors across data centers.

Key Data Center Processor Companies & Market Share Insights

Some prominent players in the data center processor market include Intel Corporation, Advanced Micro Devices, Inc., NVIDIA Corporation, Arm Limited, Broadcom, among others.

-

NVIDIA Corporation is a global technology company specializing in accelerated computing and is widely recognized in AI-driven data center processors. The company designs and manufactures advanced data center GPUs, CPUs, and data processing units (DPUs) that power modern cloud, AI, and high-performance computing environments. NVIDIA’s core offering is its GPU-based accelerated computing platform. Its processors are widely deployed across hyperscale data centers, enterprises, and supercomputing facilities. NVIDIA’s strong presence in data center processors is driven by its ability to deliver high-performance, energy-efficient solutions tailored for large-scale, data-intensive workloads.

-

Intel Corporation is a global company in semiconductor design and manufacturing, primarily known for developing advanced computing processors and data center technologies. The company offers a broad portfolio of data center solutions, including Intel Xeon CPUs, data center GPUs, and AI accelerators, which are widely used across cloud, enterprise, and high-performance computing environments. The company has a strong global presence, supplying processors to hyperscale cloud providers, enterprises, and government organizations, and continues to expand its role in next-generation computing through innovations in AI infrastructure and energy-efficient architectures.

Key Data Center Processor Companies

The following key companies have been profiled for this study on the data center processor market.

-

Advanced Micro Devices, Inc.

-

Alibaba Cloud

-

Ampere Computing LLC.

-

Arm Limited

-

Broadcom

-

Fujitsu

-

Google

-

Huawei Technologies Co., Ltd.

-

IBM Corporation

-

Intel Corporation

-

Marvell

-

Microsoft Corporation

-

NVIDIA Corporation

-

Qualcomm Technologies, Inc.

-

SAMSUNG

Competitive Benchmarking

Operating Strategies

Competitive Edge

Weakness

Mature Players: Intel Corporation; NVIDIA Corporation; Advanced Micro Devices, Inc.; Arm Limited; Broadcom; IBM Corporation; Google; Microsoft Corporation; Alibaba Cloud

- Invest heavily in advanced processor architectures, AI accelerators, chiplet designs, and software ecosystems.

- Collaborate with hyperscale cloud providers and OEMs to deploy processors at scale.

- Strengthen market presence through strategic partnerships, acquisitions, and long-term manufacturing agreements.

- Strong global brand recognition and deep customer relationships with hyperscalers and enterprises.

- Extensive R&D budgets and access to advanced semiconductor manufacturing technologies.

- Broad product portfolios spanning CPUs, GPUs, NPUs, networking, and custom accelerators.

- Exposure to supply chain constraints and foundry capacity limitations.

- Export controls and geopolitical restrictions can limit addressable markets.

- Dependence on a limited number of advanced manufacturing partners.

Emerging Players: Ampere Computing LLC.; Marvell; Qualcomm Technologies, Inc.; Fujitsu; Huawei Technologies Co., Ltd.; Samsung

- Focus on ARM-based server processors, custom accelerators, and energy-efficient architectures.

- Partner with cloud providers, ODMs, and software vendors to build ecosystem support.

- Expand through pilot deployments and strategic regional initiatives.

- Greater agility in adopting new architectures and targeting niche workload requirements.

- Increasing adoption in sovereign AI, regional cloud, and edge computing projects.

- Flexible business models and focused innovation strategies.

- Limited market share and smaller installed bases compared with established leaders.

- Less mature software ecosystems and compatibility support in some workloads.

- Lower financial resources for sustained large-scale R&D investments.

Recent Developments

-

In March 2026, Samsung Electronics announced an expanded strategic collaboration with Advanced Micro Devices to develop next-generation AI memory and computing solutions, including HBM4 memory for AMD Instinct GPUs and advanced DDR5 memory for upcoming EPYC CPUs, aimed at enhancing performance and efficiency in data center and AI infrastructure.

-

In February 2025, Intel Corporation launched its Intel Xeon 6 processors, designed to deliver high performance for data center workloads, including up to twice the performance for AI applications. These processors are also optimized for network and edge use cases and include Intel vRAN Boost, which can increase capacity by up to 2.4 times for radio access network (RAN) operations.

-

In March 2026, NVIDIA introduced the Vera CPU, designed specifically for agentic AI and reinforcement learning workloads. The processor offers up to 50% higher performance and around double the energy efficiency compared to conventional rack-scale CPUs.

Data Center Processor Market Report Scope

Report Attribute

Details

Market size value in 2026

USD 14.0 billion

Revenue forecast in 2033

USD 30.4 billion

Growth rate

CAGR of 11.7% from 2026 to 2033

Actual data

2021 - 2025

Forecast period

2026 - 2033

Quantitative units

Revenue in USD billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company share, competitive landscape, growth factors, and trends

Segments covered

Processor type, data center type, deployment, application, end use, region

Regional scope

North America, Europe, Asia Pacific, Latin America, MEA

Country scope

U.S., Canada, Mexico, UK, Germany, France, China, India, Japan, Australia, South Korea, Brazil, UAE, Saudi Arabia, South Africa

Key companies profiled

Advanced Micro Devices, Inc.; Alibaba Cloud; Ampere Computing LLC.; Arm Limited; Broadcom; Fujitsu; Google; Huawei Technologies Co., Ltd.; IBM Corporation; Intel Corporation; Marvell; Microsoft Corporation; NVIDIA Corporation; Qualcomm Technologies, Inc.; SAMSUNG

Customization scope

Free report customization (equivalent to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Data Center Processor Market Report Segmentation

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global data center processor market report based on processor type, data center type, deployment, application, end use, and region.

-

Processor Type Outlook (Revenue, USD Million, 2021 - 2033)

-

Central Processing Unit

-

Graphics Processing Unit

-

Field-Programmable Gate Array

-

Others

-

-

Data Center Type Outlook (Revenue, USD Million, 2021 - 2033)

-

Hyperscale Data Centers

-

Colocation Data Centers

-

Enterprise Data Centers

-

-

Deployment Outlook (Revenue, USD Million, 2021 - 2033)

-

Cloud-Based

-

On-Premises

-

Hybrid

-

-

Application Outlook (Revenue, USD Million, 2021 - 2033)

-

Artificial Intelligence & Machine Learning

-

Cloud Computing

-

Big Data Analytics

-

High-Performance Computing (HPC)

-

Content Delivery & Streaming

-

Database Management

-

Others

-

-

End Use Outlook (Revenue, USD Million, 2021 - 2033)

-

BFSI

-

Government & Defense

-

Healthcare

-

IT & Telecom

-

Retail & E-commerce

-

Media & Entertainment

-

Others

-

-

Regional Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

France

-

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

Australia

-

-

Latin America

-

Brazil

-

-

Middle East & Africa

-

UAE

-

Saudi Arabia

-

South Africa

-

-

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

Regional regulatory and trade environment analysis for advanced processors

Assessment of export controls, localization policies, semiconductor incentives, and compliance requirements across major regions.

Review of policy developments affecting supply chains and market access.

Analysis of implications for processor vendors and data center operators.

Supported risk assessment and market entry planning.

Identified regulatory challenges and mitigation strategies.

Improved understanding of geopolitical impacts on demand.

Analysis of data center processor demand by cooling architecture

Assessment of processor adoption across air-cooled, direct-to-chip liquid-cooled, and immersion-cooled data center environments.

Review of processor power density requirements and infrastructure compatibility considerations.

Analysis of vendor strategies for supporting high-thermal-design-power (TDP) processors.

Identified processor categories best suited for next-generation cooling systems.

Supported infrastructure planning and product positioning.

Highlighted opportunities in high-density AI deployments.

Assessment of opportunities in sovereign AI and public-sector computing projects

Review of government-led AI infrastructure, supercomputing, and digital sovereignty initiatives across major regions.

Analysis of procurement priorities, localization requirements, and preferred deployment models.

Mapping of processor vendors positioned to participate in these projects.

Identified public-sector growth opportunities.

Supported strategic targeting of government and research customers.

Highlighted compliance and partnership considerations.

Frequently Asked Questions About This Report

North America dominated with a 38.0% revenue share in 2025.

Asia Pacific is the fastest-growing region over the forecast period.

Hyperscale data centers segment dominated the data center processor industry in 2025.

Artificial intelligence & machine learning segment led the data center processor industry in 2025.

The global data center processor market size was valued at USD 12.8 billion in 2025 and is estimated at USD 14.0 billion for 2026.

The global data center processor market is expected to grow at a CAGR of 11.7% from 2026 to 2033, reaching USD 30.4 billion.

The central processing unit (CPU) segment led with a 48.0% revenue share in 2025, while field-programmable gate array segment is the fastest-growing segment.

Some key players operating in the market Advanced Micro Devices, Inc.; Alibaba Cloud; Ampere Computing LLC.; Arm Limited; Broadcom; Fujitsu; Google; Huawei Technologies Co., Ltd.; IBM Corporation; Intel Corporation; Marvell; Microsoft Corporation; NVIDIA Corporation; Qualcomm Technologies, Inc.; SAMSUNG and Others.

Factors such as the growing demand for hyperscale and colocation data centers, increasing adoption of artificial intelligence and high-performance computing workloads, and rising investments in cloud infrastructure modernization play a key role in accelerating the data center processor market.

About the Author(s)

IT Services & Applications Research Team

Technology · IT Services & ApplicationsThis report was authored by the it services & applications research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the it services & applications segment of the technology industry. All findings are based on proprietary technology databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.